Arete's Observations 10/2/20

Market observations

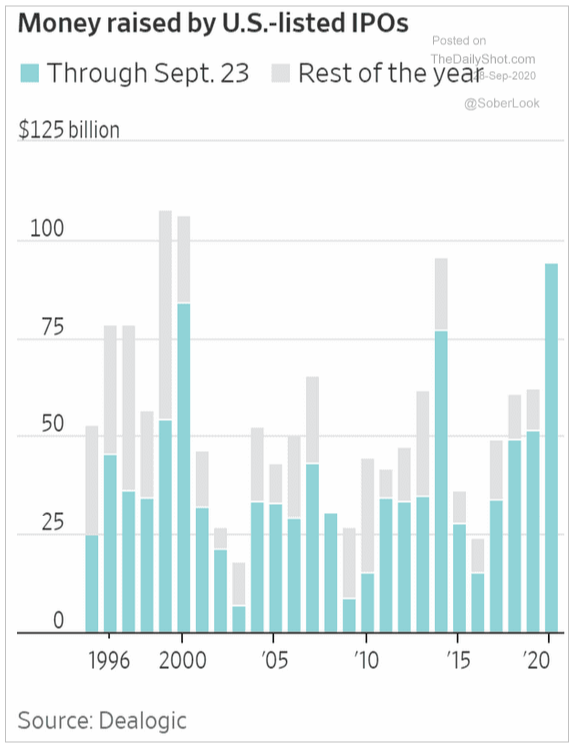

One of the bigger stories of the last few years has been the volume of corporate share repurchases. The story was big partly because of the massive volumes and partly because much of the repurchase activity was price insensitive. As I reported in a blog post from a couple of years ago, "[share] repurchases remain the largest source of demand for shares."

I also discussed how that source of demand could erode if cash flows do not continue increasing. Indeed, after weak economic progress last year, share repurchases declined from 2018. Further, after the significant impact from Covid lockdowns this year, share repurchase activity is materially lower than in 2019.

This raises an important question: Where is the incremental demand to buy shares coming from? If companies are not repurchasing shares at anywhere near the same rate, who is coming in to fill the gap and keep bidding prices up? Perhaps an even better question is: Will that new incremental buyer hang around if/when stocks fall and momentum turns down?

To be fair, repurchases are only part of the equation. Two years ago, when I wrote the post, IPO activity was low but has increased significantly recently. While still small relative to repurchases, IPOs do make up some of the deficit.

The bigger issue for me is that declining cash flows, significantly falling share repurchases, and an economy beset by a pandemic is not exactly the script I would write for near-record stock prices. Yet here we are.

Economy

Harvard’s Chetty Finds Economic Carnage in Wealthiest ZIP Codes

“’Americans have deluded ourselves for years that we are a meritocracy.’ Now they’re waking up to the often-insurmountable barriers to equal opportunity Chetty has spent his career identifying.”

“A scenario in which Covid is never corralled the way it has been in some countries in Europe and Asia haunts Chetty. ‘It’s not going to be a sustained recovery. There’s just no way,’ he says. ‘We’re going to be stuck trying to go along and accept a fair number of Covid infections and deaths and muddle our way through until finally there’s a vaccine’.”

I realize I’ve been including a number of pieces on inequality lately, so I was somewhat hesitant to include this one. I went ahead partly because inequality is an important economic, political, and moral topic. I also went ahead because Raj Chetty’s work is at once illuminating, instructive, and inspirational.

The work is illuminating because it shows how we have deluded ourselves that America is a meritocracy. Dig into all the details and that thesis is clearly refuted. It is instructive because it shows in exacting detail where the problems are and how they can vary by region or even neighborhood. One phenomenon it reveals is that there is not going to be a sustained recovery.

Finally, the work is inspirational because these are exactly the types of things we ought to be doing with lots of data and powerful processing capabilities (check it out yourself at opportunityinsights.org). We don’t have to guess at what is going on. We don’t have to settle for overly simplistic narratives. We can use these tools to solve difficult problems. Chetty provides a terrific role model for other researchers and public policy experts. Hopefully, we can make good use of it.

Management

The delight is in the detail

https://www.economist.com/business/2020/09/12/management-lessons-from-honeywells-former-ceo

“Mr Cote was fed up with junior managers declaring that they could not find suitable candidates in their area. So he had his team break down the population statistics in places where his factories were located to demonstrate that there should be many opportunities to hire workers from different backgrounds. Diversity duly improved.”

The Economist published a nice blurb on the new book by David Cote, the former CEO of Honeywell, called "Winning Now, Winning Later". The example above represents the kind of common sense and independent judgment that can seem almost trivial in hindsight but can also be incredibly effective in the moment when managing a team.

Don’t Blame the Pipeline for Your White Male Workforce

“’While it might sound like an excuse, the unfortunate reality is that there is a very limited pool of Black talent to recruit from’, Scharf said in a memo.”

These comments from Charles Scharf, the CEO of Wells Fargo, raised some hackles but are all-too common among senior business leaders. The unfortunate reality is that they are excuses and reflect lack of imagination and lack of real effort. It sounds like Mr. Scharf can learn a few things about management from David Cote.

Restaurants

Almost Daily Grant’s, 9/25/20

“Bankrupt NPC International, Inc. announced last week that it is seeking $725 million for its portfolio of Wendy’s and Pizza Hut restaurants that it looks to sell off while under court protection. NPC filed for Chapter 11 on July 1, saddled with $903 million in debt (or well more than the hoped-for sales price) thanks to a 2018 leveraged buyout.”

One of the stories that Grant’s has been on top of is the divergence between the fortunes of restaurant owners and the restaurant franchises owned by public companies. The franchisors have been hailed as “asset-light” business models and the stocks have generally done well. The restaurants, however, have been beset by flagging demand and increasing costs. The bankruptcy of NPC reveals that the divergence cannot continue forever and provides a tangible indication of the trajectory of the industry.

It also provides an indication of how the franchisors may ultimately have to contribute their pound of flesh. One of the sticking points of the NPC situation is the franchisee’s prior commitments to make capital improvements. Grant’s asks, “Might the franchisors, who have long collected royalties without direct exposure to a rugged operating environment, end up on the hook for some or much of franchisees’ capital needs?” Good question.

Shipping

Coronavirus and globalisation: the surprising resilience of container shipping

https://www.ft.com/content/65fe4650-5d90-41bc-8025-4ac81df8a5e4

“’Carriers have taught themselves a valuable lesson this year,’ says Lars Jensen, chief executive of SeaIntelligence Consulting. ‘Unless something goes horribly wrong towards the last few months they will come out of 2020 with a much better financial result than last year, despite the disruption’.”

“But so far the industry has demonstrated considerable resilience. The rise in ecommerce has given it a boost.”

Several years ago, I was sitting at a table with the presenter at a CFA Society of Baltimore luncheon and we were talking about value investing. We went back and forth on the most-hated industries we could think of. Shipping was at the top of the list.

Judging by the Baltic Dry index, shipping had some great years from the economic recovery in 2002 right up until the financial crisis in 2008. While it staged a modest recovery after, it was down in the dumps again by 2011. What appeared at the time as a potentially interesting contrarian idea, however, has proven to be unfruitful for all but a few brief periods since then.

The key is supply. The economics of expensive, long-lived assets like container ships is often driven on the margin by supply. When capital is cheap, it is easy for competitors to build and increase supply.

It does appear, however, that some industry consolidation is taking place. If that continues, there could be much lower risk of overbuilding. In addition, ecommerce seems to be providing a steady source of demand. If inflation picks up a bit and capital becomes more expensive, the shipping business could start looking very interesting.

Commercial real estate

Remember 1929 when looking for the cause of the coming financial crisis

https://www.ft.com/content/f9ff9ed0-c7ff-4718-a65b-8be712379e84

“It has not yet been recognised that Ruth Bader Ginsburg’s death significantly raises the likelihood of a US-centric financial crisis this fall.”

“Since the Covid-related economic crisis in March, the trustees for many CMBS bonds backed by troubled properties have allowed FF & E accounts to be used to pay enough principal and interest to avoid having the CMBS collateral from going into default. But that three months of cash has run out in many cases, particularly for hotels and malls. In the first weeks of September, there has been a rapid increase in the number of CMBS going into ‘special servicing’, a sort of formal default.”

As Covid restrictions continue to be lifted it is easy to look forward to something like a return to normal. Feeling the cooler fall weather makes it even easier to envision the change. Unfortunately, John Dizard reminds us that the slow-motion accident that is commercial real estate is not only not getting better but is stumbling toward default in many cases.

This is still early days for the restructuring of commercial real estate, but it has all the makings of the retail and energy sectors which are posting new bankruptcies at a steady pace. One issue is that this will run deep and affect a lot of companies. Another issue is where the debt resides. Banks were the problem children in the financial crisis and I’m sure they will suffer their lumps this time around.

The big difference, however, is that nonbank financial institutions are much more prominent holders of commercial real estate today. That means we will be reading stories about disastrous investment losses at insurance companies, hedge funds, pensions, etc. While these losses won’t create the same systemic risk as in 2008 and 2009, they will be painful for both the owners and the beneficiaries.

China

Grant’s Interest Rate Observer, October 2, 2020

“’Property is the pillar industry of China’s economy,’ Wright and Feng note. ‘These new measures are the most significant restrictions on developers’ funding and growth ever proposed, as they target balance sheet growth directly, rather than financing channels. If enforced strictly, these regulatory limits will have two major economic implications: credit momentum will slow, and construction activity will decline’.”

“Through Oct. 8, you can have an Evergrande condo for 30% off, the steepest discount in company records. It’s a classic example of the kind of debt-induced price deflation that the Federal Reserve seems to want no part of.”

I wrote in a blog post two years ago about the massive risk that Chinese residential real estate posed. The situation had all the markings of the financial crisis in the US twelve years ago. Today, those problems are bubbling up to the surface and property developer Evergrande is the poster child.

Although Evergrande made news because of imminent liquidity concerns, I am less interested about that issue per se. After all, the Chinese government can resolve such problems by diktat if necessary. The more important takeaway is that the emerging seriousness of such issues suggests the limits of credit-fueled growth are being reached.

The effects can manifest in many ways including slower credit growth and deflation in oversupplied industries. And, as I mentioned in the blog, “the slowdown in Chinese economic growth will be felt around the world.”

Politics

Enough said.

Geopolitics

War in the South Caucasus?

https://www.gzeromedia.com/war-in-the-south-caucasus

“The long-simmering conflict between Armenia and Azerbaijan over a region called Nagorno-Karabakh erupted over the weekend, with more than 50 killed (so far) in the fiercest fighting in years. Will it escalate into an all-out war that threatens regional stability and drags in major outside players?”

“A war over the enclave would resonate far beyond the region. The South Caucasus, where Armenia and Azerbaijan are located, has enormous strategic importance because it is crossed by two major energy pipelines that carry Azeri oil and Caspian Sea gas to Turkey and Europe.”

Guess what, Turkey is back in the news again in another regional conflict that has all kinds of geopolitical implications. This time, Russia is on the other side.

As a reminder, the Nagorno-Karabakh region was the site of a six-year war that ended in 1994. The result of that conflict was “over 30,000 dead” and “more than one million displaced”. In other words, this is a tinder box with potential to ugly.

Capital markets

Where there’s a silver tip, there’s a silver tap

https://www.ft.com/content/cc16f0ad-6b02-461e-b674-01a942ba4518

“The great thing about a bank group having an ETF asset on the books, as distinct from metals or commodities contracts, is that there are fewer compliance people worrying about it. And it is easier to gradually unload to retail.”

“Or as a now-retired silver trader reminds us: ‘Silver has always been subject to manipulation’.”

John Dizard is a consistently good read in the FT and this piece about the silver market is representative of his work. One lesson is that precious metals markets have always been manipulated. Those paying attention may have been able to infer this from the weekly/monthly headlines of precious metals traders from major banks being sentenced for nefarious behavior. Dizard makes clear what others gently sidestep. It is what it is – be careful.

He also does a nice job of illuminating a regular banking activity: transforming something undesirable into something attractive and sellable. Describing commodities trade finance as a bank function with “The highest ratio of potential embarrassment to revenue”, Dizard explains why these departments are being reduced or eliminated at several European banks.

That process, however, involves the somewhat tricky proposition of unloading significant excess inventories of silver on a market not in particular need of them. Lo and behold, "It seems much of that silver on hand was converted into ETFs through swaps."

So, to buyers, silver ETFs look like cheap ways to bet on silver if you happen to think the market is short. To sellers, they look like vehicles to offload excess inventory with minimal compliance scrutiny. Voila.

Implications for investment strategy

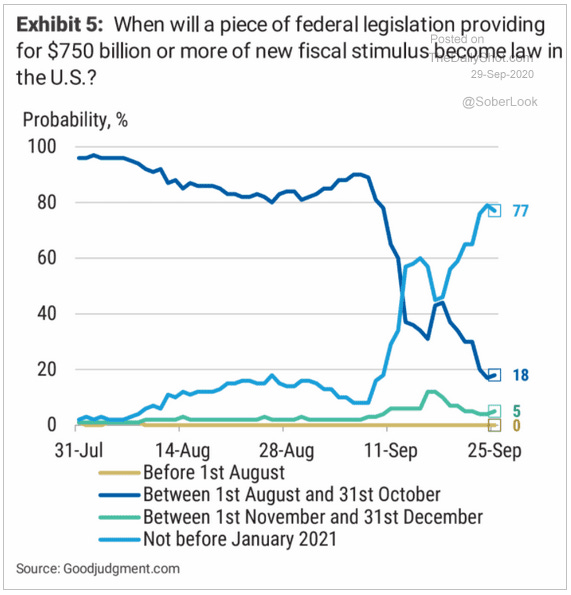

The volatility wake-up call for investors

https://www.ft.com/content/8a563aa6-2304-4cac-9202-72cdc4fb87c7

“Not only are the liquidity injections proving less potent in reliably overcoming a weakening economic recovery and less responsive fiscal policy support, but there are no easy ways to protect portfolios against major sell-offs.”

“It is no longer clear that this is a short-term ‘healthy correction’ that cleanses markets from excessive risk positioning and strengthens the foundation for further gains. More people are concerned that we may have started a more sinister adjustment process that pulls asset prices down closer to what the underlying economic and corporate fundamentals would support.”

Yes, it is hard to treat warnings seriously when we have heard them so many times over the years and they fail to pan out. And yes, that is exactly what investors should do now – treat these warnings seriously.

El-Erian is right that we are reaching the end of monetary policy effectiveness. He is also right that there are no easy ways to protect against selloffs. And, as the graph below shows, he is also right about less responsive fiscal policy support. Although the prospects of fiscal support are bouncing around a lot, it is still best to be careful out there.

“Tree Rings” report by Luke Gromen, 9/25/20

“The question ‘What is the most levered way to play this?’ is likely not the right question to be asking – rather, the right question to be asking is ‘What’s the best unlevered way to play this?’”

“The punchline is this: During one of the greatest hyperinflations in history, gold rose spectacularly … BUT…the volatility in gold was so great that if you owned gold levered in Weimar Germany, you lost all your money as many as five different times … DURING A CURRENCY-KILLING HYPERINFLATION!”

I have advocated for owning gold for a while now for a lot of reasons, not least of which is it can provide an important benefit in both inflationary and deflationary conditions. This note from Luke Gromen addresses a really important point: If gold is such a great investment idea, why not find the most leveraged way possible to invest in it?

The answer is that any leveraged investment is inherently fragile. It is fragile because volatility can wipe out the entire position before the ultimate value is recognized. In addition, the kinds of issues that can cause gold to swing so dramatically are deep-rooted issues that are associated with volatility.

The issue of leverage is also interesting because it represents such an important part of the investment zeitgeist. After such a long period of low rates and suppressed volatility, leverage has become the modus operandi for a wide swath of investment activity. You just can’t earn much with traditional long-only positions. The downside, of course, is that when things break, they break hard.

Principles for Arete’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, Areté’s Takes are designed to show both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.