Arete's Observations 10/30/20

Market observations

One of the more important phenomena I have been tracking is the increasing penetration of passive investing relative to active. This is important because as passive has grown, the passive investor has become the marginal investor – which means they determine stock prices. As long as passive funds keep taking money in, they have to keep investing it. The result is a high degree of price momentum.

An ongoing question is, what could break that momentum? The chart below introduces an interesting possibility. Momentum will be broken when sellers outnumber buyers. Historically, foreign investors have added to their positions in US stocks. While those stocks currently appear to be attractive international assets to foreign investors, they are also valuable, liquid assets that can easily be sold if necessary.

Economy

One of the recurring themes of third quarter conference calls has been the faster than expected recovery in the third quarter from a dismal quarter in the second. The graph below provides an important clue as to why: government largesse in the form of pandemic relief has underwritten consumer spending through the summer.

The graph also shows how dramatically this aid has tailed off in recent months. I see two important implications from this. One is that consumer spending and economic health are now tied inextricably to government aid. As a result of this phenomenon, economic growth is likely to be patchy and inconsistent. Although these do not bode well for long-term growth, they mitigate the chances that any kind of austerity program will put the brakes on growth.

In the Eye of the Storm

https://www.advisorperspectives.com/commentaries/2020/10/28/in-the-eye-of-the-storm

“Do not be mistaken. The relative calm we feel right now isn’t the end of the storm, it is just the eye. The market’s performance and the economy’s recovery is calm compared to the volatility of March and April, but several issues concern me as the eyewall approaches. The possibility of a stimulus package getting passed before the election is remote, despite Federal Reserve (Fed) Chair Powell’s extraordinarily direct call for more fiscal stimulus to avert economic disaster. Without fiscal stimulus, personal income will stagnate, job gains will slow, consumers will pull back, and more small and medium-sized businesses will fail. The economic fallout from lack of fiscal actions increases the likelihood of a negative fourth quarter gross domestic product (GDP) print while Main Street remains in depression.”

Scott Minerd’s comments capture the same concerns but highlight the downside risk: The calm we are experiencing now may be signaling the period that immediately precedes the harshest part of the storm.

Quarterly earnings

3M Reports Third-Quarter 2020 Results

https://s24.q4cdn.com/834031268/files/doc_financials/2020/q3/Q3-2020-Earnings-Press-Release.pdf

“Due to the continued evolving and uncertain impact of the COVID-19 pandemic, 3M is not able to estimate the full duration, magnitude and pace of recovery across its diverse end markets with reasonable accuracy. Therefore, 3M continues to believe it is prudent to not provide guidance.”

3M is one of the most diverse and highest quality companies there is. If they don’t feel comfortable providing guidance at this point, it is a good indication that the business environment remains highly uncertain.

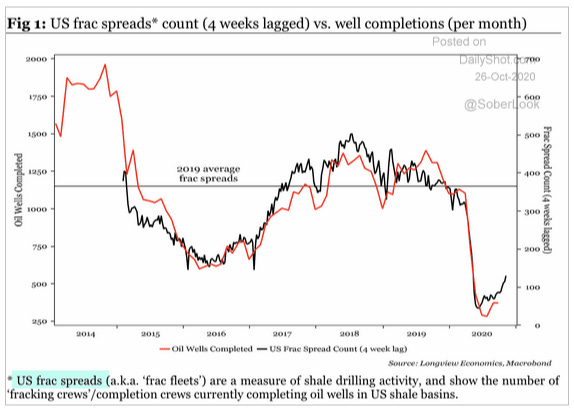

Energy

Oil firms have fallen on tough times. A big break in 2015 caused energy producers to reset expectation for growth and become more efficient. Earlier this year, energy companies suffered two more knocks from pandemic driven demand declines and unleashed supply from Saudi Arabia. Just for good measure, increased efforts to promote ESG standards have also reduced interest in fossil fuels.

A good number of companies have gone bankrupt. Others are consolidating and several big deals have been announced over the last few weeks. It’s virtually impossible for these companies to get capital. As bad as all this is, it is the kind of stuff that causes the ears of contrarian, value-oriented investors to perk up.

Yes, there will be more bankruptcies and there will be more writedowns. However, oil is a critical component of the economy. For all the interest in renewable energy, we can’t get 100% there overnight. Not even close. During the transition from the fossil fuel dominated present to whatever the future holds there will still be a need for oil.

Indeed, with recovering demand but a dearth of capital available to increase supply, the intermediate term prospect for prices is good. In the short-term, there is evidence that a bottom has been reached. That makes companies with existing assets and financial wherewithal interesting ideas.

Commercial real estate

Almost Daily Grant’s, Tuesday, October 27, 2020

https://www.grantspub.com/resources/commentary.cfm

“Lenders are putting the screws to mall owners laid low by the events of 2020, The Wall Street Journal reports today. As nationwide mall valuations have fallen as much as 75% and tenant revenues have slowed to a trickle, time is running out on forbearance and rent breaks, setting the stage for a raft of contentious negotiations and workouts.”

“A report from Green Street Research last Wednesday attempted to quantify the implications of widespread mall vacancies, finding that, within the best-in-class ‘A’ mall category, about one-third of total box locations are not only vacant but are still looking to identify their next occupant.”

This is a useful update from Grant’s as the problems in commercial real estate continue to develop but often fail to break through to headlines in front of the election. With mall valuations down on the order of 75% a lot of balance sheets are going to be affected – from REITs, banks, credit funds, and others. The pain will make its rounds.

The report also suggests the slow-motion nature of retrenchment in commercial real estate. Properties that get turned over to creditors will need to be re-marketed. Existing mall owners are compelled to offer bargains to induce new tenants to fill vacated space while at the same time absorbing higher costs to maintain and/or redevelop property. This too shall pass, but it will take time.

News

Local news is drowning in ‘pink slime’ ahead of US election

https://www.ft.com/content/f36c3e2e-bd62-4d93-853f-0d09cd8d9079

“The Kenosha Reporter is one of hundreds of local news outlets that have proliferated in recent years, particularly in the run-up to the US presidential election. Despite presenting themselves as apolitical, many are what researchers have dubbed ‘pink slime’: outlets that push low-quality, partisan material through their own sites and social media pages.”

“’The issue in 2020 I think is not going to be foreign interference,’ said Alex Stamos, director of the Stanford Internet Observatory and formerly head of cyber security at Facebook. ‘It’s much more likely that legitimate domestic actors possibly operating under their own name — with LLCs or corporations with very shady funding that are not required to disclose what that funding is — are going to dominate the online conversation about the outcome of the election’.”

“’They raise money and they spend it to persuade people politically . . . spending so-called journalistic resources to get you to vote a certain way,’ said Steven Brill, co-chief executive of NewsGuard, which ranks the quality of news sites. ‘It really is the total undermining of what anybody thinks journalism is’.”

I have complained about the diminishing quality of news, at least in terms of its information content, for several years. While this has always been a function of the advertising driven revenue model for most news organizations, the problem exploded with the popularity of social media.

An important part of the problem is defining what counts as authoritative. Despite the advertising revenue model of newspapers of past, the best ones did maintain standards of journalistic quality. When search engines and social media emerged, they were subjected to less stringent content quality standards and stole share from incumbent media companies. This forced those companies to find ways to compete and in many cases standards got compromised as a result.

Now we have the irony of all ironies: Because people lost trust in traditional media companies, they are seeking alternatives and have found them in organizations that are different, but not better, and by all accounts a lot worse. I think this is extremely revealing and has implications for a lot of endeavors.

The “pink slime” phenomenon certainly has implications for news and information services. In the absence of strong quality standards for information, “news” can easily devolve to sensationalism. As it does it also transitions from a critical input for good decision making to a tool that can be used for manipulation. In an immediate sense this undermines the political process. In a broader sense it undermines any knowledge business and therefore the basis by which human society makes progress. In other words, this phenomenon is a very big deal.

Politics

The Morning Dispatch: One Week Left

https://morning.thedispatch.com/p/the-morning-dispatch-one-week-left

“But perhaps the biggest discrepancy between then and now is in the number of undecided and third-party voters left at this point. Clinton was leading Trump in key state polls four years ago, but she was doing so with only 44 percent to 46 percent in many of the battlegrounds. In Michigan, for example, polls on Election Day showed about 15 percent of voters were either undecided or leaning third party. Those late deciders—and voters who disliked both candidates—broke heavily for Trump.”

“There are far fewer undecided voters this time around—and third-party candidates are much less of a factor. Biden’s net favorability rating currently stands at +11—significantly better than Clinton’s -5 at this time last cycle—and the former vice president is winning voters who dislike both him and Trump by a landslide.”

JPMorgan's Kolanovic Has A Warning For Those Expecting A Crushing Biden Victory

“Looking at the chart above, Kolanovic finds that changes of voter registration (change in registered D, R, D-R), is a significant variable in predicting the voting outcomes, a critical observation which virtually no existing polls takes into account since it would indicate that Republicans have a high likelihood of winning virtually all battleground states!”

Some things that have struck me in regard to election news are how much of it there is and how little it informs me. For all the verbiage spilled, I have a very hard time getting much of a sense for which way voters are leaning. I don’t buy the stories about Biden’s huge lead because the national polls don’t count, electoral votes do. I also don’t buy narratives based on what happened in 2016 because a lot of things are different this time.

All of that said, two of the most informative pieces I have found are quoted above. They both make excellent points. From what I have read many of the polling errors from 2016 have been corrected but it is also fair to look at other sources of information outside of polling. I can absolutely see how a smaller number of undecideds will help Biden. A lot of voters hated Hillary. I also think Kolanovic makes a great point about newly registered voters – they matter.

While there are a lot of other puts and takes regarding the election outcome, I remain concerned that it is sucking the oxygen out of efforts to contend with major issues. Whoever wins is going to have to deal with them.

For example, there are short-term issues such as rising coronavirus infection rates and all of the attendant risks to economic growth. The fallout from lockdowns on renters and landlords is just starting to be realized. Unemployment is still exceptionally high. Further, with political partisanship so high, it will be challenging to devise any constructive public policy to shape a better future. These will be real challenges regardless of who wins.

Demographics (aka, the “grinding transition”)

NOT OK, BOOMER! A MANIFESTO FOR A GENERATIONAL REVOLUTION

“The respective roles of public and private choices on inequalities is a fascinating ideological debate, but their effects pale in comparison with that of falling interest rates and rising asset prices. Broadly speaking, older generations own financial capital, while younger generations’ only source of wealth is their human capital, which they hope to eventually convert into financial wealth over time.”

“Thus, the ratio of household wealth to income reflects the relative position of various generations: a high ratio means that the old can buy a lot of labor with their assets. This ratio has risen to 5.3 from 3.2 in 1978, which implies that younger generations must work about twice as hard as boomers did in the 70s to acquire the same share of wealth.”

As I have mentioned on many occasions, many of today’s challenges result from demographics and generational rivalries. One of the cultural phenomena I have observed, and I’m sure there is some of me projecting my own beliefs into this, is that boomers view younger generations as not nearly as industrious as they were. Younger generations view boomers as being almost completely out of touch with the realities they face.

Since I look at a lot of numbers, I am especially compelled by the case younger generations make: They don’t have nearly the economic opportunities or financial security their parents had at the same age. Vincent Deluard of Intl FCStone captures this reality vividly with the changing value of labor in relation to financial capital. Not only have millennials suffered from the relative decline in the value of labor but have done so as the result of public policy (suppressed interest rates) that systematically favors financial capital.

So, here is a thought experiment. What if, after twelve years of suppressed interest rates, this is the last big blowoff of public policy that hugely favors boomers over millennials? What if, from this point on, the tide turns and public policy increasingly, and then dominatingly, benefits millennials at the expense of boomers? If that happened, I suspect student debt forgiveness and capital for renewable energy would only be the start of government subsidized spending. I also suspect, the outlook for inflation would be quite a bit different.

Implications for investment strategy

‘Value drought’ claims latest victim as growth stocks power on

https://www.ft.com/content/22fb929c-8b92-4235-bbcf-33378cb66c60

“As a result, the ‘mispricings are real, clear and gigantic’, Mr Asness notes.”

There has been a lot written about the value investment style lately and its epic and historical underperformance. As a person who analyzes financial statements and values companies based on streams of estimated cash flows, I can say that I have never seen markets so extreme and I can also say I could not have even imagined that they could become so extreme.

In order to better understand and assess the landscape, I have spent a fair amount of time investigating the impact of passive investing. In a recent blog post I described nonlinear risk and how the ongoing penetration of passive investing appears to be increasing that nonlinear risk. Beyond a certain threshold, and I believe we are beyond it, the puts and takes of discriminating buyers and sellers fail to cancel each other out. Instead, price insensitive passive investors keep pushing prices further and further away from fair value.

This is exactly what Cliff Asness is referring to in his comment. The market is not getting more efficient. Rather, the mispricings are gigantic. The implications are that there will be a lot of money to be made by actively navigating these discrepancies. Just as importantly, there will be a lot of money to be lost.

What the shift on austerity means for markets

https://www.ft.com/content/87669b3b-5816-465b-88fa-104627b299b6

“The notion of generalised support for the markets needs to be heavily qualified, however. As we continue to live with Covid-19, we should expect government support gradually to shift from a universal approach to one that is more selective: people over companies, viable sectors over permanently damaged ones and more partial income replacement for households.”

These are very fair comments from El-Erian and timely enough that investors can digest them and benefit from them. While the market does seem to be considering further government intervention as benign, such intervention is always political which means there will winners and losers as a result. When that becomes clearer, the market may not cast as approving a view.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, Areté’s Takes are designed to show both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.