Arete's Observations 10/9/20

Market observations

More Stocks Have Risen By 400% This Year Than Any Year Since 2000

https://www.zerohedge.com/markets/more-stocks-have-risen-400-year-any-year-2000

There just aren’t that many situations in which the economy is growing so quickly as to justify several stocks rising by 400% in a year due to massively improving fundamentals. As a result, this serves as a crude but quick indication of speculative interest.

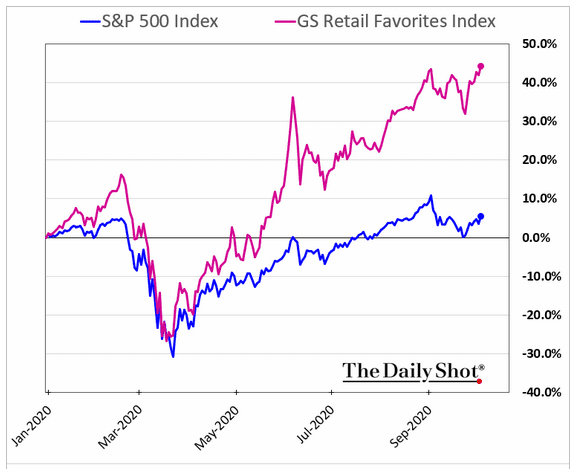

Another indication is retail participation. This graph from Goldman Sachs shows that hot stocks are hot again.

The next financial crisis may be coming soon

https://www.ft.com/content/c95e5a72-8322-4cfc-b36a-69e8998aea01

“One problem haunting finance, as Carmen Reinhart, chief economist of the World Bank, notes, is that leverage at many institutions was sky-high even before Covid-19. ‘If you look at financial sector vulnerabilities, in the longer term it is difficult to not be pretty bleak,’ she told me during a webinar.”

“’Although banks were not the origin of the crisis, they cannot expect to remain unscathed,’ Hyun Song Shin, chief economist of the Bank for International Settlements, has noted. ‘The immediate liquidity phase of the crisis is [now] giving way to the solvency phase, and banks will undoubtedly bear the brunt’.”

As a reminder, after the financial crisis morphed into a sovereign debt crisis, Carmen Reinhart was the one who literally wrote the book on the subject (along with Kenneth Rogoff). This Time is Different, was both a painstaking effort to gather data on sovereign debt and a thoughtful analysis. Among its conclusions were that beyond a certain threshold, debt detracts from growth potential.

Reinhart is now chief economist at the World Bank and is bringing her authority to the pandemic-stricken financial environment today. Her assessment that it is “difficult to not be pretty bleak” should be sounding alarms everywhere.

The article also highlights important elements of how financial problems are playing out. Although public policy addressed the “emergency” liquidity problems in March and April, those problems are now transitioning into difficult and chronic solvency issues. Further, this process is transpiring around the world and to a greater or lesser extent, will involve the banks.

Economy

Altered vistas

“Output per hour worked in America rose by more than 3% a year in 1998-2000, a feat the economy had not pulled off since the early 1970s. Growth in total factor productivity (a measure of the efficiency with which capital and labour are used, often treated as a proxy for technological progress) rose by about 2% a year from 1995 to 2004, according to Robert Gordon of Northwestern University. That was a sharp pickup from the average pace of 0.5% in 1973-95, and nearly matched the rate achieved during the heady growth years of 1947-73.”

“Productivity in the 2010s, by contrast, looks pitiful. Annual growth in labour productivity has not risen above 2% since 2010.”

Technology and hype go together so naturally that there is even a “hype cycle” to delineate stages of technology adoption. The cycle begins with expectations, usually based in reality, that quickly become inflated.

In the tech boom of the late 1990s, part of the hype was about how much more efficient the economy could be with widespread internet access. There was truth to the claim, and it was backed up by strong productivity statistics. Sure, things went too far, but much of the underlying technology really did improve economic performance.

Fast forward to the technology stocks of today and the landscape is different. Many of the claims are general in nature and many of the improvements amount to little more than cute gimmicks. Although there is technology that is meaningful, the fact remains that technology today is having nowhere near the impact on productivity as it did in the late 1990s. As the Economist concludes, “technology valuations are based, to a far greater degree than in the 1990s, on what could be rather than what is.”

Oil dragged under $40 by drab demand

https://www.ft.com/content/e5d144f6-a587-430d-b1de-9d706c1e41d3

“’I’m not upbeat about this market in the coming couple of months, I think we’ve got some real problems,’ said Ben Luckock, co-head of oil trading at Trafigura, at a Financial Times conference this week.”

“Analysts at oil brokerage PVM said ‘a tepid demand outlook, rising global oil supply and US political uncertainty’ was creating ‘a potent bearish cocktail’.”

Although certainly imperfect, the price of oil has conveyed as much information about global economic growth as any metric during the pandemic. On this basis the prognosis is not very positive.

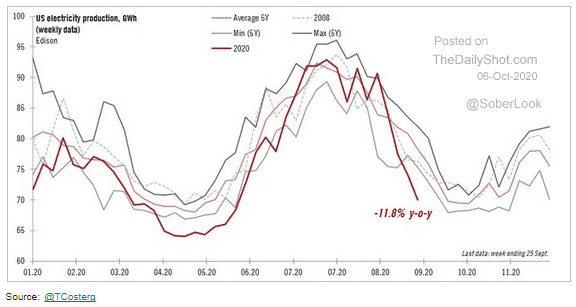

Another metric of interest is electricity consumption. This has long been used to help calibrate growth in China where official growth reports have been notoriously unreliable. Given the rapid and deep affect of lockdowns earlier in the year, it has been hard to gauge growth in the US as well. The recent decline in electricity use relative to recent history suggests economic growth is slowing down again.

Labor

News outlets are all too happy to report on jobless claims each week and extrapolate a trajectory for recovery. This exercise overlooks a bigger long-term problem, that of permanent unemployment. By this measure, the damage looks to considerably outpace the last two major recessions. This implies more than just short-term “stimulus” will be needed; retraining and longer-term provision of basic needs will be required as well. I don’t say this to endorse any particular policy, but rather to recognize the ongoing cost to the economy (and to the lives of the people affected).

Management

Hook, Line and Sinker

https://www.epsilontheory.com/hook-line-and-sinker/

“In the Long Now, the single most important executive skill is the ability to shape the external narrative of the company.”

“That is a shame for all of us. This exchange robs our collective future of the manifold promises of productivity, ingenuity and growth that come from investing in that first group of things. Instead it offers us a mess of pottage that is short-term stock price appreciation.”

While the job of a CEO has always been at least partly about creating narratives about the company, the power of those narratives was for some time bounded by the operational performance of the company. No longer. Increasingly, all that matters in the short-term is the CEO’s continued enthusiasm for the narrative.

This is a shame longer term because the preference for narrative facilitates misallocation of capital. Rusty Guinn recognizes that one of the costs comes in the form of “the manifold promises of productivity”. Interestingly, this is the same finding reported by the Economist: “Productivity in the 2010s, by contrast, looks pitiful”.

Retail

"Browsing Is Dead" - Walmart Redesigns Stores Inspired By Airports And Contactless Environment

“Walmart has introduced a new store design and layout that will be rolled out in the near term. The new design was mostly inspired by fierce competition from Amazon, airport layouts, and the contactless environment produced by the virus pandemic.”

“In a recent blog post, Janey Whiteside, the retailer's chief customer officer, wrote the new layout ‘spotlights products and end-to-end digital navigation that guides customers throughout their journeys’.”

Retail floor design goes back a long way and is the subject of marketing lore. Grocery stores are designed with milk in the back to induce greater foot traffic and therefore incremental purchases. Kohl’s made waves a couple of decades ago with its “racetrack” plan which was designed to lure customers to travel the entire store to discover great deals.

Now it looks like Walmart is planning a major reconfiguration of its floor design as well. I find this interesting because the opportunity to improve traffic flow in large stores and to leverage technology seems long overdue. I also find it interesting that when many companies are crossing their fingers and hoping for things to return to normal, Walmart is planning for a step function change in how bricks and mortar retail operates. This will be interesting to watch.

Commercial real estate

Gary Shilling’s Insight, October 2020

“A further problem facing commercial mortgage borrowers that have been struggling to meet payments is aggressive lending practices that overstated their ability to service their debts. A study of $650 billion of commercial mortgages originated between 2013 and 2019 found that even in those more-normal economic times, the mortgaged properties' net income often fell short of their necessary funds. In 28% of those loans, actual rent income trailed the projected amount by 5% or more. So even before the devastating pandemic hit, there was considerable risk that commercial mortgage-backed securities, into which these mortgages were packaged and then sold to investors, might not generate the promised income.”

Just in case investors might be inclined to believe some economic improvement could help commercial real estate (CRE) get over the hump and return to normal, Gary Shilling puts the kibosh on the idea. Importantly, he shows that a big part of the current problem was aggressive lending practices before the pandemic. As a result, expected income from CRE has been consistently less than expected.

The lesson is that much of the train wreck of CRE was already in motion before the pandemic. There is no reason to believe that a couple of tweaks here or there is going to fundamentally change that fact. The value of commercial properties will get hit and it will take time to resolve the problems.

Banks

Inside the JPMorgan Trading Desk the U.S. Called a Crime Ring

“Edmonds’s supervisors and more senior members on the desk showed him how to layer trades, he later told prosecutors, adding that it was understood on the desk that this was the way to trade precious metals futures.”

“The data feed of the trades includes each trader’s exchange credentials, allowing investigators to sort for suspicious patterns and attribute it to individuals.”

In the financial crisis of 2008 and 2009, banks were the center of attention as they had all kinds of bad loans and too little capital. By and large, they were given a pass from greater regulatory oversight because they were too big to fail. Because the magnitude and urgency of the crisis was so great, policymakers accepted the tradeoff of fast results in exchange for moral hazard.

The price has been moral hazard in spades. There have been countless instances of trading improprieties at banks ever since. It is unfair to blame just one or two “bad apples”; the problems are systemic.

The good news is regulators are getting access to more data and able to apply technology to hone in on dubious activity. While it is certainly possible this will serve as a meaningful deterrent in the future, it is also true that incentives still exist to circumvent the letter and spirit of the law.

Inflation

This graph of inflation is useful in a couple of ways. For one, it outlines the progression of the last major bout of inflation which serves as a baseline expectation for a lot of people. For another, it illustrates the behavioral element of inflation. It normally takes some time for inflation expectations to adapt to a new higher level. It takes more time yet for expectations to adapt to the possibility that things could keep getting worse. Ultimately, it becomes exceptionally difficult to break the belief system that prices will keep rising.

Asset allocation

Pension funds cannot afford not to buy more stocks

https://www.ft.com/content/1ab8e066-dc4c-4d0c-9d24-c686502a9ad8

“US equity indices have hit record highs in recent months after a breakneck rally from the deep coronavirus sell-off earlier in the year. But even at these stretched valuations, pension investors need to buy more stocks and other riskier assets.”

“If we accept that the policy response to coronavirus is likely to be inflationary, an environment that erodes the value of fixed income, it implies that a large equity allocation is needed at the heart of a retirement portfolio.”

These quotes come from Inigo Fraser-Jenkins, the head of portfolio strategy at the asset manager, Bernstein. The views he expresses are both representative of the industry and incredibly misleading for individual investors.

For one, he admits that his recommendation for pensions to buy more risky assets might seem “counter-intuitive” or even “reckless”. Actually, it is reckless. Effectively he recommends that in a game of chicken, i.e., pension investors adding risk in a desperate move to reach unattainable return targets, the best strategy is to drive faster and more directly at the oncoming vehicle. This only makes sense if you are not in either vehicle. Eventually it will fail miserably.

His argument that pension investors must do this “because they do not have a choice” is a fallacy. Of course, pension investors have a choice, albeit an unpleasant one. They can either increase risky holdings and also increase the risk of catastrophic loss for beneficiaries or they can identify the best possible opportunities the market has to offer at the risk of meeting return targets and eventually losing their job. The key is that catastrophic loss means a lot more to an individual investor in relation to his/her own money than it does to a pension manager in relation to other people’s money.

The idea that there is “no choice” but to invest in risky assets is still a wrong one even within the limited confines of the pension industry. If indeed there were no choice but to increase risky assets to the extent necessary to match targeted returns, then this could be done much more efficiently with an algorithm. Why pay for a human pension manager to do something for which he/she has no choice?

To the extent that there is any information content in this opinion piece, it is that pension managers are under a great deal of pressure to increase weights in risky assets and that will be a factor affecting the balance of supply and demand in the market. My guess is it will also be a factor leading to high sustained levels of volatility. As more pension and endowment managers are incentivized to “go for broke”, some will exceed the limits and get wiped out. That will be unpleasant for their beneficiaries but will create opportunities for others.

Gold

The Dawning of a Golden Decade, in gold we trust .report, May 27, 2020, Extended version

“It is difficult to imagine that this looming economic slump of historic proportions will not trigger a profound change of mentality in a society increasingly hollowed out by narcissistic demonstrative consumption and in which status symbols often seem to be taken for vital goods.”

“Acquiring gold is not an investment. It is a conscious decision to REFRAIN from investing until an honest monetary regime makes rational calculation of relative asset prices possible.”

The “in gold we trust .report” is a long (356 pages), comprehensive, well-written analysis of the environment for gold. For investors who are just starting to learn about gold it is a great place to begin. For those who have been following gold, it is a great place to get an update on current conditions.

One of the impressions I am left with is that the characterization of people who follow gold as grumps and “gold bugs” is mainly wrong. Rather, what I find is the people who follow gold tend to be inquisitive, open-minded, reasonable, matter of fact, and have a good historical perspective.

That historical perspective may be the most important characteristic. Gold as an asset class is most important in managing through the long cycles of history. Much of conventional investment theory is based on the notion that stocks have higher returns over long periods of time. The problem is, stocks and other financial assets also can perform dismally over long periods of time.

Implications for investment strategy

Artemis Capital Management published an excellent report entitled The Allegory of the Hawk and the Serpent and subtitled, “How to Grow and Protect Wealth for 100 Years”. The findings make a strong case for gold:

“What we learned from our in-depth study of financial history is that investors should prioritize secular noncorrelation over excess returns. The key to superior portfolio returns is to make surprisingly large allocations to alternative assets that perform when stocks and bonds do not!”

This is a hugely important point and one that often gets understated or avoided altogether by advisors. Over a very long investment horizon, it is more important to have uncorrelated return streams than it is to eke out slightly higher returns over some interim period of time. Given that gold prices have been falling recently, it is an opportune time to have a look.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, Areté’s Takes are designed to show both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.