Arete's Observations 1/15/21

Market observations

Almost Daily Grant’s, Wednesday, January 13, 2021

https://www.grantspub.com/resources/commentary.cfm

“Last year marked a watershed for the Nasdaq, as the exchange announced yesterday that it led all exchanges in total equity options trading volume, including a record 2.58 billion options contracts, a 52% jump over 2019. Similarly, CME Group, the world’s largest derivative exchange, reported that daily volume within its equity index and option categories footed to 5.6 million contracts last year, up 63% from the 2019 level.”

This section has been a repository of instances of speculative behavior since the first issue in early May. Grant’s note simply confirms much of what we already suspected: All forms of speculative behavior shot up last year. Trading activity, speculative trading (via options), and trading by individual investors all rose substantially year over year.

Economy

Waiting for the Last Dance

https://www.advisorperspectives.com/commentaries/2021/01/05/waiting-for-the-last-dance

“But today’s wounded economy is totally different: only partly recovered, possibly facing a double-dip, probably facing a slowdown, and certainly facing a very high degree of uncertainty. Yet the market is much higher today than it was last fall when the economy looked fine and unemployment was at a historic low. Today the P/E ratio of the market is in the top few percent of the historical range and the economy is in the worst few percent. This is completely without precedent and may even be a better measure of speculative intensity than any SPAC.”

The disconnect between market performance and underlying economic reality has been a consistent theme in this space but has a special cachet when coming from Jeremy Grantham. Often lost in the day-to-day minutiae of economic reports is the magnitude of the economic hit from the pandemic. Because of this extraordinarily abnormal event, it does not make sense to expect a return to normal any time soon.

Incidentally, the same perspective was voiced by Carmen Reinhart, chief economist at the World Bank this week. As she described, "a rebound this year still leaves per capita income below where it was before the covid crisis - calling it a recovery is misleading."

America’s demography is looking European

https://www.economist.com/united-states/2021/01/02/americas-demography-is-looking-european

“For those keen on growth, they [new population estimate from the US census] offer mostly grim reading. California’s population has stalled and may, for the first time, be declining. Illinois, which has shed over 250,000 residents in a decade, has shrunk for seven successive years. In the year to July, thus counting in little pandemic effect, New York endured more shrinkage than any state: it lost 126,000, or 0.65%, of its people.”

“Some states, mostly in the South, are growing fast, but not enough to lift the national rate. Overall, America’s population is barely inching up by historical standards. In the year to July it grew by 0.35% (or 1.2m) to 329m.”

I don’t have too much to say here other than to highlight that population growth is an important ingredient for GDP growth. Population growth in the US has been declining and with the new data is just barely above zero. This matters because it affects the amount of debt that can safely be serviced and, as the article mentions, “It also matters for state finances if there are fewer taxpayers to pay for public services.”

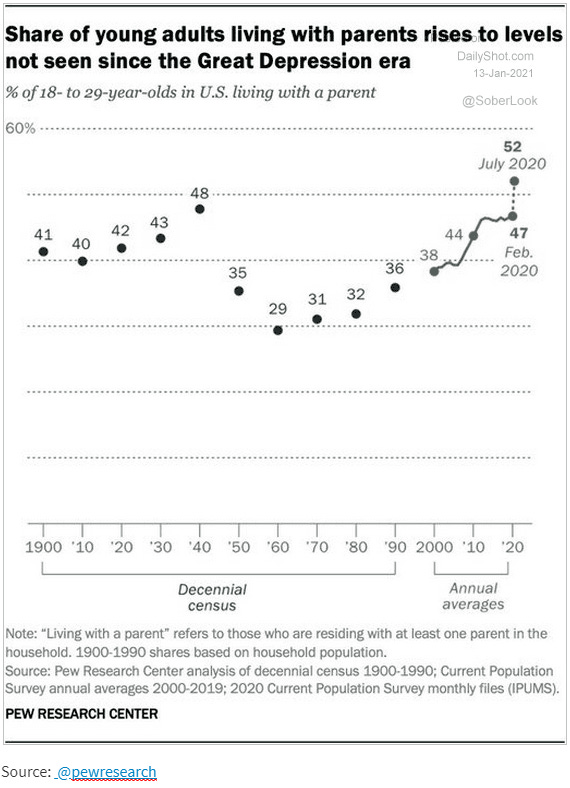

Finally, although it is by no means a conventional economic metric, the share of young adults living with parents does provide at least a qualitative perspective on economic health. Most people prefer to live on their own if possible. The fact the share of young adults living at home hit a 120-year high and rapidly accelerated the last twenty years speaks volumes about the economic conditions they experience.

Coronavirus

The Ireland Event

https://www.epsilontheory.com/the-ireland-event-2/

“Last week I became consumed by a new twist on all this – Covid numbers that were being largely ignored. Insane infection numbers coming out of UK and Ireland, apparently driven by a new virus strain, that we acknowledged over here but didn’t seem to be too mussed about.”

“And when I say ‘insane infection numbers’ I mean a 30x spike in Covid cases in Ireland over the span of two weeks in late December, where the R number – the basic reproductive rate of the disease – went from something around 1.2 to something around 3. Where you suddenly went from a few hundred new Covid cases every day to more than six thousand cases every day.”

I know everyone is getting tired of dealing with Covid and looking forward to returning to some sense of normalcy, but that is exactly the problem. Covid restriction fatigue combined with a more virulent strain in the UK is rapidly increasing infections there. Much as when the virus first became apparent about this time last year, it had already spread much further than was visible from contemporaneous news reports.

This creates a big risk although it is hard to assess the probability. Regardless, it does imply it will be imperative to distribute vaccines as quickly as possible to prevent explosive growth in infections. This presents the real possibility that some countries and regions will fare very substantially better/worse than others.

Monetary policy

Criticism of the Fed is going mainstream

https://www.axios.com/federal-reserve-inequality-criticism-ae8bc6a9-2b00-4335-93c3-5da17c074253.html

“Big names in the world of finance are beginning to call out the Fed and other central banks for their role in ramping up economic inequality and manipulating financial markets — a departure from the praise they received for most of last year.”

"In 2010, Ben Bernanke talked about the benefits, costs and risks that come with unconventional policy. He added, the longer you maintain it, the lower the benefits, the higher the costs and risks. This was ten years ago. At that time, Bernanke was thinking of unconventional policy as an economic bridge. Now, it has become a destination."

Many of us have been highlighting the limits of monetary policy all along. Monetary policy alone does not create economic growth, comes with diminishing effectiveness over time, and increasingly facilitates significant systemic risks. Now, not only are the plausible limits of monetary policy being approached, but the narrative surrounding it is radically changing character.

What used to be “the only game in town” in regard to helping the economy recover after the financial crisis in 2008 is increasingly being singled out as the scapegoat for current ills. While there is plenty of blame to go around, that isn’t the point. The point is with weak growth and few prospects for significant improvement, the easier political path is to affix blame rather than to solve problems. An important implication is that if the Fed is used as a political scapegoat, the narrative of the omnipotent Fed supporting the market gets blown to pieces.

Politics

The Morning Dispatch: It Could Have Been So Much Worse

https://morning.thedispatch.com/p/the-morning-dispatch-it-could-have

“As more video footage of the attack itself emerged, it became increasingly plain that many in the crowd had come to the event already prepared for violence. Video of men kitted out in tactical gear moving in tandem up through the crowd on the Capitol steps and into the building itself went viral on social media, as did horrific photos of a man leaping through the Senate chamber with flex cuffs in hand.”

“Another thing that became clear over the weekend was how close things came to being much worse. There was a shockingly short span of time between the locking down of the Senate chamber and the arrival of the rioters in the building. The quick thinking of one officer who lured protesters away from the chamber door may have been all that prevented actual shooting on the floor of the Senate.”

As I am sure was the case with many people, I experienced a lot of different emotions after the attack on the Capitol last week. While I felt anger and disgust, the scenes were so surreal they also took time to process. Further, in the context of so many crazy happenings the last few years, there was some sense that it was just more of the same.

I no longer feel that is the case; I think that attack will prove to be a defining moment, a wakeup call. In short, everything was fun and games until someone got their eye poked out. Now serious scrutiny is being placed on all of the people who acted violently, incited violence, or enabled it. Political donors are backing way off. What used to be viewed as harmless political activity can no longer be considered as such.

An important element of the story was the display of vulnerability of a major government institution. It is now all too easy to imagine that personal harm could have been caused to members of Congress. Further, it presents a startlingly simple playbook for any actor who may want to disrupt the US government.

If only the storming of the Capitol were a one-off freak event it would be disturbing enough. Unfortunately, there are good reasons to expect more trouble …

The Capitol Was Just the Start

https://www.nytimes.com/2021/01/13/opinion/capitol-riot-internet.html

“It isn’t just the crowd’s variety that was striking. I’ve spent the past few days watching as many videos from the siege as my eyeballs could handle, and what terrifies me again and again is the sense of surprise and entitlement — the authentic shock so many of the rioters expressed when confronted with a reality that did not match the cosplay revolution they’d dreamed about on Discord.”

“Yet none of this is over — far from it. Now that the conspiracy mob has effected such carnage on the real world, we’d be foolish to suppose that its appetite has been sated, rather than only whetted. Monstrous online lies are not done with us. The Capitol is just the beginning.”

In corroboration of this assessment, the Morning Dispatch reported, “The FBI is reportedly preparing for armed protests at all 50 state capitals and in Washington, D.C. in the days leading up to President-elect Joe Biden’s inauguration.”

This poses an important challenge for the rest of us. We have to recognize the rioters were not just some lone band of especially crotchety misfits. Rather, there are a lot of people in this country that comprise a diverse group and live in an alternate reality. They are willing to do violence to the government and to US citizens in the bastardized name of patriotism. And they aren’t going away.

Rather than be paralyzed with wonder and disbelief, we collectively need to learn a lot more about what is compelling such behavior and what all needs to be done to defuse it. Until then the baseline assumption should be this type of activity will remain a lingering threat.

Public policy

Biden's radical economic agenda

https://www.axios.com/bidens-radical-economic-agenda-cb8d8564-1e47-4bcf-908d-92f9917d7e80.html

“Power will move from Wall Street to Washington over the next four years. That's the message being sent by President-elect Biden, with his expected nomination of Wall Street foe Gary Gensler as the new head of the SEC, and also by Sherrod Brown, the incoming head of the Senate Banking Committee.”

Frankly, I am encouraged by the tone of these prospective appointments. There is a difference between unnecessary red tape and effective enforcement. Since I believe inadequate enforcement has been one of the biggest problems in capital markets the last twenty or so years, I welcome the prospect of a more level playing field.

That said, the most recent news on policy is that Biden will be significantly upsizing his initial stimulus request. While I have been working on the assumption that regardless of Biden’s politics, his policy agenda would be severely constrained by the Senate, I am watching closely for signs that dynamic may be changing. I am a lot less concerned about higher taxes (how else will spending be paid for?) than I am about government becoming more involved in allocating capital.

Investment advisory

Waiting for the Last Dance

https://www.advisorperspectives.com/commentaries/2021/01/05/waiting-for-the-last-dance

“Most of the time in more normal markets you show up for work and do your job. Ho hum. And then, once in a long while, the market spirals away from fair value and reality. Fortunes are made and lost in a hurry and investment advisors have a rare chance to really justify their existence. But, as usual, there is no free lunch. These opportunities to be useful come loaded with career risk.”

This is an understated but hugely important point: Most of the investment business is predicated on simply playing along. During one of the biggest bull markets in history this has been a winning formula for many.

The other side of that is there are almost no advisors or money managers left who are both willing and able to take a contrarian position. The landscape is littered with hedge funds and other investment vehicles that couldn’t remain as viable businesses longer than the market could remain irrational.

As a result, there are likely to be two major changes for investors to consider. One is that once the bull market breaks, investors will need to contend with a radically different investment environment. The other is that when that happens there will be precious few advisors willing and able to navigate the new landscape.

Technology

Millions Flock to Telegram and Signal as Fears Grow Over Big Tech

https://www.nytimes.com/2021/01/13/technology/telegram-signal-apps-big-tech.html

“Their sudden jump in popularity was spurred by a series of events last week that stoked growing anxiety over some of the big tech companies and their communication apps, like WhatsApp, which Facebook owns. Tech companies including Facebook and Twitter removed thousands of far-right accounts — including President Trump’s — after the storming of the Capitol. Amazon, Apple and Google also cut off support for Parler, a social network popular with Mr. Trump’s fans. In response, conservatives sought out new apps where they could communicate.”

This story is interesting on a few different fronts. One is that some users were shocked that their messaging app shares some of its data. Another is that once disabused of a false sense of security, many tech users have proven extremely fickle and switched services almost instantaneously. Another is the degree to which big tech companies have suddenly started caring about the things that get posted on their platforms. It is almost as if when bad behavior is allowed to propagate unchecked that bad things eventually happen. Hmmm.

Inflation

Just a Fantasy

https://www.epsilontheory.com/just-a-fantasy/

“Simply because the breakeven 10-year sits above 2% does not mean it will remain there. Second, it’s necessary to ask ‘why’ it’s there. Is it really productivity growth that will sustainably drive ’good’ inflation? That’s unlikely. Recent wage inflation has been a function of a change in employment mix and goods inflation a function of supply shortages.”

This post by Peter Cecchini on the Epsilon Theory website covers much of the investment environment but provides especially useful context on inflation. The main point hits on the recurring theme of reality versus illusion. The idea that the economy is going to heat up and drive “good” inflation is fantasy. The reality is fiscal support is the only thing keeping the economy moving along.

Cecchini’s account also highlights another useful point: Inflationary pressures are affected by many factors and have many cross currents. It is incredibly hard to evaluate the aggregate level merely by observing fragments of information on social media. For anyone who is beginning to make a broader effort to understand and handicap the phenomenon of inflation check out my special report on assessing inflation.

One final note. With housing being the biggest single category in the CPI basket, it has a disproportionate impact. As the graph reveals, rent inflation typical takes years to recover after an economic downturn and is well below the trajectories of prior downturns. This will be a big headwind to overcome if inflation is going to really pick up.

Capital markets

Stress test looms for financial system in 2021

https://www.ft.com/content/5df1b07a-b6d0-44ad-8911-2d9be0096a0a

“The financial fragility revealed in March 2020 highlights a fundamental change in the structure of the financial system. For much of the postwar period, it was all about channelling savings to borrowers, facilitating payments and helping people and corporations share risk.”

“In other words, a financial system with a morally hazardous inbuilt incentive for excessive risk taking is now subject to a rolling stress test on an unprecedented scale.”

There isn’t a lot of new insight revealed in this piece, but it is an excellent overview of how the financial system has evolved and what that implies. In short, it is a system built much more on moving financial assets (collateral) around than it is about allocating capital to economic enterprises. As such, it is also a system built to keep ratcheting up risk until things break. Again.

Implications for investment strategy

Given the excessive disconnect between market prices and economic fundamentals and given the rampant crazy behavior in markets, it is fair to say we are getting close to the end of the line of the bull market that started in 2009.

I see two basic paths forward. One possible path involves a major sell-off in the not-too-distant future. Many investors will repeat the playbook of buying the dip and get wiped out as those fresh purchases produce major losses. Eventually, many investors will be forced to sell. At some point, investors who maintained large cash reserves will be able to start dipping back in at prices that are finally attractive relative to economic fundamentals.

The other possible path involves a continuation of the pattern of market excesses, rapid selloffs, and stick saves by the Fed expanding into ever more unconventional policy measures. This path would include more explicit backing of corporate credit and eventually would include the purchase of stocks. I don’t think it matters that these actions are not currently legal. In a major sell-off nobody would make a legal challenge.

The implications would be quite significant, however. It would effectively turn markets into government utilities. Stocks would no longer be shared ownership interests in agents of economic growth but rather mere gambling tokens to be cashed in later. The value of those tokens, however, will be determined by the casino owner and will be lower than the original ones.

I lean toward the first scenario simply because I think it is hard to maintain major illusions for long periods of time. In a different domain, the attack on the Capitol reflects this tendency. The existence of moral hazard provides the cover for bad actors to become even more so – until something finally gives. Nonetheless, it is important to think through both scenarios and prepare for them.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.