Arete's Observations 2/26/21

Market observations

Cathie Wood's Tesla Noise Is Deafening Investors

“As for the wider market, the benchmark 10-year Treasury bond yield spiked from 1.36% to 1.43%, a new post-pandemic high, from 7 a.m. to 9:30 a.m. Greeted with a bond tantrum, U.S. stocks started the day by tanking. Then the Federal Reserve’s chairman, Jerome Powell, began his second day of testimony to Congress. Powell said the same thing he had said the day before, and prompted the 10-year yield to drop back to 1.37% while sending the Nasdaq-100 on an intraday rally of 2.6%. Such things aren’t supposed to happen, or at least not in markets that are vaguely rational. After the close, GameStop surged further, while bond yields spiked again, touching 1.415%.”

Market action on Wednesday, described above by John Authers, was bizarre but also probably revealing. Clearly, there are increasing concerns about rising rates as the 10-year went on to breach the 1.5% threshold on Thursday. Also, clear, however, is the degree to which the market appears unanchored: It just doesn’t take much for stocks to move quite a bit in either direction.

Is The Move In MOVE About To Rock The VIX

https://www.zerohedge.com/markets/move-move-about-rock-vix

UBS Securities, who writes that “today anxiety is creeping up in every corner of the market, but it’s rising faster in safe havens than stocks. If the current pace of gains in rates volatility continues, the S&P 500’s “fear gauge” will have to catch up."

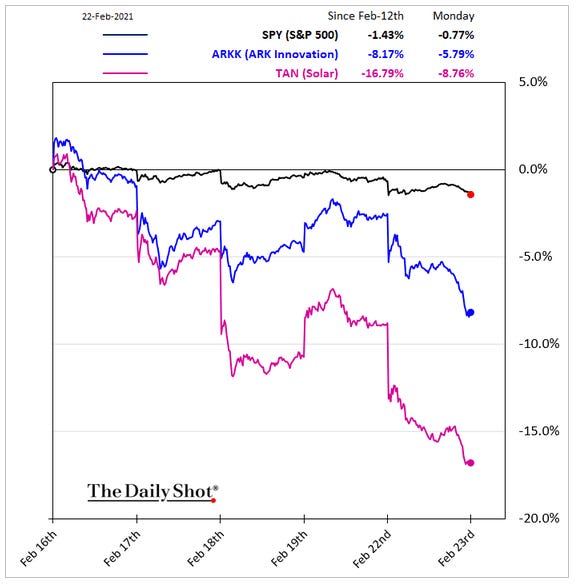

Although the stock market has remained relatively unaffected by higher rates thus far, it may be just a matter of time for those signals to make their way through. If stock volatility does follow bond volatility, expect to see a weaker stock market. We have already gotten a preview of what this looks like with some of the more growth-oriented stocks.

Economy

GDPNow

https://www.frbatlanta.org/cqer/research/gdpnow

“Latest estimate: 9.6 percent — February 25, 2021”

The Federal Reserve Board of Atlanta has created a model that adjusts the estimate of GDP for the quarter based on updates from major economic releases during the quarter. It is a useful estimate that has proved fairly accurate over time.

Given the extremely high number for first quarter GDP, it is easy to see why people are becoming more optimistic about the economy this year. In addition, since the estimate is well above the consensus of blue-chip estimates, it is fair to expect those estimates to start increasing to meet the reality. And, just to pile on, personal income seems to be jumping considerably as well. Still, something seems amiss …

U.S. growth expectations are going through the roof

https://www.axios.com/gdp-us-growth-expectations-roof-df783b65-bdd9-4634-b9c5-783709a80688.html

“The bubbly outlook for 2021 does not square with the New York Fed's reading of real-time economic data, which is once again trending lower thanks to Thursday's initial jobless claims reading and a decrease in rail traffic, which more than offset increases in retail sales and tax withholding.”

The fact is there are very strong cross currents in the economic picture, and it is extremely difficult to net them out into a single cohesive view. Further, given the extreme data, it is easy to create strong, yet misleading narratives. I strongly suspect this noisy and uncertain background will stoke volatility and be the norm for the foreseeable future.

Coronavirus

The good news is case counts, deaths and virtually all other coronavirus metrics are trending down. Further good news is that vaccines are effective and are getting distributed.

None of this means the pandemic is over, however. The threat of variants becoming dominant is significant and is especially difficult to quantify given the dearth of information available. While this risk should not be overstated, it is also not receiving the attention it deserves.

CDC Steps Up Tracking of Virus Variants After Months of ‘Flying Blind’

https://www.thedailybeast.com/cdc-takes-step-to-ramp-up-tracking-covid-19-variants-via-genome-tests

“The fact that we don’t know how much B117 is circulating means we are making all of our policy decisions… about opening restaurants and bars and other places … we’re doing it all blind,” said Dr. Ashish Jha, dean of Brown University’s School of Public Health.

Public policy

Scoop: Small businesses say even second round of PPP not enough

“Only 11% of firms that received a PPP loan say they are very confident they will be able to maintain payroll if no further government relief is provided and 67% of loan recipients expect to exhaust their second loan funding in April or May.”

This report shows the episodic and uncertain nature of fiscal stimulus but also reveals the fragile condition of small businesses. While it is understandable in a fraught political environment that policy measures may be less-than-perfect, the small business challenges are a good reminder of how much less than perfect they really are. Expectations should be set accordingly.

China

Chinese stocks drop 3% in retreat from record highs ($)

https://www.ft.com/content/32c8ece1-1e7b-4954-808b-6f92cd3b930c

Thomas Gatley, an analyst with Gavekal Dragonomics, said the PBoC was “in no mood to restimulate this year” as policymakers in Beijing have called for a further clampdown on financial risk. With the profit cycle for corporate China turning, he said, “my position remains that the underlying laws of gravity are going to take effect”.

The perception seems to be something like a repeat of 2009: After much of the world suffers a major selloff, the recovery in the global economy will be led by China. Times change and China’s desire and ability to stimulate the economy are more constrained and more nuanced than in the last episode.

While a drop from record highs is not much in terms of an absolute move, the decisive change in direction is meaningful. I think Gatley is right that China’s policy will be prioritizing the reduction of financial risk over economic growth for the foreseeable future.

Inflation

In general, I still view the short-term concerns about inflation as being over-hyped. Many of the longer-term, structural conditions that would need to exist for broad-based inflation just don’t exist right now and are not on the immediate horizon either.

One way to see this is through the comparison of spot energy prices to energy stocks. When inflation becomes more entrenched, the profitability of energy stocks will need to rise in order to provide for capital expenditures to increase supply. That hasn’t happened yet.

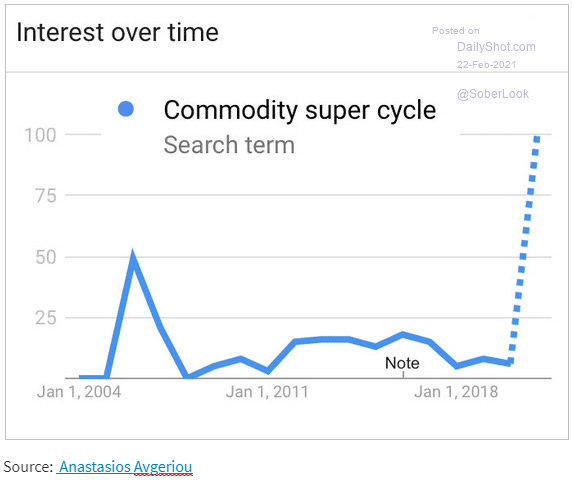

Further, much of the interest in inflation seems to be at least as much a function of short-term speculation in anything that might go up rather than long-term positioning. The recent and significant increase in searches for “commodity super cycle” help characterize the nature of interest.

All of that said, my views toward inflation have evolved somewhat. I still believe inflation is an important threat to portfolios over the medium to long term. I also still believe investors don’t need to chase prices in order to establish inflation hedges.

What has changed is my expectation for a significant deflationary event has lessened modestly. My view has been importantly influenced by the characterization of carry regimes in the book, “The Rise of Carry”, which I mentioned each of the last two weeks.

As described in the book, carry regimes can be magnified by central bank policies. Given the Fed’s profile of aggressive intervention, I believe there will likely be more carry crashes and those will be good times to add to inflationary hedges.

I also believe, however, that the Fed’s more proactive stance still enables the prospect of a final deflationary bust but does reduce the chances. On the other hand, while the Fed cannot create economic growth, it can convince global investors of its intention to undermine the value of the dollar.

Given the massive growth in money supply over the last year, many investors may believe massive devaluation has already happened. The only problem is currency value is a relative game and most other global regions are in even worse shape than the US. As a result, it is fair to expect the US dollar to remain stronger and the current carry regime to persist longer than seems reasonable.

One more point to make about inflation. Given a very long period of disinflation, most Americans are not conditioned well to deal with inflation. People expect to get exactly what they want, when they want it, and for a cheap price. Now, clogged supply chains and rising commodity prices threaten all of those expectations. Those who can be flexible in regard to substitutes and timing can avoid much of the pricing pressure. Those who cannot be flexible probably will end up paying more.

Cryptocurrencies

The spectacular interest in cryptocurrencies continues to surprise me although many aspects of the craze do not. For example, it doesn’t surprise me that a lot of people feel betrayed by the abuses of fiat currencies (count me as one of them). It doesn’t surprise me there is a widespread effort to find/create a better currency system. It doesn’t surprise me it involves technology.

But c’mon, why throw away all experience and insights that have come before? That strikes me as unwise to say the least. Rather than “standing on the shoulders of Giants” to see a little further (as Newton did), the effort seems to be more akin to re-inventing the wheel.

While there is plenty to say about crypto, and an excellent dialogue to be had on what a future currency system should look like, for now I will limit comments to those most relevant to the here and now. Given all of the money floating around looking for a home, cryptocurrencies are a natural target for speculation. Further, big price moves seem to be more a function of low liquidity than of intrinsic value …

Bitcoin's shitty liquidity - works both ways

Themarketear.com, Feb 23 2021 at 04:40

Reminder from JPM; "First, in contrast to S&P500 and gold, bitcoin liquidity has deteriorated over the past three months even as its price tripled. Second, the impact of volumes on prices looks currently much bigger in bitcoin than in gold or S&P500, almost 3x-5x in futures and 10x-20x in ETFs. In other words, market liquidity is currently much lower for bitcoin than in gold or the S&P500, which implies that even small flows can have a large price impact."

Monetary policy

Dealing with the next downturn

This is the white paper in which the policy of “helicopter money” was widely socialized about a year and a half ago. Two of the authors, Stanley Fischer and Philipp Hildebrand, are influential central bankers who often guide policy behind the scenes. As such, the paper can be considered a serious trial balloon.

The idea of “helicopter money” elicits fear and outrage in many advocates of sound money, and rightly so. The idea of “going direct” means, “finding ways to get central bank money directly in the hands of public and private sector spenders.” It doesn’t take much imagination to see how prices could skyrocket under such conditions.

Inflation via helicopter is by no means a foregone conclusion, however. For one, the authors explicitly acknowledge the limitations of policy by saying, “There is not enough monetary policy space to deal with the next downturn” and “Fiscal policy should play a greater role but is unlikely to be effective on its own”.

The authors also acknowledge risks to “the hard-won credibility of policy institutions” and the distinct possibility of “uncontrolled fiscal spending” should the boundaries between fiscal and monetary policies become too blurred. The takeaway is there is nothing easy or inevitable about this.

To this point, the playbook for helicopter money looks even more problematic. Broadly, the parameters would include defining the circumstances that require helicopter money, making fiscal and monetary authorities jointly accountable for achieving targeted inflation, nimble deployment of productive fiscal policy, and a clear exit strategy.

Personally, I don’t see how any one of the above conditions could be passed with bipartisan support, let alone all of them. There is so much wiggle room one party would never trust the other to not abuse it. Further, since “The efficacy of such a framework would be undermined significantly if it were only introduced when a downturn is already underway”, I don’t see how the policy could be approved in advance of the next downturn.

As a result, as frightening as the concept of helicopter money is, the practical constraints seem large enough to reduce it to a relatively low probability scenario for the time being. As Jim Bianco points out in Grant’s, however, the Fed is likely to get its arm twisted at some point …

Extreme investing primer ($)

Grant’s Interest Rate Observer, February 19, 2021

“The point is, the last two policy changes have been market-driven,” Bianco tells me. “The market takes a big right turn or left turn, and the Fed is forced to react to it. And, so, when the Fed says . . . we could let the average inflation rate run above 2% . . . we don’t have to raise rates. I keep screaming, ‘It’s not your call. It’s the market’s call. If you let inflation go up to 2.5% and the markets are okay with it, you’re okay with it. If inflation goes up to 2.5% and the market throws a fit, you’re 10 days away from raising rates. You just don’t know [that] you are yet.’ ”

Implications for investment strategy

Much as my thoughts on inflation have been influenced by “The Rise of Carry”, so too has my perspective on investment strategy evolved modestly. I still believe valuation is the best indicator of future returns for long-term investors and current (high) valuations imply dismal returns.

Where my view has softened to some extent relates to opportunity costs. While I have been exceedingly averse to stock exposure given exceedingly high valuations, it was easier to sit on the sidelines with a lot of cash when inflation was virtually nil and when a significant dislocation seemed relatively near at hand.

Now, my qualitative estimate of the opportunity cost of cash has risen (slightly) in two respects. First, the construct of the carry regime and the Fed’s highly interventionist policies now lead me to believe that the carry regime can persist longer than I had imagined, and that the final denouement could be avoided altogether. In simple terms, I now believe the potential for a major, major selloff that would create terrific purchase opportunities is lower than I did before.

Another way in which my evaluation of opportunity cost has changed is through the inflation forecast. Clearly inflation estimates are rising and as such, the opportunity cost of holding cash increases. On the margin, this induces me to be more receptive to putting some cash to work (albeit selectively) when carry crashes present opportunities. Most of the focus will be on adding to inflation hedges.

I do believe there will be more opportunities like this too. Carry crashes occur when financial relationships change faster than anticipated which then forces a sell down of exposure. Given the potential for rapid changes in interest rates and currencies, among others, there is all kinds of potential for some carry trade to get caught out.

John Dizard highlighted the example of mortgage banks in the FT. As rates go up, prepayments of mortgages go down, and as a result, portfolio duration increases. In order to manage duration, these banks sell Treasury bond derivatives – which drives rates higher yet.

Do not rule out a market panic next month ($)

https://www.ft.com/content/7354515b-1007-40f2-bac7-45a9f7235f70

“If my guess is right, then we have the makings of another ‘event’ like we saw a year ago.”

I also believe it will be increasingly important to get out of the mindset of outperformance. In the environment of a carry regime with extremely rapid growth in money supply, new speculative ventures emerge every day. For example, just this week I heard an analyst on a webcast describe the big investment hit of 2020 as “microcap scams”.

With so much money flowing, a lot of it will get misallocated to uneconomic enterprises. Long-term investors will be better off resisting the allure of chasing performance in the short-term in order to avoid catastrophic losses later.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.