Arete's Observations 4/30/21

Market observations

The market was quiet again early in the week despite a slog of earnings reports coming out. Everyone seemed to be waiting to hear what the Fed had to say. Once word came out on Wednesday, investors were sufficiently reassured and the market resumed its upward march. For the time being, this utter reliance on the Fed is just unhealthy. Eventually, it sets the Fed up to fail an impossibly high standard.

Robinhood, Three Friends and the Fortune That Got Away ($)

https://www.wsj.com/articles/robinhood-three-friends-and-the-fortune-that-got-away-11619099755

“Many rookie traders, accustomed to sharing birthday photos and daily online musings, showed few qualms about making investments based on what friends shared in group texts or what strangers posted on Facebook. As much as anything, their investing is a social activity.”

This story in the WSJ captures much of the investing zeitgeist of the day and in doing so also reveals how much the endeavor of investing has changed. For one it is super cheap and easy to start investing so it is super easy to get started, whether one is ready or not. For another, retail platforms are extremely accessible and entertaining and when markets almost never go down, they become extremely alluring destinations for a lot of people.

What hasn’t changed is investing is complicated and risky, especially so when leverage is used. This is a message almost always better learned through hard experience than some adamant finger wagging. Judging by the article, these three guys have probably learned their lessons, but there are a lot more to go.

Investors are struggling to time 2021's magic stock market

https://www.axios.com/stock-market-investors-time-magic-903f656d-fd0b-4996-aa27-25bc288658bd.html

"To try to guess that this is the right time to be out of the market, you may as well go to Las Vegas," Mark Stoeckle, chief executive at Adams Funds, told Bloomberg. "Here’s just as much risk doing that."

There was a time when stocks were considered so risky that they had to be sold to people, because nobody would buy them on their own. Now stocks are considered so essential to investment portfolios the harder decision is if/when to be out of the market. A sign of the times.

Media

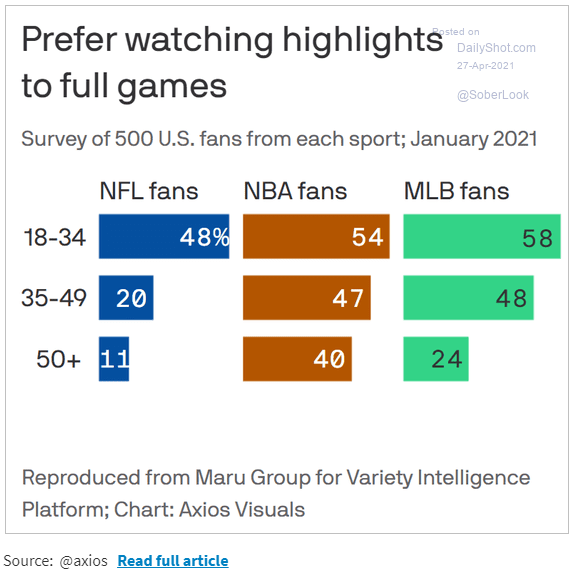

This little tidbit on sports (below) isn’t too surprising but does provide some food for thought: Younger sports fans have a much greater preference than older ones to just watch the highlights. The notion of small digestible bits as an alternative to full length content captures a trend that pervades all forms of media. It seems cliff notes compete with the original version in many cases.

While this preference for brevity and conciseness is fine for a number of things, it is considerably less so for others. Highlights of a textbook, for example, are unlikely to create a foundation of first principles that can be widely applied in other areas. A “highlights” version of instructions for a piece of IKEA furniture is more likely to lead to assembly mistakes.

Certainly, there is a place for both long and short forms of content. It will be interesting to see if this survey indicates a trend toward more short form content in general, or if it simply reflects a waning interest in major league sports.

Social dynamics

How anti-greed backlash killed the European Super League

“The 48-hour rise and fall of the European Super League is the perfect encapsulation of how anti-greed sentiment has changed the rules of capitalism.”

“The Super League was an attempt to create many more of the real money-spinners, with the profits, naturally, mostly accruing to the owners of the super-elite clubs. That violated the sense of fair play that underpins most sport, as I explained on Tuesday. Even if the Super League was Pareto-optimal, thanks to its "solidarity" payments to lower-ranked clubs, it wasn't fair. And that brazen unfairness led to its almost-immediate death.”

The pushback against the concept of a European Super League was fast and furious, largely because it violated a sense of fairness. In one sense this is interesting because fairness is a hot button for people that can elicit extreme behavior. It is also interesting that it happened primarily in Europe. I strongly suspect such a strong response would not be had in the US.

Labor

‘We are drowning in insecurity’: young people and life after the pandemic ($)

https://www.ft.com/content/77d586cc-4f3f-4701-a104-d09136c93d44

“A 30-something who works in private equity in the UK turns to collateralised debt obligations for a metaphor to describe the position of his generation. ‘The space I feel I occupy in the sociopolitical order is akin to being the first loss tranche in the debt stack,’ he says. ‘Whenever anything bad happens I have no doubt that, because we lack political and economic clout, we will be left holding the bag’.”

“Sam, a corporate lawyer from London, captures the feelings of many when she concludes she will be better off than her parents in some ways, but not in others. ‘I have a professional job and they didn’t. [But] In terms of . . . the full-belly feeling of knowing your children will have a better future than you? Not so much’.”

I continue to believe this is one of the more underappreciated yet influential phenomena pervading society: Younger generations are better off in some ways but also face insecurity in ways that older generations often have difficulty comprehending.

The consequences are far reaching. Millennial and Gen Z workers are often more aggressive in pushing for promotions and pay raises feeling they simply don’t have the luxury of waiting for advances at the same pace older workers did. At the same time, insecurity often manifests itself in disenfranchisement and a reluctance to even advocate for change. Insecurity is also leading to much lower fertility rates. If this keeps up, there just won’t be enough young people around to help take care of the old people.

Reopening

The new frontiers of hybrid work take shape ($)

https://www.ft.com/content/f568997c-513c-48b0-8422-fabacda46418

“The hope in many companies is that this sort of working pattern will allow employees to do focused work at home, reduce commutes and enable them to better balance professional and personal lives. In turn, offices will become a destination for innovation, collaboration, networking, coaching and socialising.”

“Hybrid working will involve a lot of experimentation. Anne-Laure Fayard, an associate professor at the department of technology management and innovation, NYU Tandon School of Engineering, says that patience will be required to create new habits. ‘There will be some need to design and engineer serendipity at the start. It will take time and evolve’.”

This article comes across as typical Harvard Business Review material. True to that form, the article even includes a “handy” sidebar that delineates the four remote worker archetypes.

While the article is probably useful, I don’t consider it especially insightful. After all, thinking through the broad categories of work and explicitly calling out the portions that are most amenable to remote work is not exactly rocket science. What is interesting is this simple exercise just hasn’t been done at scale before. Quite arguably the exercise of breaking down remote functions should have been a core part of any HR effort long before the pandemic.

The fact that it has not been says something about the power companies have wielded over workers. In my opinion, large companies have paid above average as a type of bribe for committing oneself to jumping through all the hoops, including showing up at the office all the time. I suspect that relationship has changed pretty significantly.

Politics

Republicans win too often to ever change ($)

https://www.ft.com/content/f1c438ea-f8fa-4142-b2e8-ffd8f3a49a24

“American voters used to throw the book at hotheads or even eccentrics. A wildness of thought and style cost Barry Goldwater a 16m-vote defeat in the 1964 election, when there were fewer than 200m Americans. For the crime of a soggy and meandering liberalism, Walter Mondale lost every state but one 20 years later. Had the Republicans tasted anything like as crushing a result in November, they would now be six months into a process of reform, or at least a constructive civil war. As it is, there is minimal incentive on their part to reflect, much less change. In a post-landslide age, neither party is ever further than one more heave from power.”

“It is soothing, no doubt, to believe that a fervent cult, drunk on misinformation, is what threatens US democracy. It gives the problem manageable dimensions. It also avoids blaming the public at large. But no sect, however vehement, can prosper without complacent multitudes.”

Janan Ganesh brings up a topic nobody wants to talk about: A big part of the problem with politics is the public at large. He is absolutely right that voters are not punishing hotheads and eccentrics like they used to. The main implication is a state of volatile politics in which moderates get squeezed out.

Public policy

Biden's next 100 days

“So look for Biden to court Republicans, but not yield to them, as he pushes a $2.3 trillion infrastructure package, to be followed by $1.5 trillion for his American Families Plan — including child care, paid family leave, universal pre-K and free community college.”

I continue to be surprised by the aggressiveness of Biden’s fiscal plans but understand that it makes sense given the very limited window of opportunity he has to get anything done. That said, the thing to watch will be what can actually get done. Republican reaction to Biden’s speech on Wednesday evenings indicated little opportunity for bipartisan collaboration.

One of the interesting issues that has arisen is the distinction between “hard” and “soft” infrastructure. If we can abstract from the recklessness of multi-trillion-dollar plans, the distinction itself makes sense. For decades now, the economy has been evolving to more of a knowledge economy. This is evidenced, for example, by a growing proportion of intangible relative to tangible assets. In order to nurture such an economy, it is important to provide critical infrastructure – which is increasingly of the softer kind.

Inflation

87% of Americans are worried about inflation

https://www.axios.com/inflation-household-spending-fed-31dc35f8-3548-48c8-8f40-b06cec19a126.html

“The problem is that wages are not rising along with prices and most Americans don't expect that they will in the future.”

“The New York Fed's survey of consumers finds that while inflation expectations are the highest in 7 years, at 3.2% for one- and 3.1% for three-year-ahead timeframes, expectations for household income growth remain at 2.7%, below where they were in January 2020.”

This is how inflation starts: Prices go up on a number of items that people buy regularly. Then, people extrapolate those prices into the future and start wondering how they will be able to continue paying for everything.

A big part of the concern is on the wage side where a lot of workers have very little ability to negotiate pay raises to keep up with increasing household costs. People who have assets are much less affected. Those with homes, for example, can take out home equity loans to finance additional spending.

This is where the rubber hits the road with inflation. If wages start going up, especially for lower income workers, spending will continue at a similar pace and the cycle of inflation will continue. If wages don’t rise to meet higher costs, spending will have to adjust downward.

Perhaps we have some early insight into the answer to this question in the graph below. The number one reason businesses expressed for not spending on capital expenditures was the lack of need to expand capacity. The commonality of that explanation actually increased from the third quarter of last year to the first quarter of this year. This is NOT the kind of response one would expect if underlying demand was raging and capacity was systemically constrained.

Manheim Steamroller

https://www.epsilontheory.com/manheim-steamroller/

“Common knowledge among investors, allocators and business operators nearly always frames the proper response to inflation in terms of price direction. We want to know which assets will win if prices begin a steady rise upward, or if prices of a particular good, commodity or service are likely to spike … What that narrative misses, however, is the importance of sensitivity to price volatility in a path-dependent world.”

Great points by Rusty Guinn at Epsilon Theory. The main one is that the volatility of prices is also an important factor, not just the direction. Any business or consumer making decisions must evaluate not just direction of prices, but also timing. Being too early or too late to a big pricing move can be more destructive than being wrong on the direction of the move.

As a result, volatility incurs costs. You need to do more research to have an idea of what is happening with prices. You might look shop different vendors. You might want to get some insurance to protect against being wrong. You might consider alternatives. These all take time and/or money. One of the reasons high inflation from the early 1980s took so long to dissipate is because investors and consumers were all too aware of what could happen with prices.

Gold

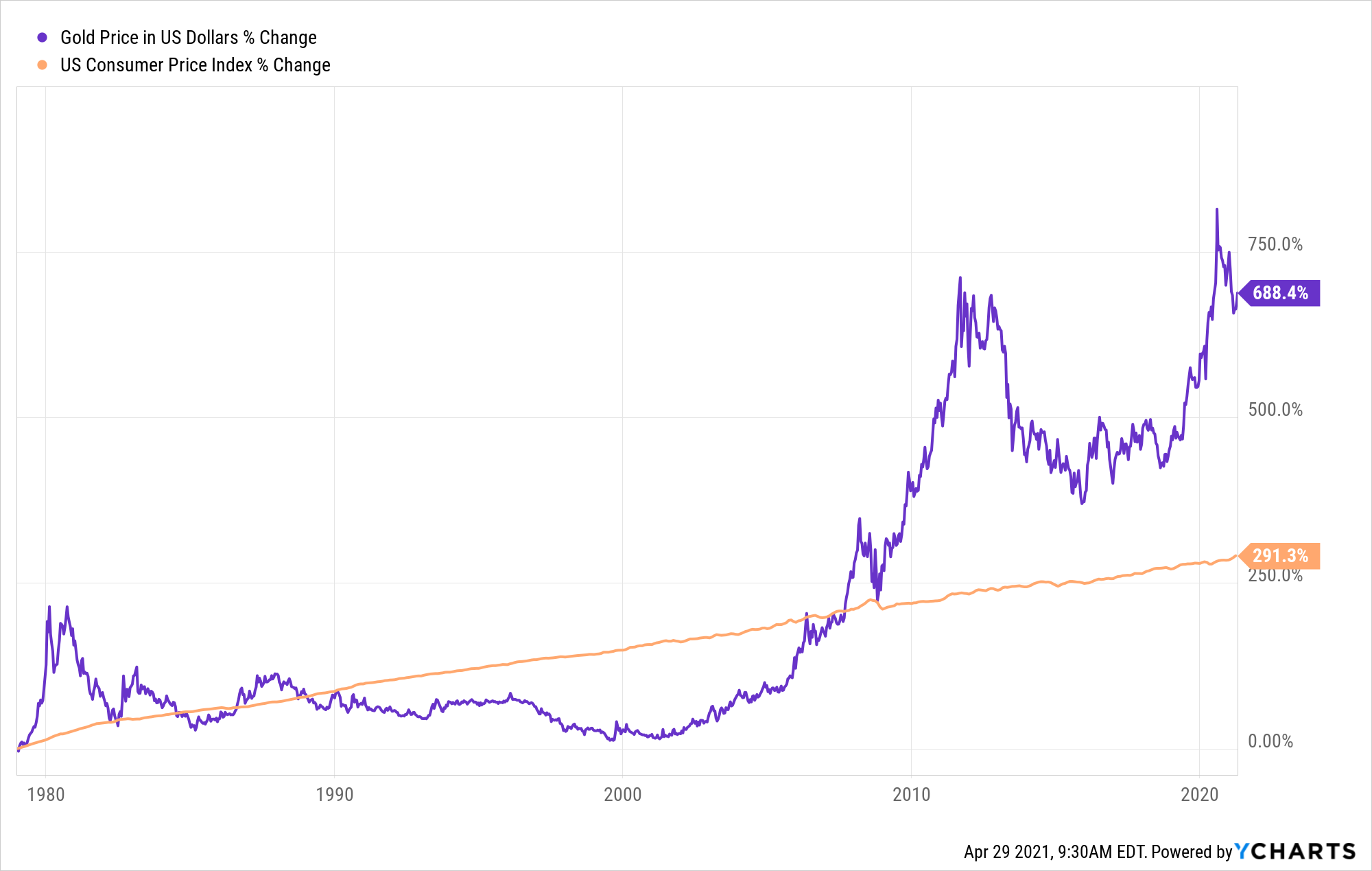

One of the main reasons cited for investing in gold is as a hedge against inflation. While this is a fair assessment, it can cause some confusion. After all, the long-term chart of the price of gold and CPI (above) shows periods of substantial deviation between the two. However, what can also be seen in the chart is that gold does rise over time to maintain pace with the CPI in a general sense, but it only does so episodically.

This highlights an important distinction. Since CPI is measured and reported on a monthly basis it does a better job of tracking short- to mid-term price changes. Gold, on the other hand, does a better job of tracking big, step function, fundamental changes. In this sense, it is probably more useful to think of gold as a hedge against devaluation.

While there are a lot of different things that could cause a significant devaluation, it is easiest to think of the risk in terms of the financial system “breaking”. With massive amounts of leverage around the world, there is little debate that such conditions cannot be sustained. The only mystery resides with the “How” and the “When”.

These types of events don’t happen frequently across history, but they do happen regularly. When they do, they re-order the ranks of wealth. As a result, gold is a useful insurance policy against such upheaval.

Decision making

Why people forget that less is often more

“A paper published in Nature suggests that humans struggle with subtractive thinking. When asked to improve something—a Lego-brick structure, an essay, a golf course or a university—they tend to suggest adding new things rather than stripping back what is already there, even when additions lead to sub-par results.”

More specifically, the set of observational studies showed that when tasked with improving a situation, 78% of people favored addition even when subtraction was equally effective. This is one of those tidbits that can be useful to keep in mind. For example, investors often add interesting ideas to portfolios as they come across them but end up with an eclectic mix of assorted securities with no clear objective. It can be quite useful to review and prune holdings that no longer make sense.

Implications for investment strategy

Major headwinds for the S&P 500 above the 3,900 level as a rising real yield causes P/E to fall hard ($)

“Despite superior Nifty Fifty EPS growth, the Nifty Fifty stocks lagged the S&P 500 in 1973-82”

Barry Bannister, the market strategist from Stifel, presented to the CFA Society Baltimore a couple of weeks ago and highlighted this important market lesson from the 1970s. According to his report, the median Nifty Fifty company grew eps at over 10% per year but returned only 3.1% per year over the ten-year period. The rest of the S&P 500 grew eps at 7% but returned 6.7%.

The lesson is classic one: When multiples get too high stocks can underperform even if earnings continue to grow. Valuations matter.

Bond investing needs a complete rethink ($)

https://www.ft.com/content/c8c15f2a-174f-4550-99e8-c4b79ec12d4f

“I [Dan Fuss] managed fixed income investments from 1958 until earlier this year, riding one of the greatest bull markets in bonds. Managing any portfolio now requires a complete rethink. There are lessons from the past but their overlap with the present and the future has diminished a lot.”

“But leverage depends on confidence. Should confidence start to unravel, the excess liquidity would rapidly depart. Central banks are watching this carefully but might not be able to control it.”

Dan Fuss has been around for a long time and has strong history of straight talking about market trends and strategies. As a result, his warning that bond investing needs a “complete rethink” should be taken seriously. He concludes since the long ride of rate declines is over, “the need for focused credit research is essential.”

This is especially interesting because it dovetails nicely with Mohamed El -Erian’s recent insights from the FT: “It became clear last week that private lenders to some of the most vulnerable developing countries do not share the sense of urgency about the risk of sovereign debt traps that is felt in governments and multilateral institutions.”

The top-down message is the same: After years and years of central banks jumping in to save investors whenever the going got tough, neither Fuss nor El-Erian seem to believe this will continue. In an environment of such excessive leverage something will eventually break. Assuming central banks do not nationalize all debts, at some point they will have to decide who they save and who they don’t. In other words, there is likely to be something of a Lehman moment at least insofar as a line is drawn.

This will be interesting to watch unfold. Some narratives suggest monetary policy killed the debt default cycle, but it seems more like it was just put on pause. If this is correct, weak credits will eventually, and perhaps suddenly, succumb to the pressure. The case of Toys ‘R’ Us bonds which I mentioned in a blog post may be instructive. With financials in disarray in the summer of 2017, the bonds nonetheless skated through the summer of 2017 with prices around 95 cents on the dollar. By the middle of September, the company was bankrupt.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.