Areté's Observations 7/2/21

Areté (Pronounced ar-uh-tay) 1. Goodness or excellence of any kind. Fulfillment of purpose or function, the act of living up to one’s potential. 2. Effectiveness, knowledge.

Welcome back!

It has been mostly a quiet week as the markets will be closed on Monday for the holiday and many people are taking the opportunity to take some time off. Investors are also largely on cruise control until later in the summer when central bankers convene for the Jackson Hole conference.

In the meantime, have a happy Fourth of July!

If you have any comments or questions, please reach me at drobertson@areteam.com.

Market observations

One of the more interesting phenomena to emerge in the last several weeks is the strength of the US dollar. After reaching an interim peak right at the end of March, the dollar had sold off on concerns of the economy overheating and fiscal spending gone wild. Shorting the dollar became a popular hobby.

The last few weeks have put a screeching halt to those theories as the dollar has rebounded strongly. The turnaround is due partly to a pause in the reflation trade but is also a reflection of the easing of overly negative positioning in the dollar. Since the dollar’s value affects every other asset class this will be worth keeping an eye on.

Almost Daily Grant’s, Monday, June 28, 2021

https://www.grantspub.com/resources/commentary.cfm

“’We’re all drowning in work,’ Matthew Kennedy, senior IPO market strategist at Renaissance Capital, tells Axios. ‘I know the virtual roadshows of some sizable deals are sparsely attended since fund analysts only have so much time. And we’ve definitely noticed an uptick in prospectus typos’.”

The beat goes on as the IPO machine continues to crank away. A strong IPO market is usually very positive for the overall market as it takes quite a bit of risk-seeking behavior to invest money in companies that have no public track record. While I suspect there is a fair amount of truth to this, I also suspect the IPO market may be getting an extra boost from retail investors who are looking for speculative opportunities.

Labor

Why jobless claims have become a useless economic indicator

https://www.axios.com/jobless-claims-data-unreliable-827dd721-c8d7-4466-acf5-64f514eafb65.html

"[F]ilings can be impacted by a range of different factors and we think the data could be particularly noisy now that some states have started reducing the programs available for benefits and more states plan to do this in the coming weeks," wrote JPMorgan economist Daniel Silver on Thursday.

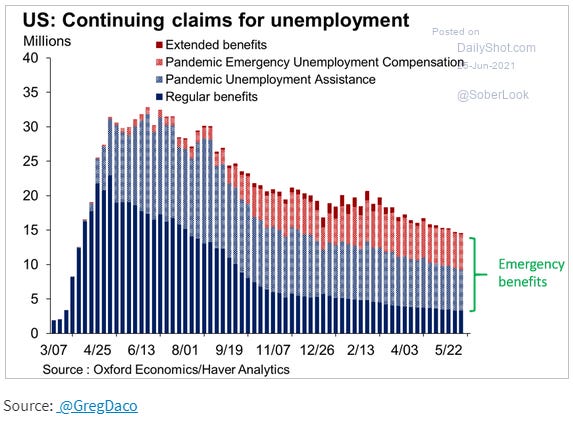

The prospect of noisy data mentioned above is illustrated in spades in the graph below. As various emergency benefits are ended, the rolls of unemployment beneficiaries will decline substantially. This will create a fairly short window during which a lot of people will restart job searches, but a lot of others will drop out of the labor force altogether.

The Economist highlighted one of the complicating factors: “But there are ever fewer temporarily laid-off workers waiting to be brought back … Meanwhile, workers who have permanently lost their jobs, who made up just 9% of the unemployed early in the pandemic, now represent about a third of all those out of work.”

While somewhere in the neighborhood of 10 million people are figuring out what they are going to do, the Fed will need to determine how much slack exists in the labor market in order to calibrate monetary policy. The potential for miscalculations amidst all the noise is considerable. For example, it is not hard to imagine unemployment declining rapidly as benefits expire. If that happened, it would be very difficult for the Fed to forestall the withdrawal of emergency monetary measures.

Coronavirus

The coronavirus has largely been out of the news which has been good news. There are places where infection rates are increasing again, however, and most of this is due to the newer Delta variant. While it does not appear as if these instances are sufficient to derail global economic recovery, they are sufficient to significantly impede progress in the countries and regions where the variant is dominant and where vaccination rates are low.

This uneven success in coping with the coronavirus provides two mild warnings. One is it is still to early to declare victory. The effects of coronavirus will be around for a while, and it is likely pockets with high infection rates will pop up here and there. As a result, supply chains and travel plans are still at risk of being disrupted.

Source: themarketear.com

Social media

Can Our Culture Escape the Twitter Doom Loop? ($)

https://frenchpress.thedispatch.com/p/can-our-culture-escape-the-twitter

“The continued unity of the United States of America cannot be guaranteed.” Why? Because “at this moment in history, there is not a single important cultural, religious, political, or social force that is pulling Americans together more than it is pushing us apart.”

“Since Twitter is based around the snappy retort, it encourages drive-by snark, insults, and lies. The target thus faces a constant dilemma. Engage with the snark, and you elevate the snark—but without enjoying the benefit of being able to develop an argument or fully rebut the lies.”

I agree with several of the points French makes here. For example, I agree “when like-minded people gather, they tend to grow more extreme.” I also agree “Twitter is the dominant platform for cultural, political, and academic elites to converse with each other.” As a result, I agree with his assessment that “the folks who are squabbling like children (and often deeply wounded and hurt in real life) are people with real power and influence.” In other words, “the Law of Group Polarization is playing itself out in public”.

What I don’t necessarily agree with (and I would love to hear other thoughts on this!) is the conclusion there aren’t any forces that are pulling Americans together more than are pushing them apart. While concepts such as “human decency”, “conflict avoidance”, and “peace and quiet” may not be easily categorized as political or social “forces”, they do rank as individual motivations. Further, there is nothing like powerful and influential figures demeaning themselves in public to significantly undermine their power and influence.

This doesn’t mean I don’t have serious concerns about divisions in the country (I do), but I also repeatedly experience and observe people being decent to one another in real life too frequently to believe the fabric of society has been completely ripped apart. That belief seems to derive from overconsumption of social media.

To that point, I do believe that social media has significantly underperformed initial expectations of what it could be. I don’t view this result as a function of people becoming nastier or of any major trends in the country. I view it as a result of social media companies monetizing their platforms primarily through advertising and of exceptionally weak governance of the platforms. What you get under these conditions are companies incentivized to incite conflict and engagement – so they do. If we want better results from social media, we either impose more stringent governance standards, pare back our use of social media, or both.

Regulation

Facebook rulings spark bipartisan calls for US competition law change ($)

https://www.ft.com/content/34e6028d-8d78-4670-9799-c374db47bd20

“[W]hatever it may mean to the public, ‘monopoly power’ is a term of art under federal law with a precise economic meaning: the power to profitably raise prices or exclude competition in a properly defined market”

The ruling by Judge James Boasberg in regard to an antitrust case against Facebook took on different meanings to different players. Facebook stock popped on the case’s outcome which the judge ruled as “legally insufficient”. Others, however, viewed the loss as a necessary impetus to further the strategic goal of rethinking and updating antitrust policy. If this is the case, and I suspect it is, then Facebook and BigTech won the battle, but will have a much tougher war at hand.

Regulators begin to grapple with DeFi ($)

https://www.ft.com/content/e6e7d9d6-7778-4286-ba6f-e5831fcbc538

“’There’s so much happening so quickly that regulators just cannot respond, as a practical matter,’ said Lewis Cohen, a partner at DLx Law, a cryptocurrency law firm. Cohen compared the boom in DeFi to a ‘giant DDoS attack on global financial regulation’, referring to a kind of cyber security assault where hackers overwhelm their targets with huge volumes of activity.”

The tale of regulators being at least half a step behind the wiliest of perpetrators is well-worn and too often fairly accurate. As the technology life cycle accelerates, however, the lag is increasing to a degree that renders regulators nearly helpless in many scenarios.

This is unfortunate. While I am no fan of over-regulation, I also believe some degree of legitimate oversight is necessary to ensure free and fair functioning of various markets. If it is not fair, people will avoid it. The Food and Drug Administration (FDA) which was established to make the food and drug products of the early 1900s, which were wildly variable in quality, safer for human consumption. When consumers realized they could trust packaged food and drug products to a much greater extent than in the past, industry demand exploded. Today’s technology businesses should consider the lesson.

Get ready for years of new tech regulations

https://www.axios.com/microsoft-big-tech-regulations-7d1565a1-c807-4006-bda0-4920a2f01427.html

"’As I sometimes put it inside the company, the 2020s will bring to tech what the 1930s brought to financial services,’ Smith says, noting that era brought a wave of new U.S. laws that created multiple new oversight agencies.”

“Smith sees opportunity in all the new laws, especially because they won't just affect tech giants, but also all the companies who rely on the tech giants' services.”

The potential for greater regulatory oversight has been brewing for years now and these comments by Microsoft president, Brad Smith, provide some perspective. One point is he see a whole new “wave” of laws coming that will be aimed at tech companies. Another point, however, is regulation isn’t inherently bad. To the extent it increases fair play it helps (almost) everybody.

Books

Alpha Trader, by Brent Donnelly

“You will never see a headline like ‘USDDAD rallies as macro portfolio manager stops out of huge short because he’s going on vacation’.”

I don’t normally read books about trading but this one came highly qualified and did not disappoint. As much as anything the book is about decision making with imperfect information and therefore speaks to my work in investment research and portfolio management as well as to many other professions. The insights about trading came as a bonus.

Much of the book revolves around concepts in behavioral finance which I thought might be somewhat tedious since I am already well-versed in those theories. To my pleasant surprise, Donnelly was extremely economical in his description of the theories and instead spent his time on their application in real situations. In doing so, his level of self-awareness and brutal honesty about his own shortcomings were both disarming and highly effective. It is important to understand bias cognitively, but it is also important to be able to correct for it practically.

To that point, one of the best lessons in the book is the observation, “once you have a position on, you are a steaming hot bias stew”. This is a representation of the endowment effect and is striking because we all have “positions on” in some sense: We have advocated for a project at work, we decided to buy something expensive, or we made a decision that affects people we care about. As a result, Donnelly’s advice to account for our biases ranges well beyond the trading floor.

I also liked the quote above because we encounter headlines that attempt to explain things every day. Donnelly’s main point is those headlines are just story lines that strive to manufacture drama. Oftentimes, however, the real reason prices move is completely mundane and uninteresting. The main point is there is a lot of noise in market prices, and it is important to not read too much into price activity.

I should also mention the book is also an excellent introduction to trading. In a market in which prices are almost completely severed from cashflow-based valuations, trading insights matter more than usual for interpreting day-to-day activity. As a result, the book is useful to anyone interested in investments. I wish this resource had been available when I started my career.

China

China and America are borrowing each other’s weapons ($)

https://www.economist.com/china/2021/06/17/china-and-america-are-borrowing-each-others-weapons

“on June 10th, China’s legislature passed a law that allows the government to take action against individuals and companies for complying with other countries’ sanctions against China.”

It’s one thing that the world’s two most powerful countries are becoming more hostile to one another. It’s yet another thing that they are forcing others to take sides. Thus far, it has been possible for countries and companies to exercise diplomacy in order to continue enjoying the best of both (east and west) worlds. That idyllic condition increasing looks like it has a “use by” date attached to it.

It will be interesting to see how far the implementation of these policies will go. Will companies like Apple and Tesla be forced to adhere more rigidly to Chinese rules? Will eurozone members be forced to pick sides? The competition between China and the US promises to be a lasting drama.

Emerging markets

Emerging markets, the Fed, and the virus

https://www.ft.com/content/2b0d7d9e-819e-4e3b-b88d-0a2f6418b838

“In the past decade or so, currencies have given EM investors a rough ride. But recently a soft dollar, negative US real rates and a recovery in commodities prices (among other factors) have broken that pattern. As ever, the index conceals a lot of complexity.”

“What that rather confusing collection of lines tells you is how much the MSCI index is weighted towards China, and to South Korea and Taiwan, two countries that play an important role in Chinese supply chains.”

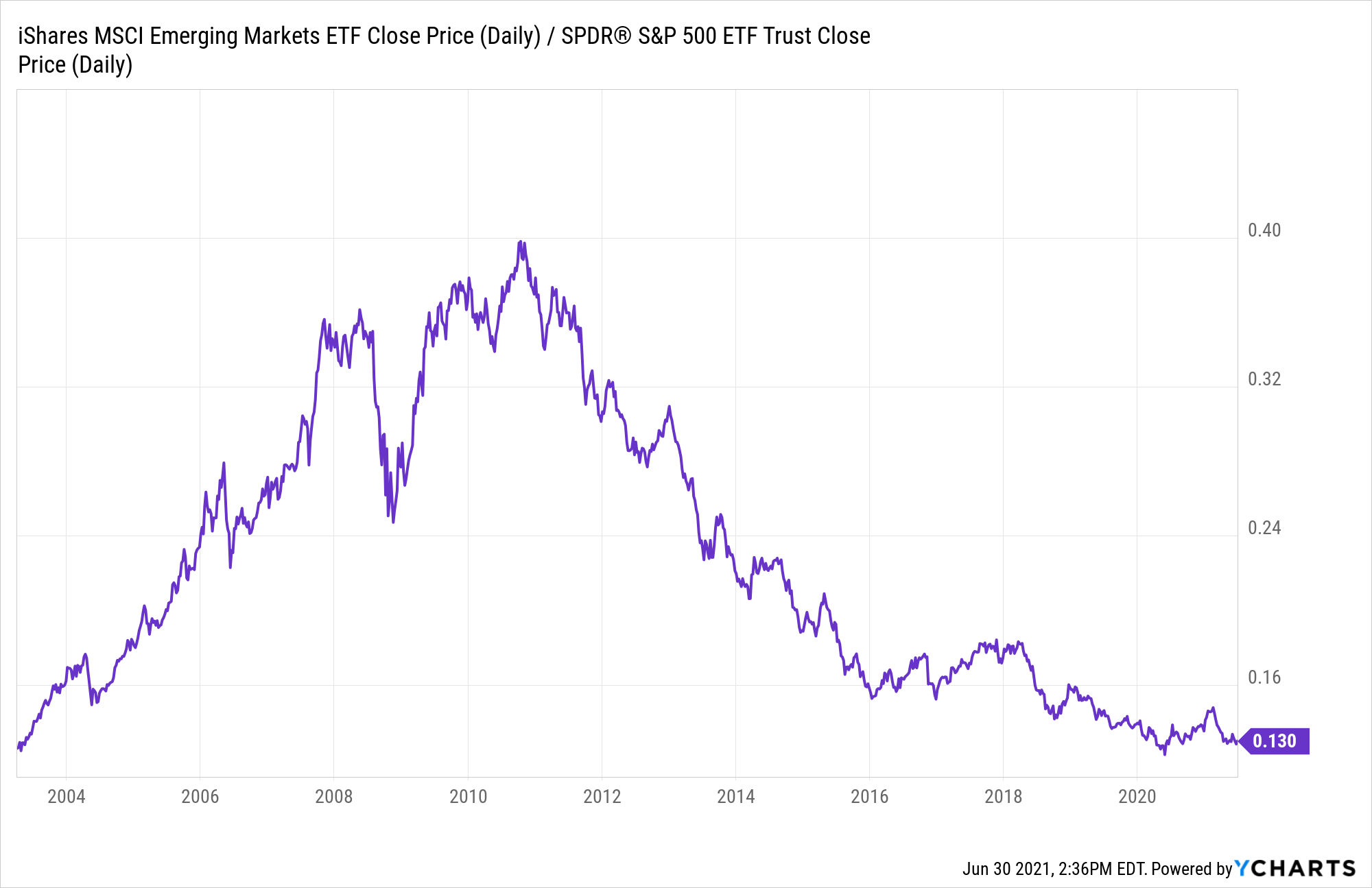

Ah, the allure of emerging markets! They were a darling trade last year and well into this year and then, poof, there was a “terrifying ‘sudden stop’ in capital flows” as reported by Robin Brooks at the Institute of International Finance. Currencies are part of the equation for emerging markets, but so is debt, commodities prices, capital flows, economic development, geographic representation, and a host of other factors.

Jeremy Grantham spoke to the virtues of emerging market exposure last week which is always an opinion to be seriously considered. As it turns out, emerging market value stocks are the only asset class his firm GMO expects to have positive returns over their forecast horizon of seven years. Slim pickings indeed.

I have to admit I have a hard time getting to the same level of enthusiasm Grantham has for emerging market stocks. I completely get the value part, and a quick glance at the graph comparing emerging markets to the S&P 500 shows ten years of underperformance which should spark some “mean reversal” reflexes.

I have some serious reservations, however, which parallel my reservations about the value style in general. The main point is things changed in 2010 when the Fed essentially made “emergency” monetary measures permanent by continuing them long after recovery from the financial crisis had taken hold. In short, the level of continuous monetary interventions substantially eliminates the types of free market incentives that enable “value” to work. I expect this pattern to continue until either central banks withdraw their unusual support or until inflation destroys the effectiveness of those policies.

Inflation

One positive indicator on the inflation front is a marked reversal in the price runups for a number of commodities. Lumber is pictured here but similar action has occurred across the commodity spectrum. In the short-term, this provides reassurance that prices are not spinning out of control.

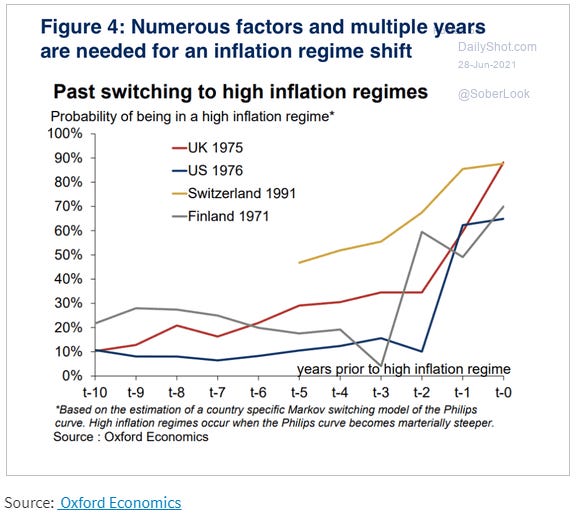

None of that means we are out of the woods yet. As indicated in the graph below, it takes time for an inflation regime to shift. This shouldn’t be too surprising. Businesses, after all, have lots of levers to pull to forestall having to raise prices. Consumers also have levers to pull. They can forestall purchases and they can employ cheaper substitutes among other things. It is only when the room for adjustment by these means runs out that prices need to be raised.

The good news is we are not at that point yet. The bad news is signs are pointing in that direction. As a result, investors may have something of a reprieve here where they can prepare for the prospect of higher inflation down the road without having to scramble and overpay for that protection.

Implications for investment strategy

I always try to put things in perspective but right at the end of the quarter and after a year and a quarter of dealing with the pandemic it seems especially important to do so now.

To this point, one of the quotes that jumped out at me from the In Gold We Trust 2021 report by Incrementum was, “the vast majority of people are actually savers as opposed to being real

investors or traders”. I think there is a lot of truth to this. Most people want their money to work for them but have no interest in taking big risks or experiencing big volatility. When I talk about “long-term investors”, this is what I mean. I am referring to people who are saving for retirement or some similar goal and would experience great hardship if they suffered significant permanent losses.

One of the great challenges when rates and volatility are suppressed and asset prices are inflated is markets in risk assets appear as a wolf in sheep’s clothing. Their serene and unthreatening appearance belies their much more vicious nature. This can tempt more risk-averse savers into assets and markets that are inherently much riskier than they appear.

This creates quite a quandary for long-term investors. As tempting as it may be to chase returns, it is important to have an idea of the risk that is involved in doing so. Unfortunately, one of the most important consequences of this monetary policy regime has been to obscure risk. I have absolutely no problems with people who want to take investment risks, even huge ones if it makes sense for them. The bigger question is, “Are those risks right for you?” In other words, “Are you more of a saver or a trader?” In my opinion, savers should be very wary of the excessive valuations in stocks.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

One goal of this letter is to provide fairly dense information content – so you don’t waste your time filtering through a lot of fluffy verbiage. A consequence of that decision, however, is sometimes things may not be as understandable as they could be.

If you have a general question that may also be useful for others to know the answer to, please make a comment in the newsletter and I will do my best to answer the question or make a clarification. If you have a more specific question, please send it to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.