Areté's Observations 7/23/21

Areté (Pronounced ar-uh-tay) 1. Goodness or excellence of any kind. Fulfillment of purpose or function, the act of living up to one’s potential. 2. Effectiveness, knowledge.

Welcome back!

The lazy, hazy, crazy days of summer are with us, and the market has certainly picked up on the crazy part. I hope you are staying sane and enjoying the summer!

If you have any comments or questions, reach me at drobertson@areteam.com.

Market observations

On Monday, the 10-year Treasury yield continued to fall by dropping 12 basis points (which is a lot) and the stock market tanked. Theories swirled about the causes. On Tuesday, the market stormed back and recovered everything it lost on Monday. One thing I am pretty sure of is this is not evidence of perfectly efficient markets.

Several data points suggest much of the buying on Tuesday was retail investors buying the dip. If so, this could provide some interesting insight. If retail investors are buying dips dogmatically, without regard to other inputs, that would leave them vulnerable to a regime change of sorts. As it happens, the outline of such a change is already starting to emerge …

Third time's the charm - most shorted trying to say something? Jul 16 2021 at 19:00 ($)

“The aggregate psychology of the fast money trading the underlying names in the most shorted basket is basically the market psychology on steroids. As we showed a few days ago, big moves lower in the most shorted basket have eventually been followed by the overall market. SPY with a lag and QQQ with almost no lag. Did we just starte [sic] the ‘catch up’ trade?”

If this thesis is right, the big move lower in most shorted stocks forebodes a meaningful decline in the broader indexes. Monday’s decline seemed to confirm the hypothesis, but the performance for the rest of the week rejected it.

Regardless of the outcome, John Hussman provided some useful insight into that aggregate psychology in his latest commentary. The key thing to understand is: “Every eager buyer must find a seller. Every eager seller must find a buyer. Either way, the buying always equals the selling. It’s not ‘money flow’ that moves prices around. It’s eagerness.” So, let’s see how long that “eagerness” persists.

Labor

Mediocre workers have nowhere to hide ($)

https://www.ft.com/content/33ecd973-30ce-4d8e-8529-d9db4c023f42

“’Mediocrity hides in offices,’ he [Max Thowless-Reeves] said, adding it was easier to identify which staff added the most value when all were working remotely.”

“’You can see everyone typing away on the same document [in Google docs],’ he said, adding that this meant you could also see who responded snappily to a query, or made a useful suggestion, or generally contributed — and who did not.”

Everyone is familiar with various office personas. There is the brown-noser who always agrees with the boss. There is the affirmer who always agrees with what has been said and then tries to add a tidbit to the discussion to sound like they are contributing. There is the “creative” wild hair who always seems to be in a different universe than everyone else …

As dysfunctional as all of this sounds, the behavior flourishes in offices because it works. This reveals a deeper truth of office life: It is not a pure performance derby for advancing the organization but a political derby for instilling positive perceptions among superiors. Thowless-Reeves just happened to discover this reality through the serendipity of remote work.

No doubt other companies are making similar discoveries as well. It will be interesting to see to what extent performance reviews and hiring practices evolve as organizations learn more about which people are “really driving them forward”.

Economy

The two big reasons to doubt the global boom ($)

https://www.ft.com/content/e8fc84b4-7faf-4e15-bfc2-8f51874d5daa

“In the US, the last major episode of forced saving came under rationing in the second world war. America won and, rather than spend wildly after the war, Americans sat on those extra savings for years. Conditions are similar now. Americans have chosen to spend only about a third of their pandemic stimulus checks, saving or paying down their debts with the rest.”

“The US is also approaching a ‘fiscal cliff’. New government spending will plummet sharply in coming months. Most economists are banking on extra strong consumption growth to pick up the slack. But history is not on their side. After a stimulus sugar rush, growth tends to fall back quickly.”

I don’t think these comments are very reflective of consensus right now but there is plenty of truth to them. As a result, these comments reveal something important: There is enough uncertainty and enough moving parts in any economic forecast to prevent a highly probable conclusion. As this uncertainty becomes manifest, I would expect the reflation/reopening trades to continue to weaken.

On another somewhat related note, I have mentioned several times that unique pandemic conditions undermined the reliability of many economic statistics. The chart below shows the length of recent recessions as called by the NBER. The fact that the pandemic recession was called at just two months long goes to show how grossly misrepresentative economic statistics can be.

Coronavirus

Markets Are No Longer Worried About Inflation ($)

The graph below by John Authers at Bloomberg provides a quick and dirty depiction of Covid fear. Clearly there has been a significant tick up recently and to levels not seen since early in the year when vaccinations were just starting to get rolled out. While increasing concern about Covid may well explain part of Monday’s market swoon, it makes Tuesday’s recovery all the more mysterious.

Social media

To curse social media is to exonerate society ($)

https://www.ft.com/content/760b7fd6-63f7-4915-a695-c1f68445d633

“What remains is social media as a cipher for a harder-to-discuss problem. This is human credulity: the demand for nonsense, not the supply of it.”

“The result is that weird tic in which social media users are discussed as if they were passive victims of demonic possession. The implication, that they would be model citizens were it not for the apps, slips by unquestioned. The politics is impeccable. It is safer to challenge a business than the public. But if the point is to fathom the problem, the evasion becomes self-defeating.”

The main point Janan Ganesh makes in this article is the “crusade” against social media “has become a way of dodging the age and depth of civic rot”. This is a hard pill to swallow but there is a lot of truth in it, and it deserves a hearing.

As Ganesh highlights, the politics of blaming a proximate cause in order to avert serious inquiry into the ultimate cause is “impeccable”. That course, however, necessarily serves as a distraction that forestalls any kind of meaningful or lasting improvement. The better questions, which each of us can be asking ourselves, are, “What are the underlying causes of this civic rot and what can we do to make them better?”

China

The graph below illustrates the stunning change in air traffic from China to the US over the last two years. Although pandemic restrictions were certainly part of the cause, this vivid pictorial also captures the more abstract themes of worsening geopolitical tensions and increasing regionalization. Yes, there will be consequences.

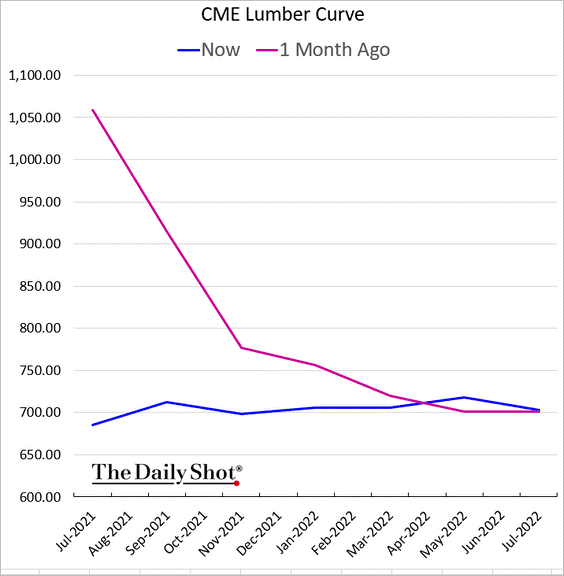

Commodities

Lumber is one example of topsy turvy commodities but there are many. While current (spot) prices are falling back into a more normal range, this is a recent phenomenon. On one hand, such volatile prices demonstrate the value of patience. If you can wait a few months to build a house, you can save a ton of money. If this is an anomalous, one-off event, it is hard to call it especially inflationary.

On the other hand, however, the wild swings in prices impose costs on both providers and consumers in the form of heightened uncertainty and opportunity costs. These aren’t always trivial. To the extent the costs are fairly significant and recur, they can lay the groundwork for future inflation.

Inflation

The other kind of Fed mistake ($)

https://www.ft.com/content/79269662-ba90-4b0b-a0a0-4a640db8c85a

“He [Rick Rieder] emphasised that there were three things he was worried about: inflation being stickier than expected (he’s looking closely at the way service industries are passing on costs to consumers); higher prices for basics like food turning into a regressive tax that ultimately kills demand; and high asset prices stifling certain markets, as in the housing example.”

With food prices remaining elevated and home prices beginning to deter new buyers, Rieder seems to be batting two for three so far. I think the line of thinking is right and one that doesn’t get enough attention. You can’t control inflation like a thermostat by setting the temperature just a degree or two warmer or cooler. As a result, when the Fed tries to increase inflation, it creates conditions under which some prices spike wildly.

While much of the crash in Treasury yields has been attributed to the delta variant, I suspect a lot of the reason is also increasing concerns about economic growth in light of regressive taxes and slowing demand for new homes. This is still very early days in what promises to be a long story with a lot of twists and turns.

And, for an added degree of difficulty, Robert Armstrong made an interesting suggestion in his daily newsletter on Wednesday. He suggested the possibility that “inflation is just the kind of thing that Republicans think Democrats will make happen, but not visa-versa.” I had not thought of that, but it makes a lot of sense. Insofar as this is the case, any measurement of inflation expectations must also be calibrated for political leanings then.

So, just to keep the inflation story in perspective, I will summarize: Inflation is a process that is built on expectations. Those expectations are a function of several things including the persistence of supply chain bottlenecks and the degree of belief in the level of government spending and on the nature (i.e., productivity) of that spending. Given very different perspectives on these items, it is fair to expect it will take time for overall expectations to converge.

Cryptocurrencies

My wild ride into the cryptosphere ($)

https://www.ft.com/content/3dd0d341-aeb4-48fe-b427-16af47211652

“Here are the steps: register with a crypto exchange platform (such as Coinbase), link to a bank account and transfer money (using the financial app Plaid), buy ethereum (the second-largest cryptocurrency, known as ether or ETH), transfer ether to a crypto ‘wallet’ (MetaMask), and then exchange ether for ‘wrapped’ ethereum, or wETH, a version of ether that, at least for now, is more seamlessly tradeable via the common standard known as ERC-20.”

“If you haven’t traded crypto before, each step feels like a leap of faith.”

A couple of points struck me about this meandering, but pretty useful, overview of cryptocurrencies. One is the limitations of the claim decentralized finance (Defi) can improve the inefficiencies and opacity of the current system of financial intermediaries. While there is loads of potential for improvement and disintermediation, the claim crypto is more useful than cash strains credulity.

Transacting in crypto requires five steps just to enable a transaction. Cash requires none. All you have to do is pay cash … and receive the product or service. Crypto advocates fear (rightly I believe) the longer-term potential for the US dollar to lose value. However, each step of trading crypto requires a “leap of faith”. Finally, the potential for Defi to reach a significant portion of the 1.7 billion people for whom establishing a bank account is too arduous seems quite a fantastic leap itself.

Another point that strikes me is how the narrative around crypto, in particular, has become much more negative. I’m sure some of that is just easier now that bitcoin is down 50% from its highs, but there is a broader effort at work here. The governments of the US and China have issued serious warnings about crypto and where major newspapers used to fear backlash from crypto zealots, they now seem far more comfortable propagating stories about links to organized crime and incredibly high energy consumption. While I have my own ideas about how these factors net out, what is really important is the narrative around crypto has changed for the worse.

Monetary policy

The BRRR Index

https://fedguy.com/the-brrr-index/

“Asset prices rise when there is more money in the system, but you have to understand what ‘money’ is. M1/M2 is not a good measure as it is heavily influenced by Fed policy, which changes the composition of money rather than the overall quantity (see here for a walkthrough).”

“The goal of QE is to lower interest rates, with the increase in reserve assets/deposit liabilities in the banking system largely incidental. As astute market participants have understood, Treasuries appreciate in value when the rates are lowered, essentially increasing the amount of money in the system. This money can then be pledged to buy equities or sold to buy bigger yachts.”

I came across the blog posts from Fed Guy through a reference from Robert Armstrong in his daily “Unhinged” email letter for the FT. It is by far the most lucid, clearly written, and understandable exposition I have come across regarding monetary policy and the inner workings of money markets.

Increasingly, this is very useful insight to have. Continued interventions and multiple initiatives combined with ever-changing regulatory mandates have transformed money markets into very different creatures from fifteen years ago. Further, constantly changing policies and reactions to problems cascade through the system creating new problems and new reactions. The result is something of a monetary Frankenstein.

For these reasons, money markets are also the machinery from which liquidity shortages often emerge that cause bigger ructions through the stock and bond markets. If you are curious about learning more how this system works and how problems arise, I highly recommend checking out fedguy.com.

Implications for investment strategy

This Cult Classic Buy Signal Isn't to Be Trusted ($)

“In the decade since [the financial crisis], however, buying of bonds has been so heavy that the spread of fixed-income over dividend yields has never returned to anything like what we previously regarded as ‘normal.’ The lines crossed a few more times, and then last March, dividend yields again soared far ahead of bond yields. The two incidents are marked on the chart:”

“Is there any way to turn this into a timing strategy in real time? It turns out that there was. There have only been two occasions when dividend yields rose more than a percentage point above bond yields. Both times, once the spread turned, there were no second thoughts.”

“Now we come to the awkward part. As of this moment, dividend yields have overtaken bond yields once more. Last year and in early 2009, this was a moment driven by a historic collapse in share prices and a wave of risk aversion. This time around, it’s happened just as the U.S. stock market is setting yet more all-time highs.”

This outline by John Authers at Bloomberg certainly highlights a quandary many investors are facing. In an investment world dominated by stocks and bonds, relative yield is a quick and dirty way to help identify opportunities to tilt the balance from one to the other.

Authers broaches the right issue by effectively asking the question, “Does the relative yield rule still apply when both stocks and bonds are fantastically expensive?” The answer is maybe, for a while. For funds with a mandate to hold only stocks and bonds, there isn’t a choice; they must own both. As a result, there will be buyers regardless of how high prices go and a choice must be made.

This points to one of the most time-honored patterns in investments though. Just as soon as you impose artificial constraints on what you can do, markets will evolve to prevent you from doing what you know you should be doing. I was a tech analyst on several funds during the internet boom in the late 90s and some of the funds had mandates to hold exactly as much tech as the benchmark. It was obvious to me most tech stocks were hugely overvalued, but I had to recommend something. In a situation like that, there is just not a lot you can do when the entire tech sector crashes.

The lesson for today is many investors are setting up for a similar fate. They are getting channeled into stocks and bonds despite the abysmal expected returns for both. The only good answer is to find a third way. Part of that alternative universe includes cash, part includes gold, and part involves other non-traditional investments that are either uncorrelated with stocks or even better, negatively correlated. This is a huge focus at Areté right now and I’ll keep you posted along the way.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

One goal of this letter is to provide fairly dense information content – so you don’t waste your time filtering through a lot of fluffy verbiage. A consequence of that decision, however, is sometimes things may not be as understandable as they could be.

If you have a general question that may also be useful for others to know the answer to, please make a comment in the newsletter and I will do my best to answer the question or make a clarification. If you have a more specific question, please send it to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.