Arete's Observations 9/4/20

Weekly observations of the most interesting happenings in the investment environment

Housekeeping

Please note I will be migrating this letter over to a new platform over the next few weeks. Please go to https://abetterwaytoinvest.substack.com and sign up if you would like to continue receiving it. I look forward to seeing you there!

Market observations

Yikes

https://www.hussmanfunds.com/comment/mc200901/

“You know it’s a bubble when you have to edit the Y axis on all of your charts because valuations have broken above every historical peak, and estimated future market returns have fallen beyond the lowest points in history, including 1929.”

“As of August 28, that estimated 12-year total return has declined to -0.95%, easily the lowest level in history.”

I have watched prices continue to surge higher along with everyone else. As a valuation person, I suspect it is a bit more frustrating, because it is so abundantly clear that stocks are not rising on fundamentals. In fact, quite the opposite.

As a result, I have tried to emphasize how crazy the disconnect between prices and underlying fundamentals have become but I keep running out of superlatives. This is why I laughed out loud at the unique way John Hussman captured the phenomenon: he had to edit the Y axis on all of his charts. Any data hound knows that is when you are really pushing the limits!

An Epic Battle Is Raging Beneath The Market Surface

“Keep in mind, if a market maker is selling the call options themselves, they then have to hedge themselves by purchasing the underlying stock. More calls being bought at higher implied volatility levels means the dealers need to purchase more Apple."

“When a parabolic rally like we have seen in Tesla starts to reverse it happens in the fast-money options before the slow-money stock.”

One of the interesting phenomena over the summer has been increased activity in stock options. Although discussions about options can get technical in a hurry, it is good to pay attention because these markets often reveal useful insights.

One of those insights is that a positive feedback loop can be created when excessive interest in call options forces dealers to increase purchases of the underlying stock as a hedge. This is a fairly mechanical relationship that has nothing to do with company fundamentals. As such, the huge rallies can unwind and reverse very quickly.

Another revelation is the information content of the implied volatility metric. This provides a gauge of the exuberance in option markets. As a result, it can not only be a useful leading indicator, but one that can’t be seen from the perspective of stock markets alone.

Credit

Lex in-depth: why rescue finance will slow recovery for businesses

https://www.ft.com/content/3afb13c5-99d1-418f-ad51-33f3d6db81ca

“The enthusiasm of boards and their backers for financial resilience means businesses will simply hold more cash. Returns will be minimal.”

“Mr Astier refers to corporate cash buffers as ‘Covid-19 liquidity funds’.”

The observation is corporate debt is continuing to rise. One interpretation is the new debt is for the purpose of boosting cash buffers and increasing resilience. It is being used to buy some time until things settle down and more normal business conditions return.

Another interpretation, however, is the additional debt is unwieldy and is pushing many companies to the brink. It is not unsustainable and reeks of desperation.

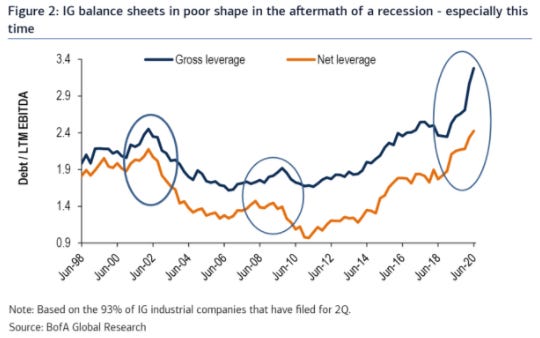

“Points of Return” email by John Authers, 8/27/20

“Starting with investment-grade U.S. companies, judged by their debt as a proportion of earnings before interest, tax, depreciation and amortization, this chart from BofA Securities Inc. shows that leverage has indeed increased dramatically. You would expect corporate balance sheets to be in bad shape in the aftermath of a recession; you wouldn’t expect them to be this bad:”

“The quality of U.S. industrial companies is deteriorating as swiftly now as it was in the earlier stages of the pandemic.”

How this plays out will obviously be important to companies and stocks. It will also figure into the inflation debate. When will company boards feel comfortable enough to release Covid-19 liquidity funds? What needs to happen to get there? What will happen with the funds – will they be spent on profitable projects or returned? The answers to these questions will do a lot to inform the nature and timing of economic recovery. In the meantime, it will be important to keep an eye on credit spreads as a warning of potential danger.

Labor

Although it is good to see the number of temporary layoffs fall significantly (at the far right of the graph), the potential that some portion of temporary layoffs will become permanent lingers. A story I highlighted last week estimated about 25% would eventually become permanent. The chart at the right shows the risks are concentrated in certain industries. The uncertainty this causes continues to grind away.

Risk management

U.S. Election Priced as Worst Event Risk in VIX Futures History

https://www.bnnbloomberg.ca/u-s-election-priced-as-worst-event-risk-in-vix-futures-history-1.1488115

“As the U.S. stock market continues to rally to record highs, the attention of many investors is turning toward November’s elections as a source of risk.”

“’In the history of the VIX futures contracts, we’ve never had an event risk command this sort of premium into forward-dated vol at a specific tenor,’ Bloomberg macro strategist Cameron Crise wrote in a blog post. ‘That obviously suggests that markets anticipate some pretty incredible fireworks’.”

There are a couple of interesting points to this story. One is that the potential for disruption in relation to the election is absolutely showing up as a risk factor in financial markets. Indeed, the event risk is commanding a record premium.

As the stock market continues skipping along to record highs it begs the question of how those investors are positioned. Record premiums on event risk suggest several would rather overpay for protection than risk being out of the market. That says something.

Retail stock market investors should note professionals’ caution

https://www.ft.com/content/e50812f0-51c1-4f8c-9072-21eb0eb8cb9d

“After all, despite the vocal concerns over valuations having split away from underlying corporate and economic fundamentals, few fund managers have been willing to challenge the market by placing outright shorts.”

“With that, the Vix volatility index has decoupled from equity indices, adding to signals that a large market correction, should one materialise, would encourage more professional selling that could overwhelm the buy-the-dip retail investor.”

Although Mohamed El-Erian comes across as a grumpy old man complaining about “kids these days” in this piece, he is right in characterizing the landscape and the risks. Foremost among the risks for fund managers is missing out on the speculative run.

That said, the Vix decoupling also indicates increasing short-term risk. These are the types of conditions that can precipitate significant risk events. Incentives exist that prevent participants from doing the single best thing to manage risk. In this case, fund managers don’t want to sell out of stocks.

As a result, they do the next best thing which is to hedge. All kinds of things can go wrong with hedges though. They can be expensive. They can fail to operate the way they were intended. During significant dislocations, counterparties can fail. There are some serious warning signs here and it would not be smart to risk anything that one cannot afford to lose.

Geopolitics

Battling over boundaries

“So if you’re thinking where Turkey can get gas that Russia can’t interfere with, that’s Iraqi Kurdistan or Israel or the eastern Mediterranean.”

“A kaleidoscope of grievances against Turkey has helped to meld a trio of European states (Greece, Cyprus and France), a pair of Arab ones (Egypt and the UAE) and Israel into a loose but formidable geopolitical front.”

The subject of Turkey has come up in the context of currency crises, emerging market travails, energy, and geopolitics. The Economist does a nice job of pulling many of the disparate pieces together.

In a sense, the situation is unfolding like a real-life game of “Risk”. As Turkey managed to “get back into the game through Libya”, it can now leverage divisions within the EU to its advantage.

How Should The European Union Respond To Rising Greece-Turkey Tensions?

“The EU has called for the sovereign rights of its members Cyprus and Greece to be respected. But the different approaches taken by France and Germany could undermine the EU’s mediation effort.”

“A revival of tourism, if the Eastern Mediterranean is no longer perceived as a conflict zone, would contribute to the recoveries of Cyprus, Greece and Turkey from the coronavirus-induced downturn. Conflict-resolution would bring reputational gains to Turkey, where the business climate suffers from weaknesses in the rule of law. This would raise the country’s ratings and improve conditions for European investment and banking in Turkey.”

As Germany and the EU get dragged into the disputes, it presents both risk and opportunity. On one hand, there is a risk of undermining the fragile solidarity the EU demonstrated in approving the pandemic relief package earlier in the summer. The opportunity, of course, is to demonstrate the kind of leadership that will strengthen the union further and accelerate economic recovery.

A recent piece on Zerohedge updates the story with the involvement of the US by way of Cyprus. You have to hand it to Turkey’s President Erdogan: He sure knows how to stir up a hornet’s nest.

Politics

QAnon lures adherents by acting like a game

https://www.ft.com/content/c6502a2f-9f85-4c82-8de9-e42fd4afe7a9

“A type of online information warfare, its objective is to sow discord and distrust. Yet it is masquerading as a live action role playing game, or Larp, and much of the population doesn’t even know it is happening.”

“The culture slowly became a potential recruitment ground for a virtual paramilitary organisation, just waiting for someone to figure out how to deploy it in the real world.”

This article caught my attention partly because the world of Larps is well outside the purview of my normal interests and partly because it involves the downside risk of technology which is in that purview. In short, all of the tools and behavioral insights that make games engaging and addictive, are also “vulnerable to being hijacked or set up by nefarious state actors”. This presents a real risk, Kaminska warns, of players inadvertently becoming actors in a game with ulterior motives.

Inflation

ERIC Head to Head Debate: Napier (Inflationist) Vs Minack (Deflationist) webinar, 8/26/20

One of the more challenging elements of evaluating inflation is determining the balance of inflationary factors versus deflationary factors. Many commentators focus on one side or another and primarily advocate for the position. Napier and Minack clearly discussed puts and takes, where they agree and disagree, how they could be wrong, and what things to watch for. In short, they both came across as the consummate professionals they are.

In short, they mainly agree on the framework from which to evaluate inflation potential. Yes, the impact of Covid shutdowns is deflationary. And yes, money supply is an important factor. The differences are more a matter of timing.

Napier believes the revolution that is happening is not in the quantity of money being created, but rather the mechanism by which it is created. He believes government guaranteed loans, exemplified by the bounceback loans in the UK, provide the “magic money tree” that politicians will inevitably abuse.

Minack focuses more on the deflationary demand destruction from Covid lockdowns. He does not believe money is a good guide to inflation potential and rather focuses on the lagging relationship of inflation to GDP growth. There are no examples, he claims, of high unemployment coincident with rising inflation.

Both make excellent points and in doing so highlight the dilemma facing investors: Which is it, inflation or deflation? A common denominator in both is expectations for public policy. Napier expects government-backed loans to metastasize into de facto monetary policy. Minack states the potential for substantial additional fiscal stimulus as the greatest risk to his thesis.

My base case remains that deflation will be the greater force over at least the next year or two, but inflation remains a significant risk longer term. I don’t see how government-backed loans can be created fast enough to displace existing loans and provide growth on top of that. Once banks and consumers know that loans can be guaranteed, there will be no going back to the old credit-based loans that can suffer losses.

The greatest risk to my base case is also new stimulus measures. Anything that can reliably get cash in the hands of consumers who would spend the money would change the game. This includes ideas such as the Fed “going direct” and new rounds of government stimulus checks.

Even with those possibilities, I am inclined to lean toward deflation/disinflation for a period of time. One reason is that policy measures have been reactive. I don’t think we will see big new policies until and unless things get a lot worse. In addition, none of these policies is a long-term solution. Finally, despite heroic efforts, none of the measures yet has worked in producing inflation. It will take a fundamentally different type of policy or a fundamentally different scale of policy to move the inflation gauge.

‘Divided’ investors caught in inflation confusion

https://www.ft.com/content/672e69b7-d069-4c97-b86c-6e1ba36ece87

“The relatively hefty premiums to hedge against very high or very low inflation make sense given the plausible arguments for both, according to JPMorgan Asset Management strategist Karen Ward. ‘On the one hand, central banks are under tremendous political pressure to keep rates low, and governments have lost their fear of debt,’ she said. ‘But once furlough schemes come to an end you can see a scenario where companies say ‘you can come back on 80 per cent of your pay, or we let you go’.”

“Kacper Brzezniak, a portfolio manager at Allianz Global Investors, said: ‘The activity in options markets suggests growing demand among investors for hedges against very high or very low inflation’.”

This FT article demonstrates that ambivalence toward inflation is more than just a theoretical discussion but is also permeating investment activity. With lots of moving parts, and featuring potential yet unpredictable policy measures, inflation and deflation are both perceived as meaningful risks that need to be managed. The only thing I disagree with is the emphasis on “very high” and “very low” inflation. That seems like an over-reaction to me and an assessment that overlooks the risks of moderately high and moderately low inflation.

Implications for investment strategy

The most important message in Hussman’s letter is his assessment that expected returns are “easily the lowest level in history”. For long-term investors, this means investing in stocks today presents the worst value proposition in history.

In a sense, this makes things easy for long-term investors. Keep allocations to stocks low and just watch the spectacle of blow off speculation. Or ignore it altogether. What matters is there is no need to worry if you are missing something. You aren’t.

This is also a good time to be preparing for whatever the future brings, which is likely to be something different. For example, it is interesting that some large pension funds have been paving the way for allocations to gold. That is one possible project. Outlining how inflation may affect your portfolio and how to protect against it is another, larger project. It is a lot easier to do projects like this, and to do them well, when you have time and prices are not moving against you every day.

Principles for Areté’s Observations

All of the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, Areté’s Takes are designed to show both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.