Areté's Observations 12/18/20

Market observations

The following screenshot from Twitter was posted on Almost Daily Grant’s on Monday the 14th. I like it because I think it captures much of the current market sentiment fairly well: The way you get ahead is to get a loan, lie about its purpose, invest it in bitcoin, and simply wait for the profits to come rolling in. Every aspect of this violates my beliefs and values, but this is what is going on.

Economy

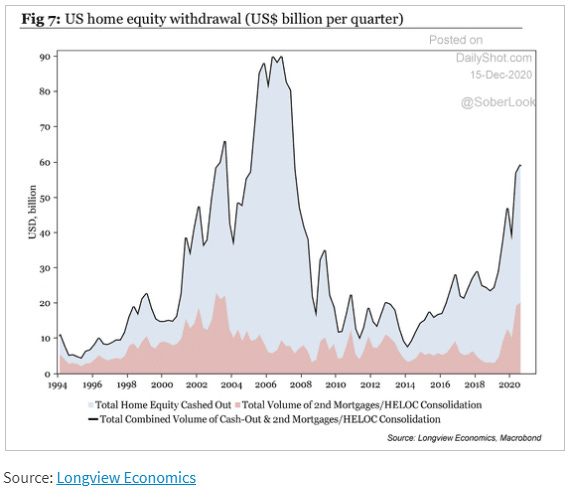

Homeowners realized $1 trillion of equity in Q3

https://www.axios.com/homeowners-trillion-equity-q3-d644ca10-feb2-4daf-a9db-28d87c0ad15f.html

“U.S. homeowners with mortgages saw a collective equity gain of $1 trillion in the third quarter, a 10.8% increase from Q3 2019, according to a new report from CoreLogic. That comes out to an average gain of $17,000 per homeowner, the largest average equity gain since the first quarter of 2014.

Housing continues to be a case of good news/bad news. On one hand, record low mortgage rates and a wave of people leaving densely populated cities are combining to push up house prices. This is undoubtedly a benefit for those who own homes and has provided some nice padding to household balance sheets.

On the other hand, it is also clear that a number of homeowners are drawing on home equity lines like they haven’t done since the housing boom in the mid-2000s. Whether these funds are being used as cheap credit for other purchases or are needed to replace income, the signs are not good. Further, the home appreciation puts the issue of inequality in stark relief: If you own a home, you realize $17,000 in bonus equity; if not, maybe you get a $1,200 stimulus check.

Federal Taxes Are Sending An S.O.S Signal

https://www.zerohedge.com/markets/federal-taxes-are-sending-sos-signal

“Federal withheld income tax receipts represent hard contemporaneous data. Tax receipts are current and complete, unlike other economic data series such as household and payroll employment …”

“Checking the tax data records from the US Treasury the decline in tax receipts over the last 9 months is the largest on record. The only comparable period is the 14% drop in 2009 during the Great Financial Recession.”

The hypothesis is the drop is so large because it includes the taxes for most small business owners. Insofar as this is the case, the huge drop reflects both the enormous impact the pandemic has had on the economy and the disproportionately negative impact on small businesses. If home equity withdrawals and other economic metrics create a somewhat mixed view of the economy, withheld income tax receipts should provide greater clarity.

Credit

America’s two-track economy: the small business credit crunch

https://www.ft.com/content/1ae439b1-75e7-4b55-876c-66533ac37db8

“But the central bank’s largesse has failed to trickle down to a large part of corporate America, with smaller businesses suffering the worst credit crunch since the financial crisis.”

“Smaller and medium-sized businesses that don't have access to capital markets are struggling mightily. They’re really hanging on for dear life, and the longer this persists, the more challenged they are. At this point, they’re being left behind. Inequality is a theme in all aspects of life these days.”

“We’ve created a caste system for credit,” he [Peter Atwater] says. “It’s significant, because its basis is entirely a function of size, not quality.”

The consequences of policy regarding credit availability are becoming abundantly clear: It really is a caste system based on size and not quality. Of course, this goes against any kind of principles of free markets or meritocracy. The objective reality is this will decimate a generation of entrepreneurs and that is unlikely to be good for the economy.

Arete’s Observations 5/8/20

“My guess is that things will be much harder for smaller private companies that do not have good access to capital. I suspect there will be a wave of bankruptcies of small and mid sized businesses.”

I wrote this back in early May and it couldn’t be any truer today, although the bankruptcies are taking longer than I expected. I feel in equal parts happy that I was able to discern major policy consequences so far in advance and disgusted that those consequences have been so harmful and so obvious. While it won’t change anything, I do often fantasize about Fed and Treasury officials being held to account by having their personal net worth used to backstop policy failures.

Public policy

Restoring UK growth is more urgent than cutting public debt

https://www.ft.com/content/50394d54-1b2e-417b-ba6d-2204a4b05f24

“There are indeed things to worry about. The level of debt relative to GDP is just not one of them.”

Ahhh, my love-hate relationship with Martin Wolf at the FT. He is very smart and attuned to many of the important public policy challenges of the times. But he can be such an economist at times, and I don’t mean that in a good way. Specifically, he can almost effortlessly make policy recommendations with total disregard to the fact that the assumptions behind them are not valid. He assumes problems away.

For example, his current policy recommendations (for the UK, but also applicable to the US) include locking in low interest rates, planning “how to close the structural fiscal deficit once the economy returns to normal”, and sustaining “confidence that the UK is run by sensible and competent people”. So, did anyone else LOL at this? Gosh, if it were just a matter of closing the structural fiscal deficit and getting sensible competent people to run the government, why didn’t we think about that a long time ago?

As a result, I completely disagree with his opinion that we should not worry about the level of debt relative to GDP. We should worry about debt for all of the obvious reasons he doesn’t state. Artificially low rates incentivize the consumption of debt for non-productive purposes which makes it increasingly difficult to “return to normal”. Structurally low growth also incentivizes government officials to pander to political interests rather than to act competently for the public good. If people were as virtuous as Wolf assumes, we wouldn’t have these problems to begin with.

Politics

The Dangerous Idolatry of Christian Trumpism

https://frenchpress.thedispatch.com/p/the-dangerous-idolatry-of-christian

“A significant segment of the Christian public has fallen for conspiracy theories, has mixed nationalism with the Christian gospel, has substituted a bizarre mysticism for reason and evidence, and rages in fear and anger against their political opponents—all in the name of preserving Donald Trump’s power.”

Later he says, “We need to fight to the death, to the last drop of blood, because it’s worth it.”

“Here’s the warning: While I hope and pray that protests remain peaceful and that seditious statements are confined to social media, we’d be fools to presume that peace will reign.”

There are at least a couple of things that I find incredibly disturbing about this report. For one, the inflammatory language, the framing of things in terms of good vs. evil, the dehumanizing of people who don’t agree, and the empowerment to do violence are all trademark characteristics of religious zealotry. In essence, this is no different than the radicalization of recruits for ISIS.

Another is this movement certainly seems to have the potential to be a serious security threat. Although “war gaming” exercises over the summer considered the possibilities of Trump refusing to leave office if he lost the election, I did not read about scenarios in which a broader group of loyal supporters might literally fight on his behalf. Although it is hard to say if the numbers amount to a serious threat, the sentiment is being given additional support by a number of Republican legislators and their donors …

Releash the Kraken

https://gfile.thedispatch.com/p/releash-the-kraken

“There’s no way Rubio admires Trump. There’s no way he actually believes this case has merit. There’s no way he believes the election was stolen. He’s just lying because he’s suffering from the political equivalent of battered spouse syndrome, which Trump induces in so many former proud constitutionalists, out of desperation to win favor with his base.”

“I don’t know how many donors the signatories of that Conservative Action Project petition would lose for their respective organizations if they didn’t join in this prairie fire of cowardice. But you can be sure that if their donors didn’t support this, that petition would never have been written in the first place.”

“But the damage being done here is real. Rush Limbaugh is trial-ballooning secession talk. People are talking about fighting and dying in the streets over a glaringly obvious lie peddled by perhaps the sorest loser in the history of sore-losing.”

When a group of people elicits this much disgust from its own “team”, then you know there is something much more meaningful happening than just trash talking from the other side. Goldberg’s comments are fair: There is real and lasting damage being done by the efforts to challenge the election.

Part of the lasting damage figures into the economic forecast. It is hard for me to imagine there is much potential for ongoing collaborative policy making under a Biden administration when there is a substantial cohort of Republican lawmakers that continue to contest the election. Given the economy will need ongoing support from fiscal policy for the foreseeable future, there is plenty of room for disappointment.

Technology

SolarWinds Stock Sinks After Massive Government Hack

https://www.zerohedge.com/political/solarwinds-stock-sinks-after-massive-government-hack

"’The compromise of SolarWinds' Orion Network Management Products poses unacceptable risks to the security of federal networks,’ said US Cybersecurity and Infrastructure Security Agency (CISA) acting director, Brandon Wales. The agency has issued an emergency directive to federal and civilian agencies to review their networks for suspicious activity and to disconnect or power down SolarWinds Orion products immediately, according to TheHackerNews.”

"This campaign may have begun as early as Spring 2020 and is currently ongoing," FireEye said in a Sunday analysis. "Post compromise activity following this supply chain compromise has included lateral movement and data theft. The campaign is the work of a highly skilled actor and the operation was conducted with significant operational security." -TheHackerNews

As can be the case when spirits are high, talk of more abstract and less flattering topics often gets sidelined. As such, while this major cyber breach has rightfully made the news, it is not getting the attention it deserves. This was a professional job aimed at a target rich environment. The head of US cybersecurity issued an emergency directive. In other words, this is a major problem.

I strongly suspect we will be hearing about the consequences of this at least indirectly for a long time to come. At very least, the hackers demonstrated “proof of concept” which can be leveraged for future exploits.

The foreseeable, yet largely unforeseen, risks of a tech crash

https://www.ft.com/content/0bfbf17e-a668-4f58-a940-cae9a9bec5f4

“Our ubiquitous use of technology has already outstripped our ability to manage it safely. Unless we upgrade our security, governance and regulatory regimes, we will remain worryingly vulnerable to the crippling of critical infrastructure, either by malicious design or by default. Call it a tech crash.”

“Given all this, it is little wonder that US defence officials have for years been warning about the dangers of a ‘cyber Pearl Harbor’ that could take down critical infrastructure, even as they contemplate unleashing devastating cyber attacks of their own.”

John Thornhill makes a great point here. Sure, technology can bring great things, but it is not an unalloyed positive. Technology also brings great risks, many of which increasingly are beyond our capacity to manage well.

This is really important to keep in mind. Whether the challenge is recovering from the coronavirus pandemic, finding ways to boost the economy, or perhaps even dealing with geopolitical conflict, it would be nice if we were both aware of the infrastructure risks and were reasonably competent at managing them. This major hack suggests we are not.

State Capacity Liquidationism

https://diff.substack.com/p/the-bullwhip-effect

“even if $600/week supplemental unemployment gets passed before the 7/31 deadline (unlikely), the updated policy can’t be implemented in time to get checks to unemployment recipients. The infrastructure for processing claims, setting payments, and getting them to recipients is just too clunky.”

“If you’re a resolute political moderate, this is all very exciting news: the country literally doesn’t have the technical chops to implement something like Basic Income, an unemployment rate- or infection rate-based safety net, online voting, or digital IDs.”

Two points here. One, if you are inclined to dismiss the cyber threat as relatively unimportant, perhaps you don’t realize exactly how antiquated many of the government’s computer systems are. This reveals a second point. As much as there might be helpful public policy ideas out there, many of them cannot be implemented on existing systems. The lack of “technical chops” in government computing infrastructure may be an even greater impediment to progress than partisan politics.

Inflation

Pandemic triggers ‘perfect storm’ for global shipping supply chains

https://www.ft.com/content/eb21056b-5773-422a-ab78-92e59cddc1b5

“Operators say the container shipping industry — the backbone of global trade — is under severe pressure due to the combined impact of staff illness, quarantining and social distancing, along with soaring consumer demand and disruption to factory output caused by lockdowns.”

A lot of inflation talk is being bandied about based on anecdotal evidence of prices of something or other going up recently. The shipping industry is a great example; a “perfect storm” of troubles has caused shipping rates to jump from lows earlier in the summer.

Much of the discussion is misleading, however. While it is true there are many isolated instances of prices rising, most of them are rising due to short-term supply and demand mismatches, not due to long-term structural mismatches. In the case of shipping, “staff illness”, “quarantining”, “social distancing”, and “output disruption due to lockdowns” are all temporary issues.

The chart below highlights the same phenomenon with consumer goods. The increase in demand for goods like used cars and appliances is temporarily higher than supply systems can keep up with. These are not the result of structural supply shortfalls. Consumers can minimize the impact of glitches like these by either deferring purchases or finding substitutes.

The bigger, long-term takeaway is that these glitches are indications of supply chains and operating systems that have been built for efficiency and not resilience. As a result, I think it is highly likely we will continue to see incidents of overshooting and undershooting of supply and demand for various items. Indeed, one of the more lasting effects of the pandemic may well be an elevated state of operational inefficiency that results in more volatile prices.

Inflation, as I describe in a new special report, is also about the aggregate of lots of price moves. To this point, Albert Edwards highlights the single most important component …

Albert Edwards: The 10-Year Yield is Heading to Zero

“Falling rent prices take a long way to filter through to the CPI, in part because data is sampled only once every six months. But rent is a major component of core CPI, representing nearly 40%, and it has dropped precipitously.”

“The recovery of value was very much tied to an increase in implied inflation expectations, as measured in the U.S. bond market. This is an artificial rise, though. The Fed’s QE, especially during April and May, was skewed toward TIPS to drive inflation expectations upwards, and that effect has persisted, according to Edwards.”

Edwards rightly highlights the huge risk for investors, especially those hopping on the “reflation” train early. Not only are deflationary pressures beginning to circulate by way of declining rents, but those declines threaten a “gap down” in economic growth. When that happens, any company with debt will face potentially existential challenges.

Capital markets

The US Treasury market is facing a train wreck

https://www.ft.com/content/ffb2a3b4-1044-4a61-921a-e288ffb82170

“There is going to be a train wreck at the front end of the [Treasury] curve next year. There is way too much cash chasing too little paper.”

“Or, you might agree with the other dealers and the regulators that it might be the time to set up a dedicated CCP, or clearing house, just for Treasuries. As one official who has been on the calls discussing the logistics of such a CCP said: ‘Eventually, it might have to be bailed out. The political cost of that bailout would, however, be lower than bailing out any banks’.”

Cause, effect. Rinse, repeat. So, it seems the go-to answer for just about any public policy ill is to increase the debt. But then irregular lumps of the stuff create problems for the financial plumbing. The answer? More debt, of course! Other than the possibility of negative rates for short-term Treasuries, I have no idea how this “train wreck” will turn out, but I’m pretty sure I know what the remedy will be.

Implications for investment strategy

Historically, the sign of a bubble top in the market has been when “retail” investors get involved. That was certainly the case in the late 1990s and the first quarter of 2000 when the confluence of internet access, discounted commissions, and soaring tech stocks created newly fashioned day traders.

I argued against the potential for a melt-up starting about five years ago because retail investors did not seem to have the resources to participate in any meaningful way. Still hobbled by the housing crisis and with real median household income not yet crawling back to the 2007 level, a good chunk of individual investors simply did not have the wherewithal to speculate in the market, even if they were so inclined.

Thanks to financial “innovation” and other conditions, the situation is different today. Fueled by greater savings (including stimulus checks) and facilitated by fractional shares and commission free trading, today’s wannabe Wall Street moneymakers are finally being unleashed again to do their thing. Increasingly, that “thing” is buying call options.

This phenomenon has implications for other investors. For one, it is these speculative, risk averse investors that are increasingly propelling stock prices higher. This matters because the reaction function of such investors is very different from that of large institutional owners. For example, when a large endowment experiences losses in its stock portfolio, it will typically add to stocks to rebalance its portfolio.

In sharp contrast, when individual investors experience losses, the reaction is often one that exacerbates the losses. Call options are extremely speculative and can collapse in value in a hurry. If that wipes out someone’s capital, they’re done. Further, large losses surprise some people and can compel them to sell stocks at the worst time. Finally, existing debt, in any form, can also compel the sale of stocks at the worst time. This is the thing that could prove quite interesting for long-term investors: When stock momentum plateaus and prices start to fall, will forced selling cause some unusually large losses in stocks? Signs point to yes.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

Please direct comments or feedback to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.