Obserations by David Robertson, 3/17/23

Last week I wrote, “There has been an eerie calm in stocks despite some pretty ominous rumblings”. Then SIVB and SBNY banks were shut down, the Treasury issued an emergency plan to protect uninsured depositors, Credit Suisse was bailed out, and volatility spiked.

If you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

By far the biggest fallout from the SIVB spectacle was in interest rates, not stocks. As Tier1Alpha put it: “The real drama occurred in the rates market where the US 2yr bond moved by the most since the crash of 1987. So the calls for the end of the world played out, but not in the equity asset class.”

Volatility spiked in both stocks and rates, but it was rates vol that made the bigger impression. The MOVE index spiked even higher than it did during the initial Covid scare as depicted in the graph from themarketear.com ($). While VIX jumped, its move was relatively modest. While I do not think this is a replay of the systemic crisis that was the GFC, I do think it is useful to remember that problems in fixed income markets signaled danger long before stock prices did.

USD fell last weekend and fell again on Monday in response to the bank troubles. Apparently it took a day or two to ferry the news over to Europe because it wasn’t until Wednesday that Credit Suisse got implicated and broader systemic concerns drove investors to the safety of USD again on Wednesday. Interesting times.

Banks

After an extremely eventful weekend and week, one of the most important points to keep in mind regarding banks is that none of the current issues are black swans or even gray swans. They are perfectly ordinary happenings that have been documented by watchers of the industry all along. For example, the FT’s headline, “Problems at tech sector lender built for years before collapse”. Grant’s Interest Rate Observer called SIVB the “bank of the cycle” … in its Nov. 15, 2019 edition - over three years ago.

“The prisoner’s dilemma was basically: I’m fine if they don’t draw their money, and they’re fine if I don’t draw mine,” said one of the CFOs, whose company had banked around $200mn with SVB.

SVB unravelled spectacularly, but its fate had been sealed almost two years earlier.

If any aspect of the episode should be characterized as extraordinary, it should be the nearly complete lack of attention of emerging risks from investors and bank customers. Sign of the times I guess.

No, the fall of SIVB was the result of perfectly ordinary neglect, incompetence, malfeasance, and greed on the part of virtually all parties involved. As Martin Wolf put it in the FT: “The marriage of risky and often illiquid assets with liabilities that have to be safe and liquid within undercapitalised, profit-seeking and bonus-paying institutions regulated by politically subservient and often incompetent public sectors is a calamity waiting to happen.” The unfortunate reality is, higher rates have put the entire banking sector on simmer and over time - the worst ones boil over.

As an example, I mentioned Credit Suisse in the 10/7/22 edition of Observations. That bank sunk to new lows this week at about half the level it was then - before diving again on Wednesday. As I said at the time, “Bottom line: Yes, CS is a disaster but it’s not the kind of disaster that is likely to be the next Lehman Brothers.” I still think that’s the case, but the task of drawing the line between who will be saved and who won’t will continue to be a big policy challenge.

All that said, there are a number of takeaways from this latest imbroglio. First, there are a lot of bad takes on the situation. I group these into two main buckets: One is people who don’t know what they are talking about but nonetheless opine loudly on the issue. Another is people who are blatantly self-interested and/or hypocritical. Unfortunately, since social media and mobile devices have become much more ubiquitous since the Lehman affair in 2008, the volume of misinformation has exploded making it harder to sort through the crap.

Another observation includes the revelation of many tech executives and VC-types as being financially illiterate. This is scary in many respects but for the last fifteen years finance has just not been a valuable skill set. Now it is. Lastly, for the first time in fifteen years, I saw some people, and knowledgeable and experienced people, starting to panic. While most of that eased by the end of the week, it is interesting to observe how easily finance types can become completely unhinged when adversity strikes them.

Economy

With both the SIVB drama and a still fairly high CPI print this week, the notion of a 2-speed economy is continuing to crystallize. Real economic activity is relatively strong whereas the economy of financial assets continues to show more cracks.

As @Stimpyz1 highlights, this 2-speed economy undermines singular arguments either FOR inflation or FOR deflation. They both exist but in different areas. The policy “trick” is to confine deflation to financial assets. This is a targeted approach akin to chemotherapy.

As described in another tweet, this assessment implies the quest to look for recession is a misguided one. That’s not the important thing. The important thing is restructuring. Judging by that metric, we are off to a pretty decent start with plenty more to come.

Geopolitics

China’s true leverage is hidden behind a complex web of overleveraged borrowers ranging from State-Owned Enterprises (SOEs), private Real Estate Developers, and Local Government Financing Vehicles (LGFVs). As Borst puts it, “As strong as the central government’s balance sheet is, it is not strong enough to bail out every contingent liability in China.” The extent of these financing arrangements make Enron’s off-balance sheet shenanigans seem like child’s play.

Here's the thing about the USD Wrecking Ball: The Fed doesn't need to Out-Hawk everyone else. By the time, things catch on fire here, it will likely be SCORCHED EARTH everywhere else, so perhaps the new question should be: Who's gonna start Out-Doving the Fed?

Michael Kao makes a couple of really good points in this piece (mainly) about China and debt in that country that don’t get enough attention. First, the magnitude of China’s debt and the scale of its complexity are truly massive. Critics of debt levels in the US often seem to miss the fact that China’s problems are far, far bigger.

Another good point Kao makes is in regard to monetary policy and, by association, relative currency strength. Once again, critics of US finances who believe the US dollar will weaken often argue the US does not have the luxury of keeping monetary policy tight for very long.

This is only true in absolute sense; it is not true in a relative sense. As Kao rightly points out, “The Fed doesn’t need to Out-Hawk everyone else”. All the Fed needs to do to retain a strong dollar is to not loosen monetary policy more than other major central banks. When the pressures of higher rates really start to dig in, they will dig in even more outside the US and put relatively more pressure on other central banks to ease. Regardless of what the Fed ends up doing, it won’t be hard for it to remain relatively tight.

China

Dancing In The Dark, Wednesday, March 15, 2023

https://www.grantspub.com/resources/commentary.cfm

Investors hoping to transact in China’s $21 trillion onshore debt market received an unpleasant surprise this morning, as electronic portals used to provide pricing information turned blank. The comprehensive shutdown followed a Tuesday missive from the China Banking Insurance and Regulatory Commission instructing brokers to switch off their price feeds in response to “data security concerns,” Reuters reported.

Though the emerging markets mainstay [HSBC] subsequently told Hong Kong-based newspaper Ming Pao that the “problem has been resolved,” foreign investors hoping to repatriate their cash can expect plenty of hassles, especially considering that the greenback has appreciated by nearly 10% against the renminbi over the past year. An analysis yesterday from J Capital Research co-founder Anne Stevenson-Yang notes that “China has always made it much harder to extract capital than to invest it. When demand for dollars rises, though, the banks raise as many obstacles as possible.”

In the context of twin deficits in the US, incongruent policymaking, and periodic diplomatic snafus, it is not hard to understand how analysts can harbor doubts about US hegemony and the strength of the US dollar. It is also not hard to understand why countries like China may see an opportunity to boost the position of the yuan in the global economy.

Take two seconds to look at the other side of the equation, however, and those wistful notions immediately evaporate. What happens when global fixed income markets are roiled and the US dollar rises? China shut down price feeds for its entire onshore debt market. What happens when demand for dollars rise? “The banks raise as many obstacles [to extract capital] as possible”. And now, almost as if on cue …

Either one of these phenomena would give very serious reason for a global risk manager to avoid exposure to yuan. Both of them together seal the deal. The US dollar is far more functional as a global reserve currency than the yuan. While China has its reasons for pursuing such policies, when the weaknesses are so clearly displayed it reveals the country’s aspirations for a more prominent currency are just that - aspirations.

Politics I

Chartbook #201 Venture dominance? The meaning of the SBV interventions.

https://adamtooze.substack.com/p/chartbook-201-venture-dominance-the

I [Adam Tooze] am as much a sucker for a financial crisis-fighting story as anyone. But even I could not repress a horrible sense of deja vu and disgust at events over the weekend. Are the same people going to go on doing this over and over again: Tragedy, farce and then what? Zombie horror show? Of course the authorities should have seen it coming. If there are no resignations at the Fed, it will be a sign of the morbid state of the US governmental elite.

But as should have been obvious all along SVB matters very much indeed, because its depositors are very powerful, very rich and very influential people who own a narrative that makes them indispensable to one vision of America’s future. And that force was brought to bear on the Biden administration over the weekend in an extraordinarily overt exercise of “venture dominance”

I personally have very mixed feelings about the Fed’s program to protect uninsured deposits at SIVB and SBNY. Adam Tooze captures some of those feelings when he expresses a “horrible sense of deja vu and disgust”. I love Matt Klein’s line that “this was more a case of a ‘bank-run by idiots’ rather than a ‘bank run by idiots’.”

All this said, banks do play an important role in the financial infrastructure. As imperfect as they may be, having them not function at all would be far worse. As a result, judging public policy against perfection is too high a standard. Sometimes we just need to take our lumps and move forward.

In addition, by way of touching many lives, banks are inherently political organizations. Any threat to the system must be taken very seriously because it would affect so many … voters. Further, when many of those lives are rich and well-connected, it is fair to expect lobbying efforts to protect those interests. This is not a value judgment, just an objective assessment of the way things are.

It will be very interesting to watch how this unfolds. On one hand, the SIVB affair certainly crystallized the consequences of the Fed’s rate hikes and the need for policy containment. On the other hand, it has also reignited the visceral disgust at widespread negligence and moral hazard. This suggests there is a much narrower path for monetary policy and regulatory measures than there used to be.

Politics II

In a time of especially partisan politics it is easy to characterize policies in simplistic terms - either progressive or conservative. What @Halsrethink highlights is that a lot of policy stereotyping should be thrown out the window when more urgent issues, like an upcoming election, present themselves.

The notion of rapidly changing political priorities was illustrated vividly in Daniel Yergin’s book, The Prize, about the oil industry. In the late 1930s and early 1940s, political sentiment was strongly against big oil companies and the Justice Department launched antitrust cases against many of them. Then, in early 1941, when US involvement in World War II became imminent, the FDR administration quickly flipped its position and embraced the oil companies in order to support the war effort:

And what Dr. New Deal had found unpalatable and unhealthy about Big Oil—its size and scale, its integrated operations, its self-reliance, its ability to mobilize capital and technology—was exactly what Dr. Win-the-War would prescribe as the urgent medicine for wartime mobilization.

The big lesson is political priorities can change quickly - and dramatically. While it is true public sentiment has been hostile to fossil fuels for many years now, it would be wrong to assume public policy would not change if a higher priority cause (e.g., election, war) presented itself.

Implications

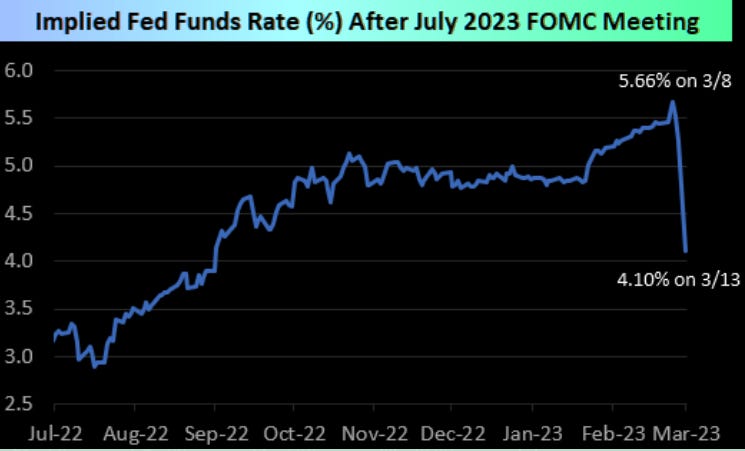

One of the most important consequences of the SIVB affair will be the effect it has on the Fed’s reaction function. While bank trouble must be considered as a potential threat to financial stability, the still-high CPI number from Tuesday (6% year-over-year) clearly indicates there is more work to do on inflation. How will the Fed weigh the tradeoffs?

It is clear from interest rate futures what the market thinks. The market’s expectations for the Fed’s rate trajectory (https://themarketear.com/premium) completely flip-flopped from no easing through 2023 to significant easing by the middle of the summer.

While significant easing by the summer is certainly a possibility, that seems to be more a function of wishful thinking on the part of market participants than an objective assessment of the Fed’s increasingly difficult tradeoffs.

Insofar as inflation is still a significant threat (and it is) and China and Russia are still meaningful geopolitical rivals (and they are), the probabilities seem to fall substantially in favor of the Fed maintaining fairly tight monetary policy. As a result, the situation demands a more surgical response. On this front, the UK’s handling of its gilt crisis in the fall is probably a useful precedent. A policy response involving wholesale monetary loosening would concede both the inflation and geopolitical objectives.

A series of phases of relatively easier conditions (that serve the purpose of absorbing periodic instances of turbulence) amounts to a policy of “controlled demolition”. This latest instance involved banks (and crypto!), but we are likely to be hearing more about real estate funds, private equity, securitized finance and other areas of the financial economy that are being targeted. This “back and forth” pattern reduces the chances of indiscriminate selling and is therefore conducive to financial stability.

This path is analogous to a flight with a great deal of turbulence. It’s not that any of the periods of bumpiness seriously threaten the plane or the passengers. It doesn’t mean the flight is a particularly pleasant one though. You just need to fasten your seatbelt and ride it out.

The implication for investors is there is not just a single pocket of financial turbulence to get through. Rather, it is more useful to think of it as a large weather pattern that can produce storms over a wide area. It’s best to treat the situation accordingly by not doing anything reckless and establishing appropriate expectations. Investors who do still probably won’t have a lot of fun, but will make it through intact.

Finally, one thing these episodes do is to highlight market risks. When those risks become apparent, those who are most exposed need to adjust - by raising cash and de-risking. This affects other investors too - by forcing the prices of risk assets down and putting a higher premium on cash and liquidity. I don’t have the same concerns as @JeffSnider_AIP about systemic risk, but I very much agree that people will be responding to the change in landscape.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.