Observations by David Robertson, 10/11/24

More news, more scuttlebutt, and more narratives to work through. Let’s dig right in.

Also, I will be taking a much-needed break next week. Observations will return on the 25th.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Traders who think Nvidia is volatile are amateurs. As themarketear.com ($) shows, the continuously traded China futures have “basically given back half of the melt up in 2 sessions.” Maybe those big policy announcements in China weren’t that big of a deal after all.

In US markets, the VIX volatility index has been creeping higher which is normally a warning sign for stocks. As Jim Bianco highlights, however, at least part of the reason is the increasing proximity to the election:

Remember, the VIX is the implied volatility of at-the-money S&P 500 options that expire in 30 days. Today, Monday, we are finally within 30 days of the election. So, going forward, the VIX is pricing in post-election volatility.

In addition, as CrossBorder Capital illustrates, volatility is also back in the fixed income complex. “Jump in MOVE not great sign” is the warning — and that is because higher volatility reduces the borrowing capacity of collateral. The jump may also be at least partly related to the proximity to the election, but it could also be an indication that “there is too much funding at shorter end of term structure”.

Finally, CPI came out a little warmer than expected on Thursday. I would argue this isn’t a big surprise based on the data, but it certainly runs counter to the narrative that inflation is dead.

Japan

This post by Tracy Shuchart succinctly summarizes the carry trade and its consequences:

Japan’s $4 Trillion ‘Carry Trade’ Begins to Slowly Unwind

Japan’s investors are starting to lose their decades-long infatuation with overseas assets.

In the first eight months of the year, Japanese investors snapped up a net ¥28 trillion ($192 billion) of the nation’s government bonds, the largest amount for the time frame in at least 14 years. They also cut purchases of foreign bonds by almost half to just ¥7.7 trillion and their buying of overseas equities was less than ¥1 trillion.

“It’s going to be one of the mega trends and it is a super cycle for the next five to 10 years,” said Arif Husain, head of fixed-income at T. Rowe Price, who has nearly three decades of investing experience. “There will be a sustained, gradual but massive flow of capital back into Japan from abroad.”

With $4.4 trillion invested abroad, an amount larger than India’s economy, the speed and size of any pullback has the power to disrupt global markets. Even as the gap in rates between Japan and other countries has narrowed, the inflows have been a trickle rather than the flood some investors have feared.

As I have mentioned several times in the past, the Japanese yen carry trade is a big deal and is likely to affect capital markets around the world for the next several years. This reality stands in stark contrast to efforts by mainstream media and Wall Street commentators to characterize the phenomenon as a flash in the pan that is already behind us.

Because so much is at stake, global attention is turning to Japanese politics for clues as to what the path might look like. Unfortunately, Japanese politics is clear as mud right now …

Japan’s new prime minister vows to tackle deflation ($)

https://www.ft.com/content/1b92d616-4268-49dd-9bc0-ec3d01c89eb3

“Things have become really bad really quickly for Ishiba,” said Tobias Harris, founder of political risk advisory firm Japan Foresight. “He’s had literally no honeymoon. But we knew that the LDP was divided. If you start off in a position where you are heading off a party rebellion, you do not really have much room for manoeuvring.”

Nicholas Smith, chief Japan strategist at CLSA, said the result would probably be to calm investors’ fears of drastic policy changes. Analysts pointed out that Ishiba needed to build consensus within a party still reeling from a corruption scandal and win over a sceptical electorate.

As the FT lays out, the political environment in Japan is especially fraught right now. Policy wonks are trying to figure out how to delicately transition away from persistent disinflation without enflaming inflation. They are also trying to do this with a huge mass of debt and while the public is still distrustful of politicians in general. Difficulty ranking: High.

Further, as the Economist ($) lays out, Ishiba is hardly the prototype of a leader destined to unify fragmented political sects. He is described as, “heterodoxical on the issues,” and while his outspokenness has “endeared him to voters,” it has also “made him an outsider within the LDP (Japan’s main political party)”. The magazine concludes that he may “may struggle to govern” in which case it would “leave Japan less capable of meeting the myriad challenges it faces at home and abroad.”

For the short-term this means public pronouncements will have very limited value because the government has too little power to effect substantive policies. That may change later in October if snap elections facilitate a consolidation of power, but it may not.

It’s useful to note that the lack of political cohesion is not just a problem for Japan, but for a good part of the developed world as well. Without sufficient consensus, there is not enough authority to enact meaningful reform. As a result, voters should not expect such until adversity focuses minds and erodes political bickering.

Geopolitics

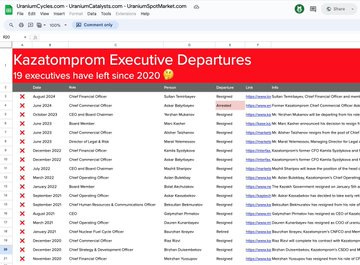

H/t to Katusa Research for highlighting this post by Casper-Nuclear Advocate:

Something is brewing in Kazakhstan, and it doesnt look good if you are a western utility.

I wouldnt be surprised if $kap is suddenly being nationalized again.

Looks like $kap is being used by Russia/China in their cold war against the west.

These are exactly the types of “weak signals” analysts get excited about. They are the little slivers of daylight emerging from behind mostly closed doors that can provide enormous insight into what is going on. Also, by virtue of being “weak”, they are often overlooked by mainstream media.

Of course, evidence like this is not sufficient for a unanimous “guilty” verdict, but it absolutely highlights where there may be trouble in the not-so-distant future. As the need for electric power generation grows in both the East and West, and as nuclear becomes an increasingly important means by which to supply incremental baseload, the supply of uranium could become an important flashpoint. Keep an eye on this space.

Finally, this is exactly the kind of potential supply constraint that seems like a one-off at first. However, when more and more of them start happening, the cumulative effect is for inflation to heat up.

Public policy

‘No more bailouts’: the missing US campaign slogan ($)

https://www.ft.com/content/9d5587a4-ffa6-4958-b984-a9d49c647013

Economic populism is a body of ideas, often random and irrational, crafted to win over frustrated voters. It tends to be good politics, bad economics, and it’s having a moment in the spotlight. As US presidential candidate Kamala Harris vows to subsidise home buyers and punish price gougers, her rival Donald Trump offers universal tariffs and “no taxes on tips”. Such slogans poll well but are likely to backfire if implemented, raising this question: are there populist ideas that can lift the economy and still win votes?

Here’s one missing in the campaign so far, that fits nicely on a bumper sticker: No More Bailouts! Doling out dollars by the hundreds of billions in 2008, and trillions in 2020, state rescues have helped incumbent companies, undermining competition and productivity. Bailouts are the new trickledown economics, claiming that everyone gains from benefits for the rich and powerful, but in the end only fuelling a sense that the system is failing and unfair.

I found this piece by Ruchir Sharma to be intuitively appealing. For one, he is absolutely right that bailouts as public policy are extremely unpopular and extremely wasteful. This is especially interesting in the context of a huge portion of Republican political ads (of which we see more than our fair share living in Pennsylvania) that focus on wasteful government spending. The targets of waste in these ads are so small by comparison though. Frustrating, yes; meaningful, not so much. Why not go for the big honking waste — like bailouts?

This highlights a broader observation: There seems to be something of a political game being played in which politicians and elites allow, and even encourage, relatively modest “wrongs” such as modestly wasteful spending. This allows voters to get angry and feel righteous about resisting such problems while at the same time completely deflecting attention away from bigger issues that actually could threaten the status quo and lead to regime change.

Bailouts are one of those “bigger issues” that deserves attention but just doesn’t get any. Another one is tax policy. Brad Setser, for example, recognized, “In 2023, the eight largest US pharmaceutical companies collectively did not pay ANY US corporate income tax.” Talk about a system that is failing and unfair!

He goes on to suggest, “Time for a real ‘America first’ corporate income tax reform, one where big American companies actually pay a bit of income tax in the US”. In addition, Russell Clark ($) observes: “That is US tax policy, makes sense for US politicians and US corporates, but not for any one else.”

So, why aren’t people getting all fired up for corporate income tax reform, or the end of corporate bailouts? I think the answer is because those are reforms that would really hurt entrenched powers. Those types of complaints are not allowed. Until we do start seeing serious discussion of such issues, it is fair to assume capital is retaining a strong position relative to labor.

Gold

This graph from themarketear.com ($) shows how gold has been rising with China’s increase in gold reserves. While it is not proof that China is the marginal buyer, it is a healthy reminder that the key drivers of gold right now are in the East, not the West. Using 10-year Treasury yields or gold ETF flows as a gauge for the movement in gold is so passé.

Investment advisory landscape

Highway to the danger zone, Almost Daily Grant’s, 10/4/24

https://www.grantspub.com/resources/commentary.cfm

“ETFs now offer nearly universal access to asset classes and strategies that were once available only to the world’s most sophisticated institutional investors,” Amrita Nandakumar, president of Vident Asset Management, commented on Bloomberg Television, adding that last week’s milestone is a “testament to how much ETFs have democratized investing.”

Thus, CoinDesk relayed last Friday that the Defiance Daily Target 1.75x Long MicroStrategy ETF (ticker: MSTX), which aims to generate 175% of the daily performance of Michael Saylor’s enterprise-software provider-cum-leveraged bitcoin speculation vehicle, attracted a cool $857 million since its Aug. 15 debut, putting the fund in the top 8% of ETF launches so far this year per Bloomberg Intelligence analyst Eric Balchunas.

In turn, newly minted peer T-REX 2X Long MSTR Daily Target ETF (ticker: MSTU), which ups the ante via 200% daily MicroStrategy exposure, gathered more than $72 million in assets a mere seven trading days after its debut.

Have ETFs democratized investing? Yes, in many ways they have.

Is Wall Street taking the good idea of ETFs and pushing it way too far. Yes, that is also true. Nobody needs a leveraged bet on an already speculative investment proposition, let also two that are nearly identical. It’s not illegal though, just wildly unhelpful.

Investment landscape I

The Omitted Variable ($)

https://www.yesigiveafig.com/p/the-omitted-variable

Regular readers know that I emphasize that markets do not represent “truth” — they represent the buying and selling activity of market participants. We are presently in the phase where an unstoppable force, Vanguard investor belief in “buy the dip,” is colliding with a radical change in global trade policy that is likely to irreparably damage the profitability of Chinese assets.

This [the exuberant rebound in China stocks] is not a sign of a recovery. It’s a sign that we are increasingly losing control. The rest is simply a matter of time.

While most of this post focuses on inflation, these comments towards the end provide some valuable perspective. First, the idea that markets represent “truth” is a prominent one, especially in the hedge fund community. This makes sense to some degree given the fickleness of their investors. If you underperform for very long at all, clients pull their money. As a result, at least in hedge fund business model terms, market prices are “truth”.

The same is not true for longer-term investors. Those with an investment horizon of many years, and perhaps even many decades, don’t particular care what market prices are today. They care about having a high probability of achieving attractive returns over the long-term.

This is where Green’s alternative explanation is especially helpful. Market prices aren’t so much “truth” as the representation of “buying and selling activity of market participants”. Insofar as that is the case, patterns in buying and/or selling can cause severe distortions between market prices and warranted value. Indeed, this is exactly the type of situation value-oriented investors look for.

More specifically, the combination of regular, persistent flows of money into broad market indexes for retirement savings, combined with share repurchase programs, create regular, persistent demand for stocks that pushes prices beyond what underlying fundamentals would suggest. This condition isn’t “truth”; it’s dynamics.

The situation has reached an extreme with US stocks — and an almost absurd extreme recently with Chinese stocks. The huge rally in the last couple weeks may seem like a validation of meaningfully changing conditions in China. Green warns us, they are not. Rather, “It’s a sign that we are increasingly losing control.” We are losing control because purely speculative behavior is affecting things like collateral values that in turn affect the real economy. Obviously, when things turn the other direction, this gets very bad in a hurry.

Investment landscape II

With so many issues swirling around the investment landscape, it’s nice to be able to get grounded once in a while. Bob Elliott does exactly that by highlighting one of the most important investment phenomena right now — debt:

The greater the government debt load, the greater the incentive to implicitly and explicitly inflate it away in the future.

The largest foreign holders of US bonds know this. No wonder they are buying gold.

Some people may prefer to call this monetary debasement but it has the same effect as inflation so I use the two terms interchangably. Regardless, the main point is, the higher debt rises relative to economic productivity, the less credible its currency becomes.

This isn’t such a big problem for the US dollar relative to other fiat currencies, but it is a problem relative to the more absolute standard of gold. This is likely to remain a key investment theme for many, many years to come.

Implications

The big selloff in Chinese stocks on Tuesday took down most commodities with it. The implication is if Chinese stocks don’t keep going up, then the reflation trade is over.

This presents an interesting question to ponder, and one which Russell Clark ($) does ponder:

So here is the trillion dollar question. Was the Federal Reserve rate increases only deflationary for Chinese assets? Was the pressure that it put on the Chinese Yuan leading to weakness in the Chinese property market? The original idea of needing asset price weakness to keep inflation in check was correct - but only in terms of Chinese asset prices? Given the size of the Chinese economy and property market, this could well be true.

If that was so, then rising Chinese equities would indicate rising inflation, and a possible tightening of interest rates in the US, meaning inflation in China leads to tighter monetary policy elsewhere.

While Clark’s hypothesis may be true, I think it is premature. Given the benefit of a couple of extra days of market action, by the middle of the week the selloff in Chinese stocks (following the massive spike) is looking more like a speculative flash in the pan than any type of inflationary event.

Nonetheless, Clark’s questions are thought-provoking. What if China continues suffering deflation but the US remains stuck with above target inflation? What if China drags the US and the rest of the world down into a deflationary recession? What would policy response likely be? Would they help or make things worse?

The answers, of course, are unknowable, but what is knowable is that the range of possible outcomes keeps getting wider. Further, it seems as if the commanding narrative is oscillating between two extremely opposite states. At very least, this radical uncertainty is unsupportive of the high degree of conviction investors have in risk assets. Perhaps this is part of what the rise in volatility indexes is indicating?

As the oscillation between two extremely opposite states increases in frequency, it begins to look like two separate states existing at the same time. Now, imagine those two states are deflationary recession in China and inflation/overpriced Treasury bonds in the US. In that case, short rates would most likely come down to stimulate global economic growth, but at the same time, higher long-rates would tighten financial conditions.

Maybe this is what Mike Green means by the chaotic rebound in Chinese stocks not being a sign of a recovery but rather “a sign that we are increasingly losing control”? Heightened speculation doesn’t solve problems, it only disguises them for a while. What happens afterward depends a lot on policy responses, but it would take an amazing stroke of both good luck and competence to be good for risk assets.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.