Observations by David Robertson, 10/14/22

The word “interesting” continues to be the operative one in describing current market events. The UK stole the limelight this week but there were plenty of other things going on as well. If you have questions or just want to get some perspective on the whirlwind of happenings, let me know at drobertson@areteam.com.

Market observations

The UK gilt market got most of the attention this week but it sent signals far and wide. Brent Donnelly shows the crazy action in S&P 500 futures on Thursday. The S&P finished up 2.6% after dropping 2% after the CPI number hit at 8:30.

Detailed October QT

https://johncomiskey.substack.com/p/detailed-october-qt

B/S will rolloff by ~78.2b in October. MBS payments should be ~21.4b in October. Subtracting 3.2b for the last bit of previously purchased MBS to settle and we get 60 (UST) + (21.4 – 3.2) (MBS) = ~78.2b of total B/S rolloff in October.

This is some geeky but good stuff from John Comiskey on Substack. The main highlights are the big liquidity withdrawal days through the Fed’s QT program - $16.5B on the 17th and a whopping $31.6B on the 31st. These are the moves that are quietly driving markets. The first is likely to make for a “Gloomy Monday” while the second is likely to make for a spooky Halloween.

Labor

Where Are the Workers?

https://www.mauldineconomics.com/frontlinethoughts/where-are-the-workers

But look on the right: the lines first crossed not when COVID arrived, but more than two years earlier in January 2018. Check the media archives and you’ll see a lot of stories about a labor shortage in 2018‒2019.

The labor shortage didn’t start in the pandemic era. It was already there well before.

This labor shortage isn’t temporary. It’s structural, it’s demographic, and it isn’t going away.

This report by John Mauldin provides some helpful context from which to evaluate labor trends. In brief, the shortage of labor is a phenomenon that has been manifesting over several years and not one that just recently emerged from Covid policies. The labor shortage is “structural, it’s demographic, and it isn’t going away.”

One question this begs is, what other trends have been accelerated by the pandemic rather than initiated by it? The day of reckoning is certainly getting closer for dealing with excessive debt. The utilization of commercial office space looks to be permanently impaired. Policies that favor labor over capital keep gaining ground. Viewing these trends through a wider lens than just the pandemic time frame gives them a very different complexion.

Another question the structural labor shortage begs is, how inflationary will this become? The main lever by which to increase labor supply is compensation so if jobs are going to get filled, they are going to need to pay more. If that happens though, it is likely to set off the Fed’s dreaded wage-price spiral. My bet is companies are going to have to start coughing up more to attract and retain the people they need.

Economy

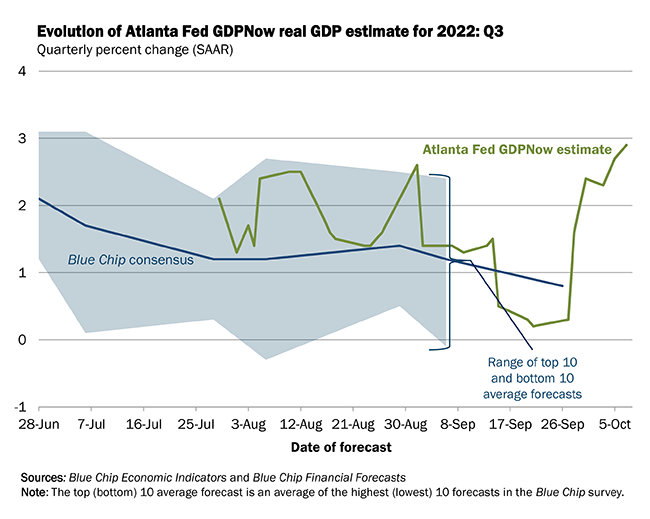

The GDPNow estimate (as of 10/7) is 2.9%. One big takeaway from this is 2.9% is respectable growth after two consecutive weak performances early in the quarter. This reasonably healthy level is also consistent with the strong labor market which was highlighted by a sequential decline in the unemployment rate last week.

This is not to say there aren’t signs of weakness, however. Thus far anyway, those pockets of weakness are not enough to alter the overall economic trajectory.

Another interesting takeaway is the magnitude of change in economic growth estimates over just the last few weeks since mid-September. This serves as a good reminder that post-Covid statistics still have a lot of noise in them and as a result, investors should not take any individual number too seriously.

Social landscape

This is a really good thread on what I can only label the “social landscape”. The enthusiastic and tribal behavior evident in some trading groups really is a sociological phenomenon to behold. Similar patterns exist in the crypto world. All are characterized by a pervasive sense of nihilism.

Similar patterns also exist in political affiliations and across many other social dimensions. The best, albeit hugely incomplete, explanation I can come up with is a lot of people have become “broken”. Something has snapped in their operating system and they just don’t work right any more. They don’t have hope, except for some crazy, quasi-religious beliefs.

I don’t see how this gets better until there is more economic equality, but mainly more equality of opportunity.

Finance

Prior to the pandemic, stock repurchases were a big topic because they were being implemented in ever-greater quantities. As such, there were valid questions as to the degree to which buybacks were being used to boost stock performance.

While there are good and bad reasons to do stock repurchases, in my judgment they are most commonly used as a form of financial engineering. Also in my judgment, the above example of META’s repurchase program (h/t @UrbanKaoboy) is broadly representative.

The bottom line is most programs do not end up being good uses of capital unless they are implemented in raging bull markets. The reason is partly because company management is no better at picking stocks than anyone else and partly because there are often ulterior motives - such as offsetting shares issued for executive compensation.

Regardless, the result too often is poor allocation of capital. As such, it is not functionally different than making a really bad acquisition or investing in incremental supply when the market is already adequately supplied.

Finally, when companies make a practice of poorly allocating capital, it helps explain how cash flow multiples can look so attractive. Sure, the company earns healthy amounts of capital, but it also wastes a fair amount of that cash, so it never makes it into the hands of shareholders.

Inflation

Inflation-linked gilts come unlinked ($)

https://www.ft.com/content/8ee9bee2-eae9-4840-b44c-90967eb72ce0

Economic fundamentals cannot explain this move [in UK bond yields]. In a liquid and efficient market, index-linked bonds would be a proxy for the real rate of interest. The real rate of interest in the UK did not double yesterday. Also, in a liquid and efficient market, nominal bond yields minus inflation-linked bond yields is proxy for inflation expectations. Ten-year inflation expectations did not fall by 40bp yesterday.

Last week I highlighted the risk of relying too heavily on TIPS yields as good indicator of real yields. This week, UK index-linked bonds proved the case in dramatic fashion. As Robert Armstrong reports, “UK 10-year inflation-linked gilt yields rose 64 basis points yesterday [Monday], hitting 1.24 per cent. This is an absolutely bonkers move.”

The main point here is market prices, and therefore the information content they reveal, are only as robust as their underlying liquidity. Heavily traded markets with heterogenous participants generally provide good price discovery. Infrequently traded markets dominated by distressed sellers do not. By the same token, infrequently traded markets dominated by central bank purchases don’t provide good price discovery either.

With the price discovery of bonds being in flux right now, the job of inferring longer-term inflation expectations becomes that much harder. As Dylan Grice points out, higher prices are evident everywhere except in longer-term inflation expectations!

I think the explanation is fairly straightforward. The most commonly used indicators for inflation are related to bond prices and central bank guidance. Central bank guidance has never been good at predicting major changes in inflation and bond markets have lost much of their signal after central banks have trampled all over them.

As a result, my judgment is markets have yet to catch up to the reality that longer-term inflation will be higher. If that happens, there will be another big shoe to drop on markets.

Monetary policy

BlackRock Gets Read the Right-Wing’s Riot Act ($)

Andrew Bailey dashed the hopes of pension funds on Tuesday, ruling out continuing the Bank of England’s £65bn bond-buying intervention into next week.

By Wednesday morning, this had changed to:

The Bank of England has signalled privately to bankers that it could extend its emergency bond-buying programme past Friday’s deadline, according to people briefed on the discussions, even as governor Andrew Bailey warned pension funds that they “have three days left” before the support ends.

A few hours after that, the story was amended again:

A sell-off in UK government bonds accelerated on Wednesday, sending long-term borrowing costs higher after the Bank of England reiterated its plans to halt its emergency gilt-buying scheme as scheduled on Friday. The central bank said on Wednesday morning that it “has made clear from the outset, its temporary and targeted purchases of gilts will end on 14 October”.

John Authers reported on what he calls “an acute problem with messaging” from the BOE which is likely to indicate “serious confusion”. The problem seems to be going around:

If these were the only two cases, we could probably chalk things up to happenstance, but similar mixed signals came out of the Fed and BOJ as well - which establishes a fact pattern.

At best, these instances represent some coordination problems or mild disagreements. At worst, they represent lack of cohesive strategy and/or lack of cohesion within the organizations. Regardless, multiple cases of “serious confusion” at the highest levels of financial authority do not bode well for the probability of navigating a soft landing.

Investment landscape I

Bailey’s gambit ($)

https://www.ft.com/content/d3033997-4fa6-42e4-948b-e6a48f479ddb

This is how Edward Al-Hussainy of Columbia Threadneedle summarises the worst-case scenario: The Bank of England entered the market, which is dislocated because of the pension funds’ need for liquidity. It says, you guys are desperate, sell at today’s low prices; we’re not paying you what the bonds were worth two weeks ago. But the pension funds really don’t want to be forced sellers and crystallise losses on their bonds. They say, this market is going to be better next week, we’re not selling here.

The thinking could be: if you are not willing to take the prices we are offering by Friday, you must not really need our help. And this may be quite right.

Andrew Bailey, governor of the Bank of England stirred things up on Tuesday when he told markets “the BoE’s special bond-buying operation would end, as planned, on Friday.” Comments immediately started pouring out complaining of a big central bank “mistake”.

There are a lot of moving pieces and different takes to this story but there are also some really important revelations. For one, the tone of Bailey’s message was, according to Robert Armstrong, “very far from ‘whatever it takes’.” In other words, this had the appearance of positioning the central bank very differently from what Mario Draghi did with the ECB back in 2012.

This hints at another revelation. While central banks do have responsibility for maintaining financial stability, it is not a universal obligation. Market participants have obligations too. This episode clearly reveals some bad behavior on the part of pension funds and other market participants. They screwed up and now they want the central bank to make them whole.

Bailey’s proposition makes the central bank the lender of last resort, but at a cost. By making support contingent, he is also making a statement that the role of the central bank should not be to socialize the risks taken by greedy or incompetent investors. This all sounds very sounds very reasonable to me.

One takeaway is the degree of vocal hostility to the BOE indicates how dependent markets have become on central banks to keep them afloat. Another takeaway is the degree to which blame is falling on the BOE diverts attention from pension funds that took unnecessary risks and other bad actors that contributed to the problem.

At the end of the day, nobody assumed responsibility for the greater good and there is plenty of blame to go around. This is just one more case of the finance industry taking risks with other peoples’ money and begging for help from the central bank when things go bad.

There is plenty more of this type of activity to come. It is the tremor that warns of bigger earthquakes on the way.

Solvency Constraints

https://fedguy.com/solvency-constraints/

A steady upwards march of sovereign yields would likely lead to financial instability by pushing some financial sector entities into insolvency. Global regulations post-GFC mandated many of these entities to hold sovereign debt as safe assets, but sovereign debt is actually not safe.

Financial stability concerns will likely force all central banks to eventually support the bond prices of their respective sovereigns.

Fedguy Joseph Wang discusses some of the bigger picture ramifications highlighted by the gilt market disruption this week. The first is longer duration bonds go down when rates go up regardless of credit standing. One direct implication is, “sovereign debt is actually not safe”.

This is important. Sovereign debt is used as collateral for a number of transactions and when the value of collateral declines, margin calls go out. This highlights the need for active liquidity management.

Further down the road, there are also policy ramifications. Countries with excessive debt will be forced to support their bond markets by suppressing bond yields to keep them below inflation. This will make bonds terrible investments. Further, since the US will likely be last in line to suffer this indignity, the US dollar is likely to remain strong for some time.

Investment landscape II

This is extremely important for a number of reasons. One, real estate is a huge asset class globally. Two, the phenomenon of mismatched duration - owning illiquid assets but providing short-term liquidity - is a far-reaching one. It will affect a lot of investors. Three, many of the assets affected have been added to portfolios as “diversifiers”.

These items all have a common thread in that they make use of securitization, leverage, or both. If you want an excellent overview, read Ben Hunt’s piece, “A Brief History of the Past 10,000 Years of Monetary Policy and Why Last Week Was a Big Deal”.

In an environment of low and declining interest rates, such as what we’ve experienced the last forty years, none of the items above are especially problematic. Debt can always be rolled over and asset prices rise as an inverse function of rates declining.

The shortcomings very quickly become toxic once the underlying assumptions of low and declining rates are violated, however. Suddenly, debt must be refinanced at higher levels and higher rates depress asset values, which depress collateral in many transactions. Suffice it to say, these problems are bubbling up to the top of portfolios all over the place and won’t stop any time soon.

Implications for investment strategy

In a challenging market, what you don’t own is often more important than what you do own. Once the underlying assumption of cheap and easily accessible credit no longer holds, problems start cropping up everywhere.

One of the first places investors will notice it in retirement portfolios is with real estate holdings. This will prove a doubly disappointing development since these holdings were often added to help diversify the portfolio. Instead, investors will experience poor performance and high correlation.

Another problem that is starting to show up is the gating of funds. Gating means investors aren’t allowed to sell the funds because there is not enough liquidity in the underlying investments to cash them out. So guess what? Investors in these funds will be riding out the turmoil without access to their money and in all probability, while prices continue to ratchet down.

Finally, in order to achieve truly uncorrelated returns, investors will need to find return streams that are unrelated to securitization and leverage. There aren’t a ton that are accessible to individual investors, but some do exist - and gold just happens to be one of them.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.