Observations by David Robertson, 11/5/21

Stocks have been rocking and rolling and bonds have too but in a different way. For an analyst, things are starting to get very interesting. Let’s take a look …

Let me know if you have comments. You can reach me at drobertson@areteam.com.

Market observations

Probably the most notable happening over the past couple of weeks has been the steady rise in stocks to new all-time highs. This has coincided with a dramatic decline in stock volatility and has focused on more speculative stocks.

They're "Foaming At The Mouth" - Nomura Raises Red-Flag At "Clown-Car" That Is Equities

https://www.zerohedge.com/markets/theyre-foaming-mouth-nomura-raises-red-flag-clown-car-equities

“...as a client points out to me this morning, this ‘cheap IWM vols / upside grab’ just so happens to also be yet-another expression of ‘foaming at the mouth’ Reddit WSB Robinhood YOLOers too, as HILARIOUSLY, the largest holding nowadays in Russell 2000 / IWM just happens to be meme stock legend AMC”

While there is clearly a lot of speculative interest, it differs from the ebullience of past bubbles. Raoul Pal recently sent out a Twitter thread which describes his take on the investment landscape …

The link to the thread is here:

Pal describes: “These young people had been let down by us all. Why should they play by our rules when they could make their own?” As a result, Millennials feel as though they have “nothing to lose”. Since 10% returns will do nothing to level the playing field for them, they believe they must take on “MASSIVE risk”. He concludes by saying “This is ALL about culture” and “Everything will change”.

This perspective does shed light on a number of things. For example, it demonstrates why the persistent setting of new all-time highs seems to lack enthusiasm. The answer is that “ebullience” is the wrong characterization. A better one might be “defiance”. In other words, the worse fundamentals are, the more interested mobs of retail buyers seem to become – because that is where the “MASSIVE risk” opportunities are.

While there have been plenty of fireworks in stocks, there have also been quite a few sparks in the bond market as well. Short rates have increased, and longer rates have decreased which has flattened the yield curve. While theories abound as to the causes, it is clear the confluence of rates administered by central banks, increasing inflation, and uneven economic growth are producing a great deal of uncertainty.

Companies

Zillow was not smarter than the housing market ($)

https://www.ft.com/content/3d610714-48f8-4b0e-bba6-1056fb431610

“Nobody understands the housing market better than we do. We intend to keep these homes for less than 90 days. We have a lot of predictive capabilities based on our housing data and our consumer insights, and we think we can weather any downside risk better than anyone. We’ve taken a lot of prudent measures to mitigate and minimise risk here. The most obvious one is that we will see issues coming because of consumer demand trends and data that we have on the housing market. And we can adjust our purchasing and we can adjust our selling commensurate with market conditions.”

“Fundamentally, we have been unable to predict future pricing of homes to a level of accuracy that makes this a safe business to be in. We hadn’t modelled this kind of pricing market nor supply market to even be possible when we got the business going. And we’ve seen all this volatility in both directions, right now in the wrong direction . . . ”

The first quote is from a co-founder and board member speaking about the house flipping business opportunity before the quarterly results. The second quote is the CEO on the quarterly conference call explaining why they are shutting the business down.

Countless new businesses have been justified on the basis of readily available capital, high hopes, and “because data”. While the ability of artificial intelligence and other technological tools is certainly creating opportunities, the challenges of modeling human behavior and other complex processes remain daunting and error prone. The main lesson, which any investment analyst already knows, is more data does not automatically lead to better performance. We’ll be hearing more stories like this one.

Supply chain

I’m A Twenty Year Truck Driver, I Will Tell You Why America’s “Shipping Crisis” Will Not End

“Think of going to the port as going to WalMart on Black Friday but, imagine only ONE cashier for thousands of customers. Think about the lines. Except at a port, there are at least THREE lines to get a container in or out. The first line is the ‘in’ gate, where hundreds of trucks daily have to pass through 5–10 available gates. The second line is waiting to pick up your container. The third line is for waiting to get out. For each of these lines the wait time is a minimum of an hour, and I’ve waited up to 8 hours in the first line just to get into the port.”

For those of us not intimately involved with supply chains, it is easy to imagine the increasingly frequent delays and shortfalls as a function of laziness or incompetence. This article sheds a great deal of light on the industry and how it operates. In doing so, it also illustrates how intractable many of the problems are.

For example, for arm-chair supply chain managers, it may seem like we just need to throw more trucks at the ports in order to start clearing them out. However, the author reveals, ““most trucking companies won’t touch shipping containers.” The reason is most port drivers are independent contractors who get paid by the load. As such, long delays at ports effectively slash their compensation to such low levels as to not be economic.

This hints at another issue: Much of the economics of the supply chain has been built on the foundation of cheap labor …

“Before the pandemic, through the pandemic, and really for the whole history of the freight industry at all levels, owners make their money by having low labor costs — that is, low wages and bare minimum staffing. Many supply chain workers are paid minimum wages, no benefits, and there’s a high rate of turnover because the physical conditions can be brutal (there aren’t even bathrooms for truckers waiting hours at ports because the port owners won’t pay for them.”

As it turns out, this form of economic enterprise built on the foundation of cheap labor has many other manifestations in our economy:

Staggering stat: 56% of grocery workers want to quit

“The reasons grocery workers plan to quit include burnout (58%), poor compensation (52%) and lack of appreciation from management or peers (53%), per the survey from Axonify, which provides online training materials for frontline workers.”

As Axios concludes, “The pandemic revealed how much we rely on low-wage, frontline workers, but it also exposed the ugly ways in which these essential workers are treated by employers and consumers alike.”

One takeaway is this system is not nearly as resilient as we might have hoped or believed. It turns out that “ugly” treatment of “essential” workers across many industries is not an incredibly sustainable condition. It is hard to imagine how this will get resolved without a fundamental restructuring of the social compact for these jobs. It is also hard to imagine how that can happen cheaply or quickly.

Politics

Crazy at Any Price ($)

https://gfile.thedispatch.com/p/crazy-at-any-price

“The other week I noted that a lot of Americans say they want the government to provide free college tuition and free universal health care, and to fight climate change. But when you ask them if they’re willing to pay $2, $10, or $100 more a month for these things, support drops precipitously (even if they’d still come out ahead).”

“Progressives constantly insist that the contents of the Build Back Better pinata are popular. But such popularity rests on the fact that people have been told that this stuff will be free because the rich will pay for it all. Ask people to pony up—even a little—and the support drops.”

Jonah Goldberg makes a couple of excellent points in this high-level assessment of the spending plans going through Congress. As is often the case, simple preference statements are often interpreted as “mandates” by political operatives. This is one of the many ways in which voters are not fairly represented.

The bigger point, however, is voters are also to blame. By freely stating preferences without any consideration to tradeoffs, they invite such misrepresentations. By failing to accept tradeoffs, voters create an enormous incentive for politicians to make promises that cannot be kept. Until voters and their representatives can agree to make crucial tradeoffs, public policy is likely to be commandeered by the most emotionally evocative ideas rather than those that can do the most public good.

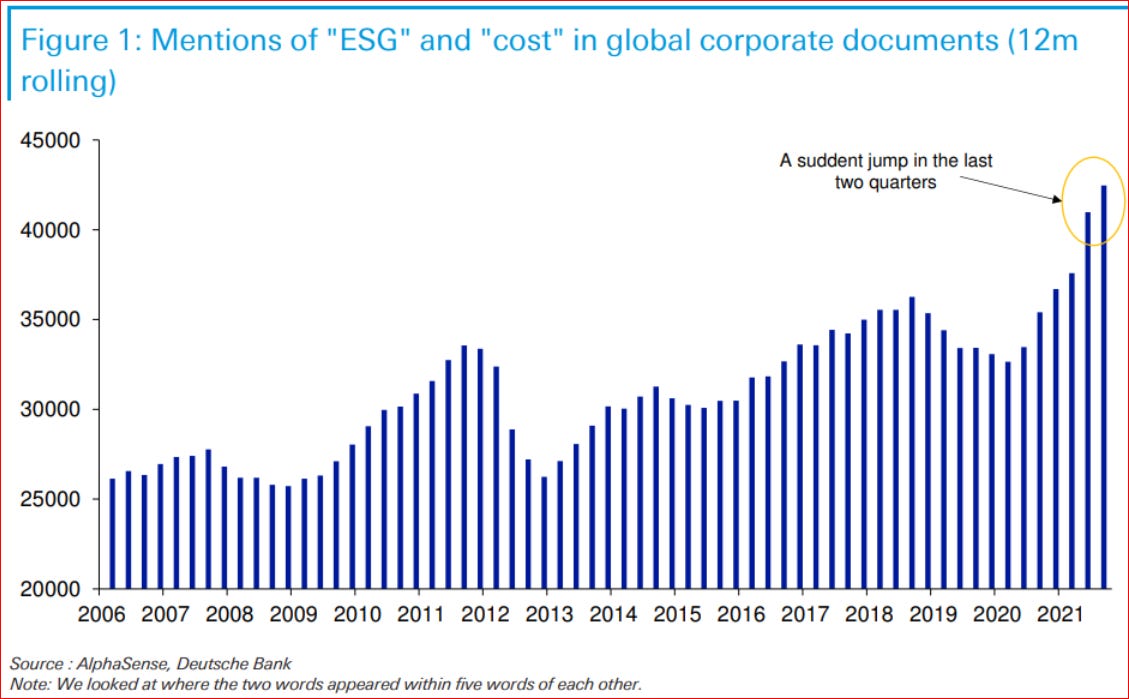

The Earnings Rally Was Great. Shame It's Over ($)

“A fascinating new report for Deutsche Bank AG, written by Luke Templeman (full disclosure: a former colleague) shows the problem. First, analysis of corporate communications shows that companies are talking a lot more about environmental, social and governance concerns in the last year, and that they tend to juxtapose ESG with the word ‘cost.’ The costs of cutting emissions, under pressure from ESG investors, are becoming onerous:”

One of the best illustrations of our political quandary is that of ESG. While many people agree broadly with the idea of good stewardship of the physical and social environment, opinions vary widely as to how much to spend on those goals. To date it hasn’t mattered much. ESG funds have been successful gathering assets mainly by focusing on businesses which structurally have low carbon footprints. That’s easy.

Things are about to get harder. As ESG principles permeate more deeply into the business landscape, all companies are being forced to incorporate them. For many businesses, doing so entails real costs. As those costs filter through businesses, at least partly in the form of higher prices, we’ll start learning exactly how interested consumers and voters are in these programs.

Cryptocurrencies

Rabobank: You Can't Raise Rates AND Prop Up Our Current Idiotic System

https://www.zerohedge.com/markets/rabo-you-cant-raise-rates-and-prop-our-current-idiotic-system

“If all of this craziness wasn’t enough for a Wednesday, yesterday also saw epic swings in crypto. ‘Shiba Inu’ --to quote Zero Hedge, ‘the Ethereum-based Dogecoin copycat altcoin which has a total circulating supply of 1 quadrillion’-- saw a surge in orders so large that it dragged down other crypto assets. Let’s unpack this, shall we? A *copy* of an altcoin --so, self-printed electronic ‘money’, on a platform full of other self-printed ‘monies’-- which is mimicking an ‘original’ altcoin openly self-printed as a *joke*, and which has a ridiculously large volume in circulation as a *double joke* about scarcity value, suddenly saw its price surge to give it a ‘market cap’ larger than many multinational corporations. And, in doing so, it took down the price of ‘establishment’ crypto jokes like Bitcoin – which Wall Street and the White House now appear to want to embrace as part of our ‘financial system’. (‘Mr. Smith, your Bitcoin ETF fund is down 10% today, because somebody launched a William Shatner-based Shatcoin. You understand, of course, that this is just how normal markets work. Prices of self-printed jokes can go up or down.’)”

This is a grumpy rant by Michael Every of Rabobank but captures a lot of the reality of cryptocurrencies right now. On one hand, the degree of pure speculation and shady activity is absolutely shameful. On the other hand, there is some really cool technology that can make a lot of things better. This point is not lost on Jim Bianco in this interview with Grant Williams ($):

“What I have argued to people, because all my customers are traditional financial types, as well. It is worth your time to invest your time to understand this space, because I think it’s going to be a big deal. Now, there’s two things going on at once. There’s the Ho-Chunk Casino, and it’s all out of control, and there’s a lot of insane speculation, and most of these coins will probably go to zero. But underneath that, there is a real technology in a change.”

Bianco goes on to specify the opportunity: “I think that one of the problems that we have in society is inequality. One of the drivers of inequality is the financial system, in that it is inherently unfair for the lower end of the income spectrum.” Fair enough; crypto can help reduce inequality. The enormous challenge is learning about crypto without getting caught up in the multitude of scams and the proliferation of pointless schemes.

Inflation

As the Fed decided to start tapering this week, the debate about inflation rages on. Some prominent and respected voices such as Lacy Hunt, David Rosenberg, and Gary Shilling continue to argue for deflation on the basis of excessive debt and its debilitating effect on growth.

While I very much respect these arguments, I still believe in the longer-term prognosis of inflation. The reason is simple: When debilitating debts and slow economic growth persist, they become political problems as much as economic problems. And, as Russell Napier ($) pointed out in this Realvision interview: “The market has a powerful way of disciplining politicians, I would say. So, I wouldn't worry too much about politicians not spending money.” In other words, if politicians don’t spend their way out of economic weakness, they don’t get re-elected.

Further, politicians have already secured funding for those spending needs by way of what Greg Jensen ($) from Bridgewater Associates calls “Monetary Policy 3 … the merger of fiscal and monetary policy”. As a result, there is both a will and a way to create inflation.

Importantly, the “way” is comprised of more than just spending. While much of the analysis of inflation relates to economic growth, the fact of the matter is in many cases costs are just going up. A little discussed phenomenon has been the disinflationary impact of things like globalization and increasingly efficient supply chains. With production becoming more regionalized and supply chains being reconfigured, many of the forces that helped keep inflation at bay are now receding. As a result, inflationary forces are being helped by both demand/supply imbalances and by reduced operating efficiencies.

Implications for investment strategy

One thing that has become clear over the last few weeks is the resilience of the market, even in light of, or perhaps in spite of, a whole host of risks. Regular readers know I believe stock valuations are unattractive which means expected future returns are significantly negative at this point. So, does this mean investors should be completely avoiding stocks right now?

My answer to that question is, “No”, but it comes with caveats. First, it is important to understand I write primarily for the purpose of long-term investing. For the purpose of building a retirement portfolio, I do think stocks in general are extremely unattractive right now. However, I acknowledge the persistent strength in the market and I also acknowledge that many younger investors may have different goals and risk tolerances.

As a result, for those inclined to “take a flyer” on a hot stock or two, I get it – and there is nothing inherently wrong with it. It is not long-term investing, but a lot can be learned from the exercise. The main point I would make is to be sure to only bet money you can afford to lose. Another is to be careful to not learn the wrong lessons. Making a lot of money by being lucky is often a recipe for losing a lot of money later. Conversely, losing a lot of money on a bad risk can make it hard for you to take smart risks in the future.

One of the areas where I think significant money will be lost is in regard to inflation. Markets still seem slow to adapt. Russell Napier described the positioning he observes:

“So, my job is to speak to professional investors, I would say two-thirds of them probably still believe in transitory inflation. So, if the owners of government bonds or a lot of them still believe in transitory inflation, there are some of them who think that these yields compensate them for inflation, because they think inflation is coming back down. Now, if they change their minds, are they buyers or sellers of bonds? Well, given where inflation is and given where yields are, they're likely to be sellers.”

While there are still valid concerns about inflationary pressures in the short-term, the longer-term picture is actually becoming clearer. Napier concludes, “The market, in my opinion, is way behind on inflation expectations and is in for a nasty shock. So, things could change quickly.” This is the one thing long-term investors should be focused on right now.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.