Observations by David Robertson, 1/17/25

The CPI number was the big news this week and next week the inauguration on Monday is likely to provide a starting gun for a whole new news cycle. Hope you get some rest this weekend!

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The consumer price index (CPI) was reported on Wednesday and the headline number came in a little hotter than expected but the core number came in a tad lighter than expected. That was enough to spark a big rally in stocks, bonds, and most everything else. The S&P 500 was up almost 2% and the 10-year bond yield dropped almost 14 bps.

The superficial interpretation was that inflation is back on its downward track which will facilitate more rate cuts this year. A deeper read-through suggests the moves were more of a relief rally than a meaningful change in trend. Most of the move in stocks happened in futures immediately after the CPI report. The US dollar dropped significantly on the report, but fully recovered by the end of the day. At any rate, there seems to be a certain jumpiness to markets early in the year.

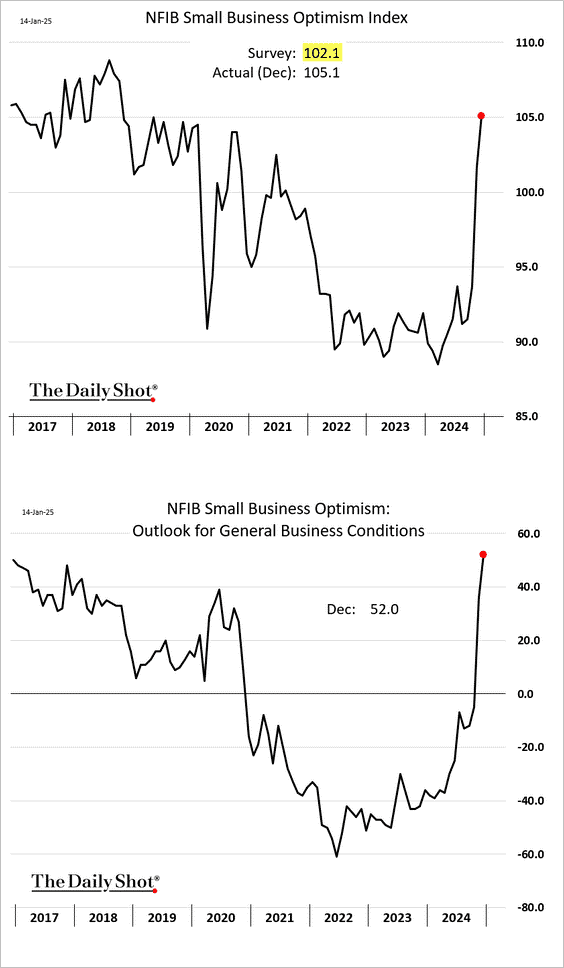

Small business is an important driver of the economy and The Daily Shot picks up on distinctly mixed messages from that group. On one hand, optimism spiked up after the election.

On the other hand, actual employment cratered in December.

I have not heard a good hypothesis to explain this paradox but I am a big believer that actions speak louder than words. Insofar as that is the case, it seems as if small businesses have high hopes for Trump being able to dramatically improve their actual business conditions once he becomes president. I guess we’ll see.

Finally, with the inauguration on Monday, there’s a good chance we’ll start getting a steady stream of news with market-moving implications. Buckle up, it’s going to get bumpy!

China

In yet another great thread from Michael Pettis, he debunks the myth that what China really needs is a big enough stimulus program:

In fact China does not need "more stimulus" nor even "more monetary easing" to boost inflation and raise bond prices, nor is that what the bond markets are saying.

That's because, contrary to the implicit assumptions of most analysts, the Chinese monetary and fiscal systems do not operate like those of the US or the EU, as I explained a few months ago. carnegieendowment.org/posts/2024/0...

While in the US and the EU fiscal and monetary expansion tends to be directed to the demand side of the economy, in China (like in Japan in the 1980s and 1990s) it is almost wholly directed to the supply side of the economy.

One takeaway is that US policy is often not a good analogue for Chinese policy. While US initiatives tend to be demand-focused, Chinese initiatives tend to be supply-focused. Boosting these leads to very different outcomes.

Another takeaway is that China’s bias to helping the supply side is the root of the problem itself. Boosting supply is more likely to exacerbate problems than to solve them. What is required is a shift in policy orientation to consumer demand. Therefore, it is the nature of the program that is a key milestone for progress, not the size of the program.

Geopolitics

I have been highlighting the increasing importance of geopolitics as an investment theme for a couple of years, most recently with the 2025 Outlook piece. To a large extent, this has been an uphill battle as traders and short-term investors often pooh-pooh geopolitics because it so rarely impinges meaningfully on daily activity. As a result, Michael Every’s report, “Macrostrategy vs. 'Grand Macro Strategy'“ (h/t @SantiagoAuFund) is an especially welcome supplement to help explain the “What” and the “Why”:

For markets, the recent, rude interjection of national security is ‘new’.

Economic statecraft uses economic means for foreign policy/national security goals [as opposed to purely for economic goals], e.g., to force a state to cease hostilities with a third party, open its markets, or act in a certain manner.

The conclusion is that markets should be prepared to supplement purely economics-focused macrostrategy with a fusion geopolitical ‘grand strategy-plus-economics’ lens, which we dub ’Grand Macro Strategy’

Grand strategy: identifying national interests and how to achieve them within the international system by using three tools: the economy, in tandem with political and military power.

One major point to take away is that the pre-eminence of national security changes the equation for the prioritization of economic policy. Just as soon as real threats are perceived to a nation’s security, economic policy becomes subservient to those higher goals. “Money does not always talk”. This is something the US hasn’t seriously dealt with in a long time.

Another major point to take away is that “Grand Macro Strategy” rarely produces insights that are exploitable for short-term trades. Rather, it highlights high level positioning and strategic counter-positioning that can shed light on relative strengths and vulnerabilities of the players as well as potential paths forward. Such insights can be enormously useful for long-term investors, not least of which for the purpose of better managing risk.

Every warns, “A more geopolitical world, by definition, should arguably preclude sole reliance on business-as-usual economic or market thinking.” It will likely take some time to fully appreciate this warning, but it is a good one nonetheless. One thing is clear, as Axios presents, global CEOs aren’t waiting around to incorporate geopolitics into their plans.

Inflation

The intent focus of traders and financial media on the consumer price index (CPI) report this week revealed a preoccupation with short-term patterns in inflation and their potential impact on monetary policy. Unfortunately, neither of these targets of attention is likely to be very useful for long-term investors. Fortunately, Mike Green does provide some helpful perspective in his recent Substack post.

First, while he was overly pessimistic last year about the economy and prospects for inflation, Green was right about the seasonal tendencies of inflation statistics and many of the underlying weaknesses in the economy. These are likely to become more pressing issues as Biden administration stimulus efforts taper off and higher rates start taking their toll.

The really big issue for investors is not how long it takes for inflation to taper gently down to the 2% target. Rather, the really big issue is whether government has commandeered monetary policy in a way that generates persistently higher inflation or whether growth is slowing so much that there could be a deflation scare. Green’s response aligns almost perfectly with that Russell Napier who I have discussed before:

The inflationary response is coming, just as it did for COVID, but FIRST comes the credit event. As discussed in today’s note, the simple reality is that deflation, not inflation, remains the risk.

This is a change in my outlook from last year. While I still believe financial repression is coming (and the inflation that feeds it), it does increasingly look like there will be some kind of deflationary scare first.

Investment landscape I

Robert Armstrong ($) picked up on something that isn’t being widely discussed yet: “Something significant has shifted in markets in the past month or so. We can all feel it. What exactly is it?”

I agree; it does feel like something has changed. Mainly, that something seems to be rising bond yields. It’s not so much that they are rising per se, which they did last year as well. It’s more what the rise signifies.

Armstrong goes through the usual suspects to evaluate causes — inflation, growth — and doesn’t find those stories particular story extremely compelling. Paradoxically, that may be exactly the problem:

The big change in the stock market, then, is not driven by a particular narrative about the economy, the trajectory of earnings or the direction of capital flows. It is driven by the lack of a clear narrative. Whether this is down entirely to the political transition taking place in the US is open to question. It does seem, however, that the incoming president’s policy of strategic ambiguity is hard for the market to process.

This presents an interesting, and I think largely accurate portrayal of the past fifteen years or so. After the GFC, monetary policy (and forward guidance) led financial markets. The narrative was one of omnipotent central bankers. After 10-year US Treasury yields hit nearly 5% in 2023, Treasury tilted its issuance hard towards bills instead of bonds. The narrative was that there was a ceiling imposed on bond yields.

In both cases, traders and investors did well to follow the lead of these monetary authorities. Essentially, all they had to do was follow the narrative that was delivered as if it were gospel.

Now, with a new administration coming in that will likely have different policies, a predominant narrative has yet to be revealed. Further, neither the Fed nor the Treasury has the same latitude to impose control that they had in the past. As a result, it is unclear where yields should go, where the new administration would like them to go, and how much authority it will have to guide them there. It’s as if an artist who learned to color by numbers no longer has the numbers for guidance.

One of the more unsettling aspects of this situation is that policies of the past were set largely to either promote or protect stocks. The notion that such protection may be going away is troubling. However, it may be worse than that. A strong argument can be made that the incoming Treasury secretary would prefer to have higher bond yields — as an attraction for luring price-sensitive buyers. That would be good for shoring up the sustainability and reliability of the Treasury market, but would expose the stock market to a number of risks.

Investment landscape II

As the fires in LA continue to wreak havoc and upend people’s lives, they also continue to add to the tally of insurance liabilities. As the Daily Shot shows, the current LA fires have already crushed the record for insured losses.

This prompted an exchange on X:

This [LA fires] is going to start the equivalent of a bank run, but of insurance companies pulling out coverage for anything even remotely high risk around the country, right?

Yup. Already happening.

In one sense this seems innocent enough. Of course businesses like insurance companies would seek to avoid adverse selection. However, this is about more than that. The really unmanageable risk for insurance companies is not losses that can be modeled, but politics — which cannot. Who knows what kinds of rewards and/or business constraints public bodies could impose in the context of a big catastrophe that brings a lot of bad PR? Hurricanes in Florida did the same thing over the summer.

The real issue is these catastrophes reveal a dirty secret about insurance: A great deal of it is underpriced for the risk that is absorbed. This means one of three general things will happen. One is that prices will go up for many kinds of insurance in order to fully account for the risks that are taken. Another is that some things, like houses in parts of California and Florida, for example, will become uninsurable.

A third, is that some insurance books will prove to be under-reserved and therefore will not be able to pay out valid claims made on them. Ultimately this means there are hidden liabilities. Someone will have to cover the claim — either the state, the federal government, or — the person who thought they had adequate insurance coverage. Ouch.

Portfolio strategy

On many occasions I have discussed the popular 60/40 (stock/bond) allocation strategy, the historical anomaly of its performance, and its structural weaknesses as we enter into a different investment landscape. Recently, other voices have also been getting louder.

Convexity Maven Harley Bassman posted:

For the past two decades, Investment portfolios (as well as Hedge Fund fortunes) have been built on the 60%/40% stock//bond allocation that relies upon their inverse correlation.

This may soon end as interest rate near 5.0%

Why...?

1) Discounting equity earnings at higher rates

2) Bonds become competitive with stocks

3) Higher rates slow earnings growth

These are all valid points about which stock investors have had little concern for many years. Bassman concludes, “I am not calling for a "crash", but I will say that at some point higher rates will hit the stock market; so my only advice is to reduce your leverage.”

I agree with @ConvexityMaven that the “modern” 60/40 portfolio is over. And I share his concern that too many still think the negative correlation still exists, and their “hedge” will fail them at the worst time.

The bottom line is market conditions are changing in a way that invalidates much of what has worked in the past. First, interest rates started getting reset higher to historically more normal levels in 2022. Second, as bond yields reset higher to historically more normal term premia, both stocks and bonds will be at risk. The forces that created so many tailwinds for the 60/40 portfolios are now turning into headwinds.

As a result, it appears as if we are at a major inflection point. At the same time, portfolio strategies are still dominated by the 60/40 strategy. This is exactly why I introduced the Areté All-Terrain allocation strategy in August 2021 — to provide a valuable alternative to the 60/40 portfolio. There will be others, I’m sure, but I’m also sure a lot of investors will have a really hard time adapting to the new environment.

Implications

The biggest issue for investors right now is bond yields. Mohamed El-Erian highlights the challenge:

Per Bloomberg article by Michael Mackenzie and Ye Xie, “Global Bond Tantrum is Wrenching and Worrisome Start to New Year.” A key question is whether “the shift in yield is seen as a paradigm shift, with some experts predicting a new normal of higher interest rates” or “it’s a temporary phenomenon.”

If it’s a temporary phenomenon, then it’s just a matter of waiting for bond yields to recede and stocks will be off to the races again.

However, there are several reasons to be less sanguine. For one, there is good reason to believe that bond yields play a role in “Grand Macro Strategy” for the US. For example, bond yields that are too low can create geopolitical vulnerabilities. Too-low yields prevent money from being invested in real capital to build out industrial capacity and discourage banks from lending.

In addition, to the extent artificially low bond yields provide a boost to stocks, the potential for a collapse in stocks, and therefore collateral values, presents a threat to financial stability. Not the kinds of things you want strategic competitors being able to target as a source of disruption. In short, low bond yields and rich stocks are vulnerabilities in geopolitical conflict.

Further, as Bob Elliott points out, “Stock market exuberance hit a fervor right at a time when the economy got 100bps market-based hike. It is going to take more than the modest adjustment to prices we've seen so far to shake out the extreme sentiment in place to kick off '25.” In other words, it will not be a short or easy path to more sustainable asset price levels.

Assuming “Grand Macro Strategy” as a driving force, and I think it is, it becomes clear how little room there is for policy to navigate a smooth way forward for rates (bonds) or stocks. There is precious little middle ground. Do too little and stocks continue to levitate and present a risk. Do too much and you risk initiating a destabilizing selloff. Either way, the Grand Macro Strategy implies a paradigm shift and investors should be prepared for that.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.