Observations by David Robertson, 12/10/21

It’s been a topsy turvy couple of weeks and that is exactly the kind of environment that can shake the confidence of investors. It is also the kind of environment in which “Observations” is especially useful. If you have questions or comments, let me know at drobertson@areteam.com. Now, let’s take a look at what has been going on …

Market observations

The last several weeks have been a tug of war between de-risking investors and impassioned dip buyers. Clearly, retail investors are well conditioned to increase exposure at any modest decline in prices. They aren’t the only ones though as companies are also actively buying the dips …

BofA Saw Biggest "BTFD" Inflows Since 2017 As Buybacks Soared... But The Window Closes On Friday

“But the most notable observation in BofA's report was that buybacks by corporate clients picked up to their highest weekly level since March, with the bank calculating that corporations bought back $3.4 billion worth of their own stock, twice the level from the previous week and well above the recent weekly averages.”

"REKT" - Stocks Storming Higher On Massive Hedge Fund Short Squeeze

https://www.zerohedge.com/markets/rekt-stocks-storming-higher-massive-hedge-fund-short-squeeze

“The simple take home message from this data, which we posted on twitter late on Monday, is that with everyone shorting aggressively into the recent dump, it was only a matter of time before we had a face-ripping short squeeze higher...”

So here is another element of fun for traders and investors: With real market risks rising, some traders are rediscovering their interest in shorting stocks. There is just nothing like beating down a stock that is already suffering, for whatever reason. The only problem is those shorts can turn into massive liabilities if and when the market turns – which it did. The bottom line is that the elements are in place for extremely volatile trading.

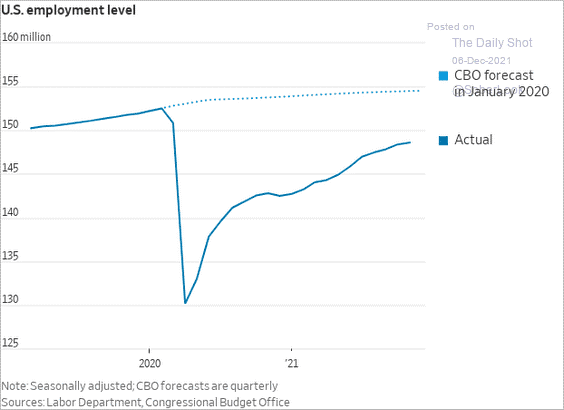

Labor

It’s been over a year and a half since lockdowns decimated employment so we are now at a point where we can make some assessments about the health of the labor market. The clearest pattern is that employment is coming back. What is also clear, however, is that employment is not on a trajectory to get back to anything close to pre-Covid levels.

One comment is this isn’t a huge surprise. I highlighted over a year ago the potential for temporary job losses to become permanent. I also wrote:

“Another insight suggests that unemployment may also be persistent. Although the estimate of 37 million fewer W-2’s probably overstates the number of workers affected (since some have more than one job), it nonetheless reveals the expectation of significantly lower employment levels for the remainder of the year.”

The main point is that it is absolutely possible to attain a pretty good understanding of many economic fundamentals by analyzing the data and drawing independent conclusions from it. Conversely, casually following headlines that are heavily influenced by narratives often confuses and obscures underlying conditions.

Another point is that the labor market is likely to remain structurally impaired. This problem is made even worse by the recent report showing productivity (the measure of output per hour worked) declined 5.2% for the third quarter. Fewer workers and lower productivity imply it will be harder for the economy as a whole to continue producing at the same level and that there is insufficient supply of labor (which should cause wages to rise).

Economy

How bad is the US economy? ($)

https://www.ft.com/content/90957187-c43e-44a7-9d70-d0218f64318f

“Voters believe the economy is bad, and no amount of stats can change their mind (at least in the short term). Jobs numbers, wage numbers, and the number of people we’ve put back to work don’t move them . . . [the numbers] will have limited impact when people are seeing help wanted signs all over main street, restaurant sections closed for lack of workers, rising prices and supply disruptions. Even where things are getting better, Biden doesn’t get credit.”

Economic growth is killing the market ($)

https://www.ft.com/content/643fe846-1604-4110-89d7-7e4ea3567e56

“It appears US consumers only see the current policy mix as providing a short-term stimulus. The major failure of the Fed/Treasury policy is that it has failed to increase longer-run consumer expectations about the economic outlook . . . so, the yield curve isn’t going to steepen until either consumer current situation perceptions ease (pulling down the two year) or longer run expectations pick-up substantially (helping support the longer end of the curve).”

Take a look at the GDPNow estimate of 8.7% growth for the fourth quarter, and one might assume the economy is flowing along swimmingly. Regardless of how representative that may or may not be, it is distinctly not the impression most people have.

For one, politics absolutely seems to be coloring perceptions of economic performance. For another, people don’t perceive fiscal and monetary interventions as having created sustainable economic growth. This presents a real problem. Until consumer sentiment improves, which presumably would follow improvement in productive capacity, it is fair to expect economic numbers to continue to lurch from one extreme to another.

Politics

The west is a victim of its own long peace ($)

https://www.ft.com/content/7d9dee20-e704-4dc1-94d9-c1c1938d6726

“Five years since the votes for Brexit and Donald Trump, it is still not understood how much populism boils down to antic rebellion rather than (the initial theory) economic grievance or (much more a leftwing thing) doctrinal belief. This is to some extent a movement of laughing cavaliers. Violence is not their wish, but nor do they recognise it as a plausible and unintended outcome of their doings.”

“To define the west’s problem as one of casualness, not wilful malevolence, is not to minimise it. In fact, it is much the harder problem to fix. The implication is that nothing short of a violent crisis will restore to people a healthy fear of the political extremes. Social media can be tamed, electoral dark money banned and education improved to little effect. These are tactical answers to a problem that could not be any more structural: in today’s grating argot, a lack of ‘lived experience’ of the consequences of populism.”

“If and when US democracy falls, giggling complacency, not moustache-twirling villainy, will be the presiding atmosphere … What has changed is the share of the wider populace who think no harm can come of extensively indulging them [populist leaders] … In toying with the likes of Trump, their main failing is one of imagination, not of conscience … It [the west] should expect its politics to wobble and lurch until such time as citizens taste the consequences again.”

The Race Between Consequences and Corruption ($)

https://frenchpress.thedispatch.com/p/the-race-between-consequences-and

“It’s consequences versus corruption. Can the instruments of American justice impose sufficient costs on the architects of the ‘Stop the Steal’ movement before the corruption of the Republican Party is complete?”

Both of these pieces discuss populism, and both highlight the importance of consequences. The fact of the matter is without severe consequences, bad behavior has a tendency to propagate. One take on the recent growth in populism is that it results from long, naturally occurring social cycles (think Fourth Turning). It will come and eventually transition into something else.

A less positive take is that in doing so, it will cause massive destruction and civil strife. There is truth to both, so it is important to remain realistic. That said, I have to admit to feeling very frustrated at times. I can see very clearly that a great deal of harm to society will be done (and has already been done). Yet, there is exceptionally little I, or anyone, can do about it. Too many people will be doomed to learning consequences the hard way – through their own direct experience with them. About the best the rest of us can do is go in with eyes wide open, stay true to our principles, and know that this too shall pass.

China

The US and China are already at war. But which kind? ($)

https://www.ft.com/content/583b44f7-5eb5-4967-983d-70d0f5573f5c

As [Ray] Dalio recently told me [Tett], “There are five kinds of war, and they are not all shooting wars. There’s a trade war, a technology war, a geopolitical war, a capital war and there could be a military war. We are certainly in varying degrees in the first four of those . . . and there’s good reason to worry about the fifth type.”

“However, [Graham] Allison has one final encouraging nugget to share: since his book was published, it has not only become a bestseller in the US but has been extraordinarily popular in translation in China too. ‘I never ever expected that,’ he chuckles, explaining that the most popular passage with Chinese readers is a description of how Britain and the US avoided a Thucydides moment in the early 20th century by not going to war. Even a trap can sometimes be escaped from.”

Two great points here by Gillian Tett at the FT. First, it doesn’t have to be a shooting war to be a war. I suspect many investors do not fully appreciate just how severe the impact of various non shooting dimensions of war can be if they continue to escalate. Another point is a somewhat optimistic one: Apparently many readers in China are also quite interested in avoiding a “Thucydides trap”.

Source: Zero Day Tracking Project. Graphic: Mehlman Castagnetti

China’s rising vulnerability to foreign investors ($)

https://www.ft.com/content/7a1cbb0e-ab57-4092-ba33-b231fc1b1783

“This faith in future inflows to portfolio assets is bolstered by the belief that those who construct benchmark indices of global portfolio assets, those conductors of blind capital, will only raise the weightings of China’s portfolio assets within those indices.”

“However, there is a growing list of reasons why foreign portfolio inflows to China can stop or even reverse. The increased risk of a cold war means it is not clear that foreigners will be permitted to fund the Chinese government’s military build-up through their purchase of Chinese government bonds.”

This report by Russell Napier gets at the heart of an incredibly important issue that is often sidestepped in mainstream media. It is nice and proper to talk about China as an “appropriate” investment destination when done in the context of diversification and exposure to passive funds. What is often not mentioned is that investment in China also amounts to funding its military build-up and therefore is ostensibly antithetical to US national security. Further, the size of those capital flows is becoming large enough to really matter.

Michael Pettis followed up with a tweet thread that basically agrees with Napier’s thesis, but he also argues the risks are less imminent. Either way, the issues are tricky and seem destined to receive some high-level political attention – probably on both sides. The important takeaway is that geopolitical activity will affect investment outcomes. As Napier concludes:

“Xi’s political goals are no longer compatible with a stable Chinese exchange rate. Xi has to choose between a flexible exchange rate and monetary independence or a deflationary economic adjustment with its attendant financial and political risks.”

Outlook for 2022

"Here Comes A Revolution!" - Saxo Bank Unveils Its 'Outrageous Predictions' For The Year Ahead

“The predictions focus on a series of unlikely but underappreciated events which, if they were to occur, could send shockwaves across financial markets:

1. The plan to end fossil fuels gets a rain check

2. Facebook faceplants on youth exodus

3. The US mid-term election brings constitutional crisis

4. US inflation reaches above 15% on wage-price spiral

5. EU Superfund for climate, energy and defence announced, to be funded by private pensions

6. Women’s Reddit Army takes on the corporate patriarchy

7. India joins the Gulf Cooperation Council as a non-voting member

8. Spotify disrupted due to NFT-based digital rights platform

9. New hypersonic tech drives space race and new cold war

10. Medical breakthrough extends average life expectancy 25 years”

While I am not normally a big fan of outlook pieces for the new year, I do enjoy the handful of pieces I come across that are thought provoking. This is one. I will admit some bias here; I like this list largely because it comports so closely with my own thinking. Each of these events is underappreciated and each could cause a great deal of havoc if realized.

I’ll go even one step further – I think there is an excellent chance most of these items will either happen or something very close to them will happen. As a result, the huge payoff bet would be that six or seven or eight of the items will ALL happen. Said a different way, I don’t think most people really appreciate how immensely unlikely a “return to normal” is.

Investment landscape

One of the key questions for stocks here is determining whether the recent dip is fairly routine and just a part of the process of moving up to even greater heights, or is indicative of a different regime altogether. I noted in September and early October many aspects of the selloff felt different and that remains true today. For example:

So much pain (for some/many) at All Time Highs ($), December 7, 2021 at 6:00:09 AM EST

https://themarketear.com/premium

“Two amazing stats:

Almost a third of the stocks in the Nasdaq Comp are down 50% from highs (see SocGen chart)

Over the last 6 months, 4 stocks (MSFT, AAPL, NVDA, GOOGL) have generated almost 70% of the S&P 500's return.”

In short, breadth has been terrible which is not a sign of a healthy market. Further, several conditions are setting up for unusually volatile year end trading …

The Powell-Put Has Been Struck Lower... And Don't Expect The Fed To Kick-Save Us Easier Anytime Soon

“SpotGamma also warns that while they are giving an edge to a rally into next week [this past week] – you must respect the downside. This is a market for large directional swings and not mean reversion. 12/17 expiration is 2 weeks out, and just ahead of that is a major FOMC meeting on 12/15. What comes from that FOMC will combine with an OPEX accelerant to make for a very interesting end to 2021.”

“McElligott concludes ominously that there is still hell to rain down (read, lots more $ selling).”

To be sure, volatility can be good for traders. Volatile conditions, however, often distinguish the pros from the wannabes since risk management becomes so much more important. We will see. In the meantime, the trend in the S&P 500 will be extremely important. If it fails to hit new highs and instead consolidates, it will open the door for a big downside move.

Also, as a quick reminder, demographics is one of the best long-term market indicators because it is a proxy of supply vs. demand for “stuff”. The graph above shows that the S&P 500 return has not just deviated from its historic relationship to demographics but has shot in exactly the opposite direction the last seven or eight years.

The reason for the deviation, of course, is extraordinary monetary policies that were implemented after the financial crisis and have continued ever since. The point is, monetary policy is the main force keeping stock prices afloat and when that force dissipates, there is a lot of downside. This is a critical factor for long-term investors who are trying to calibrate the right amount of equity risk to accept.

Implications for investment strategy

Since I get tired of hearing myself warning about the downside risk of stocks, I will let Paul Singer, the founder and co-CEO of Elliott Management, do it for me:

Investors piling on risk are setting themselves up for a fall ($)

https://www.ft.com/content/32e000cf-c95a-4940-8985-f67ca6170ae8

“However, the ability of governments to protect asset prices from another downturn has never been more constrained. The global $30tn pile of stocks and bonds that have been purchased by central banks in order to drive up their prices has created a gigantic overhang. With inflation rising, policymakers are reaching the limits of their ability to support asset prices in a future downturn without further exacerbating inflationary pressures.”

“Investors who have upgraded their risk levels, relying on policymakers to protect the prices of their holdings, may suffer significant and perhaps long-lasting damage when the government-orchestrated music finally stops.”

I couldn’t have said it better myself. While many investors continue to assume the Fed is both willing and able to rescue risk assets should danger appear, that assumption is becoming increasingly tenuous. As a result, this is an excellent time to assess your market exposure and make sure a significant and sustained selloff does not cause irreparable harm to your portfolio.

It is also an excellent time to adjust expectations for returns. Most people establish return expectations on the basis of what happened the last couple of years. This is not only flawed, but seriously flawed. I discussed the issue in regard to home prices in a piece almost ten years ago. Work from Robert Shiller and Karl Case showed at the peak of the housing expectations, people expected the return for the following ten years to be 12.6 per cent a year. The mathematical implication is that home prices would triple over that period.

The same thing is happening now with stocks. Not only are excessive recent returns being extrapolated far into the future, but they are also not being regressed to the mean. In short, it is more reasonable to expect returns over the next few years to be negative than to continue at the same rate as the last year and a half.

Some may complain that with inflation flaring up, stocks are real assets that can provide some protection. There is some truth to the statement, in general. However, there are also two major flaws. One is when inflation becomes endemic, valuations fall. At excessively high valuation multiples now, there is a long way to fall. Two, a large proportion of excess returns the last few years has been caused by excess money trapped in the financial system. As that money enters the mainstream economy, prices will go up and risk assets will go down. In other words, the inflation benefit has already been received.

So, what should long-term investors do to protect against inflation if traditional inflation hedges like stocks (as a whole) are unlikely to help much going forward? The most obvious tactical answer is gold which can protect against major regime changes. While there are other ideas as well, it is really important to adjust expectations. To a great extent, there are vanishingly few great investments, which often means “less bad” is a good goal. Accepting that will prevent investors from trying to accomplish too much. In other words, not losing too much is going to be the new “killing it”.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.