Observations by David Robertson, 12/31/21

It was a fairly quiet week in the market but the drama is building for some major market moving events over the next couple of years. As a result, it is a good time to take stock, reflect on where things are, start writing out the playbook, and prepare for some crazy things to happen. If you have questions or comments along the way, let me know at drobertson@areteam.com. Otherwise, Happy New Year!

Market observations

Should You Sell On Friday?

https://www.zerohedge.com/markets/should-you-sell-friday

A number of different charts have been making the rounds intending to provide guidance for traders. The insinuation is that these averages provide important clues as to what constitutes “normal” trading patterns and therefore create a template of expectations for the period. I just picked the one above because it was timely and convenient.

I could make many comments about these types of charts but I will keep it simple: While they appear to establish a viable template for trading, they provide only the very weakest outline of possibilities. The chart above, for example, covers a period of 35 years, but we have no indication of where trading actually occurred relative to the points on the line for any given day. We have no idea if the points on the line are indicative for any given day or simply an average of a wide dispersion of data points.

For that matter, the period from 1985 to 2019 is hardly representative of broader history since interest rates were in decline for essentially the entire period. Now that rates appear to be on the rise again, that particular history is worse than unhelpful; it is actually a misrepresentation of what investors are likely to confront.

The fact that such simplistic models are getting so much play seems to speak much more to the willingness of many investors to accept even very weak suggestions than to the informational content of the models. All of that said, there are some pieces of seasonal information that can be useful.

The following graph, posted by themarketear.com on Dec 27 2021, illustrates the seasonal effect of money flows. Obviously January is a big one and that makes sense since year-end bonuses can be slogged away and annual limits for retirement programs are reset. These are valid reasons to expect above average flows of cash to enter the stock market - and therefore for the bias on stocks to be upward, all else being equal. By the same token, look out for the period of May through August.

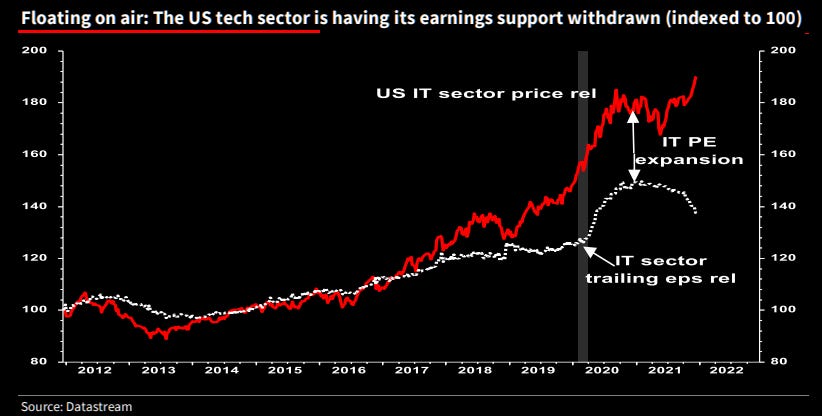

Technology

Tech has been the stalwart of 2021 but is increasingly the big worry for 2022. Looking at the chart (from themarketear.com) it is easy to see why. Not only has tech stock performance been driven hugely by multiple expansion, but recently stock prices have diverged from earnings: Stocks have been accelerating up while earnings have been accelerating down. Many tech stocks were clear beneficiaries of lockdowns and working from home. Going forward the comparisons will be negative.

Other headwinds are blowing as well. Regulators are sharpening tools to keep tech companies in their place. Rates are going up and that reduces the value of prospects far out into the future. Insiders are selling out at record rates. Investors who have been around have seen this movie before - and it doesn’t end well.

Coronavirus

The Morning Dispatch: Omicron Meets Hospital Overwhelm ($)

https://morning.thedispatch.com/p/the-morning-dispatch-omicron-meets

“That burden [of more Omicron cases] is going to fall squarely on an American healthcare sector that, according to the Bureau of Labor Statistics, is employing about 450,000 fewer workers than it was at the beginning of the pandemic. A three-percent contraction may not sound like much in the context of total U.S. employment falling about 2.6 percent over the same time period, but the churn within the field has been staggering. An October Morning Consult survey found just under one in five healthcare workers had quit their job since February 2020, and among those who hadn’t quit, 31 percent reported thinking about it. A whopping 66 percent of acute and critical care nurses said the pandemic had caused them to consider leaving nursing entirely, according to an American Association of Critical-Care Nurses poll from September.”

“In the spring of 2020, ‘I’d walk past an ice truck of dead bodies, and pictures on the wall of cleaning staff and nurses who’d died, into a room with more dead bodies,’ Lindsay Fox, a former emergency-medicine doctor from Newark, New Jersey, told me. At the same time, Artec Durham, an ICU nurse from Flagstaff, Arizona, was watching his hospital fill with patients from the Navajo Nation. ‘Nearly every one of them died, and there was nothing we could do,’ he said. ‘We ran out of body bags’.”

While the direct effects of Covid are substantial in terms of lives affected and lives lost, it may be the indirect effects that have the more lasting and costly impact. While working in healthcare has never been easy, pandemic conditions have made it nearly impossible in many cases. As the article notes, “Health-care workers aren’t quitting because they can’t handle their jobs. They’re quitting because they can’t handle being unable to do their jobs.”

This raises a number of important issues. For one, the healthcare system, as expensive as it is relative to anywhere else in the world, does not have the resources or the policies to give healthcare workers a fair chance to do their jobs in too many cases. For another, compensation and work conditions are not at levels that encourage the supply of labor. There will continue to be shortages. Finally, as the nation ages and more elderly people require professional assistance, the supply of those workers is crashing too. There is a lot of work to do to get the healthcare system up to snuff or we are going to be experiencing major problems for a long time.

Economy

The above chart from themarketear.com on Dec 27 2021 shows the trend of fiscal spending over the next few years and breaks it out by major program. The main point is fiscal spending peaked in the second quarter of 2021 and will steadily decline for the next couple of years based on current programs.

As a result, there will be progressively less help from the government in boosting economic growth for coming quarters. While this clearly provides a headwind in relative terms, people are also getting back to work which at least partially offsets the decline in fiscal spending. The big thing to watch will be the degree to which recovering organic economic growth can offset expiring pandemic relief.

China

Is China Signaling Imminent Devaluation: PBOC Fixes Yuan Weaker Than Expected For Record 15th Consecutive Day

“On Friday, the PBOC set the daily reference rate at 6.3692 per dollar, weaker than the estimate 6.3688 with a surveyed range from 6.3676 to 6.3711. And, according to Bloomberg, at 15 days the stretch of higher-than-expected fixes is now at the record since Bloomberg released its median consensus forecast in June 2018.”

“The second shocking chart I want to flag up is the one below. We all know that the renminbi has been pari-passu against a robust US dollar, but the officially targeted trade-weighted renminbi is through the roof this year and stands at an equivalent Rmb6.00/$. At a time when Chinese credit conditions are too tight, this is simply intolerable.”

Since China manages its exchange rate very carefully, that rate does provide useful signals about the government’s intent. The recent period of greater than expected weakness in the renminbi suggests China may be trying to gradually release some pressure.

As much as anything, this serves as a reminder of the monstrous task China has to contend with. It is trying to restructure the massive real estate industry without breaking the financial system. At the same time it is trying to shift the economy away from real estate and towards more strategically useful industries. And finally, it is doing all of this while trying to keep the currency stable, but not so strong as to hurt export growth.

The important takeaways are 1) This is a massive undertaking that is extremely susceptible to glitches along the way, and 2) If things go south, there is always potential for a significant deflationary impulse to be unleashed across the globe.

Inflation

Has the pandemic shown inflation to be a fiscal phenomenon? ($)

“Central banks, not governments, are charged with hitting inflation targets. But does the experience of the pandemic show that inflation is really fiscal?”

“The logical extreme of this argument is known as the ‘fiscal theory of the price level’, created in the early 1990s (and in the process of being refreshed: John Cochrane of Stanford University has written a 637-page book on the subject). This says that the outstanding stock of government money and debt is a bit like the shares of a company. Its value—ie, how much it can buy—adjusts to reflect future fiscal policy. Should the government be insufficiently committed to running surpluses to repay its debts, the public will be like shareholders expecting a dilution. The result is inflation.”

Since the Fed began quantitative easing (QE) in response to the 2008 financial crisis, pundits have been warning of imminent inflation due to the increases in money supply. I had my concerns as well which is why I have found the work by John Cochrane so compelling. It is not the money printing per se that is the problem; it is the amount of money printing that funds deficit spending.

Cochrane’s analogy to dilution is helpful for understanding the concept. Essentially, the value of the dollar gets diluted by the amount of deficit spending the Fed prints money to cover. It is very similar to the value of stock getting diluted by the issuance of additional shares.

One point is that fiscal spending is an important element of the inflation equation; it is not just a monetary phenomenon. Another point is the quantity and duration of deficit spending that gets monetized are also important factors.

As a result, we have some tools by which to gauge the inflation potential of various policies. The one-time stimulus packages in response to the pandemic were large but mostly one-off programs. As a result, it is fair to expect a noticeable inflationary impulse, but not necessarily a permanent one.

This raises a bigger question, though. Because of the enormous size of the policy response to the pandemic, and because it was completely monetized, what will happen when the economy slows down the next time around? The signs are pretty good when that happens, fiscal spending will crank up again and the Fed will monetize the deficit again. If and when that happens, the realization of ongoing monetary “dilution” will increase - and inflation expectations will ramp up.

Investment landscape

This is another tweet thread by Jim Bianco who has been especially vigilant in following rates and interpreting their signals. While many market veterans agree that rates can provide useful information content, there is significant disagreement as to how clean the signals are (due to central bank intervention) and what messages can be properly inferred from the rates.

One of the bigger disagreements currently regards the message that the low long rate is sending. Does it mean inflation will ease and investors can therefore de-emphasize the inflation risk? Or does it mean something else? Bianco doesn’t mince words with his interpretation:

“10-yr signals the breaking point, not inflation. The yield curve is what matters, inversion means too far. The curve is very flat before the first hike, and the lowest ever mkt priced terminal rate (1.75%) Message, 4 or so hikes (to 1.75%-ish) should break something.”

So, this introduces a whole new set of possibilities. The Fed can raise rates, something in the financial system will break, but inflation will remain high. Since banks are much better capitalized than in the financial crisis, they are much less likely to be the problem. As such, the Fed would have little authority to assist with private sector deleveraging, especially with inflation still running high. Things could get very interesting.

Implications for investment strategy

Like many others, I have a regular practice of coming up with a list of resolutions at the end of the year. Unlike many others, this list is probably more akin to a strategic plan than it is a simple list.

While I like having a comprehensive plan to help shape many different facets of my life, I have also found it extremely difficult to make meaningful progress across several different fronts once I become immersed in the daily grind again after the holidays. As a result, I have started a practice of identifying the one or two or three things I can focus on during the year that will really have an impact.

This approach is also relevant to portfolio management. To that point, one thing that can really have an impact in the new year is to accept that markets are in the process of undergoing fundamental change. There will be no going back to normal. As a result, many of the heuristics and mental models and rules of the road that have been developed along the way are going to fail. In some cases they will fail hugely. Be curious, test out new ones, and prune old, ineffective ones.

Relatedly, another thing that can have an impact is to be more active in your approach to investing. By this I mainly mean be more flexible. Increase resources to risk management. Don’t treat any position or theory as sacrosanct. Continuously monitor the environment for signals. Generating returns from this point on is going to require a great deal more effort. Best be prepared.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.