Observations by David Robertson, 1/26/24

Stocks hit new highs while Treasury bonds moved in the opposite direction. Let’s figure out what’s going on.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The S&P 500 kept pressing higher this week as the narrative of continued low inflation and easing central banks dominated market sentiment. One way in which the ebullience is being manifested is in the IPO market. Almost Daily Grant’s (Tuesday, January 23, 2024) reports:

Let there be deals: “We have a robust pipeline” of initial public offering candidates spanning an array of sectors and geographic jurisdictions, New York Stock Exchange vice chair John Tuttle declared at a Reuters-hosted event in Davos last week. “It’s just [about] finding that time when investors have the appetite for these companies, and companies are ready to go,” he added.

While the restarting of the IPO machine is surely improving sentiment on Wall Street, technology is continuing to do its share as well. MSFT has continued to do its share of heavy lifting but NVDA has been the rocket shot.

While the AI narrative is certainly powering NVDA, apparently a lot of guff is also. A post on X by Dr_Gingerballs is eerily reminiscent of the tech bust in 2000. Weak semiconductor industry results and lots of less-than-arm length deals create a lot of warning signs for the stock.

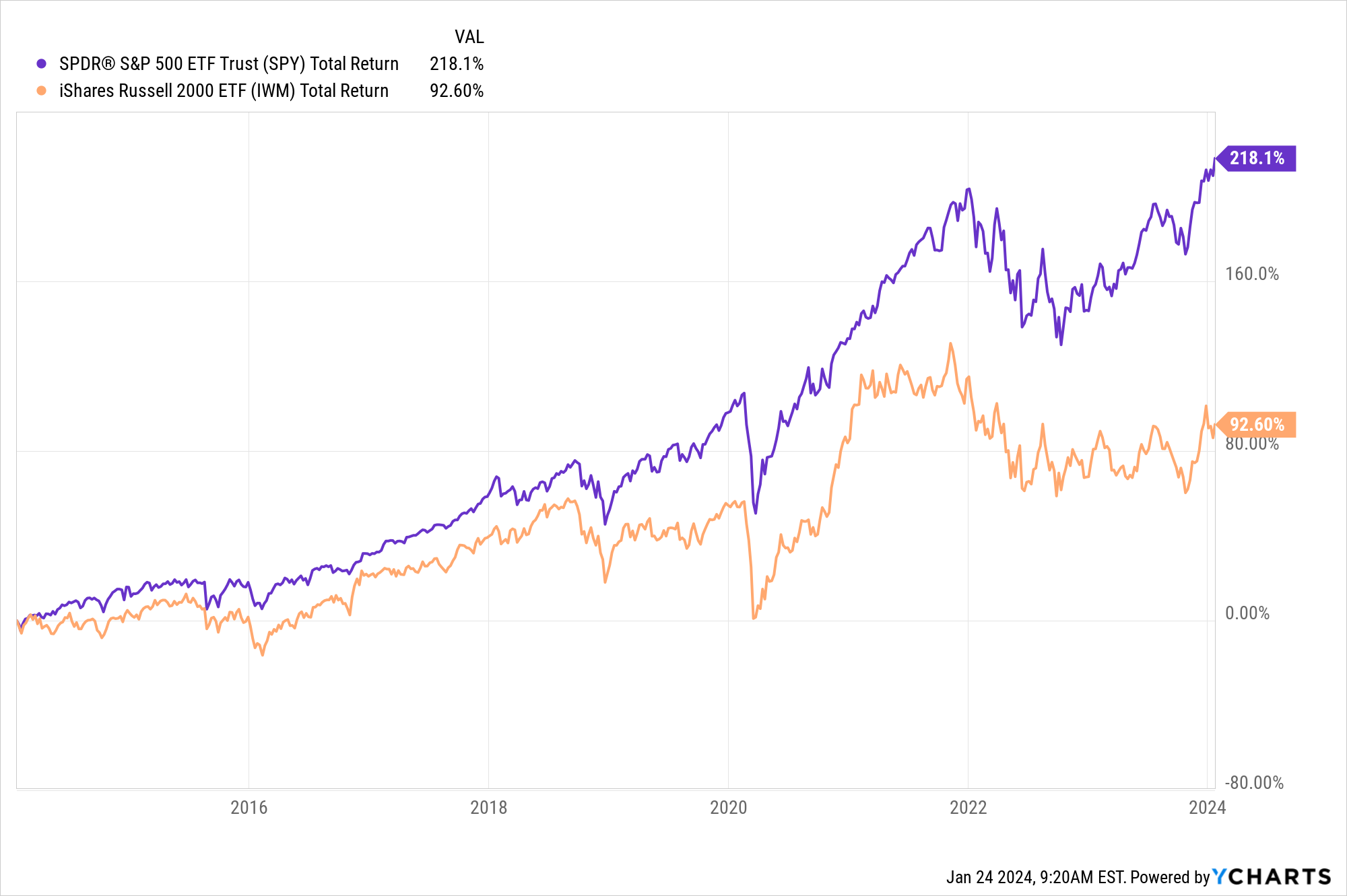

Another issue is the good overall performance of the S&P 500 belies significant divergences. Among other oddities, small caps have severely underperformed large caps. Further, while the underperformance over the past year was especially bad, it has persisted for over ten years!

This disparity is especially notable since small caps are generally riskier and therefore should command a higher return. Historically they have.

This suggests a couple of things. One is the potential for an epic reversal of fortunes by which small caps start outperforming large caps again. The other is that timing is key. After more than ten years, the divergence is still growing.

Housing

Home sales hit rock bottom last year — now, there are signs of a rebound

https://www.axios.com/2024/01/22/housing-market-home-sales-2024-statistics-data-report

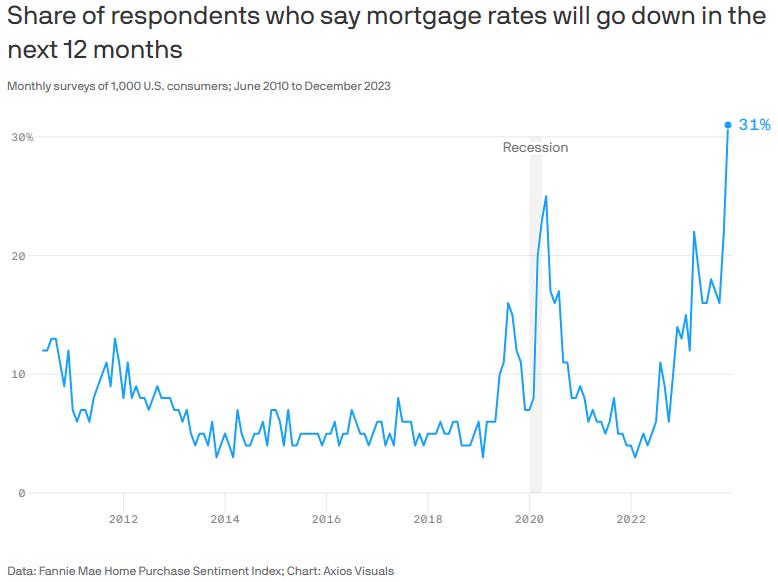

In a survey conducted by Fannie Mae last December, 31% of Americans said they expected mortgage rates to fall over the next 12 months, the highest share since the survey began in 2010 — and a clear sign of optimism about the housing market.

Just a few quick notes here. First, the combination of lower mortgage rates and the expectations of further declines is a positive sign for the housing market. One can almost hear the collective sign of relief. Further, since housing reaches very broadly into the economy, improvements here are likely to be felt elsewhere as well.

Second, sentiment on housing is often wrong, and often by quite a lot. After the GFC, I wrote an article on housing that quoted Robert Shiller in the FT:

“In a survey of home-buyers in four U.S. cities that Karl Case and I carried out in 2004, at the peak of the housing expectations, we found that the (trimmed) mean home price increase expected for the succeeding 10 years was 12.6 per cent a year. Maybe our respondents didn’t quite understand what they were implying: that would mean more than a tripling of home prices in the succeeding 10 years from an already high level.”

The main conclusion was the expectations of home-buyers were grossly exaggerated and defied all historical experience. They were just really, really wrong. It happens. The lesson for analysts is to understand it happens and to discount the information content of such surveys.

Third, there is a clear effort to propagate a narrative here. First, we are told the data represents a “clear sign of optimism”, just in case we couldn’t judge for ourselves.

In addition, the graphic used in the Axios story presents only the share of respondents who think rates will go down. The impression is that number is going to keep going up. However, this graphic was edited from the one actually presented in the Fannie Mae survey that is quoted. That survey presented the graphic below:

With the additional context, the respondents believing rates will go down looks more like reaching a historical peak that is likely to revert down. It seems pretty obvious Axios made a decision to selectively present the information graphically so as to support its narrative of “a clear sign of optimism”.

Credit

Almost Daily Grant’s, Monday, January 22, 2024

https://www.grantspub.com/resources/commentary.cfm

“The market is just on fire,” Richard Zogheb, head of global debt capital markets at Citi, marveled to the Financial Times today, referring to the breakneck recent pace of corporate financing activity. Investment grade firms have issued $153 billion worth of dollar-pay bonds so far in January thus far per data from the London Stock Exchange, easily the strongest such start to the year going back to 1990.

Positive sentiment is also on display in the credit markets. Lower Treasury rates and tighter spreads has created a sense of “smoke ‘em if you’ve got ‘em” for would-be debt issuers.

Part of the excitement is simply realizing the good fortune of being able to issue at rates quite a bit lower than just a few months ago. Part of it is an expression of relief that funding can actually get done.

Part of the excitement, however, is purely opportunistic. When sellers of something are super-excited, it’s usually a good time for buyers to increase their scrutiny. If sellers thought rates were going even lower and spreads were going to get even tighter, why wouldn’t they wait? I suspect issuers of debt see a much smaller window of opportunity than buyers expect.

China

Xi Jinping's 'forever purge' has China scared stiff($)

https://shannonbrandao.substack.com/p/xi-jinpings-forever-purge-has-china

“There's no end in sight” to Xi Jinping’s anti-corruption campaign that is “taking down scores of senior officials, bankers, hospital directors and even soccer administrators” in China, Wall Street Journal’s Chun Han Wong said last week.

“With echoes of Mao Zedong’s ‘continuous revolution,’ Xi has sent fear rippling through the ranks of the Communist Party for more than a decade with the largest campaign against corruption in modern Chinese history. It is now threatening to petrify the party as it tries to steer the world’s second-largest economy through its greatest period of uncertainty in a generation,” he wrote.

In December, Politico noted that “China's security services have ramped up repression to totalitarian levels,” as their “Stalin-like purge” swept the nation.

China has been in the news a lot for its tanking stock market. What has long been a magnet for speculative fervor has noticeably languished. While the much-touted re-opening bid that never came last year was unsettling, the recent leg lower has felt even more ominous.

One can chalk up the negative sentiment to a lot of things (I have certainly spent plenty of time describing the scale of the real estate problem), one of the least discussed factors is the political environment. As the Wall Street Journal reports, and Shannon Brandao picks up on though, China’s security services are implementing a “Stalin-like purge”. As a result, fear seems to be permeating the country.

This helps explain why Chinese stocks have been so moribund. While a new stimulus package announced this week may help soothe sentiment, it doesn’t solve any of the bigger problems. Fear can be a workable way to control a country, but it’s a lot less effective as a means by which to help a country grow.

Geopolitics

Eurasia Group’s Top Global Risks 2024

https://us12.campaign-archive.com/?e=5c7365da58&u=7404e6dcdc8018f49c82e941d&id=472f04cbac

1. The United States vs. itself

While America’s military and economy remain exceptionally strong, the US political system is more dysfunctional than any other advanced industrial democracy. In 2024, the problem will get much worse. The presidential election will deepen the country’s political division, testing American democracy to a degree the nation hasn’t experienced in 150 years and undermining US credibility internationally. With the outcome of the vote close to a coin toss (at least for now), the only certainty is damage to America’s social fabric, political institutions, and international standing.

It is often easy for Americans to survey the world with a sense of superiority. Having dominant military might, a diverse and robust economy, the rule of law, and the global reserve currency, among other advantages, makes life so much easier. As a result, it is also easy to assume geopolitical risks occur in the nether reaches.

This is what makes Ian Bremmer’s statement so striking. He makes a fair point that all of its advantages often conceal the reality that “the US political system is more dysfunctional than any other advanced industrial democracy”.

It is also a fair point that America’s leadership creates a virtuous feedback loop with its allies. Strength begets strength. Lose international standing and legitimacy and much of the ability to project power comes crumbling down.

All that said, I think Bremmer overstates the case a bit. I don’t share the same belief in certainty of damage to “America’s social fabric, political institutions, and international standing”. Sometimes you need a real test to show your mettle. However, I very much agree that meeting the challenge is no easy task and one that seems under-appreciated.

Inflation

Horizon Kinetics 3rd Quarter Commentary

https://horizonkinetics.com/app/uploads/Q3-Commentary-FINAL.pdf

• The current average interest rate on the Federal debt is 2.6%.

• The yield on Treasuries almost across the maturity spectrum is now 5% or so, meaning that as existing debt matures, the cost of borrowing will double.

This is typically thoughtful analysis of inflationary pressure from Horizon Kinetics. If you want to better understand the forces behind monetary debasement, this is an excellent place to start.

It is also a timely discussion because the potential for an explosion in federal outlays is no longer in the distant future but rather something that looks likely to happen in the next couple of years.

The main thing that could prevent a step function increase in outlays is rates coming down considerably between now and then. I suspect that is a big part of what the market is expecting. That can only really happen, however, if inflation stays extremely low … and I consider that extremely unlikely. As a result, there is a very tenuous basis for believing there is an easy way out of this. In short, the bill for excess spending is coming due.

Monetary policy

With Commercial Property, the Equity Goes First

https://www.theinstitutionalriskanalyst.com/post/the-equity-goes-first

“The Fed’s estimate today of the necessary quantity of reserves is probably about twice the level Chair Powell stated in 2018 would give him buyer’s regret. Why hasn’t the Committee changed their mind? One of the problems with the excessive reserve approach, as opposed to the necessary reserve approach, is that there is no binding upward limit on the size of the balance sheet. As a consequence, like the proverbial boiled frog, staff and leadership of the Fed may have become somewhat complacent about balance sheet size.

The main focus of Chris Whalen in this post is commercial real estate, but the insights are much more broadly applicable. For starters, the core of the problem is too much money. That’s it. That’s on the Fed and will be an ongoing issue.

Another important point is the Fed’s transition to an excess reserve framework. This has all been disguised behind technicalities and Fed-speak, but what it amounts to is the unleashing of accountability for maintaining an appropriate level of money supply. Much like elastic waistbands provide additional flexibility as one gets older, so too is the Fed giving itself extra room to maneuver by targeting a higher level of reserves. As Whalen explains, “there is no binding upward limit on the size of the balance sheet”.

As such, the Fed’s increased laxity in regard to its primary mission of controlling money supply is a signpost for higher future inflation. While this will surely be useful in minimizing risks as the quantity of bad debts piles up this year, it’s a bad sign for keeping inflation under control.

On a separate but related note, Joseph Wang recently posted his thoughts in regard to the Fed’s reaction function:

Fed officials are unlikely to meaningfully push back against the market's aggressive pricing of rate cuts regardless of the rise of risk assets. Real rates remain at cycle highs from declining inflation expectations even as recent inflation data is very close to 2%. Fed officials perceive financial conditions to be restrictive

In one sense, I think this is true and a useful insight into the Fed’s thinking from someone who worked there. In another sense, however, I don’t think this is the whole truth.

There are games being played on multiple levels here and monetary policy is only one of them. Politics is a big one. I think the most important objective of the Fed is to avoid blame. The Fed knows persistent fiscal deficits are inflationary but can’t do anything about that. So, it must appear to be fighting the good fight on inflation, but also be ready to ride to the rescue if things go sideways.

The Fed gets the biggest bang for its buck in this largely futile exercise by winking and nudging the market to do its work for it. In other words, I don’t think the Fed minds at all when the market (mis)interprets its comments as being especially dovish. If growth does slow down, it preserves policy space for reducing rates. If inflation picks up, it can be seen as maintaining a hawkish stance. It wins either way and avoids having to make tough decisions.

So, coming back to Wang’s comments, the story the Fed tells of maintaining restrictive financial conditions (based on real rates) is mainly a public relations message. It is not a good assessment of financial conditions (which are not restrictive) nor is it any especially useful indication of monetary policy stance.

Investment landscape

The Fed’s Monetary Handover

https://www.city-journal.org/article/the-feds-monetary-handover

By keeping bill issuance high, Treasury is able not only to counteract the QT performed by the Fed but also to force the Fed to taper QT. This is an abomination: monetary policy under the control of fiscal authorities … By severely shortening the maturity profile of its issuance, Treasury has provided significant monetary-fiscal easing in the past year, partially offsetting the central bank’s tightening cycle. Allowing Treasury to set monetary policy is extremely dangerous.

Stephen Miran’s point in this piece is straightforward: “This enormous expansion [in the Fed’s balance sheet] has erased much of the barrier between monetary and fiscal policy”. This is a point I have touched on several times, but Miran does a nice job of pulling several elements together into one narrative that helps provide perspective.

While statements like “QE resembles the monetization of government deficits” and “the choice to buy mortgage-backed bonds amounts to … an inherently political choice” may seem like so much monetary minutiae, they are also recognition of extremely important changes. Structurally, it has gotten a lot easier to facilitate inflation.

This hasn’t mattered a lot to markets yet, but that looks to change in the not-too-distant future. First, the Fed’s Reverse Repo Program (RRP) is looking to get depleted some time around the end of March. This is where the rubber hits road. After the RRP is depleted, money will have to come from other sources to fund the expected increases in Treasury debt issuance.

We’re starting to see warning signs, but not yet in stocks. The 10-year Treasury yield bottomed right at the end of last year. but has been rising ever since. Further, the auction of 5-year Treasuries on Wednesday was dismal. The bond market is not confirming the ebullience in the stock market.

Next week the Treasury issues its Quarterly Refunding Announcement (QRA) and that should provide some more information as to the volume of coupon issuance (i.e., supply of debt to be absorbed by the market). But it may not. Andy Constan listed “Seasonal budget deficit needs”, “New format for the release”, and the possible initiation of the buyback program as factors that could make interpretation of the release difficult.

So, there are three main takeaways. One, the Treasury market is looking wobbly and those are the rates on which the valuation of all other assets are based. Two, with lots of moving pieces, it’s probably going to be hard to determine much of anything with certainty. Three, the monetary machinery has been re-tuned to facilitate higher inflation.

Implications

The enormous importance of monetary support for financial assets the last several years has spawned something of a cottage industry in interpreting the words and actions of monetary authorities. This can involve the simple parsing of Fed press releases, but can also extend to more conspiratorial narratives about political and/or personal intent.

In a time of increased intervention, it is important to handicap the nature, degree, and timing of such interventions. However, there are also several risks to focusing too much on such hypothesizing. For one, the resultant narratives are volatile. There are massive swings back and forth. Good for astute traders, maybe, but also really easy to get whipsawed by. Relatedly, the narratives may or may not be true. We just don’t know. As a result, it hard to gain very much by spending too much time on such endeavors.

Finally, and importantly, those narratives and theories distract us from more important work. Sure, it’s important to consider the possibilities and to examine the situation from different perspectives. It’s another thing altogether to become consumed by the effort and lose track of all the little data points that in aggregate comprise the economy. Since we’re in the middle of earnings seasons, it’s a good time to dig in and see where the bottoms-up views do and do not match up with the top-down views.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.