Observations by David Robertson, 1/31/25

Another week and another flood of news to assimilate. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Monday was greeted with a sharp selloff as the implications of the DeepSeek artificial intelligence (AI) model became more widely appreciated. Semiconductor stocks got hit hard, but the hardest hit were derivative plays. For example, Vistra, an electric power company, was down 28% and Fluor, an engineering and construction company, was down 15%. Big Tech had a relief rally later in the day on Monday and into Tuesday, but Nvidia stayed on its back.

The Federal Open Market Committee (FOMC) meeting this week took on a much quieter tone than it has in the past. Rates were left unchanged, the language of the press release was little changed, and little came out of the Q&A session. The two biggest highlights were a clear effort to completely avoid any political question and a clear statement regarding the continuation of Quantitative Tightening (QT). Those hoping for some body language signaling future rate cuts were disappointed.

Rate cuts did come from the European Central Bank (ECB) and the Bank of Canada BOC). This puts major central banks on different trajectories. If the ECB continues to cut rates and the Fed continues to hold, European stocks are going to start looking more interesting.

The next big event for monetary policy watchers will be the Treasury Borrowing Advisory Committee (TBAC) report next week which will detail plans for Treasury issuance.

Economy

At this stage it appears as if the economy is continuing to cruise along on the tails of Biden administration spending, however, it is also easy to see indications momentum is slowing. Unemployment has ticked up. It’s still not bad, but it’s sure not getting better either. Liquidity is tightening up which serves to constrain economic activity. Finally, the Trump administration’s cuts to various federal programs is likely to cause a lot of households to reconsider their spending plans. These things can take time to show up in economic statistics, but they do.

One number where it looks like a slowdown may be starting to show up is civilian employment. John Hussman pointed this out in December:

Even here, it’s notable that nearly nobody has picked up on the deterioration in civilian employment growth, which has already gone negative on a year-over-year basis. Civilian employment is part of the “household survey” that determines the unemployment rate, as opposed to the “establishment survey” that provides the headline month-to-month “non-farm payroll” figure. Given our emphasis on signal extraction and noise reduction, our preference is always to extract the common signal from a very broad range of independent or partially correlated sensors. In my view, we would still need more evidence to expect a recession with confidence, but we certainly shouldn’t rule out that outcome even in response to the possibly sizeable disruptions that may be just ahead.

At the same time as economic momentum seems to be slowing, the narrative about economic growth keeps taking hits. Prospects for significant job cuts in federal government, significant increases in tariffs, and delays and “confusion” regarding payments in government programs all contribute to a degradation in the narrative about growth.

Mainly, the economy’s path seems like a bike after flying down a hill and starting up another one. You’re still moving pretty fast, but you know you’re going to start feeling additional resistance any time and are going to need to start pedaling — or stall out. Don’t be surprised if economic narratives start taking on a more somber tone in the near future.

Housing

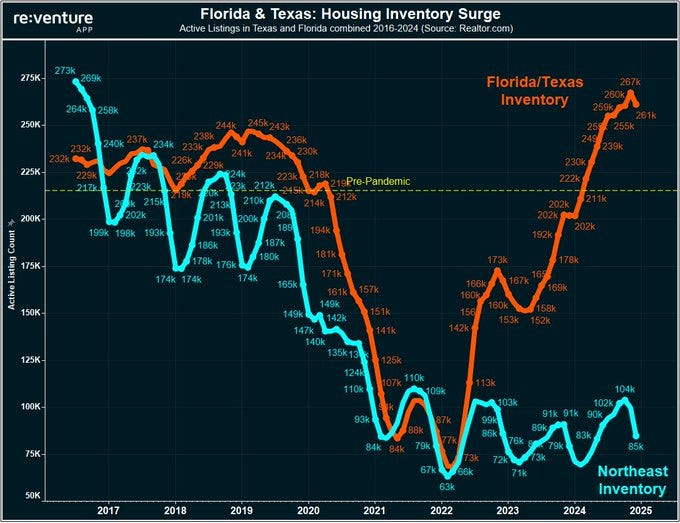

We haven’t been hearing a lot on housing lately — which makes this post from Nick Gerli all the more helpful:

Probably my favorite housing market graph right now. Orange line is inventory levels in Florida & Texas, combined. Blue line is inventory level across entire Northeast US. In Texas and Florida, there are 261,000 active listings on the market. 207% higher than the level in Northeast, which covers 9 states. Prior to pandemic, these regions were the same. Highlights the very bifurcated nature of this housing market. The downturn is happening in TX/FL, but we are still suffering a historic inventory shortage in the Northeast.

The first point is that Florida and Texas are big real estate markets and inventory in those states is surging. This matters because inventory is a key determinant of price: Higher inventory means lower prices. It also matters because so many transactions occur in Florida and Texas that prices established there are likely to spill over into other parts of the country.

Since the key differential here is inventory, this is not like the systemic risk that manifested in the financial crisis of 2008. Rather, the process of establishing more reasonable house prices for prospective buyers in some areas should ultimately be healthy for normalizing the housing market to higher mortgage rates.

That said, the process is unlikely to be pain-free as lower home prices mean lower collateral values and that will certainly affect regional lenders.

Politics and public policy

A little tiff flared up over the weekend on which the New York Times reported: “Colombia refused to accept U.S. military planes deporting immigrants, setting off a furious reaction from President Trump, who on Sunday announced a barrage of tariffs and sanctions targeting the country."

Michael Pettis describes how the reaction actually undermines US interests:

But if Washington's primary goal is to reduce the trade deficit in a way that revives US manufacturing, reduces US debt, and raises wages for US workers, threatening tariffs against countries like Colombia is self-defeating.

Colombia is a deficit country, and as such not only does it not play a role in worsening global trade imbalances and savings excesses, but it actually helps relieve them by absorbing excess savings from elsewhere.

This issue is a good microcosm of Trump-world. In part, it leaves everyone trying to figure out what in the world he is trying to accomplish. In part, the lack of an apparent strategy leaves investors wondering how to handicap the investment environment. What does it mean?

A good starting point is to recall Steve Bannon’s operational mantra: “Flood the zone with sh*t”. There are two key points to this. First, the theory is based on the assumption that “The real opposition is the media.” In other words, because media has vast power to influence voters, and because media has a liberal bias, media is the real political opponent.

Second, you don’t win against an unfair system by competing within it, you win by changing the game: “As Jonathan Rauch once said, citing Bannon’s infamous quote, ‘This is not about persuasion: This is about disorientation’.” So, you don’t try to present arguments, you try to undermine any reason for consuming media.

Well it’s not hard to understand where there is common ground between Trump and Bannon. Trump has no patience or heart for boring things like discipline or strategy. But he does have a penchant for making grandiose statements on a frequent basis.

This tendency serves him personally and also politically. A person who takes action on a great number of issues establishes at least the appearance of leadership to a broad constituency of voters. This phenomenon is probably amplified by the contrast to Biden who was a less than charismatic president through most of his tenure.

This all provides useful context from which to assess the new president’s actions. For example, in most cases it is probably safe to start with the assumption that any given action has more to do with a general plan to “Flood the zone” and to instill “disorientation”, than any thing else. Remember, from Trump’s perspective, media is the enemy — and that’s where most of us get our news from.

Relatedly, there are good reasons to believe such actions have little or nothing to do with cohesive policy direction. Sure, a number of policy ideas have been laid out, but that only matters in a game of governance. This is a game of politics.

Is it possible some good policy measures will emerge. Absolutely. There are competent people in the new administration that will almost certainly be working to that end. Hopefully, a number of them will make it.

The chances are not great, however. In Bannon’s strategy of taking down the media, the goal is disorientation. Not good policymaking. Not fulfilling voters’ wishes. Not serving the American people. It’s about disorientation. Keeping that in mind should at least provide some guidance in this otherwise tumultuous investment landscape.

Technology

On Monday, artificial intelligence (AI) related stocks got hit because of an increasing realization the Chinese DeepSeek model could operate at a comparable level but far more cheaply. Initially this sent a shockwave of panic through the space.

Robert Armstrong ($) at the FT wrote a good overview on Tuesday. He highlighted:

This puts three punctures in the winner-take-all theory of AI. It deflates the idea that the best AI results could only be achieved with Nvidia’s best chips and software; the idea that only the biggest tech companies could afford to build and run high-quality AI models; and the idea that only companies with their own AI models could offer great AI applications.

By Tuesday, AI narratives were already evolving to a gentler interpretation. Rather than imposing an existential threat, the DeepSeek development was portrayed as being representative of a natural path of technological progress. The jury is out on that one, but for now it buys companies some time to adapt to the new reality.

One thing the DeepSeek introduction clearly changed was to significantly impair the narrative for debt-based investment in the space. While the Big Tech companies mainly enjoy strong cash flows, other businesses in the AI ecosystem do not.

For instance, Grant’s Interest Rate Observer (January 31, 2025) judges “that the coming bust will not only take down data-center companies, but also reverberate across the data-center supply chain and throughout the credit markets.” Hot on the trail of other potential problem credits, Grant’s also reports, “The Financial Times sounded the alarm in November over the emergence of this ‘new asset class’ of debt facilities (about $11 billion total) collateralized by Nvidia GPUs.”

This all has echoes of the late 1990s when debt was used to finance the build out of infrastructure to support the rapid development of the internet. Unfortunately, the revenue forecasts ended up being a lot more uncertain than the debt payments.

For the time being, DeepSeek is just one small chink in the narrative armor of AI. It may be an indication of more to come though.

Investment landscape I

‘Leveraged to the hilt’: PE-backed firms hit by wave of bankruptcies ($)

https://www.ft.com/content/e83e9bd0-399f-4b46-a980-c9b73f8eb59b

Higher interest rates and lower consumer spending are squeezing debt laden companies backed by private equity groups, forcing them either to restructure through bankruptcy or buy time to recover via out-of-court settlements with creditors.

The stress on private equity-backed companies shows up starkest in a recent study by S&P Global Market Intelligence, which shows that a record number of 110 private equity and venture capital-backed companies filed for bankruptcy in 2024.

A few interesting insights emerge from this seemingly innocuous little piece of reporting. First, despite what private equity (PE) and venture capital (VC) firms are saying, many of their companies are sucking wind:

But PE and VC-backed companies have been particularly hard hit, with portfolio companies comprising a rising — and record — share of corporate bankruptcies, according to S&P data.

This shouldn’t be too surprising in a higher rate environment given that “Everything is leveraged to the hilt.” A huge number deals were done under the assumption that rates would quickly revert back to extraordinarily low levels. That is not happening.

In fact, the pain is probably being understated. For instance, “the out-of-court tactics [have been] suppressing the number of private equity-related bankruptcies in recent years.” Otherwise, bankruptcies would be even higher than stated.

This creates an interesting dilemma for investors and central bankers. While a rapidly increasing number of bankruptcies creates a clear signal of financial distress and upcoming economic weakness, much of that signal is coming from exactly the kinds of companies that recklessly endangered their balance sheets and should suffer the consequences.

It will be very interesting to monitor the Fed’s reaction function. Will it be more sensitive to the squeals to lower rates (from overly indebted companies and their PE and VC sponsors) or to protecting consumers against inflationary pressures? We’ll just have to wait and see.

Investment landscape II

Japanese investors dump Eurozone bonds at fastest pace in a decade ($)

https://www.ft.com/content/7f6b6ed7-7c55-4a41-a068-67131922363c

The prospect of higher bond yields at home and political upheaval in Europe — including the collapse of the ruling coalition in Germany leading to elections next month, and turmoil in France, which has been operating under an emergency budget law — have accelerated the sales, analysts say. French bonds were the most sold during the period, at €26bn.

Japanese investors returning home is a “game changer for Japan and global markets”, said Alain Bokobza, head of global asset allocation at Société Générale.

But, as Japanese investors start to search for returns at home, their net buying of global debt securities has shrunk to just $15bn in total over the past five years — a far cry from the roughly $500bn in such purchases they made in the previous five years, according to calculations by Alex Etra, a macro strategist at Exane.

I have talked about Japan before and the potential for it to start repatriating excess savings from other countries. This story in the FT confirms this is starting to happen and it is starting in the EU.

Interestingly, this also helps explain why bond yields have been rising across the globe despite different economic conditions and inflationary threats.

Finally, by virtue of appearing in the FT, the narrative is starting to get traction. As Japan continues to bring money home, and as that narrative builds, there will continue to be pressure on bond yields from major debt issuers across the world. Things are not likely to get any easier.

Implications

Market action on Monday was interesting and may reveal some insights about how the future unfolds.

For starters, there was a great deal of rotation. Money flowed from AI stocks into other sectors and from large caps into small cap stocks. That does not suggest any fundamental reassessment of stocks, but rather a tactical redistribution within the asset class.

Fred Hickey posted his thoughts at the time:

An important lesson I learned during the 2000-2002 tech bubble's bust: the bubbleheads are loathe to give up, so they "rotate" (see Apple today - up over $8 - yeeha -such a bargain for no growth, 38+ P/E, 10x sales & $3.5T mkt. cap!) and they continue to buy... all...the...way...down.

Bob Elliott also posted with his thoughts:

BTFD is a tough habit to break after 15yrs of success. The eventual shift away from it will create air pockets of demand many have never seen in their careers.

As a result, the rebound on Tuesday suggested at least two different interpretations of market action. Alyosha ($) presented a third in his Substack:

Shortly after the opening [on Tuesday, 1/28/25], algos started buying the Dow, S&P, and NDX futures indexes, rallying each 1.5% in an hour. All three programs paused at 10:10 AM and recommenced at 10:50.

These were sophisticated algos (I have written algos, so I am speaking from experience) that never allowed prices to decline below a rising benchmark. These execution algos can see the book of liquidity and calculate order size to both match and marginally exceed present liquidity, including any incoming orders, regardless of size, and adjust order entry accordingly. The objective is not to get the best price. It is to raise the price without allowing sellers the benefit of responsive selling into a price void. And there are algos out there written to do exactly that. Remember, we are in the age of AI.

He concludes, “Someone or a group wanted stocks higher today [Tuesday].”

So, Tuesday’s rebound could be considered as extreme enthusiasm for stocks in general, mindless buy-the-dip behavior, or a coordinated effort to prevent excessive market losses.

As it turns out, each implies virtually the same type of outcome for stocks over the medium term: A fairly long process of normalization involving successive declines succeeded by only partial recoveries, i.e., a downward ratcheting pattern. Don’t say you weren’t warned.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.