Observations by David Robertson, 2/9/24

Another heavy week of earnings, more news on rates, and an ever-buoyant stock market. Let’s take a look at what’s been going on.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Stocks continued to run up most of the week but the good news was not shared by bonds. The 10-year Treasury yield spiked higher on Monday after Jerome Powell’s appearance on 60 Minutes, fell back on Tuesday after a good auction of 3-year Treasuries, but then continued rising through the week. While yields have not shot up, they don’t look like they want to go down either.

Year-to-date the US dollar (USD) has moved higher, albeit in spurts. Interestingly, stocks have remained fairly immune from the stronger USD as well.

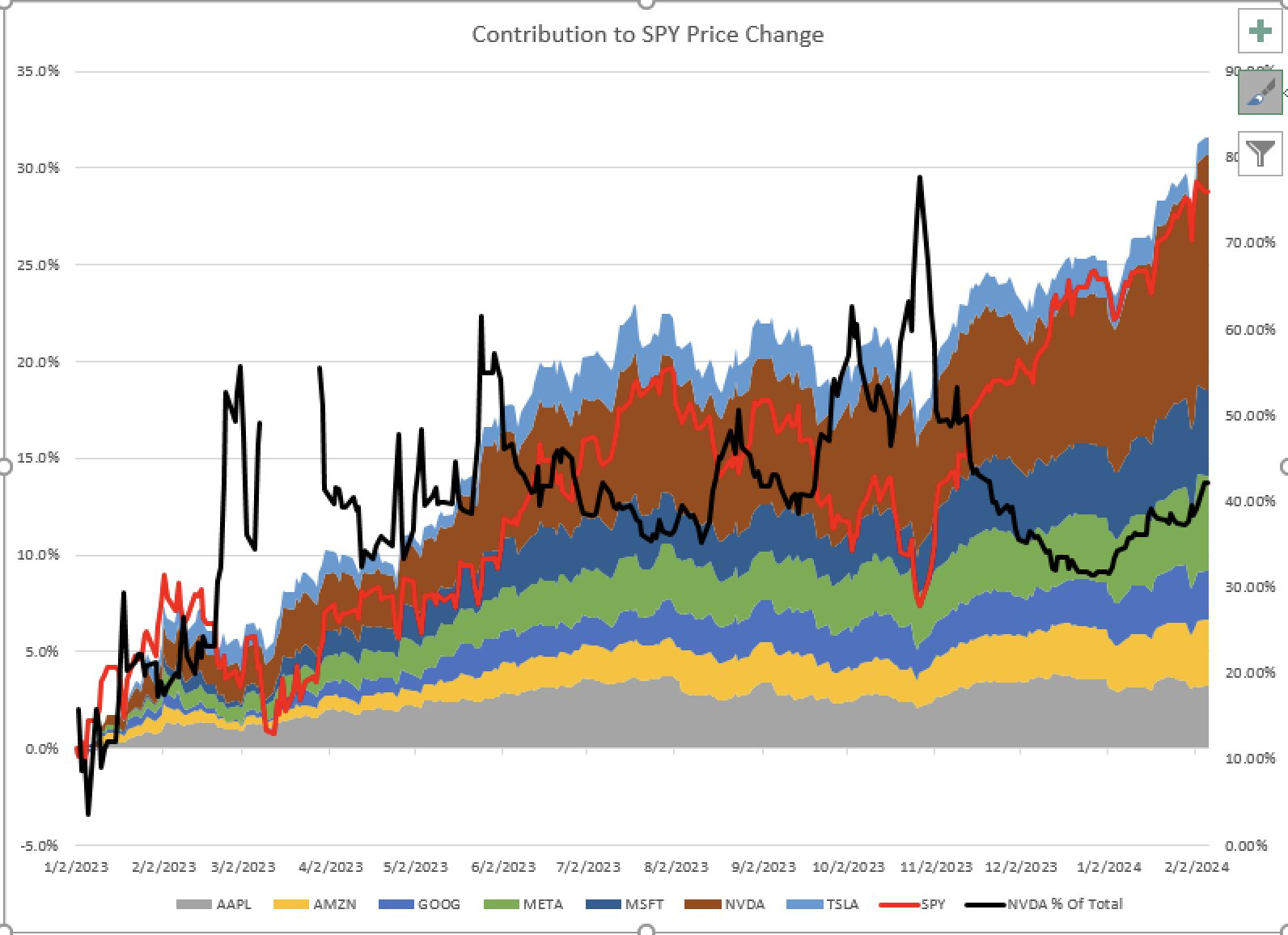

Andy Constan singled out the key driver of the S&P 500 for the last year: “Lately its been all $NVDA 42% of the Return of the Equity Market Benchmark for a year is one stock.”

Supreme Bagholder points out why such performance may not be sustainable: “$NVDA's top 4 customers account for 40% of revenues, and every one of them is actively working on their own custom AI silicon”. It’s always fun until someone gets an eye poked out.

Cluster of Woe

https://www.hussmanfunds.com/comment/mc240204/

we estimate that current market conditions now “cluster” among the worst 0.1% instances in history – more similar to major market peaks and dissimilar to major market lows than 99.9% of all post-war periods.

I call this the “Cluster of Woe” because the handful of similarly extreme instances (most notably in 1972, 1987, 1998, 2000, 2018, 2020, and 2022) were typically followed by abrupt market losses of 10%-30% over the next 6-10 weeks (average -12.5%), with losses at the smaller end of that range often seeing deeper follow-through later.

Some good perspective from John Hussman here. Sure, it’s frustrating to watch stocks go up when you’re sitting in cash or bonds. It’s a lot less frustrating when you realize what is at stake.

Credit

More on the corporate credit boom ($)

https://www.ft.com/content/97d9ad34-7446-448f-aea6-d5810b2c8510

At current valuations, though, Rosenberg prefers HY to IG for two reasons. The first is that while HY spreads may be tight relative to history, HY still gives you a meaningful step up in absolute returns versus Treasuries.

When I look at the difference between IG and high yield today, the reality is you’re picking up 200-250 basis points of yield. You’re picking up risk, but you’re getting paid for it. In IG today, you need rates to go down for that trade to work. Eventually they’ll come down, but I’m not sure it’ll be as quick as the market expects. In high yield, I don’t need rates to come down because the coupon is so much higher.

Rosenberg’s second point in favour of HY is quality. As we’ve discussed before, the HY bond universe has seen a big improvement in the composition of credit ratings.

Some good points are made in this FT Unhedged piece on high yield (HY). I tend to cringe myself when I look at historically low spreads for HY and consider the potential for the economy to slow down. However, it is also true the alternatives are not any better. Yields on Treasuries and Investment Grade (IG) debt are too low to provide attractive returns on their own; one must also make a directional bet that rates will come down. Stocks are at record high valuations. HY doesn’t look so bad in comparison.

Of course, all this is predicated on the assumption that historically low credit spreads are not a big risk. With New York Community Bank (NYCB) getting pounded due to commercial real estate (CRE) and a few other foreign banks starting to get hit as well, it’s becoming increasingly clear the CRE problem isn’t going away. In fact, it looks like CRE problems are really just beginning to emerge as tangible costs. Further, the downgrade of NYCB by Moody’s this week indicates we are probably in the early innings of credit adjustments. So, there are clearly risks to credit spreads. Ain’t nothing easy.

China

Why everyone in Shanghai is miserable ($)

As our leader explains, investors abroad and at home have lost faith in China’s policymakers, as the dismal performance of the stockmarket demonstrates. It tumbled throughout January. The Shanghai Composite, an important index, hit a five-year low on February 5th, which seems to have finally alerted China’s leaders to the problem. State investors have started buying up shares in order to stop the drop. These state funds might help stabilise China’s stockmarket. They cannot solve the deep problems that are draining peoples’ spirits.

This snippet from the Economist reveals the essence of many of China’s challenges. One of those challenges is the “lost faith in China’s policymakers”. When a system is highly dependent on policy intervention to work, faith in that intervention is critical. Lose the faith and the intervention loses its effectiveness.

Another element of the gloom is lost wealth. In a country in which “80% of household wealth is stored in real estate”, the real estate downturn has hit especially hard. Further, “The people that became successful during China’s boom years feel especially bad right now. They are watching their hard-earned wealth evaporate.”

Finally, despair has set in as “The government has not yet stepped in with a viable remedy for any of these problems.” There hasn’t yet been a viable remedy because there is no easy remedy. Interventions in the past merely extended the fantasy of rising wealth; they didn’t solve any underlying problems.

Now, time has run out and it isn’t pretty. It’s going to be a long, hard slog to right China’s economy. It can, however, serve as a warning for investors in the West. The issues are actually quite similar. Intractable economic challenges were papered over by artificially inflated asset markets. Until they couldn’t be any longer. These same challenges are coming to the US and Europe as well; it’s just going to take a while longer.

Monetary policy

What the Treasury said in the widely referenced policy statement for the Quarterly Refunding that helped ease the concern about increasing coupon issuance:

Treasury does not anticipate needing to make any further increases in nominal coupon or FRN auction sizes, beyond those being announced today, for at least the next several quarters.

What Treasury presented to the Treasury Borrowing Advisory Committee (emphasis added):

Uncertainty regarding funding needs in FY2024 to FY2026 remains relatively high, reflecting a variety of views on the path of monetary policy, the duration of SOMA redemptions, and the outlook for the economy.

several dealers suggested that additional coupon increases may be needed sometime in 2025 due to higher deficits.

Dealers generally suggested that risks for higher deficits were asymmetric to the upside, noting the potential for lagged effects on economic growth given the Fed’s efforts to tighten financial conditions over the last 21 months, the path of future monetary policy (including balance sheet normalization), and fiscal policy post the November elections.

Bottom line: headlines are used to manage the narrative; underlying details are used to cover your butt.

Investment landscape I

One of the most prominent drivers of financial assets has been liquidity. Interestingly, however, Patrick Saner recently posted a BNP table showing “that JPY liquidity is the more important driver of S&P 500 returns than USD liquidity.”

He follows with: “Even if you take the above analysis with a grain of salt, the BoJ remains the global low yield anchor and liquidity provider. As such, one should consider the global implications rather than focusing on Japanese yields (or the Yen) alone.”

Fair point and an interesting prospect. What if, for all the attention placed on US liquidity, it has really been Japanese liquidity that has been driving the financial asset train? There have been plenty of overlaps with US liquidity which would make it hard to single out. It could also explain some unusual market behavior.

As the election cycle in the US heats up, and as Treasury rates bounce all over the place, it will be easy to fixate on US markets. I think Saner is right to provide a heads up on Japan, though. It could be the butterfly that causes the hurricane if and when the BOJ starts tightening monetary policy.

Investment landscape II

Dick Bove: ‘Research is dead’ ($)

https://www.ft.com/content/992c19f6-5df6-41fa-b535-8c2aad1873f3

That [corporate finance departments were using analysts to bring in corporate finance business] worked until 2002 when the guy from Merrill Lynch whose name I forget [Henry Blodget] publicly stated that this company was no good while having a strong buy recommendation on it. That scandal resulted in a whole set of rules being created. And now you’re back to the same problem. We don’t need the analysts for research. We can’t use them for corporate finance. What the hell are we going to do with these guys? You had a swing in where the profit centre was in the brokerage industry, towards trade execution. The traders became kings, and rightly so, because they are executing the sale. So you figured out how to use the analysts: to support the trading activities of the firm. You’ve gone from the analyst being at the very highest rank in the industry to being at the lowest rung in the industry, because nobody thinks you need them. A lot of guys do really phenomenal work for many hours, and nobody gives a damn about what they write.

For those unfamiliar with Dick Bove, he was one of the really great equity analysts and one of the exceptionally few who managed an entire career in the business. As a result, his reflections are instructive.

For one, he observes that equity analysts used to be at the very top of the financial hierarchy but have since fallen to the bottom. This echoes what I have seen as well. As the economy has become increasingly financialized, and the financial business has become increasingly focused on trading as the profit center, the importance of analysts has faded considerably. Mainly, that role has changed from one of uncovering value in investment opportunities to one of justifying compelling narratives for trading opportunities.

This transformation manifested in different ways over the years. Back when today’s Big Tech companies were internet companies, the change became evident in “research” reports that were almost completely devoid of numbers. More recently, the Harvard Business Review ($) published an article highlighting the challenges of capturing the reality of digital businesses with traditional accounting standards. Unfortunately, many of the “challenges” were really just thinly disguised disdain for financial reporting:

Sadly, accounting is no longer considered a value-added function.

This is an outcome of the growing divergence between what companies consider as value-creating metrics and those reported as profits in the GAAP. Many CFOs consider financial reporting to be an exercise in mere regulatory compliance and find the resources spent on audits and financial reporting to be a waste of shareholder money. They consider the calculation of GAAP-based profitability to be more of a hinderance and distraction to their internal resource allocation decisions. One CFO commented that they now avoid inviting company accountants to their strategy meetings, while another said that CPA certification is considered a disqualification for a top finance position.

Apparently it’s just oh so pedestrian for fast growing tech companies to trifle with financial accountability (sarcasm).

Bove concludes his interview with the ominous declaration, “Research is dead as a driving factor in the market.” I feel his pain and agree in many respects. Where I may disagree is with the notion that research is dead forever. Eventually, lack of accountability leads to inefficiency and eventually scarcity forces either better efficiency or greater inequality. As a result, I very much expect research to become important again. The only question is how long that will take.

Asset allocation

The graph below from @SoberLook is probably a pretty good representation of what investors are doing to hedge against inflation. It is also highlights a mistake that a lot of investors are probably making.

That mistake is to simplistically assume stocks serve as a good inflation hedge. Yes, stocks have helped protect against inflation in the past. No, there is no pre-ordained rule that ensures stocks protect against all kinds of inflation all the time.

One key factor is pricing power. Stocks work well as inflation hedges when businesses have the ability to raise prices at, or faster than, the rate at which costs go up. Obviously, certain stocks and certain industries are going to be more successful at this than others. The mix of such businesses will determine the degree to which overall stock indexes are good inflation hedges or not.

Another key factor is valuation. If stocks are undervalued when inflation hits, there is a better chance they will perform well through a period of inflation too. Conversely, if stocks are overvalued when inflation hits, lower multiples can more than offset any benefits from pricing power.

The analysis is further complicated by the increasing roles of narratives and passive investing. If the Common Knowledge is that stocks are good inflation hedges, then stocks may actually serve as good inflation hedges until that Common Knowledge changes regardless of their fundamental merit. The challenge for long-term investors is that Common Knowledge can be a strong force driving returns, but it can also change suddenly.

Portfolio strategy

Amidst all the enthusiasm for stocks, the total return of stocks since the end of 2021 (and through Tuesday 2/6/24) has almost exactly equaled the total return of cash (in the form of short-term Treasury bills). So, to some extent, your choice has resulted in going on a wild ride - down and then up - or not. While this episode doesn’t prove anything about the future, it certainly highlights what is possible, i.e., that stocks just aren’t very helpful to a portfolio at current valuations.

This period is relevant because I think the end of 2021 marked an important change. That was when the Fed was forced to admit inflation was too high and too persistent to ignore. It was also about the same time the Biden administration re-oriented economic policy and diplomatic efforts away from a low interest rate regime.

This is important. On one hand, the heightened threat of inflation significantly constrains what the Fed can do. On the other hand, the change in public policy was an admission of both the futility of running low interest rates for much longer and the national security threat of trying to do so. In short, I believe the end of 2021 basically marked the end of the Fed put, at least insofar as that put was designed to cushion any little fall in the market. Regardless of whether one believes this or not, however, the loss of the Fed put remains a possibility that looms much larger than it did five years ago.

As a result, long-term investors are faced with a couple of difficult choices. On one hand, market narratives are powerful. If you aren’t there you are falling behind. On the other hand, if the chart above is any kind of indication of the intermediate future, why would anyone but short-term traders want to be in stocks? All that bouncing around, all those ups and downs, and all you get is the same return as cash.

Implications

As I have discussed many times, one of the bigger challenges for investors has been accounting for significantly increased intervention into markets. The Fed put was fairly easy to figure out because it was one dimensional and it came from the Fed.

Intervention now is much more varied and multi-faceted. It comes from the Fed, Treasury, fiscal spending through different agencies, and more. Often it comes with the intent of boosting markets, but not always.

I think this is increasingly going to be an important area to track. Elevated markets are desirable from a policy standpoint because higher asset prices means higher capital gains taxes and higher wealth effect spending. That favors capital.

Rebuilding the economy requires adequate wages and working conditions, though. Further, the political pendulum swung so far in favor of capital the last few decades that it finally seems to be swinging back in favor of labor.

This creates an interesting balancing act for this administration - and the next one. How will the political and economic tensions of labor vs. capital be managed? It’s hard to say and I’m sure it will change according to prevailing conditions. What does seem fairly clear though, is favoring capital over labor too enthusiastically in an election year would be political suicide. As a result, I think a good baseline expectation is for greater emphasis on progress in the economy rather than rising stock prices.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.