Observations by David Robertson, 3/15/24

It was another busy week so let’s jump right in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

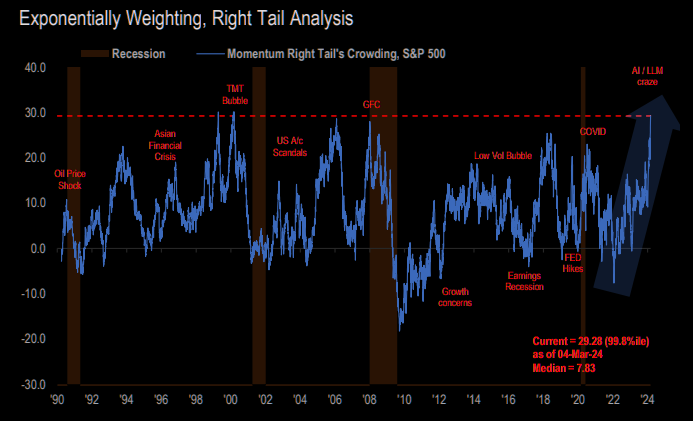

Momentum continues to rule the day. Themarketear.com ($) reports (per JPM), “Our non-linear crowding estimate of Momentum is flashing red at 99.8%ile with the fastest increase ever in the past month". Hard to get much higher than that.

Almost Daily Grant’s, Friday, March 8, 2024

https://www.grantspub.com/resources/commentary.cfm

From the bulging financial innovation files: Roundhill Investments announced the launch of its S&P 500 and Nasdaq 100 0DTE Covered Call Strategy exchange traded funds yesterday (tickers XDTE and QDTE, respectively). The products, which debuted today, target 100% overnight exposure to those benchmark indices while selling out of the money 0DTE calls each day to generate income while participating in any intraday upside to the given strike price.

One prominent former watchdog, likewise, takes a grim view of the 0DTE apparatus. Jay Clayton, Trump-era SEC chairman turned lead independent director at Apollo (as well as an advisor to crypto v.c. firm Electric Capital and digital asset custodian Fireblocks), described the products as “gambling” at a Wall Street Journal-hosted conference Wednesday, responding in the negative when asked if they should be permitted by regulators.

One trend is clear: The creation of financial vehicles that represent “gambling” (as opposed to representing shares of entities that create economic value) continues apace. Btw, PauloMacro ($) refers to 0DTE ETFs as “Max Stupid”. Well put.

Consumer prices came in a little hotter than expected on Tuesday but markets took the news right in stride. When producer prices came in hotter on Thursday, however, it seemed to strike a nerve. Not only did the hot print deviate from two consecutive benign reports, but it also sported a big increase in prices for final demand goods which had been quiescent.

S&P 500 futures turned tail from positive to negative on the report and the 10-year Treasury yield popped over 10 basis points. Apparently there are limits to how much the market is willing to be deluded about inflation.

Economy

Almost Daily Grant’s (Monday March 11, 2024) reported “Friday’s jobs print for February provided fodder for bull and bear alike”. True enough. The same sentiment was conveyed by Liz Ann Sonders:

“It’s got literally a data point for every view on the spectrum,” Liz Ann Sonders, chief investment strategist at Charles Schwab, commented to CNBC. “[Whether] the economy is plunging into a recession to Goldilocks, everything is fine, nothing to see here. It’s certainly mixed.”

For starters, I think these characterizations of economic data points being “mixed” are spot on. In addition, the mixed data provide “fodder for bull and bear alike”. In other words, the data is mixed enough to support just about any narrative you want.

I see this as a growing risk for financial assets. The mixed data make it hard to refute any given narrative definitively. As a result, rather than carefully weighing the data and allowing outlooks to evolve, large clusters of investors seem to be choosing “teams” and locking on to specific narratives.

This creates the potential for a significant deviations between market prices and underlying economic reality - and I believe that is happening now. Both inflation and long rates are going to be higher than the market is currently pricing. When this gets realized, it will cause quite a shock.

Japan

The BOJ "Has Made Up Its Mind To Hike Rates" After Union Wage Negotiations Lead To Surge In Pay

After a decade of NIRP and unlimited bond buying to keep the Japanese bond market - and economy - from disintegrating, the BOJ may have no choice but to hike rates as soon as next week. The reason: inflation in "deflationary" Japan is now not only on par with the US, but wage growth is surging and threatening to spark a wage-price spiral …

This story from Zerohedge is a pretty good summary of where things are in Japan in regard to monetary policy. In short, it looks like the BOJ is on the cusp of raising rates and that could happen as early as its meeting next week.

This has been a long time coming and there have been a lot of false starts along the way. In addition, relatively modest inflation numbers recently have caused several commentators to suggest the BOJ will continue to hold off.

Japan operates according to different rhythms than the US though. Wages are negotiated annually, en masse, not individually. Accordingly:

With the shunto spring wage negotiations largely concluding on Wednesday, economists expect large companies to give their unionized workers an average wage increase of more than 4%, compared with 3.6% last year. That would be the biggest rise since 1992.

While these increases are currently higher than inflation in Japan, wage earners still have catching up to do. As one trade union leader described, “We need to bring 30 years of wage stagnation to an end.”

This change in monetary policy at the BOJ could quite arguably be the most important macro event in 2024, and possibly for several years. Regardless of how fast or slow it goes, it sends a huge signal to the world that Japanese savings will be coming back to Japan. In an even broader sense, it marks the closing of the door of the neoliberal era. As such, it also solidifies the global swing to labor at the expense of capital. Yeah, it’s a big deal.

Monetary policy

When the Treasury pulled back on its estimates for coupon issuance late last year, the consensus interpretation was that Treasury was instituting a cap on bond yields. Specifically, 5% on the 10-year bond was viewed as a red line that would trigger policy action.

While I expressed my doubts about that interpretation at the time, preferring instead to view it as a way to ease end of year conditions for banks, the issue of where bond yields might go is coming up again. As Althea Spinozzi posted, “Sticky inflation may require the Fed to normalise the yield curve though a “reverse operation twist”.

Indeed, modifications to the Quantitation Tightening (QT) program are being discussed. Specifically, the Fed could taper QT such that only coupons would runoff and could buy “Tbills when redemptions are above the QT cap”. This would inflect the yield curve steeper.

This possibility is interesting for two reasons. One is that it runs directly counter to the consensus belief at the beginning of the year that Treasury had capped long rates. Second, it is an important marker for my expectation of a steeper yield curve that I expressed in the Outlook edition in January. This will help improve bank profitability but will also tighten financial conditions. I think this will surprise a lot of people.

Investment landscape I

On a personal basis, I have been equally amazed and appalled at the growing presence of gambling in society. It’s not that I’m opposed to gambling, per se, but it seems like it is becoming ubiquitous and is beginning to squeeze out more productive ventures. Neil Howe recently posted an interesting hypothesis regarding the popularity of gambling:

Sports gambling has proven popular among Millennial men. This may seem like a surprise, given their generally risk-averse nature. But they don’t view it as pure chance: Armed with algorithms and data, many believe they can tilt the odds in their favor.

This hypothesis resonates with me because it jives with so many things I have observed. For example, as various forms of real-time “alternative” data have become available, something of a cottage industry has emerged to exploit short-term momentum signals. This has been manifested most of all in the form of “pod shops” which I mentioned last week.

The thing that’s interesting is not that such efforts might be made, but that they have been so aggressive in taking on leverage and in pursuing situations that are likely to fail over the long-term. In other words, they too are gambling. So, while data and algorithms go some way in explaining behavior that cannot succeed long-term, at best they serve as a partial explanation …

FINANCIAL NIHILISM

https://www.epsilontheory.com/financial-nihilism/

Probably the topic within the thesis that garnered the most discussion was the concept of “financial nihilism” – the idea that cost of living is strangling most Americans; that upward mobility opportunity is out of reach for increasingly more people; that the American Dream is mostly a thing of the past; and that median home prices divided by median income is at a completely untenable level.

That’s the setup. The Boomers have all the money. The rich have been getting richer while the poor are getting poorer. The American Dream of upward mobility has been slipping out of reach for increasingly more people … That is Financial Nihilism. So if you’re like the large majority of Americans and you’re on the wrong end of this, what do you do about it?

You take bigger risks. You feel driven to take bigger risks to try and leapfrog from your current financial position (mostly paycheck to paycheck; buying a home feels nearly impossible; saddled with student loans; salary increases not keeping up expense increases) to something more tenable. More comfortable. More baller. So you gamble. You. F**king. Gamble. You look anywhere, for anything, that can give you a 5:1, 10:1, 50:1 type of payout.

I’ve touched on this subject before, but this explanation from Travis Kling is the best one I’ve seen so far. In the context of momentum-driven markets and the popularity of gambling, it is also a very timely one.

As Kling describes, “The underlying drivers of Financial Nihilism and Populism are the same – this system is not working for me, so I want to try something very different (e.g., buy SHIB or vote for Trump).” “Different” isn’t necessarily “better”, but it’s understandable why it would be tried.

One point, then, is while Howe shows how algorithms and data may facilitate gambling, it is Kling who better describes why gambling has become so popular. Gambling is in part viewed as the least worst of a crappy set of options for many people. In addition, gambling is viewed as a protest vote, an act of resistance, to a system that doesn’t work for too many people.

Another point is that I have been amazed at how many older people (though certainly not all!) seem completely indifferent to these issues. Many are complete unaware that the math is just totally different for younger people and doesn’t work any more. Others just don’t care. While this may partially explain the tone deafness of policymakers, it also suggests there will be a lot more social upheaval before things change.

Investment landscape II

With the Fed’s position on rates being a key factor for market sentiment, the following comments from Atlanta Fed President Raphael Bostic provide useful perspective (h/t John Mauldin):

“There is another upside risk [to economic growth and inflation] I'll highlight. As my staff and I have talked to business decision-makers in recent weeks, the theme we've heard rings of expectant optimism. Despite business activity broadly moderating, firms are not distressed. Instead, many executives tell us they are on pause, ready to deploy assets and ramp up hiring when the time is right.

“I asked one gathering of business leaders if they were ready to pounce at the first hint of an interest rate cut. The response was an overwhelming "yes."

“If that scenario were to unfold on a large scale, it holds the potential to unleash a burst of new demand that could reverse the progress toward rebalancing supply and demand. That would create upward pressure on prices. This threat of what I'll call pent-up exuberance is a new upside risk that I think bears scrutiny in coming months.”

Point number one is that phrases like “expectant optimism” and “ready to pounce” are not phrases one normally hears upon entering a recession. While there are still clearly areas of weakness, the economy as a whole seems to be more oriented to gearing up for higher growth than for paring back operations.

Point number two is this reality paints the Fed in a different light: It is not looking solely to start a campaign of lowering rates back toward the zero bound. Rather, it is also wary of allowing a big inflationary burst of growth. As Bostic summarizes, there is a recognition that “the risks to achieving price stability have balanced out. That is, there are now two ways things could go wrong.”

It’s hard to say how much of the business world’s “expectant optimism” is based on the misguided notion that the Fed’s first rate cut will signal a return to very low rates and how much of it is based on strong economic activity. Regardless, Bostic’s views of the risks appear to be far more “balanced” than the market’s.

Portfolio strategy

The Keynesian Stupidity Contest ($)

https://www.yesigiveafig.com/p/the-keynesian-stupidity-contest

I remain steadfast in my view that R2000, exposed to the credit refinancing risk of 2024, the loss of momentum leaders, and continual redemptions from active managers, remains the weakest part of the market. While all eyes are focused on the S&P500 and Nasdaq, it’s the unloved R2000 that has my eye.

However, due to competitive forces profit metrics tend to be mean reverting. And this is particularly true in recessions and even more so for a broader index like the R2000 with fewer monopolists. So, the odds of a return to average profitability (3.7% ROS) are quite high. A fall of this magnitude would reduce EBITDA by about 30%. Meanwhile, the current coupon on debt averages about 5% for the R2000. The looming maturity wall suggests that it will be repriced towards 8% at current spreads. So a 50% increase in interest expense and a 30% decrease in EBITDA would be enough to send interest expense as a % of EBITDA to 73% (6.4/0.7x8%) and likely over 100% of EBIT.

Mike Green makes an important point here that with all the momentum in the larger cap indexes, investors may be getting distracted away from an arguably more important phenomenon: The enormous headwind to profitability for small cap stocks. If you incorporate the additional expense of repricing existing debt higher with the potential decline in profitability from an economic slowdown, you would be looking at a new interest expense that would consume the entirety of the average small cap’s earnings before interest and taxes (EBIT). In other words, you would have a major credit event.

While I probably have less concern about a major economic slowdown than Green does, at least in the near future, I agree that credit is an important risk to be monitoring and that it probably isn’t getting the attention it deserves. This is especially noteworthy given the fact that many have called “for a rotation to small caps.”

The small cap recommendation is predicated on the anticipation of relatively high nominal GDP growth, facilitated by the policy goal of rebuilding the industrial capacity of the country. Rejuvenated middle class incomes, supported by fiscal policy, will reduce inequality and increase economic growth in a virtuous cycle. Or so the logic goes. This is a fine goal, but it’s not going to all happen in just a few months and it will also have to overwhelm the concomitant losses of over-leveraged companies. In short, it’s likely to be messy.

Implications

By the sounds of it, the idea of financial nihilism originated with Demetri Kofinas. He also provides a description of the landscape that inspired it:

While Soros saw prices affecting fundamentals (and vice-versa), financial nihilists see price as "the thing" in and of itself, completely unmoored from any relationship to underlying reality. It's a post-modern investment framework where price becomes self-referential.

All of this has been made possible because policymakers have suspended the moment of clarity by capturing the game, turning free-market capitalism into a type of regressive financial socialism for asset holders.

There are three key aspects to this mental model. One is that prices are completely unmoored to any underlying reality. Another is that it is a “regressive financial socialism for asset holders”. In other words, it’s an inequality amplifier. If you already have financial assets, awesome. If not, that sucks for you. Finally, it has been entirely contrived by policymakers who have “captured the game”. They made decisions and implemented policies that have created this situation.

Personally, I think this is mostly a correct assessment. As a result, I am not at all surprised that as people increasingly appreciate the situation for what it is, they aren’t at all happy with it. Normally this would elicit a more revolutionary response, but that’s not what has happened. Instead, (mainly) younger investors seem to be thinking along the lines of, “if the game is rigged, then let’s 10x it”. When in Rome …

So we see NVDA, SMCI, and MSTR. We see meme stocks. We see cryptocurrencies. We see an explosion in derivatives. We see 0DTE ETFs. All of this is shocking to someone who is in or near retirement, but has its own perverse logic for younger investors. For them, if the game is rigged for investors and against workers, then why schlepp away at a job knowing the odds are against you? That’s a real risk too. Sure, the game may change some day, but why waste time waiting for that day to come?

Insofar as this characterization broadly captures the dynamics of financial nihilism, it has extremely important implications for investors. To date, monetary authorities have been happy to allow fairly rabid behavior in markets as a means to an end. Strong markets inflate tax dollars, help the Fed normalize short-term interest rates, and keep the banking system running properly.

The ultimate goal of policy, however, is to reorient the economy away from financial engineering toward industrial production and to empower labor relative to capital. So, at some point, the means (capital) comes into direct conflict with the end (labor). I’m sure the Biden administration will do its best to have the best of both worlds going into the election. As markets continue to rise and inflation picks back up, however, this is getting harder and harder to accomplish. Once it turns, there will be a long way to fall.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.