Observations by David Robertson, 3/4/22

It was another wild and woolly week as violence in Ukraine ramped up, the President addressed the nation and everyone is left wondering just how serious things can get. If you have questions or comments, let me know at drobertson@areteam.com.

Market observations

After minute by minute updates from Ukraine last weekend, everything seemed to settle down Sunday evening. Indeed, the week started off with a surreal sense of calm in the stock market given the magnitude of events.

The same cannot be said of the fixed income or currency markets, however. Treasuries rallied hard on Monday and Tuesday with 10-years right around 2% a week ago Friday and dropping under 1.7% on Tuesday … and then crashed on Wednesday. Apropos to the dramatic volatility, there were plenty of “sigmas” bandied about to characterize the uniqueness of the situation.

Currencies were also affected. The Russian ruble cratered as a result of sanctions on the central bank and the US dollar was exceptionally strong.

In large part, markets seemed to be watching and waiting to figure out what, if anything, to panic over. Charlie McElligott from Nomura captured the situation as well as anyone: “the focus in coming-days will likely be in the financial system ‘plumbing,’ where we are seeing expected signs of risk-off - but certainly no current ‘stress’ - in USD funding space, as markets wait for the first fallouts of the Russian liquidity lockout”.

Commodities

One of the most noticeable market phenomena this week has been the explosion higher in oil prices. Already at high levels at the start of the week, oil took off on an even higher trajectory and went further into backwardation. The conflict in Ukraine and the consequent sanctions placed on Russia are putting people on high alert for where the glitches in the supply might start showing.

"The Market Is Starting To Fail": Buyers Balk At Russian Oil Purchases Despite Record Discounts, Sanction Carve Outs

Acting as if energy were already in the crosshairs of Western sanctions officials, refiners have balked at buying Russian oil and banks are refusing to finance shipments of Russian commodities, the WSJ reports citing traders, oil executives and bankers.

The sanctions on Russia are essentially making toxic any association with the country or its oil. As a result, banks, tankers, transport companies, refiners, brokers, anyone whose fingerprints may be on a transaction, are potentially at risk for severe penalties. The safest route is to abstain altogether.

This has two major effects. High compliance with the sanctions make them especially effective in causing financial pain. However, because they are so effective, anyone involved will also be making future plans to mitigate exactly this risk in the future.

For the time being, there is a standoff. Russian pain is immediate but fairly quantifiable. Western pain, in the form of much higher fuel prices and/or shortages, has yet to be felt. If storage gets depleted while supply is still below demand, there will be a hefty economic and political price to pay. This is not the kind of slow, steady price increase you would want to justify a long-term bull case on energy.

Goehring & Rozencwajg Natural Resource Market Commentary, February 23rd 2022

http://gorozen.com/research/commentaries/4Q2021_Commentary

We have always been big believers that OPEC’s spare capacity has been significantly overstated.

After agreeing to the 2015 production cuts, Russia made known that it had little interest in further collaboration with OPEC. What Russia wanted and what the Saudis desired were not aligned and the schism between the two huge oil-producing countries became obvious after the COVID-19 pandemic began severely impacting global oil markets. In response to collapsing demand, the Saudis again approached Russia in March of 2020 and requested its cooperation in reducing production—a request that Russia rejected. In response to this rejection, the Saudis initiated a vicious price war with the intent of bringing the Russians back to the negotiating table.

A couple of great points here from Goehring and Rozencwaig who never shy away from independent, nonconsensus positions. One is that a good argument can be made that OPEC’s spare capacity is less than advertised. If so, this would bring forward the timing of sustainable price increases and ultimately greater investment in new production. Good to keep in mind.

Another points to the inherently fractious nature of OPEC. The history between Russia and Saudi Arabia has been considerably short of collegial. When push comes to shove, it is hard to say which interests will win out - those of the cartel or those of the individual countries. This adds a lot of uncertainty to an already dynamic mix.

Ukraine war disrupts global market for grains ($)

https://www.ft.com/content/b6712657-d6b7-4d56-95f7-849a653d5a66

The disruption of grain exports from Ukraine and Russia through the Black Sea will probably lead to physical shortages of food in the world, particularly for countries dependent on those supplies. If the war is prolonged, it will impact millions of people living in places such as Egypt, Tunisia, Morocco, Pakistan and Indonesia. That could have political consequences.

According [sic] S&P Global Platts, Russia and Ukraine together were projected to export 60mn tonnes of wheat in the crop year of 2021-2022. All Ukrainian wheat exports, and most Russian exports, pass through terminals along the north shore of the Black Sea. It is not certain when Black Sea ports can reopen. Ships are not available for chartering, and even if the owners were willing, insurance would be unavailable.

John Dizard reminds us the fighting in Ukraine affects more than just the cost of gas for US consumers; it also affects the cost and even availability of food in many places around the world. The result of food shortages, especially in many places already additionally burdened from the consequences of Covid, is a slow-burning geopolitical fuse.

The long and the short of it is the situation in Ukraine is much more than a short-term “war” story. It is also a humanitarian story - both for the citizens of Ukraine and for consumers of its food production worldwide. As Dizard concludes, “It is all a reminder of the historic importance of Ukraine’s grain production.”

Geopolitics

I have to admit I was mesmerized by the story in the Ukraine as it really started unfolding over last weekend. There were so many interesting things happening all at once.

For starters, I was observing mainly through Twitter and I found the reporting to be pretty darn good. I quickly got a visceral sense of what it was like to be there and what was at stake. Very powerful.

Apparently, I wasn’t the only person so affected. Demonstrations across the world emerged to express sympathy for the Ukrainian cause.

I was also fascinated, however, by many other stories that were playing out in real time. The mobile phone video appeal of Ukrainian President Zelenskyy resonated with people around the world. In doing so, it also allowed Zelenskyy to create the narrative himself, rather than have it be established by mainstream media companies from afar. It succeeded because it felt real. There is much to appreciate in such use of technology.

The widespread sympathy that was elicited also revealed a streak of humanity that crossed the globe transcending national boundaries and political parties. In a flash it reminded people of the things that are really important.

Another story line that developed was the demonstration of diametrically opposed philosophies of power. I highlighted the concept of “New Power” in a blog a few years ago based on the lessons of Jeremy Heimans and Henry Timms in a Harvard Business Review article. The playbooks of Zelenskyy and Putin highlighted this to a tee.

Heimans and Timms explain that "Old power is enabled by what people or organizations own, or control that nobody else does ..." In contrast, "New power operates differently, like a current. It is made by many. It is open, participatory, and peer-driven … The goal with new power is not to hoard it, but to channel it."

It seems to me like there are two things going on here. One is Putin is a reprehensible figure for the violence he is imposing on innocent people. Another, however, is he is the poster boy for old power. It is not hard to conflate the two and just want them to go away. As a result, I think this may very well be a “coming of age” moment for new power. Already it has caused Europe to rapidly change course on energy and defense policies. If this is a tipping point for new power, the scope of change will be vast.

Inflation

Jim Bianco has been all over the political importance of inflation and he highlights it again here. Certainly the Fed is in a tough spot. On one hand, it must contend with inflation that remains persistently high.

On the other, it must contend with economic growth which is tanking quickly. The current reading is 0.0%

Regardless, the Fed will have to pick one over the other and when it does, a lot of people will be disappointed.

Monetary policy

Bond Chaos As Rates "VaR-Shocked" Amid Full-Blown Stop-Outs

https://www.zerohedge.com/markets/rates-var-shocked-full-blown-stop-out-fashion

TL/DR Bottom line: the Fed is about to lose control, with the market saying it is unable to hike into what everyone now realizes is a major stagflationary shock.

When the President spoke on Tuesday evening, he listed inflation as the number one priority. When Powell gave testimony to Congress on Wednesday, he pledged to fight inflation. At the end of the day, it doesn’t really matter that much, as the zerohedge piece points out.

If the Fed starts raising rates but inflation remains high, as increasingly appears will be the case, inflation expectations will still shift higher. If the Fed fails to act for fear of hurting the economy, inflation will remain high and expectations will shift higher. Either way, we get stagflation.

Investment landscape

Sanctions and markets ($)

https://www.ft.com/content/75b4737a-3390-4982-84f9-f9235bc88a38

The point is that, as Unhedged’s friend Edward Al-Hussainy of Columbia Threadneedle puts it: “You don’t know where these waterfalls will come to an end.” Nor do you know what is being sold because people don’t want it, or instead because it is liquid and something has to be sold. US stocks are selling off in overnight trading now, for example. This could well be a liquidity grab rather than a flight from risk (that said, in extreme situations, the two are impossible to distinguish).

For extremely courageous investors in possession of scarce liquidity, this will mean some assets will be going on sale in the days to come. But a very long term view will be required. Expect to see irrational prices — that go on to get more irrational still.

Illiquidity is sort of like driving too fast; it’s something older people always seem to be warning about and it seems like so much finger wagging until something bad happens. Investors in Russia are getting a first hand account as sanctions take hold and they have no way of transacting their holdings.

This isn’t necessarily a huge problem, but it can certainly become a problem if a holder is leveraged or otherwise needs immediate access to the holdings. Lack of liquidity brought down Long Term Capital Management in 1998 and nearly took down several banks that had lent money to the hedge fund.

One point is liquidity problems often take some time to emerge. The subtitle of the article above says it well: “A dash for liquidity has begun, and will spread”. It takes time partly to realize who gets squeezed first. It also takes time for investors to assess who else might be the target of sanctions or capital controls. This is how contagion starts.

Another point is when liquidity dries up, it can have counterintuitive effects. For example, if efforts to sell illiquid securities fail, and cash is required, then liquid securities are next in line. As a result, it is often high quality, liquid securities that sell off during liquidity crises - because they are the only ones that trade in sufficient volumes.

PwC fined over exam cheating involving 1,100 of its auditors ($)

https://www.ft.com/content/2e246b48-a6a9-4dc6-b4fb-136b62ab3a3a

PwC Canada has been fined more than $900,000 by Canadian and US accounting regulators over exam cheating involving 1,100 of its auditors.

KPMG was fined $50mn by the PCAOB in 2019, partly for the improper sharing of answers by its auditors, some of whom also manipulated a computer server so they could pass even if they scored less than 25 per cent on the tests.

While accounting is a far cry from the situation in Ukraine, it does represent another important aspect of the investment environment: The horrendous amount of rot that pervades the audit business.

For a little background, the purpose of an audit is to “ensure that the books of accounts are properly maintained … as required by law”. In other words, it is to make sure the subject organization is playing by the rules - for the larger purpose of ensuring people can trust the financial information.

Of course, it is impossible to be perfect and there are always a few bad apples, but the examples above represent absolutely systemic cultural failures. More than 1100 auditors cheating on exams? Auditors who manipulated a computer server in order to pass? This isn’t just a mistake but rather a focused and intentional effort to subvert the very principle of oversight the firm exists to uphold.

In my mind any auditing firm exhibiting this magnitude of failure should not be allowed to continue operating. Let the firms fail and the few good auditors start up new, honest operations. In the meantime, I wouldn’t trust any of the financials these firms audit.

Investment strategy

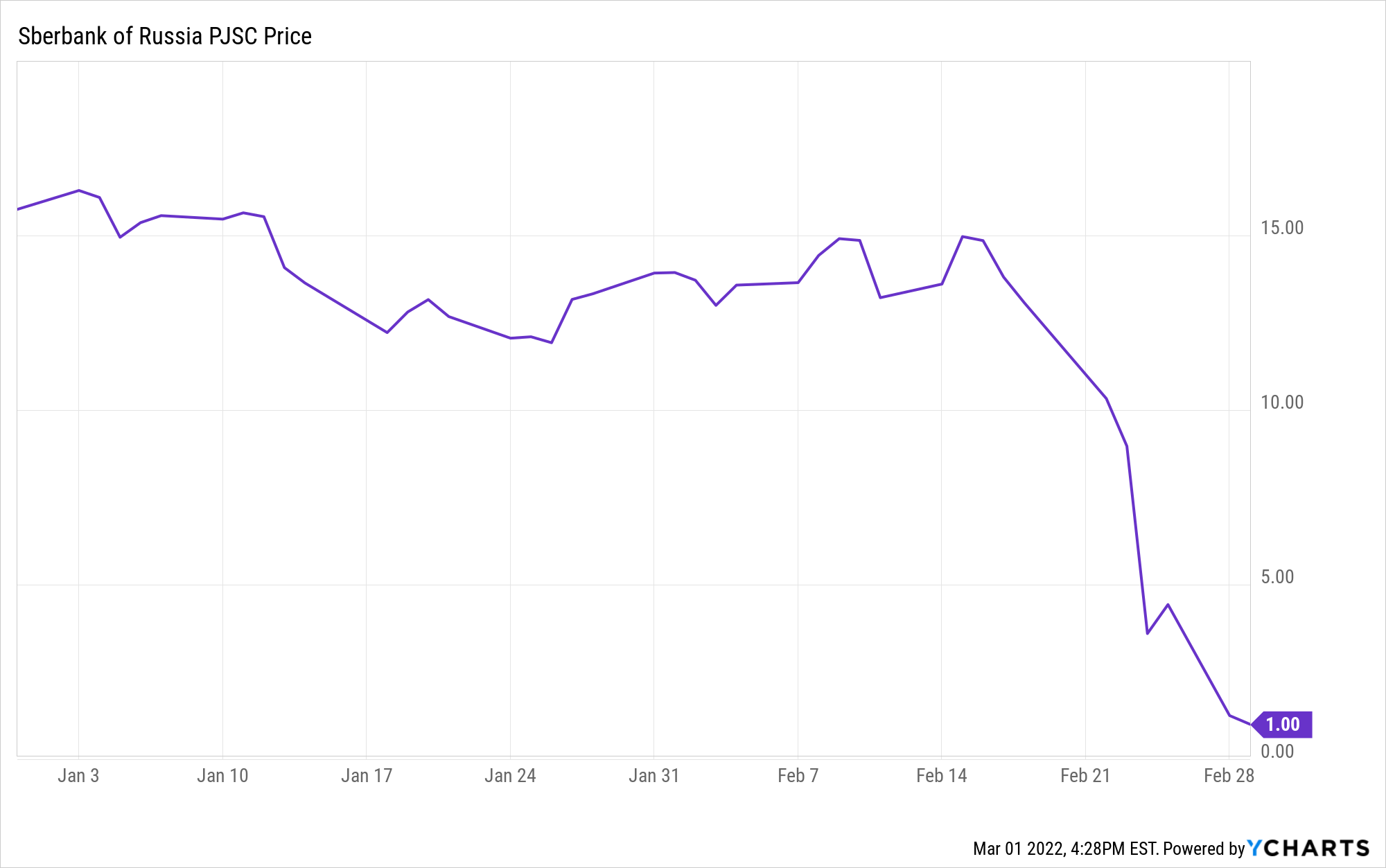

I’ll come right out and say it, it looks to me like we are in a new regime for the investment environment and one in which risk now matters again.

A couple of examples from Russia certainly make the point. Below are year-to-date charts for the index of Russian stocks and the ADR for Russia’s largest bank. As of Tuesday, down 67% and down 94% respectively. Ouch!

To be fair, Russia is not a huge player in global capital markets. Also, volatility is certainly elevated with the conflict in Ukraine and arguably therefore should decline, all else equal.

This is a broader point worth addressing though. While it is true that volatility does not naturally trend over time, it is also true that the unnatural forces of central bank intervention and the proliferation of passive investing have combined to create an extended period during when volatility did trend … downward.

The lesson is, the (unnatural) downward trend can’t last forever. Just as a beach ball does not naturally sink, it can, however, be held under water for a significant length of time. But it does eventually pop back up to the surface.

This creates two challenges in the volatility/risk environment. One is trying to figure out what a “neutral” level for VIX might be. Hard to say, but not in the very low double digits as it was in late 2017.

Another challenge is navigating the path to “normalization”. If we agree a “normal” level of VIX should be higher, what is that level, and how does it get there? The constant, downward trend in volatility had the effect of reinforcing risk-seeking behavior. Whenever investors took on more risk, it worked out. So, they took on more risk.

This doesn’t generally work so smoothly in reverse. Leverage often causes the party to stop suddenly. When it does stop suddenly, it causes other players to re-evaluate risk. As this behavior cascades, contagion spreads. At very least, higher signals of risk and uncertainty should be used to reduce exposures.

Implications for investment strategy

A week like this past one reveals many things and one of them is the nature of risk. The types of risk that often get miscalculated are those that happen rarely, but have a large impact when they do. The Russian invasion of Ukraine counts as one and the imposition of serious sanctions, namely on Russia’s central bank, counts as another.

What does it mean for investors? One big implication is that when rare events happen, they often undermine the assumptions that are used in models. While models are often helpful in “normal” environments, they break down, often violently, when foundational assumptions no longer hold. When the situation gets dynamic like this, it is best to re-test all assumptions and to avoid dogmatic attachment to models.

Higher levels of uncertainty make everything harder. It costs more to hedge. The risk of hedges failing increases. Prices bounce around more. Entirely unimaginable possibilities emerge. This can all be extremely disorienting if one isn’t prepared. Perhaps worse, it can feel like a lot of really bad luck. But that’s the problem; it is just the other side of “luck” being too good for too long.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.