Observations by David Robertson, 3/8/24

Stocks continued to run, albeit with a major hiccup on Tuesday. The focus was on Jay Powell’s testimony this week, but there is a lot more than that going on. Let’s take a look.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The main overall driver of stocks continues to be momentum. The graph from @SoberLook tells the story as well as anything:

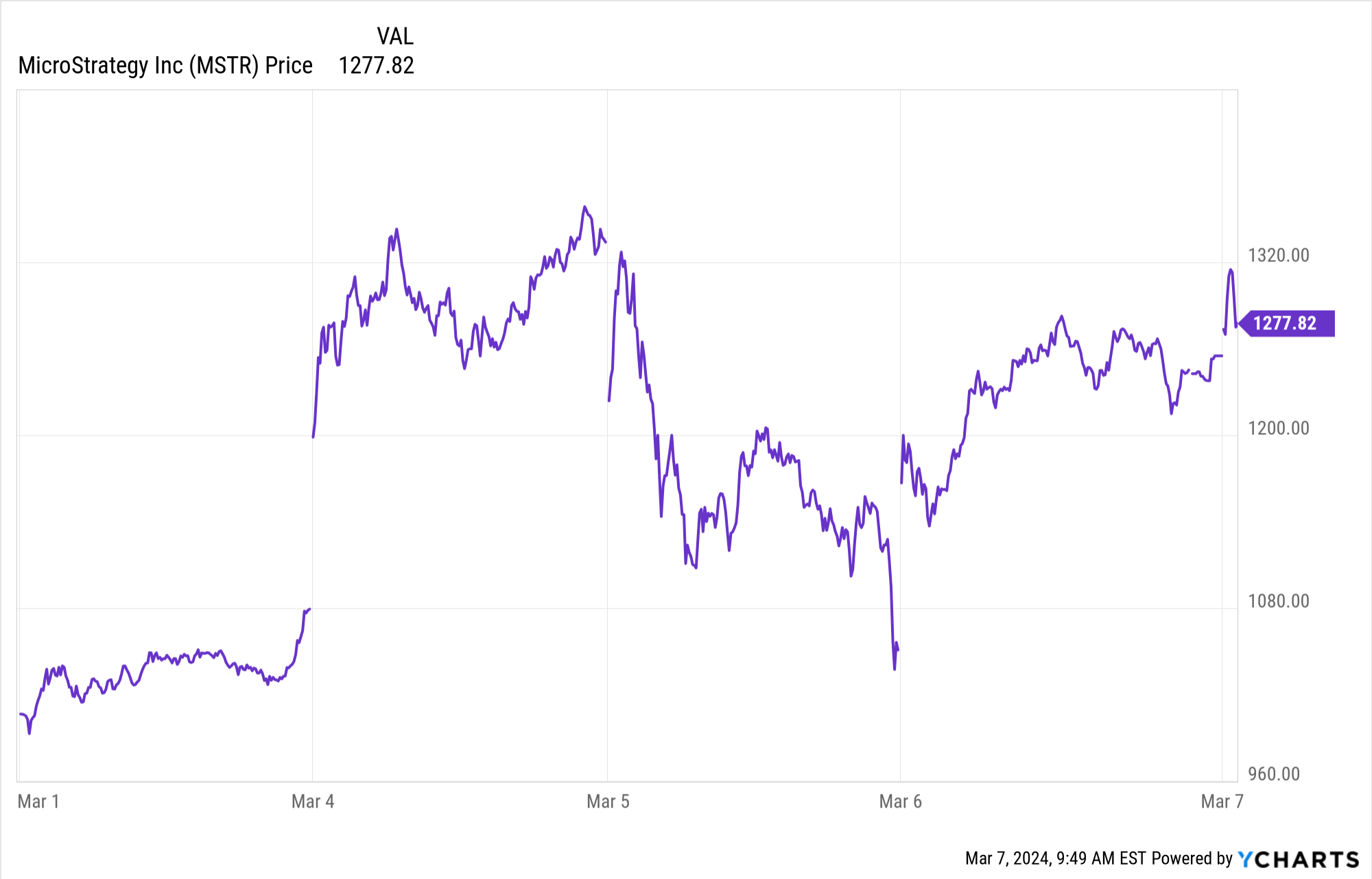

While momentum continued to work through the week, there was a major glitch on Tuesday. Microstrategy (MSTR) was the poster child. After gapping up on Monday, the stock crashed on Tuesday, down 16% at one point. By Thursday it was as if nothing happened - bygones. The volatility index, VIX, was much slower to normalize, however. This action indicates both the incredibly strong momentum at the current time, but also the underlying vulnerability.

Another highlight of the week was gold which started breaking out. After hovering around the $2000/2050 range for most of the past year, gold rose consistently through the week to break above $2150. Given how solidly the 2000/2050 line has held, the breakout could be meaningful for the US dollar, commodities, and a host of other assets.

Finally, I couldn’t help noticing this little pearl of wisdom from SqueezeMetrics: “The absolute smartest stuff you'll read about finance comes from people who left their finance jobs and have no intention of going back. There's a lesson in there.”

Economy

Adam Posen: ‘We overlooked how resilient people are’ ($)

https://www.ft.com/content/ef923a9b-a71a-4d26-b519-836b332b2ab3

My view is that it’s genuine [the increase in productivity]. What happened was that a huge share of workers at the low end of the income distribution basically said you only live once; life’s too short for this. All the while the government was stepping in. So the “reservation wage”, the minimum bundle of pay and working conditions required for a given job, went up. Workers increasingly don’t want to be doing, say, home healthcare for too little money. They’re willing to change jobs.

One of the key factors in determining sustainable economic growth is productivity and the long-term trend has been down. Debt and demographics have a lot to do with that but as economist Robert Gordon posited, most of the really transformative innovations had already occurred by 1970 or so - making substantial subsequent improvements unlikely. I think this is a good baseline expectation.

That said, productivity has spurted up the last few quarters and Adam Posen makes some good points as to why this recent progress may not be transitory. Covid created a step-function change in how the labor force works. It reduced the cost of changing jobs and the opportunities increased. As a result, Covid also facilitated a jump in labor productivity.

While I am always initially suspicious of theories espoused to explain relatively short-term deviations in productivity, I also believe Posen’s thesis deserves consideration. Covid fundamentally changed the work environment - as indicated by the much higher percentage of hybrid workers, among other indications. I have also noted the record high participation of women with children in the workforce.

In addition, Zerohedge recently highlighted the “massive surge in the number of Americans taking early retirement.” It goes on to present a model developed by the Federal Reserve Bank of St. Louis that shows “the US has around 2.7 million more retirees than initially forecasted”.

Surely strong markets have been an important factor in inducing the surplus of early retirements, but it still says something about the labor market. If the workers who are relatively well-paid and who spend most of their time checking their portfolios and planning vacations self-select to remove themselves from the work force, why wouldn’t overall productivity improve?

I am going to remain cautious but watchful on the productivity trend. If it proves durable, it would be enormously beneficial to the economy and to financial stability.

Liquidity

Almost Daily Grant’s, Policy Honk, Friday, March 1, 2024

https://www.grantspub.com/resources/commentary.cfm

“Rates are pretty restrictive,” Chicago Fed president Austan Goolsbee told attendees at a Princeton University-hosted event Thursday. Referencing the tandem of today’s 5.33% effective funds rate and 2.8% rise in the core personal consumption expenditures index over the 12 months through January, Goolsbee rhetorically asked: “the question is, how long to remain this restrictive?”

Yet no one seems to have clued in Mr. Market. The S&P 500 ripped higher by 5.3% last month, marking its best February showing in nearly a decade, while the broad Nasdaq Composite Index reached a record high Thursday for the first time since 2021.

While Goolsbee is certainly positioned on the dovish side of the spectrum, Jay Powell’s testimony to Congress this week conveyed the same basic message: It’s only a matter of time before the Fed starts cutting rates.

Not that Mr. Market needed any more encouragement. As Almost Daily Grant’s chronicles, markets are up strong and there are widespread signs of exuberance. The main question is, “Is Mr. Market miscalculating?”

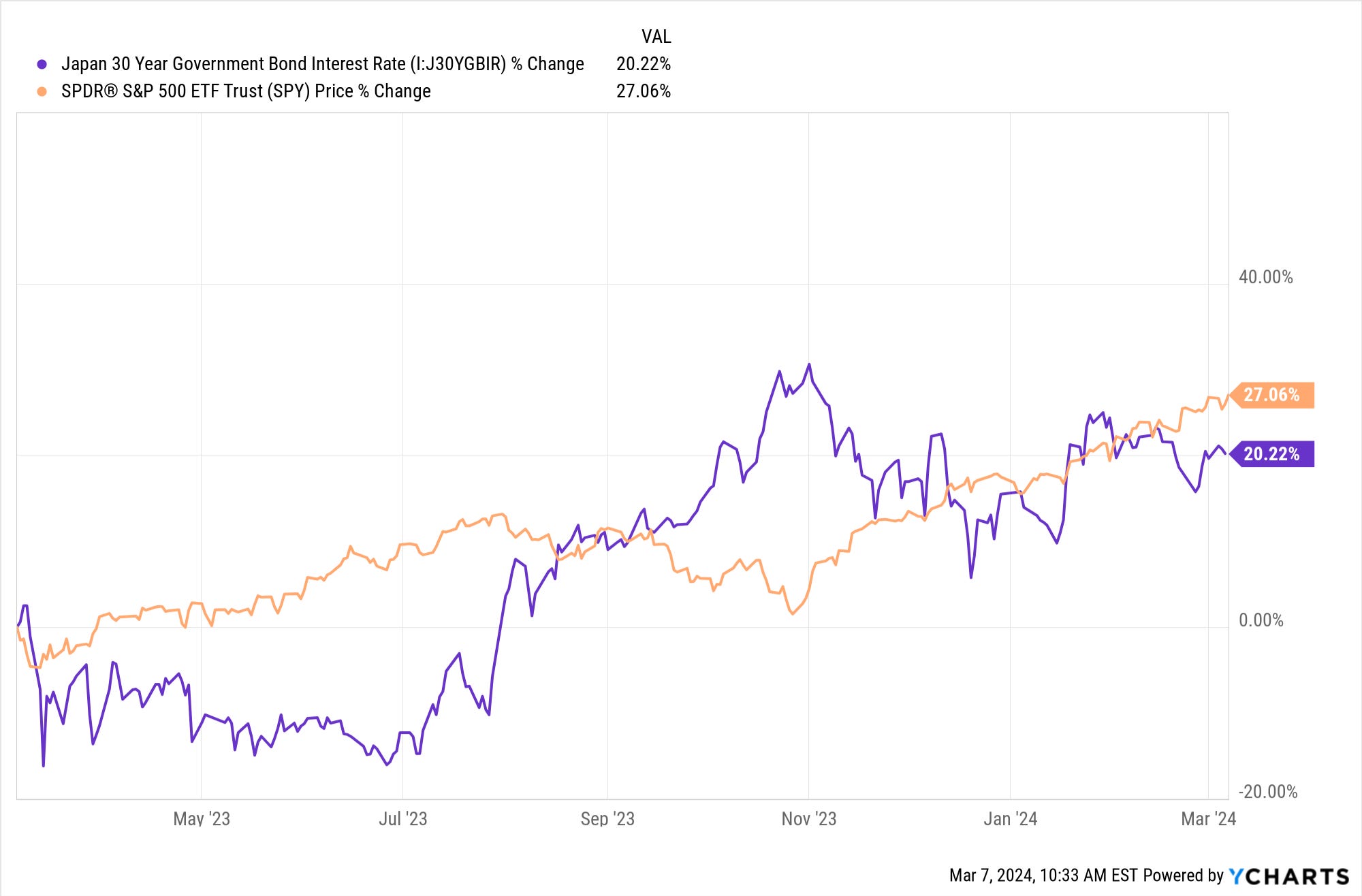

Based solely on the Fed’s position, which is what everyone is focused on, the answer is probably, “No”. But the Fed is not the only provider of liquidity across the globe. If you take a look at the 30-year JGBs (Japanese Government Bonds) you can see a strong inverse relationship with the S&P 500. When JGB yields went up last summer, the S&P 500 turned down shortly after. When JGB yields peaked and then fell in late fall, the S&P 500 turned around.

Since the end of the year, however, JGB yields have been trending up - and so has the S&P 500. To the extent JBG yields are the more important global indicator of liquidity, Mr. Market may be making a big mistake.

Inflation

Drive Through Financing, Almost Daily Grant’s, Thursday, February 29, 2024

https://www.grantspub.com/resources/commentary.cfm

Every restaurant operator knows that prices will be taken up over time, to mirror the inevitable rise in operating expenses [i.e., the dollar’s ever-deteriorating purchasing power -ed.]. He or she also knows enough not to be perceived as a leader in this regard, because some customers will blame the messenger.

A few weeks ago the CEO of Wendy’s made news by saying the company was considering “surge” pricing. After a hailstorm of angry comments, not least of which came from Congress, the company turned tail and nixed the idea.

All that did, however, was to confirm two things. One is the political sensitivity to higher prices. The other, as Roger Lipton, from Lipton Financial Services, noted above, is the business reality of costs rising faster than prices.

One takeaway is there is latent inflationary pressure that is likely to be realized in the future. The restaurant business is just one example. Another takeaway is the inability of policy (either through lower fiscal spending or tighter monetary policy) to do much to solve the problem. Finally, given the very limited set of options, businesses are more likely to respond en masse, rather than individually. That would suggest the progression of inflation is likely to be one of waves rather than small incremental changes.

Investment landscape I

Stockmarkets are booming. But the good times are unlikely to last ($)

But today, in addition to the usual doomsaying, a chorus of academics and market researchers argues that it will be tough for American firms to deliver the long-term growth required to reproduce extraordinary recent stockmarket returns. Michael Smolyansky of the Federal Reserve has written about the “end of an era”, and warned of “significantly lower profit growth and stock returns in the future”. Goldman Sachs, a bank, has suggested the “tailwinds of the last 30 years are unlikely to provide much boost in the coming years.” Jordan Brooks of AQR Capital Management, a quantitative hedge fund, has concluded that “a repeat of the past decade’s equity market performance would require a heroic set of assumptions.”

There were a lot of comments over the course of the week about The Economists’ cover illustration and whether it will serve as a useful contrarian indicator. Maybe the Economist pulled one over on everyone by associating a bullish illustration with an article that was bearish on the market.

In terms of justification for the bearish position, little new information was presented. Of course, valuations are exceedingly high. And yes, research shows “the difference in profit growth between the 1962-1989 period and the 1989-2019 period is ‘entirely due to the decline in interest and corporate-tax rates’.” In other words, it was all due to favorable policy (in aggregate) and none due to improved operating performance.

What is probably more interesting is that these issues are becoming more mainstream. This is causing the narrative to shift from “you’ve got to be in stocks” to something like “you might want to consider easing off of stocks”.

As more and more Baby Boomers hit retirement, it wouldn’t be surprising if risk aversion becomes a more prominent feature of the investment landscape. Once your primary source of income turns off, the threats of high valuations and lower earnings due to higher interest and higher taxes sound a lot more ominous.

Investment landscape II

Leading Lambs ($)

https://www.yesigiveafig.com/p/leading-lambs

What has happened in the last few weeks is an increasingly narrow market being led by increasingly evident stock price manipulation. I do not use that phrase lightly. We can see this most fully in the Russell 2000. Since the S&P500 broke to a new all-time high on January 19th, the character of the R2000 advance has been astonishing. A total of 152.72 points have been added to the index for a 7.94% gain. Of that gain, nearly one third comes from just 10 of the 1,175 stocks that rose in a near vertical fashion

This is Mike Green at his best in analyzing the huge run up in the Russell 2000. As he points out, “No such acceleration is seen in the aggregate [fundamental] data”. No, this isn’t due to macro or operational improvement.

His explanation is that “hedge fund pod shops are doing something very different [than fundamental analysis]. They are coordinating to drive equities into indices”. In other words, they are intentionally manipulating the largest small cap stocks higher so they will be forced to be included in the large cap indexes. When that happens, all the passive large cap index funds will be forced to buy those stocks, and that will provide exit liquidity for the hedge fund pod shops. In Green’s words:

While gross, and likely illegal, can you really blame them? The ability to manipulate stocks into an index is an obvious application of the insights that passive funds have to buy.

So, one point is this type of activity has nothing to do with economic activity or allocating capital. It’s merely a game (of sorts) to transfer wealth from passive funds to hedge funds. The opportunity only exists because passive funds are too dumb and the regulatory environment is too lax to do anything about it.

The other point is it is useful to be aware that a big part of the reason the small cap indexes are shooting up has nothing to do with the economy. And that is Green’s main point: “In a passive world, stocks no longer qualify as leading economic indicators.”

Investment landscape III

Know Your Enemy - Praetorian Capital

https://pracap.com/know-your-enemy/ (h/t PauloMacro)

I certainly don’t agree with everything Kuppy says, but this piece serves as a great companion piece to Mike Green’s piece above and provides a little more guidance in doing so. He starts with the hypothesis that “we’ve hit peak pod-shop”:

The idea that you can run a highly levered, yet fully hedged portfolio, with negligible volatility seems illogical. Pod-shops have grown massive and have completely distorted the market—often as multiple pod bros tend to have the same trades on, bullying a stock in the direction that they favor, stampeding everyone in their way. These guys live and die on rate of change. They use almost real-time data, data that I mostly ignore as a longer-term investor. If this week’s credit card runs are inflecting up, they buy more, if they’re inflecting down, they short more of it. They frequently play quarters, often playing intra-quarter. Pods seek momentum and trend; they don’t seek fair value.

In my realm of value investing, I’m genuinely amazed at how these pods will short high-quality, rapidly growing businesses at under five times cash flow—just because the next quarter will be weak. I don’t understand how that strategy makes money, except during highly truncated bear-raids, yet the pods keep playing at it as they fixate on short-term rates of change. Then right after the negative print, they often accelerate their short selling, pressuring the stock in the pre-market and further spooking the longs. They want to take a bad quarter and stampede things, so that they can cover.

I found this especially useful because it dovetails with what I have observed, explains a great deal of unusual market action, delineates the risks involved, and highlights the opportunities.

For starters, one thing that has happened since Covid hit is that some stocks have gotten really, truly cheap on a cash flow basis. That’s an opportunity that didn’t exist in the QE years.

In addition, Kuppy explains the mechanism by which the mispricing has happened. Since hedge fund pods focus only on short-term rates of change, and since they usually work with pairs trades, valuation doesn’t matter at all. “Pods seek momentum and trend; they don’t seek fair value.”

This presents opportunities for valuation based investors, especially those with a longer time horizon. Stocks with improving fundamentals but terrible price action can be bought, but you need to have the research chops to be right on fundamentals and you need to have some patience.

That patience also applies to market exposure in general. Kuppy expects “most of these pod-shops will eventually liquidate in a cataclysm of margin calls”. When that time comes, it will also present an opportunity to anyone who has cash on hand to pick up the carnage.

Investment advisory

A couple of weeks ago I mentioned a podcast David Einhorn had done that has been getting a lot of attention. In it he makes the case that markets are broken, meaning “passive investors have no opinion about value”. The more net flows are dominated by passive strategies, the less stock prices have anything to do with fundamentals.

Coincidentally enough, two investment luminaries have recently revealed indexes based on thoughtful research, not just size (market capitalization). Chris Whalen created the WGA Top 25 Bank Index (WBXXVPSW) based on market and operational factors. As he puts it, “We believe that somebody needs to actually do the work on picking good banks from the bad, especially when the consumers are retail investors.”

In a similar vein, Jim Bianco also recently revealed the launch of the WisdomTree Bianco Total Return Fund (WTBN) on the NASDAQ which “seeks to track the price and yield performance, before fees and expenses, of the Bianco Research Fixed Income Total Return Index”. The new fund provides access to Bianco’s research and offers “differentiated positioning relative to the market universe”.

While this is a fairly compelling indication of increasing interest in more active management, it is only anecdotal. Interestingly, a survey presented by Dave Nadig, an expert on ETFs, shows over 40% of advisors are now planning on increasing their allocations to active strategies. That makes the shift to active a lot more than just anecdotal.

It’s not hard to see why this is happening. As passive has gotten bigger, its flaws have become more obvious. More importantly, its risks have become larger and more imminent. This isn’t to say there won’t be a place for passive investing, but it certainly is looking like there could be a big fall out over the next several years.

Asset allocation

Why Not 100% Equities

https://www.aqr.com/Insights/Perspectives/Why-Not-100-Equities

If you are of a certain age and look through the streaming services for something to watch, it’s hard to escape the fact that a huge proportion of the series and movies are just reconfigured versions of shows that came out twenty or thirty years ago, usually in an updated, but less compelling regurgitation. Unfortunately, the same can be said of many investment theories.

The latest one to make the rounds (again) is the idea that long-term investors really should be invested 100% in equities rather than in some combination of diversified assets.

Cliff Asness, who can be prickly and quick-tempered, but who is also incredibly knowledgeable about finance, demolished the argument for 100% equities thirty years ago and is reminding investors again of the faulty logic.

The main flaw in the argument is it simply picks the highest returning asset class which is equities. As Asness highlights, selecting the highest returning asset over the long-term does provide the highest returns, but this finding is trivial. If you want to go with stocks, then why not leverage the stock portfolio? Why is 100% the right risk level and not 150%, or any other level?

This raises another flaw in the argument. If there is a certain risk level that is optimal, it would make more sense to construct an optimally efficient portfolio and then lever it up or down to the desired risk level.

What this incident highlights for me is the disservice that so much of the finance and investment industries do to investors. There is really good research and learning out there that can help investors. Unfortunately, there are a lot of bad and insincere takes that can be confusing at least, and misleading at worst.

Implications

Crazy market action in a lot of places has spawned widespread talk of whether we’re in a bubble or not. I think the discussion overlooks two important points. First, what would it matter? How would knowing we’re in a bubble (or not) better guide investment activity? The answer is it wouldn’t be helpful - so it doesn’t really matter.

The other point bubble talk overlooks is that key elements of the landscape are contributing to the bubble-like action. One of those is the continued flows into passive funds. Those regular flows keep prices going up. It’s got nothing to do with behavior.

Another element is policy. Sure, there is wildly speculative behavior going on, but in the context of fiscal spending that just keeps flowing and monetary policy that backs off every time there is even an inkling of a threat. So, maybe a better description would be that we’re in a policy-driven quasi-bubble.

The key here is policy. Policy can be expected to remain fairly unrestrictive so long as policy goals remain the same and so long as inflation and other threats do not impose meaningful constraints. As a result, I suspect things like gasoline prices and inflation breakevens are going to be far more useful guides to market direction than any kind of consensus on whether we’re in a bubble or not.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.