Observations by David Robertson, 4/1/22

The news was quieter this week but that doesn’t mean the landscape is less uncertain. Undoubtedly, many managers hunkered down just trying to get to the end of an incredibly volatile quarter. With the start of April, it will be back to business as usual. Let me know if you have questions or comments at drobertson@areteam.com.

Market observations

One phenomenon that got increased attention during the week was the rapidly weakening Japanese yen. John Authers points out that the yen’s recent dive leaves it “as far below its long-term trend as it has been this century” and further emphasized, “This is strange as the yen is generally regarded as a safe bolt-hole when geopolitical or financial tensions are raised”.

Further, as inflationary pressures pick up even in Japan, we are getting a nice preview of the limits of monetary policy under conditions of extreme debt. The Japanese central bank has committed to buying as many 10-year bonds as necessary to cap rates at 0.25%. There are two major problems, however. One is that the pressure gets released through weakening currency. The other is that it is virtually impossible to control the entire curve.

Keep an eye on this space. As themarketear.com ($) put it on Monday, “When a massive asset class / currency (3rd most traded globally) moves like this it more often than not gets ripple effects in other asset classes / risk appetite. It is worth paying attention.” In other words, Japan may be one of the first places where the rivets start popping out of the financial system.

Despite a plethora of ominous signals, stocks continued marching up through Tuesday and remained fairly bouyant until late on Thursday. One notable coincident indicator has been volatility which got absolutely crushed over the last three weeks.

'Meme-Mania' Is Back: Nomura Cautions Return Of "Foaming At The Mouth" Behavior In Options Markets

The WSB-crowd is back in a major way on this Equities bounce, where for the past 2 weeks, we see the collective “upside grabbing” activity at levels only previously witnessed during prior speculative frenzy periods in the COVID / WSB / “stimmy” era (our basket of 10 of the most prominent “meme stocks” has seen their aggregated daily Call option volumes jump to over +2 z-scores as of last Friday vs the 2 year lookback)

In trying to identify the drivers behind the recently strong action in stocks, especially in light of so many macro headwinds, Charlie McElligott relies on one of the usual suspects: Retail option buyers. Take a look around the market and the hypothesis certainly fits the evidence. Huge and unusual moves in retail favorites like TSLA have dominated the action.

Companies

Coming off strong GDP growth in the fourth quarter, prospects for the first quarter were always more fraught. Reduced mobility from the Omicron variant kept things from getting off to a strong start and a vibrant reopening was rudely interrupted by Russia’s invasion of Ukraine. As the graph below indicates, leading indicators point to a significant slowdown.

Models can be useful in framing economic outcomes, but it is always good to reconcile those to real life experiences as well. To that point, the CEO of Restoration Hardware recently gave a long, rambling answer to what he is seeing in the economy right now - and it’s not good. He even made a reference to the movie, The Big Short.

Yes. Well, look, I mean it's probably one of the most difficult guides since 2008 and '09 … I think it's triggered a greater awareness. Like its like someone I think this was ring the bell, everybody pay attention, and then all of a sudden. everybody started talking, yes … And you've got inflation like I’ve never seen … I mean I think ·· I don't think anybody really understands what's coming from an inflation point of view, because either businesses are going to make a lot less money or they're going to raise their prices. And I don't think anybody really understands how high prices are going to go everywhere … you've got to be able to improvise, adapt, overcome and kind of be ready for anything … I wouldn't call it happy days right now. I'd call it expensive days, be ready. But its not just us, it's everybody I know in every industry …

In short, raw materials costs are going up, distribution costs are going up, everything is going up, and either prices will go up and slice into demand or margins will get pinched. The rubber is starting to hit the road on inflation and if the experience at RH is at all indicative of the broader economy, things are about to get a lot uglier.

Commodities

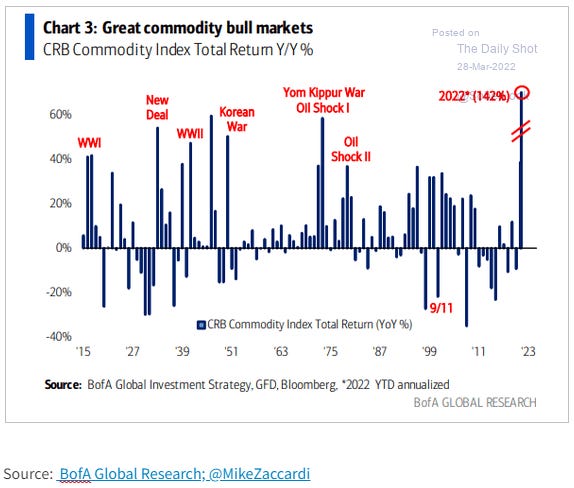

Perhaps the most important market-related story of the first quarter was the break out in commodities. As the chart below shows, performance in the first quarter ranks with the biggest commodity shocks in the last century.

Of course, not all commodities move together. Some like ammonia (below) have absolutely skyrocketed, passing $1600 after having rested in the $200 - $400 range for years. Unfortunately, some like ammonia are also absolutely critical for maintaining food production.

The impact of the oil market’s Russia Shock is somewhere between big and truly massive—likely costing the market between 1-4 MMbpd in Russian supply

The oil market has always been a difficult one to forecast; but right now, it’s more-or-less impossible. The variables currently at play are so large and uncertainty bands so wide that it’s hard to land on anything approaching a high probability base case.

Much of the narrative about commodities in the first quarter was about how high they could go. While it is true that really dire scenarios exist, and it is also true that the supply conditions for many critical commodities are not good, it is also true that there is a huge amount of uncertainty surrounding longer term outcomes.

Rory Johnston does a really nice job in this Substack post identifying both issues. While he characterizes the possible outcomes for oil as ranging from “bad” to “calamatous”, he also calls the forecastability of the oil market right now “more-or-less impossible”. This is an excellent insight to keep in mind before impulsively trading oil or any other commodity.

Public policy

Weaning Europe off Russian energy will mean making changes ($)

Energy prices, whether of petrol, gas or electricity, have rocketed in Europe. Some people might barely have noticed. In France, the authorities have essentially capped electricity and gas bills. Italy on March 18th added €4.4bn ($4.8bn) in subsidies to limit power-price rises for companies and consumers, on top of the €16bn already agreed in recent months. Several countries have cut petrol duties, a much-needed source of tax income. European leaders meeting in Brussels as The Economist went to press were due to discuss new state largesse to households and industry. This is the “whatever it takes” approach at work. As with covid-19, government is paying first and will ask questions later.

The reality of Europe’s tenuous position in regard to energy could hardly have been highlighted any more starkly than by Russia’s invasion of Ukraine. One might be so bold as to view such a challenge as a necessary impetus to make difficult tradeoffs, but alas, one would be wrong, at least so far.

Strikingly, and baffling to those of us who see viable policy options, “no one is seriously considering the obvious way of using less of it [Russian oil].” All sorts of good policy ideas exist, but they are not even being discussed. As the Economist reports, “What is startling is how little is being asked of Europeans.”

There are several possible reasons why governments are not even trying to solve the problem, but the most likely “possibility is that politicians now think their electorates are incapable of sacrifice.”

Whether such sentiment is justified or not, it has serious implications. As Jared Diamond highlights in his book, Collapse: How Societies Choose to Fail or Succeed, a key factor is “society’s responses to its environmental problems”. He elaborated further in a piece for the FT by saying a key predictor for successful response to a national crisis is “acknowledgment rather than denial of a crisis’s reality; acceptance of responsibility to take action; and honest self-appraisal.”

Suffice it to say, failure to even try to solve the problem doesn’t count as a success factor. This implies either the European project will fail or the EU and its constituent countries must dramatically reconfigure their governments in order to be able to respond more constructively. These issues are just as true, albeit to a lesser degree, in the US.

One implication is that without a clear directive for public policy to solve problems in the public’s interest, it is much harder to anticipate the direction or scope of policy intervention. As a result, the dispersion of possible outcomes for factors like demand destruction are extremely high. It is fair to expect a lot of volatility around commodity prices in the meantime.

Another implication is that governance is the main constraint, not policy ideas. Thoughtful solutions and analysis have been proffered by Doomberg and Adam Tooze on Substack, among others. The good news is there are lots of good ideas to work with once governments decide to actually tackle the problems.

Geopolitics

Russia’s Other War of Attrition Is Against Europe ($)

Russia’s greatest military victories came in wars of attrition.

Suppose for a moment that Putin never intended to conquer all of Ukraine: that, from the beginning, his real targets were the energy riches of Ukraine’s east, which contain Europe’s second-largest known reserves of natural gas (after Norway’s) … Even if this is not the aim, the possibility of entrenching Russia’s energy power is now at the center of the broader conflict between Putin’s Russia and the West.

The bad news is Russia may well be using time as leverage against Europe in a war of attrition. Not only are European countries short energy and bereft of sound long-term policies to resolve that imbalance, but now they are also facing the immediate threat of having to manage with significantly less energy.

While the imposition of rationing may help focus minds, such hardships may also weaken political support and soften the resolve to stand strong against Russian aggression. Time will tell, but this will be a big test for Europe.

Regulation

Stories about accounting tend to get put on the back burner until a huge kitchen fire requires all hands on deck. This may be one of those times as suggested by Francine McKenna’s provocative subtitle, “Is the regulator ready for the flood of findings, fines, and sanctions that might jeopardize the viability of more than one firm?”

There are so many problems it is hard to tell where to start. So many cases of conflicts of interest. So many cases of brazen disregard for regulations. Fines that are so small they are considered a cost of doing business rather than any kind of deterrent. Rinse and repeat.

One of the many reasons I vote proxies is because they provide a glimpse into how companies operate. Oftentimes the non-audit charges are quite high. My rule of thumb is that non-audit expenses of more than ten percent of the audit charges signals significant potential for conflicts of interest. It’s just another way of smelling the smoke before the whole kitchen burns down. It sounds like the SEC may finally be doing the same thing.

Investment landscape

A great deal of my commentary over the last year or so has been identifying the various headwinds to the standard balanced or 60/40 portfolio. While the longer-term argument against stocks is straightforwardly based on excessively high valuations, the argument against bonds is a little different. The main point is that inflation is likely to become the preferred way of dealing with excessive debt and as a result, long-term bonds will suffer ongoing erosion of value.

There was little hint of this last year, but as inflation has persisted and the Fed has ramped up efforts to control it, the headwinds for bonds became painfully apparent in the first quarter. This pain is quite likely to persist and as a result, the bond portion of balanced portfolios is likely to be a drag on performance just like the stock portion.

Fund houses buy up ‘alts’ specialists to move beyond equities and bonds ($)

https://www.ft.com/content/c8d45e1f-e30b-411e-81e1-cfb78bf57fc4

Traditional asset management groups are racing to expand offerings in alternative investments as they seek to boost profitability and head off competition from private equity giants.

The big fund houses also recognize the headwinds to the 60/40 portfolio and are relying on their usual bag of tricks to provide “answers”. Those “answers” to 60/40 headwinds include funds that are riskier, have less liquidity, and just by pure coincidence happen to generate much higher fees for them.

A major point is that investors do need better alternatives to balanced funds and there are smart ways to do that. Much of what the fund industry is drumming up does not fit that category, however.

Implications for investment strategy

We suspect the bubble in the private sector is even bigger than the one transpiring in the public markets.

“Coatue Management investors are pulling $250 million from the firm’s main hedge fund. But they won’t get all the money they’re asking for. Assets invested in private companies will be withheld by Coatue and placed in a side-pocket, according to people familiar with the matter. That amounts to 13% of the cash being sought by clients -- a total of $33 million.

Coatue’s decision comes as the firm, like many industry peers, has increasingly invested in private companies, hoping to see outsized gains when these enterprises go public. About 11% of Coatue’s main hedge fund, which ran $15 billion as of year-end, is comprised of private firms. But as market volatility increases asset managers may be forced to mark down the value of their non-public stakes.”

High leverage, overstated valuations, and constrained liquidity are all increasingly problems that are undermining investments in private companies. Interestingly, and not coincidentally, just as fund companies are making a concerted effort to push “alternatives” out to retail customers, reports from within the industry are revealing all kinds of problems.

One interesting difference this time around is that indications of stress are showing up in private companies before public companies. That may partly explain why public markets have remained relatively healthy in light of numerous macro headwinds. In regard to both public and private companies, as always, caveat emptor.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.