Observations by David Robertson, 4/25/25

Aaaand … we’re back. After a few relatively peaceful days last week, market turmoil cranked up again this week. Let’s take a look.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The biggest news item was a set of comments from Secretary Bessent regarding China and tariffs. He was obviously trying to soften tensions without deviating too far from the hard line mission.

At any rate, stocks bounced, the US dollar (USD) bounced, and gold got pounded. Superficially at least, his comments took the edge off concerns that Trump was driving the US economy off a cliff.

Interestingly, however, bond yields while dipping initially, ended up changing little. As a result, it looks like Bessent’s comments probably bought some time, but didn’t change anything fundamentally.

Gold

Gold has been hitting new highs with regularity and yet there is still little attention from financial media. Helpfully, Alyosha ($) provides some interesting trading insights:

The move is abnormally vertical, usually associated with a squeeze. However, there is zero evidence of stress or urgency in futures. Simply put, everyone that owns gold won’t sell it.

In other words, this is not a familiar, run of the mill, kind of thing that tends to be a flash in the pan and then it’s over. In another note, he ($) elaborates:

Open interest is as far from indicative of bullish excess as I can imagine. Comex monthly volume is in the lower 50% of its historic range. The slow stochastic has been trending higher for 3 years, and the April 2025 acceleration higher implies a long-term void that, rather than becoming a vulnerable spike, or Icarus reversal, might become a long-term support area.

In other words this extraordinary void, among the technical possibilities, is actually establishing a new low between $3000 and $3500… not a new high. Let that sink in…

Now this is very interesting. Not only has gold rocketed higher, but there is a good chance it is establishing a new low?

The move in gold is also happening concurrently with US dollar (USD) weakness and an unusual weakness in longer-term bonds as well. As a result, this is looking less like a one-off spike in a particular asset and more like something much bigger. As Alyosha rightly concludes, “we are in extraordinary times”.

Politics and public policy

As we all continue to ride through the twists and turns that is the roller coaster of the Trump administration, it is always helpful to find something more stable to build our ideas and outlook on. Jonah Goldberg ($) comes through again with this piece of insight:

I think the concept of “mandates” is anti-constitutional garbage. Again, I think I have to live with it as a colloquial thing. If by mandate you mean, “He ran on this, so he should try to achieve it,” that’s fine. But that’s not how Trump and Vance conceive of it. They believe the democratic will of the people (i.e. the slight majority of people who voted for him or against Harris) gives them license to simply have their way.

For one, I think virtually all newly elected presidents overstate their “mandate”; it goes with the territory. For example, I think Biden overstated his mandate by imagining himself a modern-day FDR, whereas swing voters mostly voted for him because he wasn’t Trump.

That said, Goldberg is saying this Trump administration is going much further yet by interpreting the electoral victory as a “win” and as such, a license to do whatever it wants. This helps explain the aggressive agenda, the polarization of opinions, and the attacks on several parts of government and democratic institutions. To the victor goes the spoils …

However, this vastly expanded view of what the mandate is also reveals a critical weakness: There are negative consequences to that overreach. As the Economist ($) puts it, Trump “is beating his own record for rapidly annoying American voters”

The Economist goes on to provide the evidence: “His [Trump’s] approval rating has fallen by 14 points since he entered office”, “In polling from YouGov/The Economist, Americans give Mr Trump a net rating of minus-seven percentage points on his handling of the economy”, and “Nearly one in five of Mr Trump’s own voters in 2024 say they disapprove of his handling of inflation and prices”.

These are minor problems now, but promise to be major problems when midterms come around. On that front, Economist data indicates a significant warning flag: “Mr Trump has a net negative approval rating in all six swing states he flipped away from Joe Biden in November’s presidential election (Arizona, Nevada, Georgia, Pennsylvania, Michigan and Wisconsin).”

The polling data corroborates anecdotal data of feisty Town Hall meetings with Republican Congresspeople and a burgeoning force of new political opposition. As the Bulwark ($) reports, “Fired Govt Workers Are Pissed Off and Running for Office”:

In fact, there’s been so much interest from former federal employees that groups like Run for Something and Emerge, which help recruit and train new candidates, have hosted information sessions on Zoom specifically to help former federal employees navigate being first-time candidates.

To put the infusion of opposition energy in context, of the “more than 200,000 people Run for Something had signed up to become potential candidates since the group launched eight years ago, some 80,000 have joined in the past five months.”

The Trump administration is also confounding the country’s CEOs. The FT ($) reports:

“We didn’t believe him. We assumed that someone in the administration that had an economic background would tell him that global tariffs were a bad idea,” said one Wall street executive. “We are in for a roller-coaster ride.”

In sum then, the Trump administration assumed a much bigger mandate than it actually got, acted on that mistaken belief, and in doing so destroyed a great deal of the political capital it had and also gave new life to many forms of political opposition. The main point is that acting with complete disregard for others has consequences. There will be others.

Political and public policy II

David Brooks: I Should Have Seen This Coming ($)

https://www.theatlantic.com/magazine/archive/2025/05/trumpism-maga-populism-power-pursuit/682116/

We conservatives earnestly read Milton Friedman, James Burnham, Whittaker Chambers, and Edmund Burke. The reactionaries just wanted to shock the left. We conservatives oriented our lives around writing for intellectual magazines; the reactionaries were attracted to TV and radio. We were on the political right but had many liberal friends; they had contempt for anyone not on the anti-establishment right. They were not pro-conservative—they were anti-left. I have come to appreciate that this is an important difference.

The left really did create a stifling orthodoxy that stamped out dissent. If you tell half the country that their voices don’t matter, then the voiceless are going to flip over the table.

As is so often the case, David Brooks provides interesting insights into today’s political landscape. For starters, he notes the persistent insularity and arrogance on the left was an important cause of the anger and frustration on the right. In addition, he notes the right separated into two major factions, one of which became obsessed with antagonizing the left.

This helps explain the fixation of the ascendant reactionary right with trolling the political left. It also explains why it is so hard to discern a strategy or a plan amidst the many conflicting ideas: Because the political goal is solely about being anti-left. There is nothing more substantive than that. As a result, the reactionary right isn’t so much reading from a playbook as from a hymnal.

There are also other reasons to doubt the ability of the Trump administration to effect any kind of grand strategy regarding trade, immigration, taxes, or anything else. The reason is it doesn’t have the team in place to do so. It has a team selected on sycophancy and loyalty, not competence and experience. Further, decision making is centralized with Trump himself — who is notoriously unpredictable.

Ben Hunt doesn’t mince words in his assessment:

It’s not just incompetence, it’s incompetence at scale. Ideologue woke-right clowns now have the keys to every cabinet car. I cannot own enough portfolio insurance against USG error, and if you don’t see the building tsunami of capital flight you’re just not paying attention.

The structure of the Trump administration is not an environment that is conducive to ensuring success. Rather, it is an environment with all the odds stacked up against success. That doesn’t mean success can’t happen on occassion, and it doesn’t mean there aren’t some good people sincerely trying. It just means the central tendency over time is to come up short on making improvements. That should be the baseline assumption.

Politics and public policy III

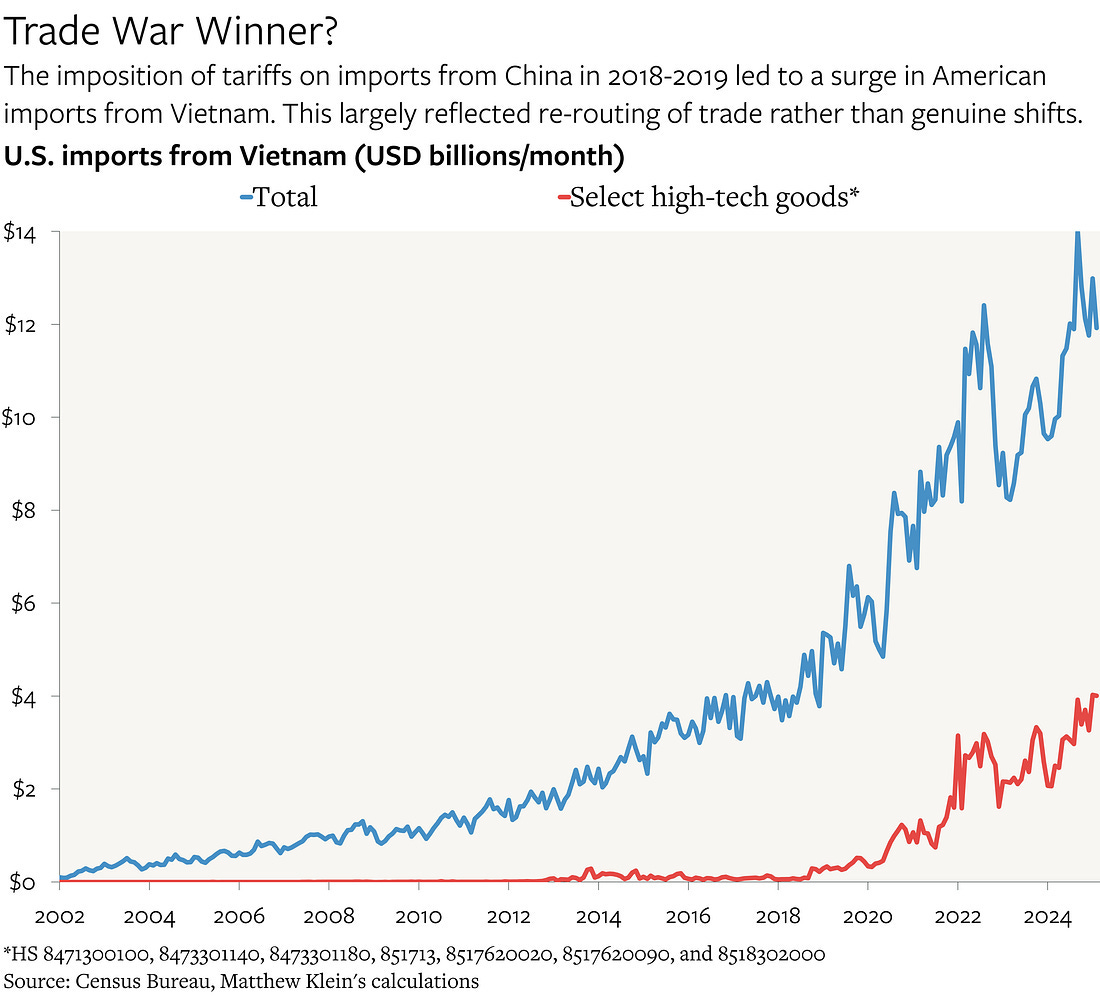

Tariffs are still the main public policy consideration (at least as of this writing) and while there are a lot of things we don’t know, there are some very useful things we do know, or at least have a decent handle on. Matt Klein ($) provides some important lessons from the last tariff episode.

The main point Klein makes is that trade usually finds a way to happen even when obstacles are imposed. In 2018-2019, tariffs on China were circumvented by directing trade through Vietnam:

The growth rate of U.S. imports from Vietnam surged starting in 2018-2019, which coincides with the first set of tariffs on Chinese goods. This is particularly notable when focusing on a subset of high-tech goods that Vietnam did not export to America at all before 2018, but which now account for almost 30% of the total. At the same time, Vietnamese imports from China also surged by almost exactly the same amount.

As Klein illustrates so clearly, in the 2018 episode of tariffs, Chinese exporters simply adapted and rather than shipping directly to the US, shipped indirectly to the US using Vietnam as an intermediary.

This story is actually not very different from that of sanctions. After the Russian invasion of Ukraine, sanctions were placed on Russian oil. That didn’t mean Russian oil stopped flowing; it just meant it flowed to different places and through different channels.

Indeed, this is the conclusion Klein reaches in regard to the new tariffs: “Despite the apparent best efforts of policymakers in both countries, trade between China and the U.S. is likely to persist.” That’s what happens when there are good economic reasons on both sides for it to persist.

That said, good economic reasons can be overwhelmed by bad geopolitical reasons and this may be one of those times. Nonetheless, the base case expectation should be more moderate than the rhetoric at either extreme. Indeed, this was borne out to a large extent with Scott Bessent’s comments on Tuesday.

Investment landscape I

Recoup Deville, Almost Daily Grant’s, Monday, April 21, 2025

https://www.grantspub.com/resources/commentary.cfm

Retail doubles down: The spring selloff has done little to mute animal spirits, with leveraged long exchange-traded funds gathering a net $6.6 billion during the five days through April 11, per a Thursday Bloomberg bulletin. That’s more than double any prior weekly haul over the past two years and roughly ten times the sum flowing to bearish-biased products. Thanks to an influx of fresh cash, shares outstanding across the 50 most popular leveraged ETFs jumped 20% from the April 2 “Liberation Day” through the end of last week, Citigroup-compiled data show.

“Amongst our most active traders, we see a willingness, if not eagerness, to embrace the volatility in hopes of maximizing their profit potential,” Interactive Brokers’ chief strategist Steve Sosnick told Bloomberg, noting that six such leveraged vehicles ranked among the platform’s top 25 most actively traded assets last week. “There’s a generation of investors who have become quite willing to accept risk.”

While market volatility may be unsettling for a lot of investors, a group of retail investors is doubling down. Not only does money continue to flow into stocks, but it is doing so via the most speculative leveraged vehicles available.

Clearly, this behavior has been an element in the massive market swings this year and clearly it is predicated on some notion that markets will not be allowed to stay down. For now, it’s good to be aware that animal spirits are still percolating. It will be interesting to see what finally causes the capitulation.

Investment landscape II

Donald Trump vs Mr Market ($)

https://www.ft.com/content/e7143a09-b280-4fd5-9efe-2d8684b4294f

The sheer uncertainty is disastrous for the real economy, too. Corporate decision makers would like to get on with the making of decisions. Should they redesign their supply chains? Relocate production to avoid tariffs? Shut down some operations and sack their staff? Start building and hiring elsewhere? For now the only reasonable response is to hold on tight to the giant mahogany desk in front of them and pray the world stops spinning.

This is the paradox, then: stock market investors are cautiously optimistic because they expect that Trump is going to change his mind; physical investments are on hold because people are waiting to see what will happen after Trump changes his mind; and bond market investors are nauseated because Trump keeps changing his mind.

A couple of interesting ideas come out of this FT piece. First, it is fairly clear that investors and CEOs alike have become acclimated to following the lead of policymakers as a key to their decision making. No doubt there is good reason for this: Business and economic data falls out from the direction set by policymakers. For many years it was the Fed telling markets what to do. Now, it is the president.

This lesson was probably reinforced in the early days of Covid. The early responders to economic slowdown ended up being the losers of market share when the Fed introduced vast amounts of liquidity and the government jacked up fiscal spending to cushion the economic blow. Anyone who lived through that knows better than to react to data before knowing the policy response.

Unfortunately, the “wait and see” reaction function may have been a bad lesson to learn. As the economic environment becomes increasingly fragile, and government finances become increasingly precarious, it’s not at all obvious that government or monetary officials can do much to boost the market, even if they wanted to. That means a lot of companies will be slow to react when business turns down and therefore vulnerable to significant harm.

Investment landscape III

Market excitement this week focused on a very weak start coming off the Easter holiday, a strong finish into the close on Monday, and then another push upward on Tuesday on comments from Secretary Bessent. Part of the rebound was probably based on the moderation of some of Trump’s more disruptive ramblings of late. Part of it was probably also narrative management.

The bigger question for investors is whether the rebound signals something of an “all clear” message to re-engage in risk or whether it is simply a pause in a bigger dynamic. Endgame Macro posted on exactly this subject:

This [yield spread between US Treasuries and German Bunds] isn’t about chasing yield. It’s about perceived safety. With the Dow suffering its worst April since 1932 and U.S. markets flashing volatility and funding stress, investors are reallocating toward what they see as more stable sovereign collateral even if it pays less.

This divergence is a reputational alarm. When capital starts treating Bunds as the safer haven over Treasuries, it reflects a deeper trust shift in the underlying monetary architecture. The message is clear: capital is preparing for systemic dislocation, and it doesn’t want to be trapped in the wrong sovereign paper when the next liquidity freeze hits.

This is an extremely important point. The spread between US Treasuries and German Bunds is one of many signals that Treasuries are losing their appeal as a store of value and a risk-free asset. The rise in gold prices is another indication. In short, there is something much bigger going on than whether stocks are up or down on the day.

This phenomenon is important in not just quantitative, but also qualitative terms. Endgame Macro describes it as a “credibility fracture” and says, “This is what it looks like when trust begins to unwind at the sovereign core.” In another post the change is described as “a trust rotation not just out of risk assets, but out of the very institutions that once anchored global stability.” In yet another post, the shift is described as “not about replacing the USD as a medium of exchange. It’s about replacing the U.S. Treasury as the trusted store of value in global reserves.”

Clearly, the shift away from US Treasury bonds as a global store of value is a monumental shift. As such, it has enormous potential to be disruptive. Unfortunately, as with any major shift, like a broad-based margin call, it does not pay to stick around. Also, unfortunately, once the process gets started, there is no turning back.

Implications

It’s hard to capture the importance of severe market dislocations beforehand. Call them a regime change and you sound unnecessarily alarmist. Treat them as run-of-the-mill volatility events and you understate the enormous potential impact on portfolios for years and years to come.

Perhaps one way to appreciate the enormity of risk in US financial markets right now is to re-assess the assumptions underlying them. Most investors will probably look at things like earnings growth and inflation risks. While these are important factors, there are others that are even more fundamental.

One of those is the US dollar (USD) and the other is the depth and liquidity of the market for US Treasury bonds. US investors have simply not had to worry about USD debasement significantly undermining their purchasing power. Nor have they had to worry about bond yields blowing out (at least not in several decades) and crushing the valuation of financial assets. Take those assumptions away, however, and you start getting a picture of how transformational the upcoming changes are going to be.

Of course, there will be efforts to manage the process. Of course, the path and the timing will be unknowable to a large extent. However, once the process starts, there will be no going back.

That means if you are not extremely comfortable with your level of risk exposure, you need to act NOW. If you are comfortable, and have a fair amount of liquid assets, you can start war gaming the types and amounts of risk you might want to add at much lower prices in the not-too-distant future.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.