Observations by David Robertson, 5/13/22

It was another crazy week with stocks falling, bonds rising, and cryptocurrencies imploding. Let me know if you have questions or comments at drobertson@areteam.com.

Market observations

The week started off with a brutal selloff on Monday leaving the S&P 500 down 3.2%, but bitcoin was the real dumpster fire dropping 10.7%. Things chilled on Tuesday and on Wednesday the CPI disappointed coming in slightly lower than March but higher than expectations. Stocks resumed their slide as most of the crypto eco-system started caving in on itself (see below).

Another interesting observation by John Authers at Bloomberg reiterates just how much the business environment has changed from Covid lockdowns. It compares the performance of physical retail stalwart WMT to online phenom AMZN. Since the end of last year WMT has kicked butt. A big part of this for sure is simply the reversal of gains by AMZN and other lockdown-friendly businesses - but wow, what a turn.

Commodities

"A Recession Is Necessary" To Lower Demand As 'Real Economy' Routed By Soaring Fuel Prices

If you are the owner of an oil refinery, then crude is trading happily just a little above $110 a barrel - expensive, but not extortionate. If you aren’t an oil baron, I have bad news: it's as if oil is trading somewhere between $150 and $275 a barrel.

The oil market is projecting a false sense of stability when it comes to energy inflation. Instead, the real economy is suffering a much stronger price shock than it appears, because fuel prices are rising much faster than crude, and that matters for monetary policy.

Commodities got hammered on Monday and the beatings continued on Tuesday. This unpleasant event suggests something material has changed in the space. The most obvious and probably cause is a re-evaluation of likely economic growth in light of continued Fed tightening.

Regardless, the reversal provides occasion to review some tenets of commodities investing. One is that stocks are often high-beta versions of the underlying commodity and therefore are even more volatile and likely to overshoot in either direction. For example, even with significant supply threats due to Russia’s invasion of Ukraine in late February, uranium miner CCJ is now just flat year-to-date. Copper miner FCX is down year-to-date.

Another lesson is that one can be right on commodity direction but still wrong on the investment vehicles selected. Part of this is due to the inherently complex nature of global manufacturing and logistics systems and securities markets and part is due to unpredictable public policy responses.

Javier Blas highlights one timely example with the differential between oil and gasoline. While oil prices are higher than last year, it has been refining margins that keep breaking records. As oil has sold off this week, refining margins have remained high. This also creates another problem: The differential complicates the job of trying to benefit from commodity trends (who benefits more - producers or refiners?) and also understates the economic harm caused to consumers. Never a dull moment.

Credit

Credit markets shudder ($)

https://www.ft.com/content/a87b2af7-885f-40b8-9f35-3e6951230615

In the start of the Fed hiking cycle, it’s essentially a sweet spot [for leveraged loans] . . . The difference this time is three-fold. One is that the market has a lot of low-quality debt. The second is that the Fed is moving so fast, it’s unlike anything we’ve seen recently . . . . And the last point is [many lowly rated companies in] the B3/B- cohort . . . are loan-only or they’re more dependent on floating-rate structures.

You will notice that Gleysteen [who is more sanguine about credit] is reassured by equity-heavy capital structures, while Mish [who is quoted above] is worried about loan-only ones. Part of the disagreement may boil down to the fact that the two analysts watch different companies. As is often the case with credit, no one person has the whole picture. Much of the riskiest lending in this cycle has been done in private markets. We won’t know for sure how vulnerable the market is until something breaks.

While credit weathered the start of the year in fairly good shape, cracks are increasingly beginning to appear. The first quote is a good synopsis of the key headwinds. The second quote, by Armstrong and Wu, is a good reconciliation of the “Pro” and “Con” views on credit - the view depends a lot on which companies one focuses on.

One key point is that a lot of poor credit relies on regular re-funding. Another key point is that a lot of poor credits fly under the radar in private equity structures or in other places outside of public scrutiny. As a result of this landscape, the probability of credit problems quickly becoming nonlinear (i.e., lots of bankruptcies) is quite high.

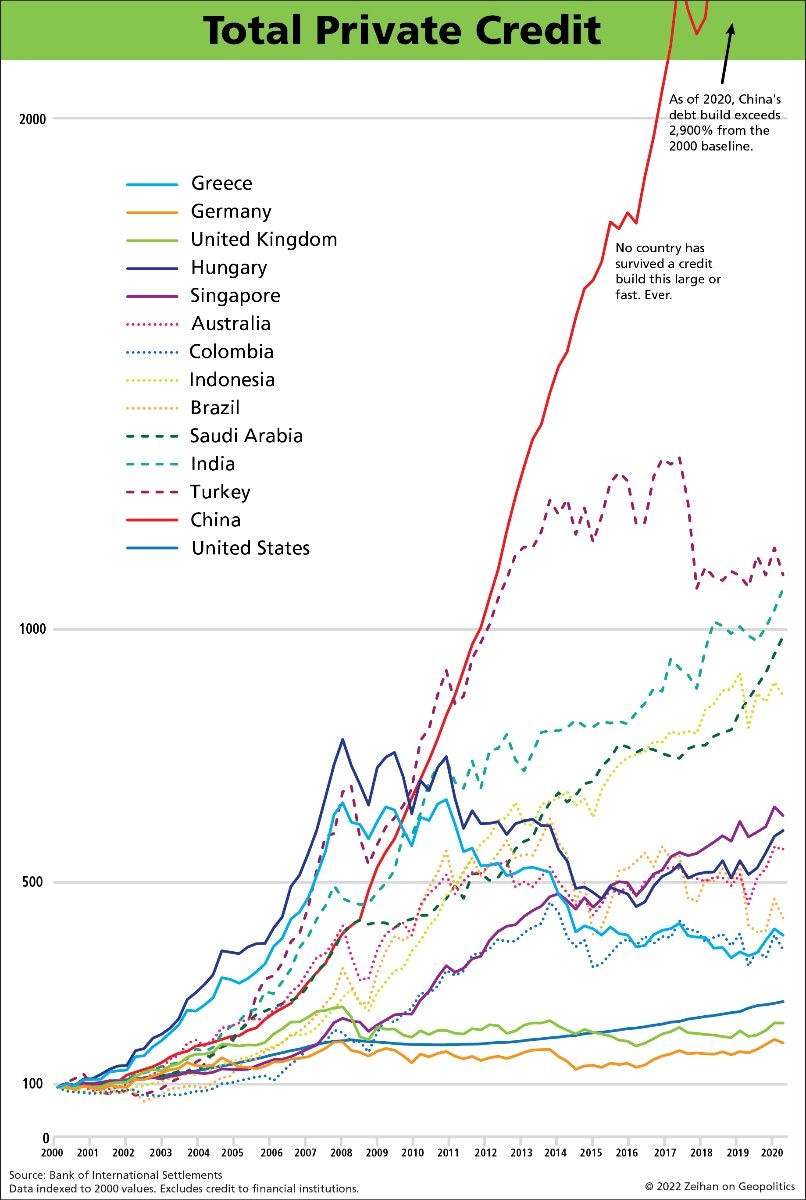

Credit, and the End of the World

https://us11.campaign-archive.com/?u=de2bc41f8324e6955ef65e0c9&id=7e1cf6645f

The absolute financial blowout that is China has generated the largest and most unsustainable credit boom in human history both in absolute and relative measures. The Chinese will exit the modern world just as they entered it: with a big splash. The only question is when.

Peter Zeihan reminds us that the great credit explosion of the last two decades was not just a driver of the huge boom in private equity but also a driver of markets worldwide - especially emerging markets. As credit tightens, the effects will be felt far and wide. Housing in Australia, for example, is a big risk, and China (solid red line) is the biggest risk of all.

Geopolitics

The Russian invasion of Ukraine has ignited debate on the subject of globalization. While Russia’s aggressive actions deserve special consideration in regard to sanctions and other policy measures, frictions in global trade have been evident for years. Properly diagnosed, many of the problems and imbalances related to globalization are ultimately a function of inequality.

This is a point Raghuram Rajan makes in the FT article and also one that Michael Pettis made with Matt Klein in their book, Trade Wars are Class Wars. One takeaway is that in order for global imbalances to change, the underlying cause must be addressed rather than the subsequent symptoms. In short, the most sustainable way to reduce large export surpluses in countries like China, Russia, and Germany is for those countries to facilitate redistribution of income such that their own populations can afford the products they produce.

Relatedly, another element of this puzzle which Rajan addresses is simply having a plan. While planning seems like such a waste when times are good and the wind is blowing at your back, it is essential for providing focus in times of need. In the absence of more thoughtful policies toward globalization, growth around the world will suffer but conditions in emerging markets could become disastrous.

On a separate but related topic, the Russian invasion of Ukraine forced a lot of companies to decide quickly whether to continue doing business in Russia or not. Mostly that was a relatively easy call since Russia acted so badly and public sentiment was so strongly in favor of Ukraine.

Now that the initial fervor has dissipated, the equation has changed. The US government is outlining new policies to ensure national security which naturally include restrictions on the export of technologies to hostile or potentially hostile countries. At the same time, many tech and industrial companies want to ensure long-term business growth in countries like China and Russia.

This is going to be a tougher tradeoff for companies to make. Thus far the majority seem to be sticking with the profit motive at the expense of national security. From the perspective of Klon Kitchen, however, the decision is clear: “we can and should hold companies accountable when they knowingly and materially improve our rivals’ ability to kill Americans.” I suspect this will get a lot more visibility in coming weeks and months and will also force consumers and investors to make tradeoffs as well.

Monetary policy

The real fed funds rate reveals who US central bankers are ($)

https://www.ft.com/content/dc8c38f9-d1f2-4340-bee4-81141244a283

That current hard versus soft landing debate though seems a false dichotomy. A third outcome might be that the Fed does not act vigorously enough to force any cooling of the nominal economy and inflation lasts longer than the current consensus.

The Fed wants to be viewed as a conscientious inflation fighter but the extremely negative real fed funds rate says otherwise. Despite the Fed’s jawboning, they are what their real fed funds rate says they are.

This is a bit of a hot button of mine and Richard Bernstein is spot on: The Fed wants to be viewed as your friend but in actuality it is neither competent nor friendly. It is a hot button because it is disingenuous - and that disingenuousness poses an enormous risk to investors.

I understand the politics and I understand that it does not behoove leaders like Powell to be overly dramatic about negative consequences. At the same time, however, it isn’t right to be considerably less than truthful or to grossly understate risks either. The more you believe Powell’s pledge to fight inflation and protect American citizens, the more you are likely to get hurt.

Investment analysis

Soft Now, Hard Later

https://www.mauldineconomics.com/frontlinethoughts/soft-now-hard-later

“What that shows, I think, that is so easy to ignore in this field is that good investing is not about what you know, it’s not about how smart you are. It’s not about where you went to school. It’s not about the connections that you have. Good investing is overwhelmingly just about how you behave. It’s about your relationship with greed and fear, how gullible you are, who you trust, who you seek your information from, your ability to take a long-term mindset, long-term time horizon. That’s what actually matters. That’s what moves the needle more than anything else.

“And all of those topics are not analytical. They’re not about data and formulas. All of those topics are behavior, and behavior is kind of a soft and mushy topic. That’s not analytical. You can’t summarize it on a spreadsheet or with a formula. So it tends to kind of be ignored in investing, even if it is one of the most important aspects of investing.”

I have a label in Evernote called “wisdom-investment” to capture smart nuggets of insight when I come across them. This quote from Morgan Housel at the Mauldin Strategic Investment Conference fits the bill perfectly.

One aspect is the de-emphasis of analysis. While I have been an analyst my entire career and deeply value the exercise, it is also important to recognize that analysis is not what has the biggest effect on investment returns for most people most of the time. The answer to that is behavior, or if you prefer, temperament.

I think Housel’s comments are especially important in a digital age with pervasive social media. It is so easy to get access to numbers and analyses and it can be extremely tempting to use them. In this sense, analytics are not unlike guns; quite useful in the hands of people who are well trained to use them and well aware of the risks, and extremely dangerous in the hands of people who aren’t.

Indeed, this brings us back to temperament. It is people who know the risks and shortcomings of data and models and actively question them that can make the most use of them. One of the most common patterns I see in the investment world is people who are technically competent making bad decisions because they overweight the importance of analysis and fail to adequately check behavioral tendencies like greed and fear. The good news is that most investors can do quite well simply by administering a healthy dose of common sense.

Cryptocurrencies

Cryptocurrency TerraUSD Falls Below Fixed Value, Triggering Selloff ($)

One type of cryptocurrency, a so-called stablecoin, is meant to keep its value at $1. But on Monday, the third-biggest stablecoin, TerraUSD, fell as low as 69 cents, causing a flood of investors to sell their holdings.

But unlike traditional stablecoins, TerraUSD is an algorithmic stablecoin. These pseudo dollars aren’t necessarily backed by any assets at all, instead relying on financial engineering to maintain their link to the dollar.

So, one interesting aspect of Monday’s wicked selloff was a problem in the cryptocurrency markets. I’m not going to make any pretense of being a crypto expert here, but I can comment on some general mechanisms and their commonality with, and relevance to, traditional financial markets.

First, stablecoins are like money market funds in that they are expected to maintain a base value. Break that and you break the entire proposition. Imagine looking at your brokerage statement and rather than finding the full amount in a money market fund there, you see a total that is 30% less than it should be. Very big deal.

Second, just like with other assets, a drop in value can ripple through and affect other assets. This can happen by way of reduced collateral value like it did with subprime mortgages in the financial crisis. It can also happen by way of forced selling when it triggers margin calls. In both cases seemingly small niches can infect markets much more broadly.

Third, the whole case reveals so much about cryptocurrencies in general. On one hand, I applaud the cleverness and experimentation being applied to discover better financial services. On the other hand, crypto projects are rife with arrogance and righteousness that often prevent interesting ideas from becoming useful solutions. For example …

A $3.5 billion bet on bitcoin becoming a ‘reserve currency’ for crypto is being put to the test (h/t @donnelly_brent)

https://www.cnbc.com/2022/05/09/what-is-terrausd-ust-and-how-does-it-affect-bitcoin.html

“This assumes normal market conditions,” said David Moreno Darocas, a research analyst at CryptoCompare. “During periods of high volatility and one-sided buy/sell activity for UST, the above stabilizer may not be sufficient to maintain the peg in the short-term.”

This story reminds me of the business world when the CEO decides to invest a lot of money beefing up the company’s IT, but does so without the close collaboration with business leaders. You end up with technically sophisticated applications that are often incomprehensible and useless to the business units.

If you want to dig in more, Jim Bianco was early in flagging the problem on Twitter, jonwu.eth put out a good explanatory thread there as well, and Zerohedge posted a nice summary on Tuesday and another one on Wednesday. Almost Daily Grant’s also contributed to the discussion on May 10, the SEC chimed in, Jim Bianco reported on Thursday that the problems are metastasizing, and Ethan Wu ($) provided a nice summary on Friday.

Investment landscape

Dara Khosrowshahi's memo yesterday calling for a focus on profits over growth and free cash flow over adjusted EBITDA is an important event: it's a signal that the current tech industry downswing is transitioning from a trend deviation to a new trend that will feed on itself for some time.

But speculative froth at the level of one company can translate directly into the fundamentals of another company in its supply chain. That's been great news on the way up, and it will be painful on the way down. One of the first Diff posts, back in February 2020, was "One Company's Net Dollar Expansion Is Somebody Else's Lower Gross Margin." It was a hypothetical concern then, but it's a real concern now.

One of the hardest aspects of running any business, and especially that of a startup, is running full out in one direction, and then having to suddenly change direction - and run full out in that new direction. This is often referred to as a “pivot”. While this normally refers to a change in business strategy involving products or markets, for example, the dynamics are the same when it addresses a change in the landscape.

To this point, Uber’s CEO sent out a loud signal to his workforce that the landscape has changed and the company’s priorities need to change with it. He is right. Out with growth and in with free cash flow. This will change the types of projects the company funds, the strategic priorities, and even the types of people who are successful there.

This is a message almost every CEO should be sending out right now.

One of the key elements of change in the landscape is inflation and supply chain issues. Javier Blas has done an excellent job reporting on commodity markets and the news is grim: We are on a path to such intense shortages for certain products like diesel and gasoline that some filling stations may run out over the summer.

To be sure, this is not end of the world kind of stuff because it does not suggest refined oil products will stop being produced. It does suggest, however, that more planning will be needed. Gas may not be readily available on long road trips and deliveries that rely on trucking may be late or forestalled indefinitely. Good luck!

Implications for investment strategy

With so many forces roiling the markets currently the number one priority for long-term investors is to realize the investment landscape has changed and become far more challenging. The number two priority is to hunker down. If you were well prepared beforehand, congratulations. If not, there is still time to adjust risk exposure to a level you can be comfortable with.

Finally, priority number three is to start doing the work and preparation for what comes next. A big hint is that it will not be a “return to normal”.

Thanks for reading!

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.