Observations by David Robertson, 5/31/24

There wasn’t a lot of news in the holiday-shortened week, but with stocks remaining near all-time highs, there was plenty to think about. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Commodities have gotten some more attention lately as various metals such as gold, silver, and copper have made big moves. Mostly, this has been relegated to polite side conversation, however, and nothing remotely as headline-worthy as artificial intelligence. Nonetheless, commodities have quietly been performing quite well:

It is interesting that for all the attention on stocks and all the concern about commodities, GRHAX has handily outperformed the S&P 500 over the last one, three, and five year periods. It may not be Nvidia, but it’s not nothing either. I suspect a lot of investors would be surprised by this.

Now, there are some caveats. The Goehring & Rozencwajg Resources fund (GRHAX) is just one commodities fund of many and mostly holds stocks that focus on mining and resource development. Second, funds focusing purely on commodities positions rather than stocks have not done as well. As a result, GRHAX is a less than perfect representation of commodities in general. It is a real fund, though, and absolutely does reflect what is going on in the commodity space.

I have commented several times in the past that it can be very difficult to time the addition of commodities to a portfolio because they are so volatile. This remains true. What is also increasingly evident, however, is the multitude of drivers for monetary debasement. There is always risk involved and increasingly one of those risks is not being protected against inflationary pressures.

Public policy

Brad Selzer’s post on China fx rates reveals an interesting insight about China’s policy making:

Exceptional piece by Guo Kai of the China Finance 40. Bottom line: to introduce real two [way] risk (and volatility) into the yuan/ dollar, the PBOC occasionally needs to signal that it wants a stronger yuan (i.e. a rebound)

This effort to introduce two-way risk is especially interesting given that it is being made as structural factors suggest there should be downward pressure on the yuan. The FT reports: “Market pressure is growing on the People’s Bank of China to allow the renminbi to weaken, as traders bet that the yawning gap with US borrowing costs will lead more investors to sell out of the Chinese currency.”

The effort to support the yuan suggests other motives at work. Those include a desire to keep speculators at bay, to provide time for a more gradual transition in currency valuation, to impose some sense of stability in the currency, to favor labor over capital as a policy preference, and to push back on the relatively strong US dollar. Thus far, the policy is having its desired effect: “Analysts are divided on which way the Chinese currency will move next.”

China’s policy stance in regard to its currency also stands in notable contrast to the US where policymakers seem much more comfortable accepting the costs of moral hazard. Efforts to provide liquidity and other forms of support provide the benefit of avoiding problems for some period of time but create the risk that greater disruption will happen later.

At the end of the day, both approaches ultimately accomplish the same thing by forestalling the day of reckoning. Sometimes that delay can be useful and sometimes it isn’t.

As a number of market risks are growing in magnitude, it will be worth watching US policy direction for more signs of incorporating two-way risk. If policy starts incorporating two-way risk on a greater scale, markets can evolve with little disruption. If it does not, then the chances of severe disruption go up.

Technology

While artificial intelligence remains the dominant market theme right now, we are starting to hear some dissonant voices on the subject, and very credible voices at that. First up is Yann Lecun, the chief AI scientist at Meta:

Meta AI chief says large language models will not reach human intelligence ($)

https://www.ft.com/content/23fab126-f1d3-4add-a457-207a25730ad9

Meta’s artificial intelligence chief said the large language models that power generative AI products such as ChatGPT would never achieve the ability to reason and plan like humans, as he focused instead on a radical alternative approach to create “superintelligence” in machines.

Yann LeCun, chief AI scientist at the group that owns Facebook and Instagram, said LLMs had “very limited understanding of logic . . . do not understand the physical world, do not have persistent memory, cannot reason in any reasonable definition of the term and cannot plan . . . hierarchically”.

If it sounds like Meta’s approach to AI is moving in a different direction from most of what we hear in media, that’s not the half of it. Lecun’s “radical alternative approach” involves “creating AI that can develop common sense and learn how the world works in similar ways to humans, in an approach known as ‘world modelling’.”

I find it interesting that the FT describes Lecun’s vision as a “potentially risky and costly gamble for the social media group”. Well, that’s one way to put it. However, every single AI investment right now is potentially risky and costly because it’s never been done before. Further, one of the top minds in AI is acknowledging publicly that much of what companies are trying to do with LLMs and AI is unlikely to work due to their inherent shortcomings. Pursuing projects with such dark omens seems at least as risky and costly.

Another positive, but less than completely ebullient perspective on AI comes from technologist Joe Lonsdale by way of John Mauldin’s newsletter:

Artificially Intelligent

https://www.mauldineconomics.com/frontlinethoughts/artificially-intelligent

“It turns out there's these simple constructs of statistical feedback where when you scale them up, it actually seems to approximate different types of intelligence really well. These are called large parameter models, or on [just] words they're called large language models, and it's basically like an engine that builds many, many abstract layers to predict the next word, the next token… So that statistical engine is the thing we talk about.

“Now most of the time we're talking about AI and it's having a huge impact on the economy, and I think it is important to think of it as a statistical thing, but in some cases it feels like it's reasoning in a lot of areas. You could train it to think in different ways to perform different tasks and we're doing a lot with it right now.”

While Lonsdale is a little squirrely about it, he makes two important points. One is that a large language model (LLM) is best thought of as a “statistical engine”. This is a quiet way of admitting that LLMs operate in a completely different way than human beings do.

The second point is in certain areas, the outcomes from LLMs can “feel like it’s reasoning”. In other words, pure statistical analysis of language can create the appearance of human reasoning activity. This establishes important parameters for where LLMs can potentially be very useful, and where they aren’t likely to be useful, at least not for a long time. This sounds very similar to what Lecun said.

Finally, in regard to the possibility of machines reaching human intelligence (the idea of a “singularity”), Lonsdale was more reserved than many others:

“And I think a lot of people who are in the field think there's a good chance it [singularity] gets there in 15 years, and it's a possibility. My bias, John, is the world doesn't go in these singularity exponentials very often. I think the world moves in S's. I think things change quickly and then they level off for quite a while, and they change quickly, and they level off for quite a while. My guess is that God didn't build quite as simple of a universe as some of these computer scientists think and that there might be multiple more S's still to go.

Finally, here is some perspective from the front lines of AI (h/t Aakash Gupta, Jesse Felder):

I just left Google last month. The "Al Projects" I was working on were poorly motivated and driven by this mindless panic that as long as it had "Al" in it, it would be great. This myopia is NOT something driven by a user need. It is a stone cold panic that they are getting left behind.

The vision is that there will be a Tony Stark like Jarvis assistant in your phone that locks you into their ecosystem so hard that you'll never leave. That vision is pure catnip. The fear is that they can't afford to let someone else get there first.

This exact thing happened 13 years ago with Google+ (I was there for that fiasco as well). That was a similar hysterical reaction but to Face book.

BTW, Apple is no different. They too are trying to create this Al lock-in with Siri. When the emperor, eventually, has no clothes, they'll be lapped by someone thinking bigger. I'm not a luddite, there *is* some value to this new technology. It's just not well motivated.

Taken together, these three accounts establish a useful and variant perspective on AI. First, there are very useful things AI and LLMs can be applied to that will make a difference. Second, there are also plenty of things AI is not well suited for. This is related to a final point that artificial general intelligence (AGI) is not an imminent or especially useful goal to shoot for.

The fact that these perspectives are out there and getting incorporated into decision making is a sign of maturity from the craze of 2021. The fact that these perspectives are still in the minority suggest there is still a long way to go before the perception catches down to the reality.

Narrative landscape

Last week, Ben Hunt put out this post:

It’s fascinating to me that China is encircling Taiwan as part of a military exercise, the pro-China parties in Taiwan are trying to pass legislation to limit new prez, there are mass protests in Taipei … but not a word of this in MSM.

This certainly resonates with me as many of the things I consider important to the investment landscape I no longer find reported in any meaningful way in MSM. Indeed, part of the reason I started Observations was to at least partly fill this gap by reporting on things I find to be meaningful, relevant, and underappreciated. For a number of reasons, many of these things used to be reported in MSM but no longer are.

MSM often does circle around to stories that are meaningful and relevant, but only after those stories have gained attention on social media and elsewhere. This changes the value proposition of MSM as a trusted and valuable source of information. I have had to evolve my research efforts because of these changes and am often shocked by how little people even recognize this change. I am shocked in just the same way by the number of people who haven’t even heard of Substack yet.

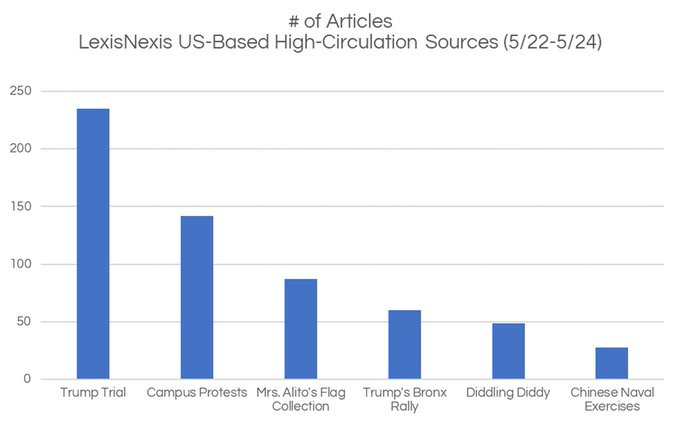

Hunt followed his criticism of MSM with a description of what MSM does report on. He posts a graphic of “the LexisNexis # of articles from US-based high-circulation media sources over the past few days on various topics of crucial national interest.”

This list reveals a couple of important things about MSM. First, as much as anything, it has become singularly focused on entertainment. Second, and largely as a result, it has become deeply unserious about prioritizing real news. Rather, it provides a regular assortment of trivialities and distractions.

As such, MSM has become equivalent to McDonald’s in the food world. It’s relatively cheap, easy and convenient. It will get you through to the next meal. But if you’re looking to get in shape or at least be fairly healthy, you’re looking in the wrong place.

This is probably obvious to a lot of people, but there are still a lot of people who rely on MSM based on habit, if nothing else, and a lot of it is generational. Nonetheless, different approaches to news and information can easily lead to very different views of the world.

Investment landscape I

Due to the holiday shortened week, auctions of US Treasuries were especially dense. Both the auctions of 2-year and 5-year Treasuries on Tuesday were weak and yields rose as a result. The 7-year auction on Wednesday was not quite as weak but still subpar.

In what is becoming a familiar pattern yields fell in the days prior to the auctions, this time in front of the three-day weekend. When it came time for real money to be put to the test at auction, however, greater trepidation and higher rates were the result. All three auction posted yields higher than the when-issued yield immediately before the auction which suggests a difference between futures markets and real money demand.

One observation is that risk appears asymmetric to the upside on rates. Another observation is this is yet another case of misplaced priorities in news coverage. While journalists are tripping all over themselves about Nvidia and artificial intelligence, the most important story for the market right now is rates. On that subject, there is barely a whisper.

Investment landscape II

The case of the fragile 27% ($)

Grant’s Interest Rate Observer, MAY 24, 2024

“Commercial Real Estate and Bank Systemic Risk,” the title of a new working paper by Paul Kupiec, a senior fellow at the American Enterprise Institute in Washington, D.C., makes the case for concern in 61 closely argued and copiously documented pages.

Taken together, says Kupiec in summary, the bear market in commercial real estate, the zero-percent-to-5%-plus moonshot in the federal funds rate and the high concentration of troubled CRE assets in too many bank portfolios have created “significant systemic risk.”

Commercial real estate (CRE) continues to be the simmering problem that takes ever-so-long to come to a boil. Because this measured cadence is not especially attention-getting, it is easy to exaggerate the risk of CRE in both directions. On one side, it has been easy to understate CRE risks since there haven’t yet been any major disruptive blow-ups. On the other side, it has been easy to overstate CRE risks based on current rates being much higher than the rates on many existing CRE loans. Time and access to alternative forms of borrowing have alleviated the pressure thus far.

For the time being, it’s important to remember the CRE risks are still out there and still to be felt to their fullest extent, whatever that may end up being. At very least, banks are going to be feeling some pain. Grant’s sums up:

With all that said, the message of Kupiec’s study is indisputably bearish. It shows, to start with, that many hundreds of banks are overextended in commercial real estate of whatever type. And it reveals that the post-2022 lurch higher in interest rates has impaired the capital that exists to absorb the potential losses of those at-risk assets. What the study mentions, but does not explore, are the risks to property owners that high refinancing costs will impose.

As to those refinancing costs … time is running out on the potential for rate cuts to enable economic refinancing. When properties start failing to get refinanced on economic terms, there will be better price discovery and those prices will be down. Not a disaster, but not even remotely over yet.

Implications

While the narrative of AI remains quite strong and dominates financial news, tech stocks are looking toppy, long-term rates are working their way back up and commodities have remained strong. In short, it looks like the market might be reaching some kind of tipping point.

What might that tipping point portend? One possibility that I don’t believe is very likely is a crash. Yes, valuations are excessive, but liquidity is high, flows keep coming in, and authorities have a lot of levers to pull to prevent a melt-down. This will change over time but does not appear to be a big risk now.

That said, it wouldn’t be surprising at all to see a significant change in leadership in the market. Tech stocks are due for a breather, inflation continues to prove stubbornly high, and a lot of cyclical and commodity stocks are just not very expensive, especially relative to the big tech stocks. If growth starts picking up again, these stocks could catch a big tailwind going into the end of the year.

Thursday’s results give some indication of what this might look like. Perennial tech standout Salesforce dropped 20% on good but less than stellar results while stodgy old Hewlett Packard rose 17%. Dell, which has been gaining attention for growth in AI servers, was down 16% premarket due to lower than expected growth in that market.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.