Observations by David Robertson, 6/10/22

The jobs report and Target’s second guidance adjustment in a few weeks made news and while these provide some color about the economy, there is an eerie sense something much bigger is developing in the background. Let me know if you have questions about the market or would like some more perspective at drobertson@areteam.com.

Market observations

For the last couple of weeks stocks have bounced around without making a lot of headway one way or the other. During that same period, however, volatility has continued to decline.

This has created an environment conducive to a brief risk rally - and that is exactly what has happened. Riskier funds like Krane’s China Internet Fund (KWEB) and the ARK Innovation Fund (ARKK) have outperformed.

During that same period, however, longer-term interest rates have started creeping back up as well. Like a dark storm cloud on the horizon steadily moving closer, the 10-year yield has risen from a local low of about 2.72% in late May to over 3% again this week. It may take a little time for this warning signal to reach risk takers, but it will.

Another warning signal is going off in currency markets. The Japanese yen continues to weaken considerably and this is unusual for a major currency. Japan continues to loosen monetary policy while the rest of the world tightens. This is exactly the kind of divergence that can cause major quakes in asset markets.

Economy

Employers are still raising pay to attract workers, but they’ve chilled out a bit. “Firms seem to be less willing to raise wages sharply in order to fill openings than they were last winter,” as Peterson analysts put it. That’s not pleasant for the individual worker looking for a boost to the old paycheck, but it’s a good sign that the economy overall remains robust but not berserk.

Last Friday the jobs report came out and got a lot of attention to start this week. The Dispatch ($) summed it up well: The number itself was good, but not excessively good. We’re getting back close to the employment levels before Covid, although the composition of jobs has changed a fair bit. All in all, the report did not add a great deal to the market calculus, but it did reveal a number of important characteristics of current market dynamics.

One of those important characteristics is the Fed’s focus on jobs. As Robert Armstrong and Ethan Wu reported, The Fed cares about job openings, and so you should too ($). Clearly, the Fed wants to anchor attention on jobs so as to justify monetary policy - namely continuing to tighten to fight inflation.

Clearly too, it is intellectually vacuous to use just one metric to guide policy in an economy as big and diverse as that of the US. This just reinforces the notion that the jobs target says more about what the Fed wants to happen than about the economic landscape. In short, the jobs target probably gives the Fed more room to tighten than a more comprehensive economic assessment would.

Another aspect of current market dynamics is the continued effort to characterize the economy and markets in a positive light. While I understand a lot of readers of paid publications don’t want to hear bad news, extending such great efforts to justify a “soft landing” and to avoid discussing the consequences of a serious bear market strike me as a disservice to investors.

The cold hard truth is the markets are most likely to be extremely difficult for quite a while (i.e., more like years than weeks). It is far better to act on this before it is widely accepted than after.

Credit

If you look at the last year and a half of revolving consumer credit in the FRED database you see an acceleration off the bottom at year-end 2020. This graph has been making the rounds as a justification that the consumer is tapped out and therefore is resorting to credit cards as “bridge” financing.

If you look at a slightly different series, however, that focuses on revolving credit from commercial banks, you see a slightly different pattern. Growth also accelerated off a low at the end of 2020, but began slowing visibly at the end of March and has been nearly flat since the end of April.

What gives? One hypothesis is that banks may have started tightening credit whereas their nonbank competitors have continued swiping up loans. If that is the case, many nonbank consumer lenders are increasingly exposed to adverse selection and likely vulnerable to growing credit risks.

Another hypothesis is that bank credit cards are more reflective of overall consumer behavior than the securitized consumer credit series. If that is the case, consumers aren’t so much tapped out as simply normalizing growth after a rapid return to pre-covid levels of revolving credit.

Either way, it is clear higher prices for shelter, food, and, gas, among others, are hurting a lot of consumers. It is not clear, however, at least not yet, that consumers are broadly resorting to credit cards to cover those cost increases.

Commodities

The prices of oil and oil products continue to do well as inventories flirt with new seasonal lows. Especially troubling for gasoline is that there is normally a period of building inventories in the late spring which has not been experienced yet. If such a build does not happen this year, expect even lower inventories and higher prices.

This is the type of evidence that fuels ever-higher oil prices, but there is contravening evidence as well. For one, insiders of energy companies have been selling shares like they are going out of style. For another, in general, commodities follow the path of Chinese industrial activity - and lately that has been down.

Finally, commodities are notoriously volatile and subject to massive swings. While I am always reluctant to place too much weight on historical analogies, the comparison below by Javier Blas gives a good indication of not only what can happen with oil, but also what actually has happened.

None of this is to say there aren’t good arguments for commodities though; there are. One of the better examples is outlined in a nice thread by @PauloMacro. The thrust of the argument is step-function higher oil prices resulting from Russia’s invasion of Ukraine increased margins and forced many traders out of the market. As a result, trading has become far less liquid which means price discovery is not robust.

I think there is a lot of truth in this framework, but I also think it lends itself more to some well constructed trades than it does to long-term investments. I can say I believe in the theory enough to be extremely cautious regarding the negative impact of higher energy prices on company margins and discretionary consumer spending.

Inflation

The inflation report came out on Friday morning and garnered a lot of attention - and for good reason. Many market watchers were looking for a decline as further evidence inflation has peaked. Others were concerned inflation would remain high, and perhaps even increase further, which would put enormous pressure on the Fed to continue tightening aggressively.

The numbers came in hot. The overall CPI increased 8.6% for the year which was an increase from last month, and 1.0% sequentially, which also was a big increase. The report characterized increases as “broad-based”.

A good synopsis by Zerohedge reveals headline CPI has now “risen for 24 straight months”. In addition, accelerating prices for services are taking over for past price increases for goods. Finally, shelter, which tends to be a sticky part of the inflation equation, is “accelerating dramatically”.

The bottom line is inflation is not going away easily or quickly. That means the Fed will have to continue pressing and that means more headwinds for asset prices.

Monetary policy

No Soft Landings

https://www.mauldineconomics.com/frontlinethoughts/no-soft-landings

“My real worry on the downside is that it may be that the fragilities are so great at the moment that a moderate degree of tightening will in fact spark a downturn of such a magnitude that even if the Fed does back off, that there's not much that can be done about it, that will have a downward momentum... that we really won't be able to handle.”

One of the exceptionally few voices to have understood and foreseen many of the problems of the financial crisis in 2008, Bill White, spoke at John Mauldin’s conference recently and made waves with his comments. In short, he noted, “the banks are weaker than many think,” and as such, the threat of a debt deflation is very real.

With many investors singularly focused on inflation, White’s message is an important and timely one. It is true that inflation is a risk and is likely to be more persistent than many realize. It is also true, however, that the financial system is extremely fragile and therefore vulnerable to uncontrolled selloffs.

The Fed and other major central banks have some tools to deal with deflation but are limited in two ways. For one, there is very little the Fed can do if financial contagion strikes again as it did in 2008. By itself it cannot restore confidence. For another, such a situation would force the Fed into a difficult choice: Fight deflation at the risk of igniting uncontrolled inflation or continue vigilance in fighting inflation at the risk of allowing a massive debt deflation.

One main takeaway is that inflation is not the only risk to protect against; deflation is a real risk too. Another is that the two extremely opposite outcomes are joined by a similar cause: The willingness and ability of the Fed to fight one over the other.

Risk management

Given my cautious stance on the markets, risk management continues to be a top priority. This piece by Brent Donnelly fits right in. Although it is oriented more to trading, the principles are the same for everyone and can be easily adapted for long-term investors.

“Don’t blow up” seems like an easy enough principle to follow except for the fact that so many people violate it. Much of the problem is behavioral: People like the returns from a certain stock or fund or sector and become increasingly convinced of its merits. One thing leads to another and before long, a huge proportion of net worth is wrapped up in one investment. This is an easy way to blow up.

Another way way to blow up is when investors think they are far more diversified than they really are. This was a big problem during the financial crisis of 2008. If the vast majority of your investments move together, it doesn’t matter that you have different ones; they all act in sync. This situation can take another turn for the worse if margin calls or panic selling ensue.

One practical point is that experience helps a lot in preventing blow ups. For one, experience reveals the many ways in which blow ups can happen. As such, it provides a vocabulary of setups to avoid. In addition, by providing a view into the negative consequences, experience also provides the motivation to do the hard work of risk management.

Investment landscape

The last couple of weeks has felt light on meaningful news. Part of this can be ascribed to a slower summer pace, but it feels more like the lull before the storm to me.

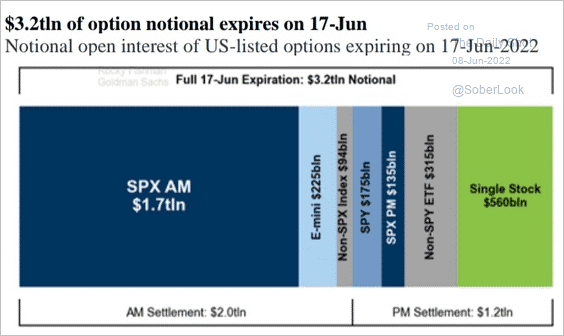

The Fed’s Quantitative Tightening (QT) begins next week on the 15th when some of its Treasury holdings mature. This will drain money from the system and create a headwind for asset prices. Two days later, on Friday, a huge options expiration has significant potential to unsettle markets. Finally, the Russell indexes will rebalance later in the month which will cause a lot of shifting from unprofitable technology companies to energy and commodity stocks.

All of this is happening in an environment of extremely low liquidity. As a result, there is very little ability for asset owners to make big changes to positions without significantly affecting market prices. I wouldn’t be at all surprised if we get some major fireworks before the 4th of July.

Implications for investment strategy

A great deal of commentary the last few weeks has focused on the Fed’s ability (or lack thereof) to engineer a “soft landing”. It is fair to focus on the Fed because its reaction function to whatever the economy and markets produce will be a key factor in determining their future direction.

I continue to believe that it is a useful exercise to consider what part/parts of the market could “break” and how the Fed would react in each case. As I have mentioned before, there are a lot of contenders and virtually all permutations are fair game. The most interesting situations, however, are the ones that would cause the Fed the most anguish - because they would force the Fed to make difficult tradeoffs.

For example, suppose a bank were to become undercapitalized and needed to raise capital in adverse conditions. This shouldn’t be too hard to imagine. Banks are big holders of Treasuries which are trading at much lower levels today than at the beginning of the year. In addition, a tweet posted three months ago highlighted trouble at a fairly large bank. Also, William White is warning about “fragilities” that are beyond the Fed’s control. This is all before considering the potential for worsening credit conditions.

What would the Fed do if a fairly big bank needed capital? If the Fed failed to intervene it could facilitate financial contagion like in 2008. If the Fed acted too aggressively to intervene, it could lose all credibility in its fight against inflation.

The Fed could lie. It could continue to talk about QT while actually scaling it back or reverting to QE altogether. It could break the law. It did in March 2020 when it supported private credit - so there is both precedent for the act as well as for the lack of accountability. The Fed could propose a bank holiday to buy some time.

I’m not the only one with a proclivity for inquisitiveness. Grant’s Interest Rate Observer (June 10, 2022) Wants to know:

How would the Fed react to such an event [of a sudden drain of bank reserves]? How would it react if inflation were still running hot? How would the bond market react if, in response to a destabilizing jolt in money-market interest rates, the Fed restarted QE?

In short, there are a lot of things the Fed could do to manage fairly focused problems, but it would be hard pressed to contrive a broad strategy to manage the situation if conditions forced widespread selling of assets. In addition, any such moves would likely be constrained by the need to consult with the White House first. Finally, just like an aging athlete, the Fed’s strength and agility in a time of need has not been severely tested for a long time. None of these things give confidence the Fed can do much to prevent a painful selloff this time around.

Thanks for reading!

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.