Observations by David Robertson, 6/17/22

The week started off rough and didn’t get much better. This is the part of the movie where the suspenseful music turns up and the audience is on the edge of its seat. Let me know if you have questions or comments at drobertson@areteam.com.

Market observations

After stair stepping down last week, the S&P 500 continued its path downward this week, albeit with a more erratic path. Notably, after the Fed announced a bigger hike on Wednesday than it had guided to from the previous meeting, stocks were up about 1.5%. The next day, all that was given back - and more.

Interest rate moves have also been exceptional. The higher than expected (by many) CPI last week forced a recalibration of monetary policy and market expectations of rates. The longer-term chart establishes a nice perspective of just how much things have changed since the beginning of the year.

As much as the Fed says its actions are predicated on economic activity, it depends a lot which measure you look at. Even though unemployment is typically a lagging indicator, that is currently the Fed’s preferred measure in regard to policy direction. The real-time estimate of GDP, however, tells a different story. It has been languishing for the last month and as of yesterday (the latest reading), the estimate of GDP growth is 0.0%.

Of course, the US economy is extremely diverse and no one measure does it justice. At this point, however, it is a stretch to call the economy “robust”.

Finally, rates in Europe have been making news as well. With the ECB positioning to take its foot off the gas pedal, yields in Italian debt have surged. As John Authers reported, “The growing risk of fragmentation more than counteracted the ECB’s move toward tighter monetary policy on the foreign exchange market, and pulled the euro downward.” The move was enough to prompt an emergency meeting of the ECB, but the result of that only revealed how poorly positioned it is to operate in an inflationary environment.

Housing

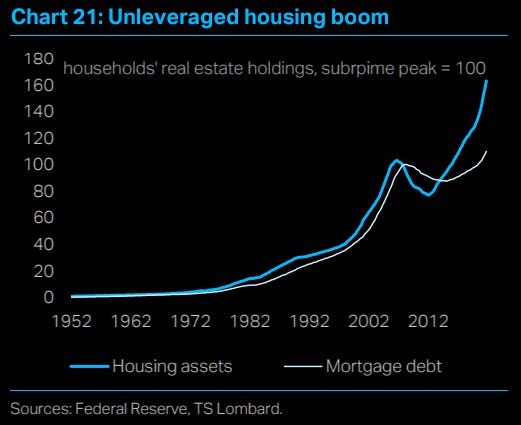

I have mentioned changes in the housing market before but it is a good time for an update. For one, new mortgage payments are skyrocketing in ways they have not done historically. This is due to a combination of (still) rapidly increasing home prices and rapidly increasing mortgage rates. Just eyeballing the graph, mortgage payments are up about 80% in two years.

Another point is that rapidly rising home prices matter because homes are often the biggest asset people have. Further, since home prices have risen so much faster than mortgage debt, houses have also been the source of a huge increase in net worth for many people.

Taken together, these phenomena present significant potential for net worth to get clipped. While it takes time for housing markets to digest such changes and adapt to them, that is exactly what will happen. I don’t anticipate a crisis similar to 2008-2010 since there has not been overbuilding as there was then.

Rather, I suspect the number of transactions will drop significantly until selling prices become more affordable to buyers at current mortgage rates. Indeed, this is already being confirmed by Zerohedge which reported, “real estate brokerage firms Compass Inc. and Redfin announced plans to reduce their workforces amid a housing affordability crisis.” This will make it very hard for families who have to move and very disappointing for young families who are waiting to buy their first house.

Air starts to seep out of the bubbly Canadian property market ($)

Canadians may scoff at such doomsayers. After all, bubble talk is nothing new, with economists blaring warnings since at least 2010. Nevertheless, a comparison between Canada and other rich countries should give rise to some concern. Since 2000 the average house price has more than tripled in Canada; in America, by contrast, it is up by just about 60% (see chart). The median home in Canada costs ten times the median household income, the highest multiple since at least 1980. Within the oecd, a club of mainly rich countries, only New Zealand has seen house prices increase at a faster rate relative to incomes over the past two decades.

In Toronto, monthly mortgage payments at the median home price gobble up an astonishing three-quarters of median household income, according to the National Bank of Canada, a commercial lender. A rule of thumb is that mortgage payments should be just about a third of income. Little wonder that transactions are way down.

Another twist on the housing story is that things are far worse in some other countries. Canada (and Australia, New Zealand, and others), are also beginning to slow down. Those countries, however, never experienced the house price declines of the US in the GFC and therefore currently have higher prices and more burdensome debt loads. While these markets are nowhere near as large as the US, if they suffer anything close to the pain experienced in the US in the GFC, it will be felt elsewhere as well.

Technology

One of the dynamics many investors (and analysts) miss especially about tech companies is the deeply pro-cyclical nature of many parts of the operation. These self-reinforcing feedback loops work in both directions to amplify swings. When things are working, it creates the impression that good technology and smart, hard-working people are out conquering the world. And there is truth in it.

However, just like it can be hard to notice the wind at your back when riding a bike, it can be surprising how much harder the pedaling is when you turn around and head into the wind. In the same way, it can be surprising how much harder business becomes when the company’s stock goes down rather than up.

@buccocapital documents a couple of examples. When your stock is down 50-90%, that presents a huge pay cut for employees who receive stock. This means “you have to work just as hard, but for less money”. The quality of sales leads for reps goes down and the sales cycle gets longer. This creates lots of incentives to go elsewhere to reset your comp. That’s what often happens - and is happening across many companies now.

Of course companies have options to quell the exodus, but none of them are good. They can “Provide a ton more equity to entice reps to stay”, they can “Provide a ton of equity to entice reps, and they can “Shift their comp mix to cash”. Regardless, the companies will either suffer “massive dilution” or much higher cash costs.

It is important to note that while the impetus of the stock decline doesn’t necessarily have anything to do with the business, the exodus it causes will affect the operations of the business. As a result, companies that use stock compensation liberally can easily get caught in a downward spiral that eventually becomes existential.

Gold

One of the points I have been making since I unveiled Areté’s All-Terrain strategy is that the 60/40 (stocks/bonds) portfolio design was about to encounter significant headwinds. That has happened (and continues to happen) in a big way.

While stocks are down this year, arguably the more surprising phenomenon has been the terrible performance of bonds. Since bonds are supposed to be the “safe” part of the portfolio, it begs the question, “What is safe anymore?”

The chart above from @TaviCosta illustrates a useful comparison. Quite clearly, year-to-date, gold has been much safer than bonds.

While this may sound almost sacrilegious to some investors, what it demonstrates more than anything else is the answer to the question, “What is a safe asset?” has different answers depending on different circumstances. In environments of declining rates, bonds can do quite well over long periods of time. During periods of rising rates, however, bonds can get punished.

Monetary policy

A lot of drama surrounded the FOMC meeting as the CPI came in hot last Friday and market expectations for a rate hike jumped soon after from 50 bps to 75 bps despite the Fed being in a blackout period. When it came time to announce, 75 bps it was.

One of Powell’s responses shed a bit of light on the Fed. In response to an inquiry about the rationale for going with 75 bps instead of the guided amount of 50, he said, “We had expected to see inflation start subsiding”. So, here is a Fed that a year ago did not see inflation as a problem at all, and once it finally acknowledged inflation was a thing, thought it would suddenly go away. OK, that’s probably a little harsh, but c’mon, this is the one job they have.

While it is somewhat encouraging to see the Fed finally act to quell inflation, it is disheartening to hear how little it understands about the phenomenon. Given its misses thus far, there is little reason to believe the Fed will be able to get its arms around inflation any time soon - and that means misguided monetary policy will an additional obstacle for investors to deal with.

What the Fed giveth, the Fed taketh away ($)

https://the-blindspot.com/what-the-fed-giveth-the-fed-taketh-away/

The euromarkets do not manufacture dollars, sterling or marks with no reserves at all. But the reserves are chosen by the banks themselves and not laid down by authority. This enables them to pay more for deposits and charge less for loans than their domestic competitors.

The whole euro phenomenon is but one example of the tendency of markets to find a way round official controls; and monetarists who usually proclaim that they are market economists will have to find ways of working with the financial markets rather than against them.

Amid all the drama of the FOMC meeting on Wednesday, Izabella Kaminska made some useful points to help keep investors focused on the important stuff. A big part of the farce of monetary policy is the mistaken belief (yet one the Fed continues to nurture) that the Fed has tight controls over money supply; it does not. The eurodollar market accounts for a large and growing portion of money supply and the Fed has virtually no control over it. This market was an important factor in the GFC and also part of the rationale for Paul Volcker’s historic tightening program.

While new regulations helped tamp down the activity level of shadow banks after the GFC, many of the same activities have been largely replicated in the world of cryptocurrencies. As a result, the recent implosion of cryptocurrency platforms actually serves a useful purpose for the Fed by reducing money supply. It also does so in a fairly quiet, backdoor, way without the need for new regulations or enforcement authority.

A couple of important lessons arise from this. One is that there will always be forces that try to circumvent regulations. Unless and until more thoughtful regulation and more effective enforcement emerge, it is fair to expect this to continue. Another lesson is the Fed does not have total control over inflation. Yes, the Fed can affect markets; no, the Fed does not have tight reins over all inflationary factors. This is a big reason why inflation is likely to be fairly persistent and one that many investors will probably learn the hard way.

Public policy

Policy errors of the 1970s echo in our times ($)

https://www.ft.com/content/d5d68068-d3d7-4948-a13d-b36e8c2b8339

I [Martin Wolf] worked as an economist at the World Bank in the 1970s. What I remember most about that period was the pervasive uncertainty: we did not have any idea what would happen next. Many mistakes were made, some out of over-optimism and others out of panic.

Whether in regard to monetary policy, fiscal policy, or policy from global or regional organizations, Martin Wolf’s comments provide a lot of reasons to be cautious about the efficacy of public policy. In an environment of so much uncertainty, any expectations should be established with wide margins of error. Further, rapidly changing conditions and high levels of uncertainty create ripe conditions for policy errors to be made. This is a good cautionary tale for policymakers to first do no harm and a good cautionary tale for investors that a lot of crazy things can happen.

Investment landscape

In other news … another major central bank (BOJ) is having trouble reconciling its view of the world with reality. Despite herculean efforts to keep its 10-year rate at 0.25%, it has not been able to do so. Although some pricing services suggest the problem is bigger than it is right now (see tweet below), the large amount of attention the issue is getting points to the high level of anxiety it is causing.

Japan matters for a lot of reasons. In a very general sense, it is a large economy with a lot of debt. If it gets into a debt spiral, it will affect other countries, not least of which is China. In addition, Japan’s low rates have encouraged traders to short the yen in order to buy other assets. If/when that unwinds, those other assets would have to be sold - into an environment without a lot of willing buyers. Stay tuned - this could get very “dynamic”.

Implications for investment strategy

With Quantitative Tightening (QT) underway and a couple of meetings of major central banks this week, a couple of points stand out for investors. One is, this is what it feels like when liquidity goes away - get used to it. There is no place to hide. Just about the best you can do is hunker down and wait for the storm to go over. This is not a time to be a hero; hang on to what you can and live to fight another day.

Another point is it is becoming increasingly evident just how out of their element major central banks are. They have the wrong models for understanding inflation. They are institutionally incurious. They don’t even really try to adapt. They have grown in prominence during a period in history that demanded so little of them as institutions. Perhaps worst, they have so little humility. They stubbornly refuse to acknowledge what they can - and cannot - control.

I say all this not so much to disparage them, although there is some of that, but rather to warn investors that we do not have good pilots flying the plane here. Martin Wolf’s warnings are especially appropriate. There is all kinds of room for mistakes, “some out of over-optimism and others out of panic”.

So, one implication is to take what the Fed and ECB and others say with a grain of salt. For one, they don’t have any special insights into what is going on right now and for another, they have a different agenda than most investors. Another implication is that as they flail their arms and become increasingly desperate, they create a lot of additional potential to add uncertainty into the mix.

Finally, a message to the Fed, the ECB, and to many investors who have not gotten the memo yet: Let go of the overly optimistic expectations already. This doesn’t mean turning into a permabear or becoming cynical about everything. It means being able to observe the incredible headwinds, call them as such, and react accordingly. Do that and you will preserve a lot of wealth and be in good position when things begin to turn.

Thanks for reading!

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.