Observations by David Robertson, 6/20/25

The week had its ups and downs but there is plenty to discuss. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Stocks jumped out of the gate on Monday and volatility fell precipitously. Part of the move was reflexive “buy-the-dip” behavior after a down day on Friday and part of it was reflexive “fade the geopolitical event” behavior that has been part and parcel of the long bull run in stocks.

The only problem is Israel and Iran are still launching missiles at one another and there is no indication of imminent peace.

On Tuesday, weak retail sales and industrial production renewed the narrative of imminent recession. Trump also ditched the G7 gig in Canada and high-tailed it back to DC. Bonds rose and stocks fell and volatility spiked again.

On Wednesday, the Federal Open Market Committee (FOMC) revealed to an anxiously awaiting investment community that almost nothing had changed. Yes, expectations for unemployment and inflation were a tad higher and for GDP a tad lower, but there was absolutely nothing newsworthy. Just the way the FOMC wanted it.

The markets were closed on Thursday for the Juneteenth holiday and a certain amount of chop can be expected on Friday with options expiry.

Politics and public policy I

While new initiatives keep spewing forth from the Trump administration, enough time has lapsed now to form some opinions on programs like DOGE, and therefore to also infer some tendencies in the Trump administration itself.

Scott Lincicome ($), writing for the Dispatch, is a great candidate to evaluate DOGE because of his deep sympathies for reducing the size of government. Indeed, he highlights:

I work at a place with an entire website called “Downsizing the Federal Government,” so having a major new government project (and two of the world’s most attention-getting people) dedicated to the worthwhile—and increasingly urgent—cause of shrinking bureaucracy and cutting spending is an obviously good thing.

As such, it is not surprising Lincicome is sympathetic to the heightened visibility on “profligate government spending”. However, he is also clear-eyed about the results which have been disappointing: “Cato budget hawk Romina Boccia explains, Musk and company wildly underdelivered in terms of durable federal spending cuts.”

One of the reasons for this underperformance was the deliberate avoidance of collaboration with interested parties. For example, Lincicome notes, “My Cato Institute colleagues even documented, in herculean fashion, all the things to cut in a December 2024 report.” While those priorities reflect the particular politics of Cato, the point is thoughtful people had already considered many of the cost saving opportunities. There was no need to re-invent the wheel.

Rather than leveraging such resources, Musk decided to ignore them, even though he had absolutely no experience with government. This led to a lot of bad mistakes and unnecessary friction.

One of the bad mistakes was failing to realize that a great deal of government spending is programmatic. As Lincicome explains, “much of the government waste and fraud identified by various reports also requires congressional action because it’s hardwired into large U.S. spending programs designed by Congress.”

In other words, government over-spending is structural. In order to fix it, congressional action, i.e., structural reform, would be required. This was widely known and completely ignored.

In terms of performance, DOGE under Musk can be considered to have almost totally failed to attain its goals. The effort was at best amateurish and unprofessional. At worst it was counterproductive. All of these qualities now also reflect on the Trump administration. Perhaps the worst consequence is that the people who legitimately wanted a smaller government will be most disappointed by the failure. The only surprise is they didn’t appreciate that DOGE, by virtue of its acronym (and other signals), was not a serious effort from the start.

Politics and public policy II

First it was tariffs that caused a lot of squealing amongst the business community and ended up with selective pauses and exceptions. More recently, Section 899 of the budget bill, aka the revenge tax, has forced “Business chiefs [to] head for Capitol Hill to fight Trump’s foreign investment tax” according to the FT ($):

Dozens of executives from some of the world’s biggest companies will travel to Washington this week in a bid to stop a plan to raise taxes on foreign investments in the US [Section 899 of the budget bill], warning it may hit millions of American jobs.

“Senators recognise that it’s counter-productive to the economic vision for the administration, which has made a big point about trying to get more investment to the US.”

Once again it seems, Trump administration policy is causing angst even amongst its more fervent supporters. While the policy is still being debated in the Senate, current indications are that the Section 899 provisions will be included, albeit in a modestly toned down form.

It wasn’t just Section 899 that has been getting attention, though, as an escalation in immigration enforcement has rankled Americans of all types, again, even including Trump supporters. Judd Legum ($) reports:

In late May, top Trump aide Stephen Miller directed U.S. Immigration and Customs Enforcement (ICE) to increase arrests to 3,000 per day — roughly triple the agency's previous high-water mark. The directive prompted ICE to begin targeting workplaces in industries known to employ a large number of undocumented workers, including agriculture, construction, hospitality, and textiles.

A few days later, Trump changed the policy by excluding the agricultural and hospitality industries. A few days later, that exception was rescinded.

The first and most obvious observation is there is nothing like a cohesive approach to public policy with this administration. The norm is for inconsistency, capriciousness, and instability. You never know what tomorrow will bring.

Another pretty obvious observation is the increasing degree of pushback. One might expect a relatively new administration to implement policies that were at least fairly popular. That has not been the case though. While many voters broadly support the spirit of policies that address trade and immigration, there is increasing displeasure with overly aggressive enforcement practices.

Public policy III

The unpopularity of Trump administration policies is showing up in other places as well. As Jonathan Cohn ($) reports for the Bulwark:

Pretty much every blow to health care that was in the House version of the bill remains in the bill language Senate Finance Chairman Mike Crapo (R-Idaho) released on Monday.

What’s remarkable is that there is no reason to think the public wants this. Consider the already-dim assessment of the House version of the legislation, as revealed in a new KFF poll: Sixty-four percent of respondents hold an unfavorable view and just 35 percent hold a favorable one.

While, as Cohn notes, some Republican lawmakers actually do want this and some just “don’t want to cross Trump,” the support of the budget bill by legislators continues to antagonize their voters. Even more surprisingly, cuts to Medicaid and the Affordable Care Act promise to inflict disproportionate harm on Republican districts. Why are so many members of Congress acting against the interests of their constituents?

Martin Wolf ($) picks up on the same idea in the FT this week. In particular, he observes:

the combination of tariff increases with the OBBBA “would reduce after-tax-and-transfer incomes on average among the bottom 80 per cent of US households. The bottom 10 per cent of households would see an average reduction of more than 6.5 per cent in incomes, while those at the top would see an increase of nearly 1.5 per cent.”

As a result, Wolf concludes the One Big Beautiful Bill Act making its way through Congress does not show concern for ordinary Americans. Rather, he calls it a powerful example of “pluto-populism” in which “The rich receive most of the goodies; the poor become poorer; and the fiscal deficit stays huge.”

Although it is still early in the Trump administration, patterns are becoming clear. One of those patterns is the implementation of policies that hurt most Americans for the benefit of the wealthy few. This is completely antithetical to the concept of representative democracy and makes one wonder how long it can last.

Social dynamics

Demetri Kofinas produces the Hidden Forces podcast and is regular guest of other content providers in the investment industry. His commentary is regularly thoughtful, unconventional, and reflective of a generation that faces a lot more economic headwinds than its forebears. In a recent social media post, he assessed the geopolitical landscape, but quickly turned it into a commentary on our current socio-political environment:

Millions of honest, hard-working, and fundamentally kindhearted people in this country no longer find our discourse and politics recognizable. And worst of all, we feel powerless to change things. Who will lead us through this darkness?

No one is flying the plane. That’s too scary for most people to acknowledge so they pretend instead that those pointing out the obvious just have TDS or are otherwise unable to see the master plan in all this.

I always appreciate the insights Kofinas brings to investment issues because he always does his homework and is always thoughtful. What I appreciate most, however, is what those things look like through the eyes of someone who is also a generation younger than I am.

I find this instructive, especially as the nation ages. Tomorrow’s leaders don’t have the same formative experiences with extreme national pride. Conversely, they have a disproportionately greater experience with moments of extreme national shame. There is less pride, less hope, and more disenfranchisement, and understandably so. The economic opportunities are fewer and the obstacles are greater.

Kofinas calls it like he sees it and it’s not pretty:

I don’t see a master plan. And I’m tired of pretending that there is one. I also don’t think there will be anyone to “lead us out.” I think when societies reach this stage of unraveling and internal collapse, they more or less stumble their way through over time and eventually emerge to wonder what happened and how they let things get so bad.

In one sense, this is simply the realization of consequences. Debt pulls consumption forward. When a country takes on too much debt, it robs its future generations of opportunity. This is exactly what Kofinas is observing. There is no “master plan” because there is no politically acceptable way to extract the country from its excessive debt burdens and the hole it has dug for itself.

While the outlook is bleak, there is a sliver lining. Perhaps, as more people look out over the horizon and see the same darkness Kofinas does, maybe that will provide the impetus to stanch the decline and to create a better plan. Meanwhile, the outlook for household formation and consumer spending has to be lower than for previous generations.

Investment landscape I

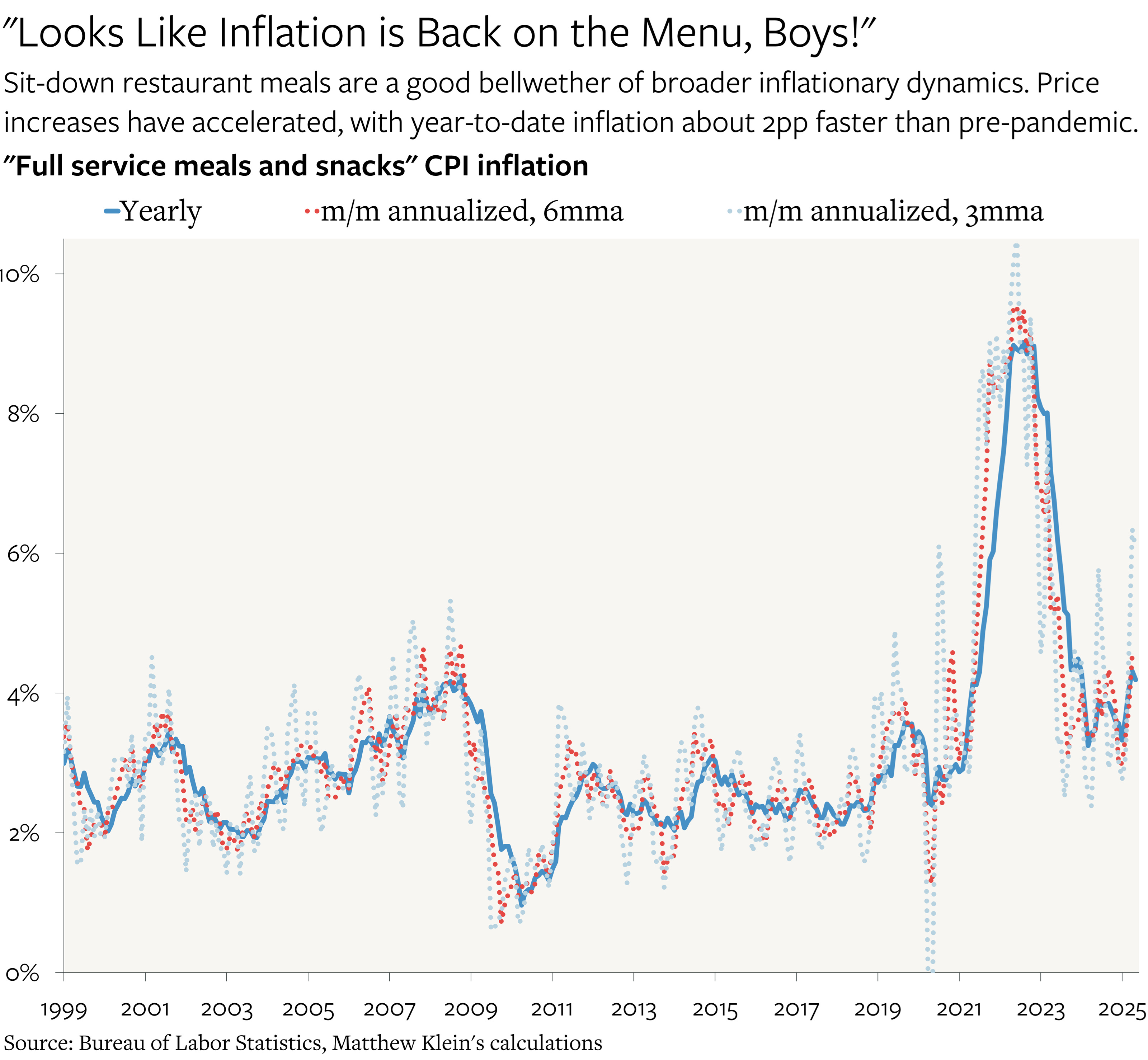

Signs of incremental economic weakening keep rolling in, but at the same time inflation stubbornly refuses to dissipate. Matt Klein ($) sees inflation ticking back up:

If I could only track one component of the CPI to get a sense of underlying inflation pressures in the economy, it would be the price of a meal at a sit-down restaurant. “Full service meals and snacks” are discretionary purchases of non-tradable services, where the biggest input costs are commercial rents and wages, followed by groceries, machinery, and cutlery. Restaurant prices were an early warning signal that the reopening inflation spike would be larger and last longer than I had initially hoped, and the relatively slow disinflation in this category was a useful corrective to those who thought that underlying inflation was set to return to pre-pandemic norms.

While I would guess that part of the recent spike is noise attributable to the lagged impact of rising grocery prices, the larger takeaway is that prices are still rising persistently faster than before the pandemic, which is consistent with other measures. The magnitudes are neither large—1-1.5 percentage points annualized—nor obviously harmful.

The good news is that while inflation is still clocking in at a rate above the Fed’s target of 2%, it is not spinning out of control either.

The bad news is that this is happening even as signs of economic activity are declining. This highlights a common tendency among the investment commentariat: A lot of analysts views inflation exclusively as a function of demand imbalance. The problem with that narrow perspective is that it ignores two other causes of inflation that are currently at work — supply constraints and monetary debasement. Add those two factors to the equation and you get slowing economic growth and persistently high inflation.

Investment landscape II

The working hypothesis continues to be that the absolute priority of the Trump administration is to pass the budget bill and its attendant tax cuts. Until that is done, all efforts must go to serve that purpose.

So far, the evidence continues to confirm the hypothesis of tax cut prioritization. The administration’s first tactic regarding the bill was to rush the bill through the House before meaningful resistance could be mounted. After it passed the House, the tactic switched to obfuscation to create uncertainty about what was in the bill.

Now that the bill’s contents have been reviewed and assessed (and widely disliked), the administration’s tactics are turning to distraction. At first, ICE aggressively ramped up enforcement efforts and created a number of media-worthy spectacles. More recently, drama around the Middle East has grabbed attention.

While the conflict between Israel and Iran is serious and has been simmering for a long time, it also appears as if Trump is using the occasion to “flood the zone”.

This potentially ulterior motive is exposed by the lack of any strategic necessity on the part of the United States to get involved in the conflict now. As geopolitical strategist Ian Bremmer assesses:

option for united states to take out iran’s nuclear capabilities at fordow doesn’t go away in a month or half a year.

why not allow israel to destroy above ground capacity, setting the iranian back by many months and maintain the capability?

what’s the urgent need for the united states to directly involve itself in the war right now?

If the working hypothesis holds, we will continue to see more dramatic, headline-grabbing proclamations from the White with the intent of diverting attention away from the budget bill. At the same time, the odds of meaningful volatility events in stocks or bonds that might threaten passage of the bill will remain fairly low.

Investment landscape III

The hypothesis leaves two main possibilities for how events transpire through the summer. One is that the bill passes, maybe not by the imposed July 4th deadline, but comfortably ahead of the X-date when the Treasury runs out of money, probably in late August. With that major priority accomplished, along with the lifting of the debt ceiling, Treasury will begin reloading its general account. As it does, it will deplete liquidity from the financial system and put pressure on risk assets.

A second possibility is that the budget bill gets held up, perhaps due to horribly negative polling, and a legislative battle ensues in July and August as the X-date closes in. The longer the debate goes on and the more public attention it receives, the more likely its passage is to be fraught. Nonetheless, it has to pass in order for the debt ceiling to be lifted.

In both cases, whether the bill gets passed fairly easily or not, there is likely to be a splintering of the Republican party. In the case tax cuts are passed, there will be little remaining common ground amongst factions that are otherwise ideologically opposed on many issues. In the case tax cuts are not easily passed, ongoing debate is likely to highlight and enflame pre-existing fractures.

Either way, we are likely to enter the end of summer with lower liquidity and Republican infighting, just as the economy continues to slow, the consequences of tariffs continue to roll in, the cold war with China grinds on and the conflict between Israel and Iran festers. In short, it’s probably best to enjoy the calm now while it lasts. There is a good chance there will be fireworks later in the summer.

Implications

One of the more prominent themes of the investment landscape the last few years has been the growing force of government intervention. While increasing constraints on government policy, mainly in the form of excessive debt and deficits, limit longer-term policy options, the need to provide narrative cover renders the short-term a low signal environment.

The importance of observing and incorporating fundamental changes in dynamics, even in the absence of intervening price volatility, is captured beautifully by Rudiger Dornbusch in the quote:

“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.”

Just because you may not see prices changing much day to day, doesn’t mean extremely important changes aren’t going that will one day manifest, and perhaps quickly. It’s easier to stay apprised along the way than to try to catch up after the fact. Stay safe out there.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.