Observations by David Robertson, 6/23/23

The market has been pretty indecisive lately - it seems like everyone just wants to get through the end of the quarter. That may be a mixed blessing as Q3 comes with some ominous forebodings.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

All the market chatter has been focused on NVDA and the unbelievable momentum of artificial intelligence and Big Tech. This is creating a need for professional (i.e., paid) investors to catch up or suffer career risk (i.e., get fired). At the same time it is creating an insufferable need amongst retail investors to chase performance. The chart below from themarketear.com ($) gives a good indication of just how extreme the race has become.

That’s one view. Another, very different view, comes from PauloMacro via Twitter. From his perspective, “This upside panic is cathartic. It signals the All Clear Echo is completing.” This is the phenomenon he has previously referred to as “Max Stupid”.

He goes on to explain how he thinks events will unfold:

In Q3 we should see a fulcrum in narratives. I expect a convergence of SLOOS tightening [i.e., bank credit surveys], long and variable lags, US deficit/issuance crowding out private sector (RRP only goes so far), and importantly cross-currency FUNDING to collide.

Another take on the same theme comes from Financelot:

Extreme VVIX / VIX divergence is a warning sign that we're in the final stages of the market cycle (blow off top). Currently at a divergence level only seen every few years. This aligns with the SKEW divergence where OTM vs ITM Puts reach an extreme before a market reversal.

How one views the market opportunity right now depends significantly on one’s time frame. Short-term, stocks could continue to go up, but the headwinds (and downside) are building. At some point in the not-too-distant future, there is likely to be a good chance to short. Longer-term, there is a lot of “Max Stupid” to avoid.

On a separate, but not wholly different note, Almost Daily Grant’s reported, “Tiger recently offered to sell a chunk of its positions in roughly 30 startups in bulk via a so-called strip sale, receiving no takers.” They aren’t the only ones. Apparently five relatively large “strip” portfolios have been shopped and received no bids.

This is another case of “no transactions” = “no price discovery”. It means buyers and sellers are too far off on price to agree a transaction. It also means the current value of those portfolios is almost certainly well below their reported value. As transactions eventually get done - and prices established - there is likely to be a step function down.

Credit

Credit spreads have remained fairly tight which is a condition that has confounded a number of market participants. I have documented many of the theories as to why this is the case, but there are two key points to keep in mind. Number one, the Fed’s key tool to affect the economy, interest rates, is a blunt one. Number two, it is working. As can be seen from the graph from themarketear.com ($), defaults are rising and are now only exceeded by the years 2020 (pandemic) and 2009 (GFC).

The main takeaway is that higher rates are biting into credit. Maybe not in highly visible macro statistics yet, but they are biting. The longer rates stay near current levels, the more damage to credit there will be. Eventually that will also bleed into other risk assets. Consider yourself forewarned.

Oil

Global Oil Data Deck (June ‘23) ($)

https://www.commoditycontext.com/p/global-oil-data-deck-june-23

Apparent Chinese petroleum demand rose another 900 kbpd in April to a staggering 17.6 MMbpd, a far-and-away all-time high and up 3.6 MMbpd y/y given depressed COVID-zero base effects in Spring 2022. However, it should be stressed that this number is unrealistically high, especially given the fact that economic activity was sluggish enough to prompt Beijing into a fresh wave of stimulus announcements last week.

Quick little insight on the oil market from Rory Johnston here. For all the bulls beating the drum on China’s recovery, the prospect that a great deal of recent demand strength is best explained by the effort to fill China’s SPR is a wet blanket. Further, Johnston continues to believe “that Chinese SPR-builds are best understood as transitory, discretionary demand”. Once that stops, demand will be a lot lower.

Inflation

Market Sit-Rep June 15th, 2023 | "Turbulence"

https://mailchi.mp/e197b346070f/market-sit-rep-june-15th-2023-turbulence

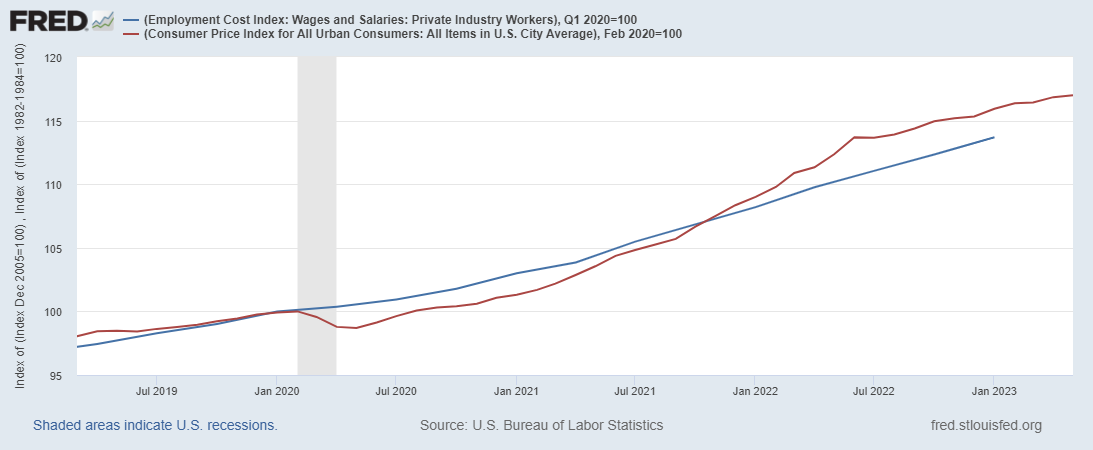

The reality of Average Weekly Earnings Growth being negative for an unmatched 26th consecutive month is often disregarded. An imbalance arises when income growth trails inflation. This discrepancy between inflation and wage growth equates to diminishing purchasing power. Even though inflation's rate of change might slow down, indicating its temporary nature, the reduction in purchasing power leaves a permanent mark on many people's financial health.

As inflation has been moderating the last few months, disinflationists have already started taking victory laps. Never mind inflation is not a short-term phenomenon that normally disappears as quickly as it emerges, like a summer pop-up rain storm.

After literally decades of wages failing to keep up with inflation, the pandemic finally provided an impetus for wages to jump ahead. After a few short months, however, inflation started heating up and after about a year and a half, those gains were lost.

The key issue here is price levels as opposed to inflation changes. For over a year and a half now, wage-earners have again been losing ground to inflation, even though inflation is moderating.

This presents a sticky challenge. The Fed’s Jerome Powell started off the FOMC meeting last week with the words: “Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.” By this standard, wage earners are part of the inflation problem, even as they are losing ground to inflation.

While the Fed continues to do contortions to justify its policy, the political reality is wage earners are falling behind again. With next year being a presidential election year, inflation is sure to be a hot button, but then so will real incomes, i.e., purchasing power. This also suggests there is a good chance some fiscal policy will emerge along the way to ease voters’ minds (and pocketbooks).

Monetary policy

I continue to be amazed, and to some extent, amused, by how many mainstream economists and journalists seem to treat monetary policy as a strictly independent and strictly economic exercise. Neither is true (in my opinion) and therefore most accounts misinterpret the real thrust of monetary policy.

To my point, Stimpyz’ post on Twitter, makes explicit the notion the Fed has “an agenda here that transcends inflation”. Yes, inflation is part of it, but no, inflation is not the whole gig.

When you start to add up all the arithmetic realities that Powell is going OUT OF HIS WAY to ignore, disregard& disrespect it is painfully obvious there is an agenda here that transcends inflation. Repeat after me: The Neutral Rate is not zero, no matter what the models say.

The outlines of that “other’ agenda appear in another tweet:

It wont be until the dots [from the Fed’s dot plot] suggest higher FOREVER that markets begin to see policy in the correct light. ZIRP and QE were failed experiments. They have damaged UST liquidity, perhaps irreparably. Thye wont go down this road again.

Interestingly, this analysis suggests the elimination of QE and ZIRP are the target of this expanded agenda. Even more interesting, they are the target because it is now evident those policies have caused financial instability. Almost too crazy to be true. The Fed doubles down on a policy (QE) that subsequently undermines its single most important mandate: Financial stability. Oops.

Yet another tweet by KKGB Kitty provides a slightly different perspective on Fed policy, but also features the notion “that the Fed decision had nothing to do with monetary policy”:

Almost everyone is lost amid the confusing messaging from yesterday: No hike day while pencilling in 2 more hikes later. What you need to understand is that the Fed decision had nothing to do with monetary policy. They had the margin to give some breathing space to both the Treasury and the banks and they made the financial stability choice. By not hiking, they allow Jeanette [Janet Yellen] to raise circa $ 400 b while draining RRP and not relying on a reserves drain.

One takeaway from this is monetary policy, as implemented by the Fed, has many progenitors; economics and money supply are only part of the picture. Politics and the reversal of its own mistake (i.e., QE) are also part of the broader agenda. In the political realm, higher rates are needed to provide the necessary incentive to rebuild productive capacity and higher rates also serve the needs of national security in a number of ways.

Another takeaway is that anyone whose primary investment thesis depends on the Fed coming in to save the day for investors by reinstituting QE is going to be sorely disappointed. Times have changed. Those who don’t change with them, will be consumed by them. Investors who focus exclusively on economic analysis as the foundation for Fed actions are going to get wrong-footed time and again.

Interest rates

Is the yield curve lying? ($)

https://www.ft.com/content/aa775ede-ed46-4d23-91d7-8908bd7d687e

There are two basic ways to call the yield curve a liar in mid-2023.

The first way is to argue that we are in an unusual economic cycle, in the following sense. There is an amount of tightening that is sufficient to bring down inflation; call that amount X. Then there is an amount of tightening that will force the economy into recession; call that Y. The idea is that, unlike past cycles, X is less than Y, and the Fed will stop at X.

The second way to call the yield curve a liar is to suggest that long rates have become hopelessly distorted — are too low, essentially — and therefore the curve no longer sends a reliable signal. It is common to blame the Fed’s bond-buying programs for the distortions. All you really need, though, is an argument that 10-year bonds are badly mispriced and that their yields should be higher (meaning the “real” yield curve is shallower than the apparent one).

The yield curve has been an important market signal and Robert Armstrong and Ethan Wu do a nice job of framing the skepticism around it. While I believe “hopelessly distorted” is too extreme in describing long rates, I also believe it is insane to assume the massive purchases of bonds by the Fed during QE and the exceptionally low inflation expectations of most of the last fifteen years don’t have any distorting effect on long rates.

John Hussman corroborates this view by showing the shortfall of 10-year Treasury yields relative to historically useful proxies:

Another reason that we’re hesitant to step out into long-duration bonds is that yields remain inadequate. Historically, the weighted average of Treasury bill yields, core inflation, and nominal GDP growth has been something of a lower bound for 10-year Treasury yields. Presently, the 10-year Treasury yield (blue) is well below benchmarks that typically define an “adequate” yield. That’s part of the reason why the yield curve is so inverted.

Interestingly too, Chris Whalen makes the case that long-term rates need to rise in order to prevent a complete collapse of the banking system. He focuses more on the distortions caused by the Fed’s purchase of Mortgage Backed Securities (MBS):

Why does the Fed need to sell MBS from the system open market account (SOMA)? Because only by releasing that massive duration locked away inside the sterilized confines of SOMA back into the markets can the FOMC get long-term interest rates above 4%. Adjusted for option-adjusted duration, the Fed's $2 trillion MBS position is larger than its portfolio of Treasury debt.

By getting longer-term rates up close to or slightly above short rates, which is where Hussman’s analysis says they should be, banks can earn a spread on their lending again. That spread will create profit - which will build capital - which will offset the unrealized losses on their held-to-maturity portfolios of longer-term Treasuries.

In my mind, the inverted yield curve says more about policy priorities than it does about the economy right now. My guess is the yield curve is inverted because the Fed has been afraid of both raising (and maintaining) short rates while also allowing long-term rates to rise too much. As a result, it prioritized short rates and held off on long rates. My expectation is sometime fairly soon, long rates will start drifting up closer to where they should be, say in the 5.0 - 5.5% range.

Landscape I

One of the many great challenges of this investment environment is incorporating the growing tendency of government to intervene when things do not go its way. The challenges come on two main fronts. One involves going beyond the analysis of the investment landscape to also include potential policy responses in various scenarios. The other involves re-imagining policy intervention from a purely reactive exercise to a much more proactive one.

On the first, for example, it is wrong to consider inflationary pressures without also considering the role of fiscal spending. Going forward, decisions on monetary policy, rates, the relative strength of the US dollar, commodities, credit, and many other core aspects of financial markets will be driven by the problems they solve for industrial policy and geopolitical strategy, among others. If you get the broad direction of those overarching public policy plans right, you should be able to avoid many of the bigger potholes along the way.

The second challenge involves a change in mindset regarding the nature of policy intervention. When times are good and the environment is benign, there is no need for strategic policy direction. The only real need is to be able to respond to emergencies.

When times get tougher, governments need a plan in order to appear as if they are doing something to solve the problem. Otherwise, they don’t get re-elected. This means public policy tends to become more cohesive and more proactive. It is also useful to remember that policy doesn’t need to be complete, or completely consistent. Oftentimes, policy is designed to simply steer things in a general direction, rather than to mandate specific actions. Other times, individual policies may conflict with the overarching plan. That doesn’t mean there is no overarching plan or that there will always be internal inconsistency.

Landscape II

Two of the big investment themes I have discussed over the last several years are the “carry” regime and the notion of antifragility as explained by Nassim Nicholas Taleb. Thematically, the two present something of a macroeconomic “Clash of titans”.

On one hand, the carry regime creates a powerful but ultimately self-destructive environment. In the effort to foster financial stability, central banks often also encourage, directly or indirectly, moderated volatility. Moderate volatility, facilitates more lending, however, which pushes volatility down even lower. While this can continue for quite some time, it ultimately blows up because of too much leverage. It creates a system that, in a word, is fragile. For perspective, Brent Donnelly noted recently:

The other theme percolating in the background is a strong appetite to sell volatility and own carry trades. It’s reminiscent of 2006 and 2007, when you had the entire market positioned for a recessionary calamity and instead, you got two years of grinding, low-vol, carry-friendly action.

On the other hand, Taleb who made a name for himself by characterizing “black swan” risks, went on to describe the antidote to volatility in his book, Antifragile. There are two main prongs of attack. One, avoid fragility. Things that are large and complex are fragile. When the going gets tough, a lot of things can break. Two, actively seek out things that benefit from volatility. New ideas, new friends, new experiences, and new ideas, among others, can all provide explosive benefits when conditions change unpredictably.

So, as monetary authorities seem to be trying to manage a process of “controlled demolition” (of financial assets), what wins out? On one hand, “demolition” suggests antifragility wins out. On the other, “controlled” is simply another way of expressing the management of volatility - which suggests carry wins out.

Ultimately this is a matter of short-term vs. long-term. In practice, it is infeasible to consistently control the demolition. As a result, there will be periods of more and less control. At the same time, the carry regime is inherently fragile long-term and therefore cannot be the longer-term outcome. As a result, I view the process of controlled demolition as one of providing guardrails on volatility on a medium-term path to more normal, and less artificially controlled, volatility.

Implications

One implication of increasingly interventionist public policy is the timing of events is also increasingly a function of policy. For example, everyone now knows after the debt ceiling deal was done, there would be a massive issuance of new debt to refill the TGA and to meet growing deficits. The issuance is off and running but no detrimental effect on stocks yet. What gives?

As KKGB Kitty explained in the “Monetary policy” section, there are good reasons for Fed and Treasury officials to buy some time. Allow the TGA to get mostly refilled and get through the end of the quarter, and authorities will be in a much better position to deal with any possible negative consequences of a selloff. That doesn’t mean the selloff isn’t coming; it just means part of the intervention is deciding when it comes.

Increasingly, investors must consider not just what officialdom wants in a given situation, but when it wants it to happen.

On a related issue, it can certainly be argued that long-term rates are artificially low for a reason - because the Fed and the Treasury want them there in order to facilitate the full implementation of higher short-term rates. The main question is, when is it ok to let them go up again?

The answer appears to be later this summer - say mid-July/August. Insofar as this is correct, the implication is negative for risk assets.

This will be something to watch closely for the reaction function of both investors and public authorities because it will be very hard to control. For one, any change in market direction can easily overshoot. For another, any intervention to micromanage things can backfire spectacularly. For another, the response to a significantly down market is an imponderable: A good number of today’s investors have not had to deal with real, sustained market adversity. It’s hard to say how they might react to losing a ton of money. There is certainly potential for extreme volatility and extreme behavior.

Good luck and stay safe!

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.