Observations by David Robertson, 7/19/24

Political news is heating up and someone took the market off cruise control. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Stocks sold off on Wednesday apparently led by rumors of an even harsher crackdown on semiconductor sales to China. Zerohedge summarized a Bloomberg report indicating “The Biden administration is considering imposing the strictest trade restrictions available” on companies like Tokyo Electron and ASML.”

This is interesting for a few reasons. For one, we seem to be at the stage of tensions with China in which both Democrats and Republicans are vying to be seen as the toughest competitor. The cost of that competition will be lower revenues for semiconductor companies and will almost certainly affect other big tech companies as well. Finally, other collateral damage is likely to be TSMC, which happens to be not only the largest semiconductor manufacturing company in the world, but also the largest constituent in a wide variety of emerging market funds.

On a separate not, the lower than expected CPI number got all the attention last week but the producer price index (PPI) came in higher than expected the following day. As Craig Shapiro posted, “PPI strong + CPI soft = corporate profitability margin squeeze.” It will be interesting to see if pressure on margins on is becoming apparent in quarterly reports the next few weeks.

Finally, Chris Whalen posted some of his thoughts on banking regulation in light of recent events: “With the landmark Supreme Court decision in Loper Bright Enterprises v. Raimondo, overturning Chevron USA v. National Resources Defense Council, much of the rule making by the Fed and other prudential regulators is exposed to attack.”

He’s right and there almost assuredly will be attacks on bank regulation and Fed rule making. While this clearly presents an opportunity to “right” some “wrongs”, it also presents an opportunity for utter chaos. Further, this applies to everything, not just banking.

I hope this does create an opportunity to clean up some regulatory practices that had become hopelessly ineffective over time. However, I also worry that a big can of worms has been opened that will wreak havoc and spawn unintended consequences for years to come.

Inflation

How Many Benign Inflation Prints Are Enough? ($)

https://theovershoot.co/p/how-many-benign-inflation-prints

But there is also a countervailing risk [to waiting to cut rates until after capital spending falls]: policymakers may be overemphasizing the significance of the latest data and underemphasizing the possibility that at least some of the recent slowdown in inflation (and job market weakening) may be noise.

I am not sure which analysis is correct, but I am wary of taking two months of benign inflation prints as proof that inflation will remain subdued

Of all the guffaw that came out of the CPI report and Jerome Powell’s comments last week, it was refreshing to read the eminently sensible analysis from Matt Klein on inflation. In short, two months of good numbers is not enough to change policy.

Of course, this doesn’t mean the Fed won’t go ahead and cut rates, it just means doing so on current data is a poor justification. Wouldn’t be the first time, won’t be the last time.

Another interesting element of the inflation dynamic is the relatively recent divergence between the mean and median expectations of longer-term inflation. A nice post by Jordan Weissmann highlights some interesting findings from a recent paper on the Michigan surveys. As can be seen from the graph, the divergence between mean and median expectations has been increasing substantially since about 2020.

The paper reports, “the elevated level of mean long-run expectations has been amplified by the methodological transition from phone to web interviewing that began in April 2024, because respondents on web interviews are consistently more willing to report extremely high expectations than on phone interviews.” As a result, it concludes, “recent trends are … unlikely to reflect a fundamental deterioration in consumers’ inflation expectations.”

This may be, but who’s to say numbers reported from web surveys are less representative than those from phone calls? How representative is the person who picks up a call from an unknown number and chats for a while?

The paper itself acknowledges, “mean expectations have well exceeded medians during periods of higher realized inflation”. All I know is if my job depended on making sure long-run inflation expectations remained anchored, I would be running all kinds of tests to better understand the data divergence and to be absolutely sure those expectations were not becoming unanchored.

Housing

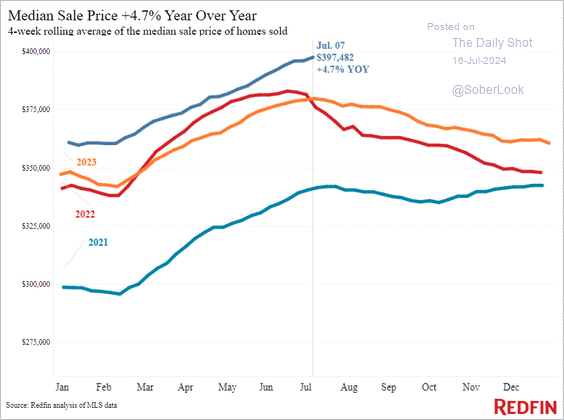

A couple of graphs of the housing market from @SoberLook nicely encapsulate the current market. First, buying conditions for houses are becoming absolutely miserable. This can be seen as a sentiment proxy for achieving the “American Dream”.

Second, a big part of the problem is that prices continue going up. Combined with high rates, it explains a big part of the still-falling buying conditions.

A big part of the problem is inventories are still low, but they are rising. As more homes come onto the market, especially in states like Texas and Florida, there are likely to be more price concessions which is likely to better facilitate demand with supply. In other words, greater supply will yield better price discovery.

This is true in other markets as well. When very few assets sell, those sales prices are not indicative of the market. As a result, as transactions pick up, it is fair to expect downward pressure on home prices - and on other assets as well.

Politics

GZero Daily, Tuesday, July 16, 2024

https://us12.campaign-archive.com/?e=5c7365da58&u=7404e6dcdc8018f49c82e941d&id=cb2ffe06eb

On the policy front, the RNC’s first day, themed “Make America Wealthy Again,” introduced the party’s economic platform. Speakers hammered Biden for high prices and Mike Waltz, co-chair of the platform committee, said that the Trump campaign would focus on helping "the forgotten men and women of America," by “unleashing American energy” and “sending a cruise missile into the heart of inflation.” Scott and others blamed illegal immigration for “crushing American workers.”

Teamsters Union President Sean O’Brien did not endorse the ticket but still received the most speaking time onstage, which he used to call for labor reform law and to attack big businesses and corporate lobby groups for “waging a war against American workers” – rhetoric that would have been unheard of before Trump steered the party toward the working class. O’Brien has hinted he may not endorse either candidate, which would be a big loss for Union Joe.

After the United Auto Workers president endorsed Joe Biden, it is very interesting to see the Teamsters president take center stage at the Republican convention. Clearly there is political competition for the blue collar vote. Clearly also, neither party can claim to have a lock on getting that support.

This raises a bigger point. For as much as Republicans and Democrats are both trying to muster support from blue collar workers, their broader economic policies often conflict with that objective. Regardless of whether you think wages are being suppressed by illegal immigration or not, higher wages will force inflation higher. If that happens durably, it will almost surely impinge upon markets.

I suspect this is a big reason why the labor vote is up for grabs. When push comes to shove, neither party believes it can sacrifice the benefits of strong capital markets to gain favor with labor. As a result, while both parties are keen to get the labor vote, neither has been willing to offer much more than platitudes for it.

This brings up a recurring theme of mine - that of political realignment. In order to attain whole-hearted support of workers, any political alliance will need to accept, and perhaps even embrace, that the consequences of such a move are likely to be detrimental to markets.

Maybe one of the major parties can pull it off. Maybe a new party will have to be formed. What is clear is that the political winds are shifting towards labor (and away from capital) across most of the world. In the US, however, the unique sway of capital over the political machinery has prevented further progress by labor. It will be very interesting to see if this starts changing.

Geopolitics

It is easy in the US to underestimate the importance of events that happen outside of the US. Not only do they rarely threaten Americans directly, but the indirect effects usually fall beneath the radar for most people. These factors make the thread by Matthew Light on X especially eye-opening:

Having recently spent a few weeks in Poland and Estonia, I formed the impression that the Russian invasion of Ukraine has transformed neighbouring countries in ways that US and western governments completely fail to grasp. Two years of war have radically reshaped expectations.1/

From the Estonian colleague who calmly told me there will be a Russia-Nato war in the next few years in which Estonia will be partially or completely destroyed, to the Polish mother who no -longer wants her son to pursue a military career--people are drawing conclusions. 2/

They are concluding that Nato is feckless and cannot or will not deter Russia. They are questioning whether their own institutions, and allies, are up to the challenges confronting them. And they are factoring likelihood of war into their own life plans in ways that shocked me. 3/

One thing that becomes immediately clear from Light’s account is that people who live in close proximity to Ukraine have a very different take on Russia’s invasion than what we read in US news accounts. For them the threats are real and immediate. They are not abstract and distant. As a result, they are “radically reshaping their expectations”.

They don’t see Russia’s invasion as an innocent little excursion. They are much closer to the deaths, the broken families, and the relentlessly bombed out towns and villages. They see Russia’s aggressions as proof of concept. They know they are likely to be next in line in the absence of sturdy resistance.

Light’s conclusion is the “reputational damage to Nato (and I daresay the EU) has been huge. They have been exposed as inept and compromised.” People in Eastern Europe “see what is being allowed to happen to their neighbour” and are adjusting their life plans accordingly. While there are obviously costs to standing by Ukraine, there are also obviously costs to not doing so. Those include reputational damage and extend to a diminished capacity to form effective alliances. It’s a choice.

Monetary policy

While everyone is looking at rate cuts from the Fed as the key market indicator, the Quarterly Refunding Announcement (QRA) from the Treasury at the end of the month may have an even greater impact. This is where Treasury lays out its expected funding needs, and in particular, the amount of longer-term debt it will need to issue.

Craig Shapiro homes in on the issue in a recent post: “Even though Yellen has said not to expect increases in duration issuance in the next few quarters,” “the conditions for the Treasury to issue further out the curve have only improved since the last QRA,” but “the borrowing needs have grown materially since the last update”. In other words, why wouldn’t Treasury increase issuance of longer-term debt?

If such issuance was forestalled in a politically motivated effort to suppress longer-term rates and therefore improve Biden’s reelection chances, does that change after his poor debate performance? Regardless, the chances of longer-term rates going up seems to be higher than the market is currently discounting.

Investment landscape I

Charles McGarraugh is talking his book here, but he makes an incredibly important point. Since Covid, markets have structurally changed. As a result, “bonds and equities as asset classes no longer cross hedge each other”:

Chart 2: Bond/Equity Rolling 120-day returns correlation, last 10 years (SPY vs AGG, Bloomberg data)

A regime shift in returns profiles happened with Covid, with the correlation across financial assets now skeing [skewing] highly positive due to predominance of monetary uncertainty over global growth uncertainty.

In other words, bonds and equities as asset classes no longer cross hedge each other, and traditional "risk parity" is broken. Therefore most "diversified" portfolios of financial assets now suffer from excess volatility drag hurting their prospects for long term compounded returns.

To remedy it we will see a structural "reach for diversification" across the asset management industry just as in the previous regime we saw a reach for yield. This will drive changes in product lineups for most asset managers, and change the nature of the financial advice most competent advisors will need to give clients. *Liquid* diversifiers are now more valuable than ever.

This has very major implications for the vast majority of investors. The reason is that the vast majority of investment portfolios are based on a balance of stocks and bonds.

As McGarraugh argues, however, the environment has changed such that those portfolios are no longer “diversified” in a meaningful way. Thus far it hasn’t mattered much because stock returns have remained strong.

It will matter though and the way it will be felt is though increasing portfolio volatility. The answer is to seek out “liquid alternative risk premia” such as “commodities, trend, relative value, managed futures, real assets etc.” Copy that.

Investment landscape II

Investors should focus less on rates and more on the money flows ($)

https://www.ft.com/content/c122f9ab-4f38-4163-9278-65e6e3cfac2f

At $600bn, year-to-date inflows to mutual funds and ETFs exceed those for any year bar 2021. As many a portfolio manager will acknowledge when not in marketing mode, it is ongoing inflows — not the cheapness of their asset classes — which keeps them buying.

In the six months following markets’ most recent trough last October, global reserves rose by $600bn, ongoing QT notwithstanding. As such, the risk rally was no coincidence: it was almost as though central banks had been doing QE.

Thinking in terms of these money flows — and not just rate changes — casts this year’s market performance in a very different light.

Mutual fund flows in the past few weeks have remained quite strong, notwithstanding the lack of support from reserves. That decoupling may have further to run. But with the liquidity torrent from central banks unlikely to be re-established in coming months, any further rally from here looks at risk of drying up. And rate easing, when it comes, is unlikely to be a substitute.

Just to repeat here, for those sitting in the back, strong market performance has not been due to any significant fundamental reason but rather due to “ongoing inflows”. With money continuing to flow into stocks, they must be purchased at ever-higher prices.

With liquidity as a key driver of stocks, its trajectory is an important indicator. On that front, strategist Matt King says “the liquidity torrent from central banks [is] unlikely to be re-established in coming months”.

Taken at face value, this has two important implications. One is that exuberance for stocks is exceeding that warranted by liquidity alone. This is a setup for a selloff.

Another is that the enthusiasm for rate cuts is misplaced. Insofar as liquidity has been the major driver, and I believe it has, lower rates without liquidity support is bound to be extremely disappointing for investors. Beware what you wish for.

Investment landscape III

A recent story in Axios reported:

Gen X consistently ranks in surveys as the least-prepared group for when they stop earning … The first members of Gen X were born in January 1965, which means they turn 59 ½ this month and can start withdrawing money from 401(k) and other retirement accounts without paying a penalty.

The first thought I had reading this story is, yeah, a lot of Gen Xers are going to have a tough time with retirement. The second thought I had is, holy cow, without a withdrawal penalty, that could be quite a bit of money coming out of the market. As I mentioned in the previous item, flows have been driving stock prices. If and when the flows reverse, the new marginal buyer will have very different, and more price sensitive, incentives than the passive funds that have dominated for so long.

Increasing unemployment will also reduce inflows to stocks as 401k contributions slow. Further, if corporate margins start getting squeezed, they will have less money to repurchase shares, and that will reduce flows as well. I don’t know when the turning point is coming, but it looks like it’s coming.

Implications

With the Republican National Convention this week, it’s hard to avoid the subject of politics and a great deal of the commentary focuses on “Trump trades”. For starters, I am naturally disinclined to engage in that kind of speculation because there are so many things that can go wrong. Candidates lie, divided government impedes action, other priorities arise, and on and on.

Nonetheless, in a market driven by narratives more than anything else, it is important to understand them. On this point, the Republican platform sounds to me like a smorgasbord of ideas from Reagan Republicans, populists, and general pro-business types. It’s as if they sent out a questionnaire and included every single thing voters said they wanted. I can’t help but think, “If you stand for everything, you stand for nothing”.

Another aspect of such a varied platform is that there are bound to be inconsistencies and conflicts. I’m not the only one noticing this. As John Authers highlighted in his piece Thursday:

the Trump platform is mutually contradictory. His current economic wish list includes:

Tariffs

Lower interest rates

A weaker dollar

Fiscal expansion

Lower inflation

None of the first four is compatible with the fifth. All things equal, the Republican platform is a list of measures to boost inflation.

The least damaging implication is that the message comes across as confused and lacking sincerity. That won’t win over a lot of undecided voters, but it won’t lose committed voters either.

The more damaging implication is that there is no clear direction forward for the party. Even worse, it could signal significant potential for internecine warfare amongst different factions for policy direction. All this is exacerbated by Trump’s well-earned reputation for capriciousness.

So, in a market driven by narratives, the expansive grab bag of Republican priorities makes it really hard to form any kind of cohesive narrative. In the absence of such a cohesive narrative, investors may be a lot less amenable to seeking out risk.

While risk has been building in the market all year with new highs being set at regular intervals, I would not be at all surprised that the rally gets killed not by a silver bullet, but by the simple lack of a stable narrative to keep building on.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.