Observations by David Robertson 9/24/21

Last week I observed “odd trading behavior” that could cause “an important inflection point”. The week before, I characterized a “somewhat eerie pall over the market”, remarked on the weakness of crypto, and suggested watching the US dollar for clues. This week, those warning signs materialized in weakness for stocks – but only for a few minutes before concerns completely evaporated.

Let me know if you have comments. You can reach me at drobertson@areteam.com.

Market observations

The week started off on a weak note with S&P 500 futures down 1.5% on Monday morning. The market traded down another percent before staging a buy-the-dip rally late in the day. Vix exploded higher, bonds were up, and the dollar was up. Interestingly, and perhaps tellingly, gold was one of the few green markers on the screen and bitcoin was down almost 8%.

The biggest single impetus for the weakness was Evergrande, the large Chinese property developer which is in deep financial distress and missed interest payments due early in the week. A couple of interesting insights come out of the market’s response. One is “the Pavlovian”, buy-the-dip (BTD) mentality is still strong and is not likely to go away quickly …

Perfection is gone - SPX futs "well" below the 50 day, Sep 20 2021 at 04:35 ($)

https://themarketear.com/premium

“Spoos is down, breaking below the big 50 day moving average so many have been referring to.

The latest ‘loved’ buy the dip has now transformed into pure long pain. The crowd is now relying on hope that the bounce materialises so they can get out flat...

We have explained the complex psychology of this market over past weeks. The Pavlovian investor has learnt the hard way to buy every dip. They are now all waiting for the reward, but so far only p/l pain is delivered.”

Another point is the market is treating every event like Evergrande as a binary event like Lehman: Either the financial markets are seizing up and the world is going to end, or everything is ok – carry on. The graph below from themarketear.com ($) shows the wild and wooly (and short-lived) round-trip of Vix.

Increasingly, a third option – that of a long, slow grind - is presenting itself. For now, BTD still carries weight, but its effect seems to be weakening. It will be very interesting to observe how BTD traders adapt to an increasingly hostile environment for their chosen strategy.

Economy

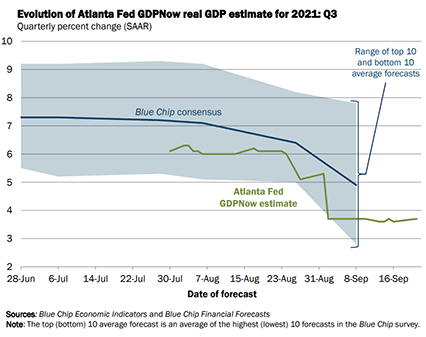

The graph below from the Federal Reserve Board of Atlanta’s GDPNow website shows how rapidly growth estimates have tailed off over the last month and how much lower the quasi real-time estimates are than the “Blue Chip consensus”. The euphoria from strong prints of 6.3% and 6.6% for the first and second quarters, respectively, has clearly worn off.

The reasons for the slowdown are becoming increasingly clear: Supply chain bottlenecks and higher prices aren’t just annoyances. Such challenges are widespread and persistent enough to slow down the whole economy …

Homebuilders sound shortage alarm

https://www.axios.com/newsletters/axios-closer?

“Lennar, one of the country’s biggest homebuilders, said material shortages of windows, lumber, flooring and more kept it from delivering as many homes as it could have.”

The outlook for automakers gets cloudier by the day

“The outlook for global automakers and suppliers continues to worsen, amid heightened risk from supply chain disruptions, including the ongoing semiconductor chip shortage.”

“IHS Markit slashed its forecast for global light-vehicle production in 2021 by 6.2% — about 5 million vehicles. It's cutting even deeper — 9.3% or about 8.45 million vehicles — for 2022.”

Further, persistently higher prices on necessary goods act like a tax. Fuel prices rank right at the top of that list because so many people commute, because the price increases are extremely visible, and because they have a demonstrably negative effect on budgets that have very little cushion …

Biden’s fuel price problem ($)

https://www.ft.com/content/9a42c01e-3122-4df5-9842-6acd4fed1185

“Simply put, high fuel prices are a vote killer. The US has one of the world’s highest rates of car ownership and Americans like cheap fuel. When prices rise, politicians worry they will be blamed.”

“A study by researchers at Northwestern University in 2016 found that for every 10-cent rise in petrol prices, the approval rating of the incumbent president dropped by 0.6 percentage points, after controlling for other factors.”

This set of circumstances is likely to make the Fed’s job extremely challenging. If the Fed is not diligent enough on tightening monetary policy, increasing prices threaten to slow the economy to a crawl on their own. If the Fed is even slightly too aggressive with tightening, stocks and bonds can fall significantly and create a different drag on the economy. At this point, I’m not sure there is enough room to operate for the Fed to be effective.

Politics

Crunch time for Biden’s economic plan: ‘Failure is not an option’ ($)

https://www.ft.com/content/5e3defde-3260-4e61-9ecd-b142b30d1a69

“You’ve got to reset the table in terms of strengthening institutions, but most importantly, strengthening the idea that the government can do good things to help people’s live,” says [Sen. Mark] Warner.

On one hand, it is hard to dispute the challenges in assembling an economic plan. As Warner also noted, “But how this all fits together . . . is maybe the most complicated Rubik’s cube you can imagine”.

On the other hand, however, it strikes me the foundational assumption is all wrong. Warner argues the table just needs to be reset, and the idea government can do good things just needs to be strengthened. Perhaps, as a Senator, he is just talking his book. To me, and I’m sure to many other people, it sounds like he is almost dangerously out of touch.

If we limit ourselves to just the news items in the last couple of weeks, we find Fed governors trading securities that stand to directly benefit from policies they set. Even better, what stands out as a clear conflict of interest in the public eye was not even a breach of the Fed’s own rules on personal trading.

In addition, the testimonies of several Olympic gymnasts revealed so many acts of negligence, insensitivity, abuse, and outright malfeasance on the part of the FBI as to raise the question if the organization isn’t rotten to its core.

I could go on with the hugely disproportionate impact lockdowns have had on younger people and the rapidly diminishing confidence in the dollar as a vehicle to retain value. That’s not the point, though. The point is, a lot of people, especially younger people, are losing confidence in the governance of the country and of institutions in general. They/we don’t need a pep talk; we need systems and institutions that are completely re-imagined to be fit for purpose and we need better performance by leaders.

Regulation

Facebook's social balance is in the red

https://www.axios.com/facebooks-social-balance-red-30f1b393-fd7a-4bb2-8a11-c509df21e6a5.html

“A system called XCheck, the subject of Monday's story in the Journal series, placed millions of prominent users in a VIP tier that allowed them to break Facebook's rules with few or no consequences, leaving the door wide open to the spread of harmful content.”

“The Journal also reported how harmful Instagram can be for young girls — a huge issue that comes as the company continues to weigh a separate version of the photo and video service aimed directly at the under-18 set.”

The Wall Street Journal published a multipart series on Facebook featuring many of the costs the company’s practices impose on society. This has all the appearance of a concerted effort because these issues have all been around for a long time. One has to ask, “Why are we reading these now?”

The image I have a hard time shaking is that of a movie where someone goes on a journey that is ostensibly a hunting trip, only to gradually realize they are the ones being hunted. Facebook has been aggressive in growing, acquiring potential competitors, and breaking rules. It appears as if somebody is looking for payback.

China

This Is How Contagion From Evergrande's Default Will Spread To The Rest Of The World ($)

https://www.zerohedge.com/markets/how-contagion-evergrandes-default-will-spread-rest-world

“Yet despite the retrenchment, an Evergrande collapse, even a controlled one, would still reverberate through the Chinese economy given liabilities equal to 2% of the country's GDP. It would cripple the embattled property sector, leading to a painful bond selloff among the rest of China's property developers, hammering China's real estate sector, which accounts for approximately 70% of Chinese household wealth as we showed back in 2014 ... and will result in a recession even in a best case scenario. That said, a ‘best case’ scenario is unlikely: the company's bank exposure is wide and a leaked 2020 document, written off as a fabrication by Evergrande but taken seriously by analysts, showed liabilities extending to more than 128 banks and over 121 non-banking institutions.”

Financial pundits have been falling all over themselves to explain why Evergrande is not a big deal so I will take some space here to set the record straight.

First, Evergrande has a huge amount of debt and is effectively bankrupt. What this means is the market for residential property in China just transitioned from one where prices were set by price-insensitive buyers to one where prices are set by forced sellers. This is a huge difference and will lower, and perhaps dramatically lower, prices of Chinese real estate.

Second, when prices start going down, loans go bad and when that happens, money gets destroyed. This amounts to monetary tightening and is exactly what happened in the throes of the financial crisis. This tightening is magnified by the fact that lower prices mean less collateral for borrowing.

Third, I have been warning for several years the impetus for a significant change in market conditions could come from outside the US. Investors who are singularly focused on the US are going to be flying blind.

Fourth, none of the problems emerging from the Evergrande situation are new. I highlighted the problems with Chinese residential real estate in a blog post entitled, “The most important asset class in the world,” three years ago and I certainly wasn’t the first to probe the topic. The takeaway is investors have become exceptionally skilled at responding only to immediate, acute, crises and ignoring chronic, unsustainable problems.

Finally, most of this analysis is not about rocket science analytical inquiry. Rather, it is about choice. Some of us see dangers and prudently manage them or avoid them altogether. Others, like Blackrock, seem more interested in gathering assets regardless of risks …

Monetary policy

The Fed’s big meeting on Tue and Wed came and went and – almost nothing changed. The one thing we did learn was despite widespread speculation the Fed would lay out a timeline for tapering, it provided no more than vague guidance on the subject: “If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.”

It is interesting these comments were widely interpreted as a signal tapering would start in November. Point one is Fed press releases are intensely scrutinized before being published. If it didn’t say “November”, it didn’t mean “November”. Point two, the Fed sees data before the rest of us and was likely intentionally noncommittal. After weak jobs numbers on Thursday morning followed by very weak PMI data, it wanted to avoid a hard commitment it would have to back away from. In other words, I wouldn’t be getting too excited about a substantial or sustained tapering just yet.

Inflation

Summers and Roubini on inflation ($)

https://www.ft.com/content/f8378ca3-9182-4e14-9d54-9d7a213f82b0

“To reduce those debt ratios, going from 2 per cent to 3 per cent inflation is not gonna be enough. You need to have significant, unexpected inflation that wipes out some of the real value of long-term fixed-rate debt. And by the way, a lot of the debt is shorter term and has to reprice, or the debt is in foreign currencies so for emerging markets the option of wiping it out with inflation is not there, and you have outright defaults.”

“. . . Markets will eventually price in volatile inflation, so inflation risk premia become higher. Therefore real rates rise, and eventually debt service ratios are going to become unsustainable.”

These comments from Nouriel Roubini (and captured by Robert Armstrong at the FT) reveal a much uglier profile of inflation than the Fed likes to admit. In essence, the policy purpose of stoking inflation is to help reduce the value of excess debt. That doesn’t happen with nice, neat 2-3% inflation, however. In other words, the stated policy of moderate, controlled inflation is not fit for purpose (of reducing the value of debt). Just one more indication to treat the potential for “significant, unexpected” inflation as a real threat.

Analyst tips

Sept. 11 and the Future of American History: Niall Ferguson

“We can learn from history because there will always be Collingwood’s tigers in the grass. But we must remember that we see the tiger more easily with binoculars than with the naked eye: technological discontinuity matters at least as much as the eternal historical verities (power corrupts, democracy turns into tyranny via demagogy, and so on). If the global war on terrorism was Vietnam reprised — if the fall of Kabul was the fall of Saigon re-enacted — it matters that the earlier event was broadcast on television and the later one on social media.”

This article by Niall Ferguson captured my attention because the dimensions of prediction he drew are useful and because they very much apply to investment analysis. For example, prediction about things like human nature can be fairly accurate because human nature doesn’t change much. Whether it is a concept like “power corrupts” or one like “obfuscation of accounting numbers tends to be a bad sign”, the insights are robust across a wide variety of conditions.

Ferguson’s main point, however, is about technological discontinuity. Not only is technology very hard to predict (because it changes rapidly and can manifest across society in unpredictable ways), but it is also at least as important as “the eternal historical verities”. For example, I never would have guessed the massive increase in affordability of, and access to, financial data would lead to an almost complete abandonment of attention to financial metrics and valuation. Yet here we are.

One lesson is, “it matters that the earlier event was broadcast on television and the later one on social media.” Another lesson is, it is very hard to be a leader in technology for a long period of time – because tech does change so dramatically.

Investment landscape

The Green Protocol: A New Vision for Crypto, Pt 2

https://www.epsilontheory.com/the-green-protocol-a-new-vision-for-crypto-pt-2/

“The future is a world of bets, on everything, all the time. So is the present. Absorbed by the speculation layer, ‘the market’ is no longer an exchange for buying fractional ownership shares of real-world companies doing real-world things, but instead is a virtual casino for betting whether the numbers associated with a three or four-letter symbol will go up or down.”

“Absorbed by the speculation layer, ‘sports’ is no longer a venue for passionate support of a team’s real-world competitive success, but instead is a constant exercise in odds-making across every conceivable derivative aspect of the individual competitors and the competition itself.”

This is another very thoughtful piece by Ben Hunt, which is worth reading on many levels, but I highlight it here for the purpose of characterizing the market landscape. The notion of a “speculative layer” helps capture how markets have changed and what it means for investors.

The observation that markets at this stage are “virtual casinos” far more than efficient capital allocation mechanisms has significant implications for long-term investors. Many investment plans rely heavily on stocks and bonds for the bulk of exposure due to the historically attractive risk/reward characteristics of these assets. As stocks and bonds become progressively more speculative, however, the default activity of regularly allocating funds to stocks and bonds is actually making retirement portfolios riskier and more speculative. Further, it is doing so as investors get progressively closer to retirement and should be reducing risk instead.

So, one point is the proliferation of “speculative layers” absolutely increases risk for investors saving for retirement. In doing so, however, it also increases the value of analysis that can disentangle speculative layers from intrinsic value.

Implications for investment strategy

Do physical assets offer investors refuge from inflation? ($)

“Moreover, these assets produce cash flows that usually track inflation. Many property leases are adjusted annually and linked to price indices. Some—those of hotels or storage space, say—are revised even more often. The revenue streams of infrastructure assets are typically tied to inflation, too, through regulation, concession agreements or long-term contracts.”

“That might all sound very alluring, but it should come with health warnings. For one, performance has become harder to predict: think of retail space and office blocks (under threat from e-commerce and remote work), airports and power plants (exposed to decarbonisation) and even farmland (vulnerable to climate change).”

This is a good piece from the Economist with a couple of appropriate and timely lessons. One is physical assets, or more broadly real assets, are a good place to look for protection from inflation. There are a lot of reasons why “Inflation often coincides with rises in the prices of these assets” and the article details a number of them.

Importantly, the article also highlights some of the reasons why physical assets should “come with a health warning”. Perhaps the biggest reason is one the article does not highlight: Many physical assets, especially property, were purchased with large amounts of debt. Further, as borrowing rates have declined to rock bottom levels, the prices of most of these assets have risen to very high levels. As a result, it won’t take much in terms of revenues fading or borrowing costs increasingly to significantly impair the value of some of these assets.

In short, many of these real assets that are supposed to benefit from inflation are also beneficiaries of easy credit which can be extremely vulnerable to tighter credit conditions. It will be extremely important to disentangle which factor exerts more influence.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.