Areté's Observations 5/21/21

Areté (pronounced ar-uh-tay): 1. Goodness or excellence of any kind. Fulfillment of purpose or function, the act of living up to one’s potential. 2. Effectiveness, knowledge.

Market observations

Being well over a year into pandemic-affected markets and just over a year since the first issue of Observations came out, I thought it would be an opportune time to reflect back on some of those observations.

At the time I wrote, “In trying to understand the forces driving this [remarkable rebound in stocks from March lows], a couple of stories stand out. One is that retail investors have re-engaged with stock investing.” The following quote from the FT highlighted the point:

‘Gamified’ investing leaves millennials playing with fire ($)

https://www.ft.com/content/9336fd0f-2bf4-4842-995d-0bcbab27d97a

“New investors have been enticed by stock trading apps such as Robinhood, E*Trade, and SoFi Invest, which offer slick user interfaces, low fees and near-instant account opening … ‘Robinhood has gamified investing. Trading is now so simple that it can be easy to make impulsive decisions’.”

Indeed, substantially increased retail activity was a story through the rest of the year and is still going strong in 2021. The most popular trades have smacked of impulsiveness and a YOLO ethos. Nonetheless, by and large the exposures to risk worked and many retail traders graduated to even more speculative options trading.

While that progression certainly seemed to work for a while, the tide now seems to be turning. Increasingly volatile stock activity and the inherently risky nature of options has caused many amateur traders to learn their lessons the hard way. A good example was illustrated in a story about three photographer friends who had experienced travails in the market that I highlighted in the April 30, 2021 Observations.

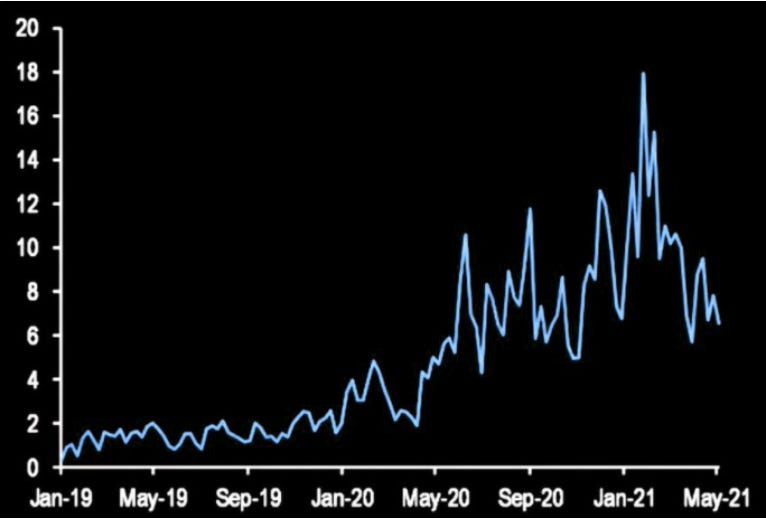

Because it is hard to consistently make money trading, good times always attract new players. Slowly but surely, however, they tend to get weeded out by losing enough money to pose a real threat to their livelihood. This process of attrition of retail traders seems to be proceeding as the graph below shows the decreasing exposures of retail investors to options trades.

Source: themarketear.com

The process of attrition may also be working its way through cryptocurrencies. Wednesday was a wild day for most of them – plunging twenty and thirty percent early in the day, recovering much of that, and then finally selling off again. As themarketear.com reported on Wednesday, in the last 24 hours 775,000 traders had their accounts liquidated on margin calls. In other words, when people use a lot of leverage, attrition can happen fast.

Economy

With so many puts and takes on economic growth, one of the more reliable gauges has been activity. Further, a good leading indicator of activity is comfort. As the graph below shows, the level of comfort people have across various activities has increased substantially in the last four months as the vaccine rollout has continued apace.

Interestingly, this top-down perspective jives almost perfectly with the bottom-up, anecdotal evidence from my regular walks around Philadelphia. Much larger crowds of people are out and about and in many cases activity levels seem very close to those before the pandemic. While a spell of beautiful spring weather has probably been a contributing factor, this is indisputably good news.

Unhedged: the FT’s new email on markets and finance ($)

https://www.ft.com/content/931a6091-a5cf-4a00-bddb-fdf8fe493e6e

“2Q is likely the peak in US real GDP growth . . . There’s also the possibility that 1Q 2022 sees corporate and personal taxes increase, which means there could be not just a slowdown, but a slowdown to below-trend growth temporarily as we start the new year. At a minimum, risk is rising as the year goes on due to the pace of vaccinations slowing (leaving open the possibility of another seasonal health issue by the winter), the large fiscal thrust passing, the possibility of the Fed starting the conversation on tapering, and tax increases.”

As Robert Armstrong points out in his inaugural email on markets and finance, however, there are also reasons to believe economic sentiment is near a peak. Clearly, much of the stimulus is temporary and the potential for monetary and fiscal speed bumps is quite real.

The way growth swings in one period versus another though is heavily dependent on public policy which is inherently uncertain. Will taxes be raised and if so by how much? Will there be significantly more stimulus or are big spending bills now essentially a thing of the past? We just don’t know these things and as such, expectations are likely to ebb and flow as the news changes.

Millennial philanthropy may forever change finance ($)

https://www.ft.com/content/bb84572b-89bc-4cc3-9d0c-5e6121b04191

“this attitude shift suggests that millennials have less tunnel vision when talking about ‘finance’, ‘politics’ and ‘social issues’. Instead, their sense of the economy is interconnected, not least because they do not treat an issue like the environment as a mere ‘externality’ to an economic model, as it was in the 20th century. Therein lies another reason for generational misunderstanding. And, perhaps, a source of hope.”

While there is absolutely a point to be made about the future of philanthropy and values-based investing here, I think the bigger point is the tendency of millennials to view social challenges from a broader, more holistic perspective. Interestingly, this is much more in line with original economic thinkers such as Adam Smith.

An argument that has been made by Jim Grant and many others is that economic policy and much of public policy in general has been hijacked by very narrow thinking which he calls the “PhD standard”. Ideas such as “the only objective of a company is to earn a profit” and the “wealth effect” allows monetary policy to manage economic growth are products of such narrow thinking. The big honking problem, however, is that many of these elaborate economic theories fail to comport with reality.

Worse, many of these elaborate economic theories also have strongly negative consequences which their proponents are reluctant to acknowledge. Until fairly recently, the negative consequences have been assumed away or considered to be “conundrums”. With an increasing segment of the population seeing cause and effect more clearly, and being less willing to suffer such foolishness, policymakers may start being held to account for their failings to a much greater degree.

Public policy/Coronavirus

While the dominant theme over the last year has been the coronavirus, just about any evaluation of what has happened and what can be learned needs to incorporate the role of public policy in its various forms.

In terms of public health measures, responses ranged from dismissive or half-hearted early in the pandemic to extremely intrusive later on. All the while, messaging was extremely inconsistent and misinformation was rampant, and everything was laced with politics. Compliance was all over the map.

As Karen Harris described at the Mauldin SIC, the most striking effect of the coronavirus is “the step change in what is considered acceptable intervention in an emergency and the lower bar for what constitutes an emergency”. In regard to both monetary policy and fiscal spending, more and more money flowed on thinner and thinner pretenses.

What can be learned from looking back? One thing is nothing that actually happened was a foregone conclusion. The implication is that we are in increasingly unstable times and can’t rely nearly as much on heuristics to safely guide us or on reasonable parameters for expected outcomes.

Another is that increasingly activist makers of public policy are continuing to decrease the influence of free market forces. Further, as policy makers exhaust their tool kits, investors also need to assess the increasing likelihood policies will eventually fail. The Fed is an excellent example. The longer the Fed avoids talking about tightening policy as inflationary concerns rise, the more its credibility diminishes.

Politics

The Defenestration of Liz Cheney ($)

https://gfile.thedispatch.com/p/the-defenestration-of-liz-cheney

“But the idea that this [the vote to oust Cheney] was just a tempest inside the beltway tea pot strikes me as profoundly wrong. History is a bit like one of those choose-your-own-adventure books. Small decisions that seem trivial move events, people, and institutions along paths that lead to more choices while simultaneously foreclosing other choices. If you’ve ever read a book about the lead up to World War I, you know this.”

“But ‘inside baseball’ has consequences. The people at that meeting made a choice, and that choice will constrain, create, and close future choices to come. The next time Donald Trump lies about the 2020 election being stolen, Republicans will still have a choice to speak up or stay silent. But the costs of speaking up just went up dramatically.”

I am quoting Jonah Goldberg’s article on Cheney again this week because he hits on something extremely important that almost nobody is talking about. The ouster of Cheney was not just a run of the mill political coup; it was a decision path that opens some opportunities but forecloses others. Those other paths it forecloses are things like evidence-based, bipartisan discussions that can help the country recover from the pandemic. While I don’t want to be alarmist, and it is early in the game and a lot of things can happen, the path to incredibly hostile and dysfunctional politics just got a lot easier while the path to bipartisan compromise got a lot harder.

Geopolitics

Ian Bremmer at the Mauldin Strategic Investment Conference, May 10, 2021 ($)

“We [the US] remain the most powerful country in the world, but we're also the most politically dysfunctional and divided of all of the advanced industrial economies. That means that the legitimacy that we have in promoting free and fair elections, or promoting transparency, or promoting rule of law is less than if it was being done by Canada, or Germany, or Japan, or other systems that are seen as more functional, that are seen walking the talk.”

It is hard to pass up a choice quote by Ian Bremmer who always seems to have illuminating insights into gnarly geopolitical dilemmas. One of the main points I take from this is political dysfunction in the US is beginning to exact a cost in the form of reduced global influence. As a result, less effective leadership creates space for more conflict and more challenges in the geopolitical realm.

China

Almost Daily Grant’s, Tuesday, May 18, 2021

https://www.grantspub.com/resources/commentary.cfm

“Citing sources close to the Chinese government, the New York Times reports this morning that ‘significant losses’ are in store for both domestic and foreign creditors of Huarong. Indeed, Beijing is ‘strongly committed to making sure that foreign and domestic bondholders do not receive full repayment of their principal,’ per the Gray Lady.”

For some reason, the massive significance of China in the investment landscape has been skirting under the radar lately. While the standoff between regulators and creditors of Huarong has potential to send a loud signal one way or another, it is merely a symptom of a broader problem. If China really wants to lower credit growth and establish a more stable financial system, it must lower goals for economic growth. The decision will be felt widely either way.

Real estate

Just as year-over-year comparisons in the stock market are remarkable, so too are comparisons in the real estate market. I put the following quote in the very first Observations on May 8, 2020:

The 90% economy that lockdowns will leave behind

https://www.economist.com/briefing/2020/04/30/the-90-economy-that-lockdowns-will-leave-behind

“In an environment of uncertain property rights and unknowable income streams, potential investment projects are not just risky—they are impossible to price. A recent paper by Scott Baker of Northwestern University and colleagues suggests that economic uncertainty is at an all-time high.”

Indeed, “impossible to price” meant that exceptionally few deals were done which meant there were exceptionally few fire sale prices for comps. The continuation of the recovery through the year helped resolve some concerns, but the announcement of successful vaccines late in the year transformed “unknowable income streams” into knowable ones.

As a result, the prospect for distress in real estate also shifted dramatically. Willy Walker, CEO of Walker & Dunlop, noted at the Mauldin SIC said he was seeing almost no distress: “And there's almost an insatiable appetite for people who say, I will reacquify [sic, re-equify] your project, I'll either buy you out, I'll put new capital into it, but I'm going to give you the opportunity to live for another day”. Yet again the opportunity for value-oriented investors was swiped away.

As people are returning to the workplace another, slightly different, pattern is starting to emerge. For some companies having a centralized, high quality physical presence is an important part of their brand or culture. As a result, demand for those types of properties should remain high. Companies less tied to centralized physical space will require less of it. This is likely to create greater dispersion in the fortunes of commercial real estate.

The property developers still betting on London offices ($)

https://www.ft.com/content/d6b8d468-e339-497d-b165-0de10bcddcae

“What exactly is going on? In dozens of interviews with property executives, investors and analysts, one explanation comes up repeatedly: coronavirus will cleave the office market in two. ‘There will be a clear bifurcation: anything that is flexible, modern and has access to open air will be high in demand and rents will be resilient there, but in the secondary market there will be accelerated obsolescence,’ says Mark Allan, chief executive of Landsec, a FTSE 100 developer with 60 buildings in London.”

“In a recent Knight Frank survey of almost 400 large employers who collectively employ around 10m people, 37 per cent of respondents said that property formed part of their strategy to attract staff. Half said that offices supported their corporate brand and image.”

Inflation

The Mad Mob Has Gone From' Inflation Deniers' To 'Believers In A 5 Year Threat'

https://www.zerohedge.com/markets/mad-mob-has-gone-inflation-deniers-believers-5-year-threat

“This shows the market is very fearful of what happens when central banks inevitably have to tighten.”

The label of “very fearful” as to what the market feels about central bank tightening is an exaggeration, but the graph is informative, nonetheless. Essentially it acknowledges there will be some short- to mid-term price pressure, but the longer-term concern is still deflation. This probably reflects some concern that the Fed will tighten and some concern that fiscal policy won’t be able to continue at the same pace and/or level of effectiveness. Either way, the longer-term inflation gauge is not flashing red yet.

Source: Zerohedge

With shorter-term inflation numbers rising, longer-term numbers still negative, and economic numbers likely to bounce around to the beat of sentiment for fiscal spending and taxing in Washington, inflation expectations are likely to be pretty unstable for some time. This point was highlighted in the April 30, 2021 Observations and is still underappreciated: “The volatility of prices is also an important factor, not just the direction.”

Implications for investment strategy

As a valuation-based investor I have found much of the last eleven years extremely frustrating as have others. As the Fed continued excessively loose monetary policy well after the financial crisis in 2008, it also changed the game of investing from analyzing companies to chasing the “mechanical rabbit” of risk further and further out on the curve. No fun.

While these conditions may persist for some time longer, I am becoming increasingly enthusiastic there is a better way to plough through these challenges for two reasons. One is due to a more thoughtful approach to asset allocation, and one is due to a better set of investment tools.

In the first case, asset allocation is arguably the most important tenet of investing. While most allocations include a wide array of stock and bond exposures, most of those assets are much more correlated than many investors and advisors imagine. This reality was brilliantly illustrated by Chris Cole at Artemis Capital Management and is hinted at in the graph below. Fortunately, as Cole describes, there are more thoughtful ways to reduce cross-asset correlations and therefore improve diversification.

In the second case, the environment of extensive and persistent monetary intervention has created a massive self-fulfilling carry trade. In the short-term, the Fed is creating all kinds of incentives to take risk with stocks. In doing so, however, it is also vastly increasing the risk of a major selloff that can prove devastating over the longer-term. This payoff proposition is actually the antithesis of real investing which entails foregoing immediate gratification for longer-term reward.

Fortunately, a fairly recent rule change by the SEC and the emergence of a new investment company called Simplify Asset Management are combining to turn one of the biggest market risks into a strength for long-term investors. Because of the self-fulfilling carry trade, longer-term options are extremely cheap. Although such options have historically only been available to select institutional investors, they are now accessible through a few different exchange traded funds (ETFs).

This allows Simplify to create funds that not only provide exposure to risk assets but also mitigate the most extreme risks at very cost-effective prices. Combined, the two developments substantially improve the risk/reward proposition for investors relative to most existing products and strategies. With the growing potential for significant disruption in coming years, these are very welcome developments.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates that have more than one side, I try to represent both sides of an argument and to express my opinion as to which side has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue today is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

One goal of this letter is to provide fairly dense information content – so you don’t waste your time filtering through a lot of fluffy verbiage. A consequence of that decision, however, is sometimes things may not be as understandable as they could be.

If you have a general question that may also be useful for others to know the answer to, please make a comment in the newsletter and I will do my best to answer the question or make a clarification. If you have a more specific question, please send it to drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.