Observations by David Robertson, 10/13/23

The week started off with attacks in Israel. The bond market reversed with rates coming down while the stock market basically said, “meh”. It does beg the question, how much bad news can the stock market be inured to?

Also, I will be taking next week off for vacation and will return the following week on 10/27.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Interest rates continued to make headlines as the 10-year Treasury yield shot up and then quickly gave up ground this week. At the same time, the bond volatility index, MOVE, continues to remain elevated. While there is still a lot of uncertainty about the “right” level for rates, and I continue to believe they should go higher, Brent Donnelly interjected some well-needed level-headedness into the debate:

The level of rates matters, too, of course, but quite often the angst comes mostly during the upward repricing of yields and once they find their new, higher happy place people calm down.

Whether yields have found their new happy place or not remains open for debate, but we certainly got a glimpse of what things are like when they aren’t happy.

While there was plenty of volatility in markets this week, the answer you get depends on who you ask. As the graph from themarketear.com shows, bond and oil volatility remain elevated, stocks not so much.

Economy

Last Friday, the jobs report came out with unexpectedly strong headline jobs numbers and stocks took a dive. After taking some time to digest the full report, weaker wage growth and a higher proportion of part-time jobs drove stocks higher. Same report, totally different reactions.

This is a microcosm of the economic and market environment for the last year or so. Good numbers drive stocks up one day and bad numbers drive stocks down the next. It is also a continuation of the environment of mixed signals I described six months ago:

On one hand, the financial economy is going to be a constant fire fighting brigade for the foreseeable future. There is no easy way out.

On the other hand, the consumer economy is holding up relatively well. There will be ripple effects for sure - tighter lending standards will impede consumer spending and unemployment will rise, but mostly these two different parts of the economy will be on different trajectories

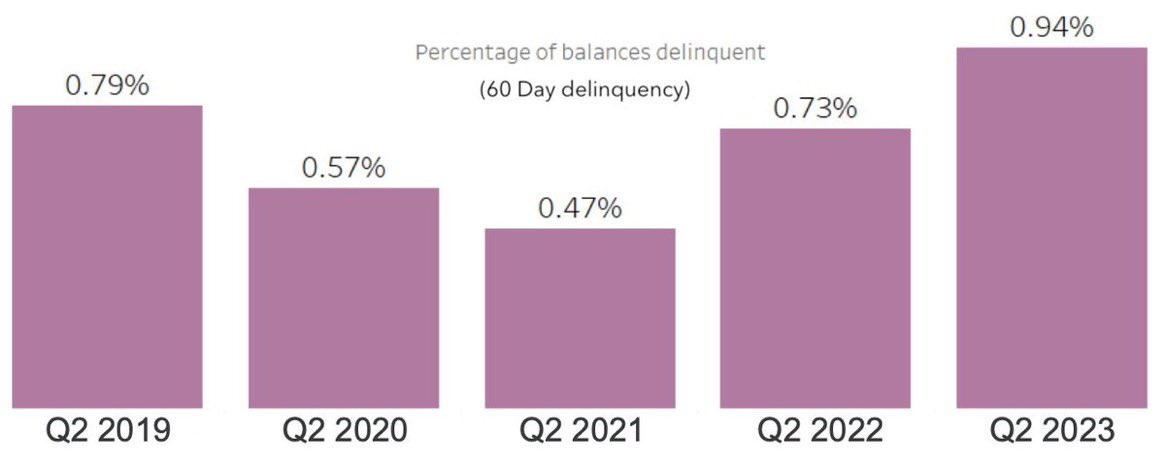

The choppiness in the economy continues apace. One of the many financial headwinds is appearing in the form of increasing credit problems. For example, CarDealershipGuy highlighted the rising trend in auto loan delinquencies on X:

It is important to take all of these signals in context. As CarDealershipGuy assesses, the auto loan delinquencies are “Not a crisis but concerning trend”. The same is true for other credit trends such as bankruptcies. Yes, they are going up. Yes, it is a concerning trend. No, it is not a crisis. And, by the way, bankruptcies were artificially suppressed by low rates for over a decade.

While it is important to monitor the progress of the economy under a higher interest rate regime, it is also important to not overreact. While credit is getting weaker, wages and consumer spending are holding up alright. It is more useful to think of these as offsetting forces in the economy than to consider the economy as one hegemonic force.

China

There is a social media meme that goes something like, “How do you indicate _____ without actually saying it?” In the case of China, it could go, “How do you indicate the country is, or is becoming, uninvestable for other countries?” without making such a blatantly off-putting statement?

It sounds like we have an answer. As Almost Daily Grant’s reports (from Friday, October 6, 2023):

Beijing’s tough treatment of foreign companies this year, and its use of exit bans targeting bankers and executives, has intensified concerns about business travel to mainland China. Some companies are canceling or postponing trips. Others are maintaining travel plans but adding new safeguards, including telling staff they can enter the country in groups but not alone.

“There is a very significant cautionary attitude toward travel to China,” said Tammy Krings, chief executive of ATG Travel Worldwide, which works with large employers around the world. “I would advise mission-critical travel only.”

Plenty of companies and investment shops are bending over backwards to rationalize their continued involvement with China. Sunk costs and abstract arguments can forestall the difficult decision for some time.

The warning signs are becoming progressively harder to ignore, though. As Almost Daily Grant’s concludes: “Foreign executives are scared to go to China. Their main concern: They might not be allowed to leave.” Message delivered. Message received.

Geopolitics

The Hamas attacks on Israel over the weekend rightly attracted a lot of attention and concern. While much of the news has focused on learning just what happened, why, and where things are going, the incident also serves to remind of us of the broader geopolitical context in which it happened.

One factor is deglobalization. While there has not been a wholesale withdrawal of US military support across the world, the US has clearly refocused its priorities closer to home. In addition, both China and Russia have become preoccupied with domestic economic weakness and have been forced to limit international entanglements. The result has been to create, on the margin, something of a power vacuum. For those who are interested in causing problems, there is an incrementally better opportunity to do so.

Another factor is the continued strength in the US dollar (USD). USD strength imposes the greatest hardships on emerging market countries which suffer in a multitude of ways. At a higher level, credit becomes more expensive and trade becomes more difficult. At a grass roots level, many basic commodities like food and fuel become much more expensive. While these dynamics often fail to make international headlines, they certainly can agitate populations.

The bottom line is geopolitical risk has risen. The Hamas attack serves as a stark reminder.

Inflation

Producer prices came out Wednesday and were up 0.5% sequentially, which was on the high side. Normally producer prices lead consumer prices so this is not an encouraging indicator for the direction of inflation. Regardless, both bonds and stocks were up on the day.

The CPI report is due Thursday but I will be on the road so won’t be able to comment on it, at least not this week. As a single data point, it shouldn’t have much effect on the market, but given the high level of complacency right now, an unexpectedly high number could force investors to rethink the trajectory of inflation.

Investment landscape I

"Capital Light" is a Trait of the Cycle as well as the Industry

https://www.thediff.co/archive/capital-light-is-a-trait-of-the-cycle-as-well-as-the-industry/

All of that effort—again, all of which is in the fantastically high-margin, low-capital-intensity world of software—creates three new ongoing costs:

There are so many features, and so many interactions between them, that the size of documentation balloons. There's also a trickier marketing question, because the marginal new user of the product is not someone looking for the original core feature, but someone trying to integrate that feature into specific workflows. As their needs get more specific, broad advertising works worse, and hyper-targeted search ads whose keywords indicate an immediate propensity to spend get expensive.

The cost of user support also rises, and the amount of information support staff need goes up. They're no longer helping customers use a single product; they're helping them debug the surprising interactions between different products.

Even worse, these other products are constantly evolving; the price of maintaining a single piece of software that doesn't plug into anything else can be low, but the cost of making sure it continues to cooperate with everything else is not.

One point of this little exposition on the software industry is that properly accounted for, software businesses need to keep investing in their businesses in order to maintain their value. Just because a number of those “investments” appear as operating expenses in accounting statements and not as capital expenditures doesn’t change the business reality. Nor does it change the fact that assets, albeit intangible, are being generated.

Another point is just like with more tangible asset intensive businesses, ongoing maintenance spending is required to maintain the value of the asset and therefore the franchise. As Hobart rightly notes, software will eventually start looking a lot like more (tangible) capital-intensive businesses:

Absent excellent management, government protection, or extraordinary good luck, the industry's economic balance sheet, as opposed to its accounting balance sheet, must end up looking like that of a capital-intensive industry like airlines.

Finally, in the event economic conditions get tougher, some companies will choose to maintain operating margins at the expense of maintaining investment in the business. This will create opportunities for differentiated performance for both companies and investors, just like in other industries.

Investment advisory

Investors should fight the temptation of cash ($)

https://www.ft.com/content/49c1df89-7890-4643-920b-10443a05592e

In this scenario [recession], the cash rate does not stay at today’s elevated levels as central banks, convinced their work is done, start to ease their foot off the brake. Bond markets factor in more interest rate cuts than are currently priced, which would send bond prices higher. An investor who bought a 10-year US Treasury bond at a yield of 4.5 per cent would see a total return of roughly 13 per cent if that yield fell 1 percentage point over 12 months.

So, the case here is that investors should forsake the temptation to take shelter in cash at an attractive yield. Instead, investors should count on a recession, accurately anticipate the Fed lowering rates in response (despite ongoing inflationary pressures, not least of which is too much money), and reap in the capital gains of bond prices. Bingo, bango, investing is a piece of cake!

Now, there happens to be no mention of the fact that term premia are still extremely low relative to historical norms - which means there is a good chance bond prices can continue to fall. Nor is there any mention of inflation expectations. If those expectations went up just a bit, they would cause more damage to bond prices. Oh, and by the way, the actual performance of bonds the last three years has been breath-takingly awful. But hey, that’s all technical stuff that “retail” investors don’t really care about, right?

Let’s also throw in the fact this commentary is written by a senior executive at a large financial institution, JP Morgan. Institutions like that make their money by selling financial “products” to people. They don’t make much money at all if those people prefer to keep savings in cash.

And this is the thing that always rankles me. Once you see a large financial institution from the inside, it is hard to unsee its inveterate need to gather assets and sell products. This certainly doesn’t mean everything that comes out them is a lie or a gross exaggeration, however.

One thing it means, though, is that everything they say is a sales pitch that often obfuscates or avoids even more important considerations. If you want the “whole truth”, you’re going to need to do more work. Another thing it means is they aren’t sending out investment reports to help you produce better outcomes. Nope, they are doing that to sell stuff.

Investment strategy I

The Death of Bonds? ($)

https://www.yesigiveafig.com/p/the-death-of-bonds

My hunch is that the Fed breaks something, starts cutting rates and suddenly the world reawakens to the reinvestment risk of cash. As the yield curve re-steepens, it becomes easier to finance long-dated bonds, further raising demand.

I don’t agree with Green’s position that inflation will continue to decline but he makes an important point here: The prospect of “the reinvestment risk of cash” is a real risk, and especially so for those of us who are holding a large proportion of cash.

One point to make is reinvesting cash will involve something of a call on timing. As unfortunate as this is, by itself it is not a valid criticism of holding cash. When the Fed decided to continue Quantitative Easing until well after crisis conditions demanded, it baked into the cake the necessity of “timing” the eventual return to more sustainable conditions. All you need to do is look at the colossally bad performance of Treasury bonds over the last three years to see how the Fed imposed a timing requirement on investors.

Another point is that such a timing decision doesn’t require the pinpoint accuracy of a savvy hedge fund trader. Rather, it is the kind of thing that really just falls under the purview of “active” management. This type of decision is part and parcel of judging the relative attractiveness of major asset classes and allocating accordingly. It’s not easy, and should not be done haphazardly, but nor is it virtually impossible to position an allocation so as to reap the best returns the market has to offer.

Finally, the exercise of managing cash holdings can be thought of mainly as an exercise in risk management. Given a choice, what seems less risky: Trying to time the exact moment when overvalued stocks and bonds turn south, or gradually redeploying cash as financial assets become cheaper? To me, the latter is far easier to implement. While neither exercise is without its downsides, these are the choices we have been given.

Investment strategy II

When I transitioned the investment strategy for Areté Asset Management over to the All-Terrain allocation strategy from the mid-cap strategy in the latter part of 2021, one of the main reasons I did so was to improve the translation of the research and analytical work I was doing into better performance. The fact was, this was not happening through stock selection. Not for me, not for anybody.

For a number of reasons, the investment landscape became such that it was dominated by macro themes. A policy position of low rates and a trend in the proliferation of passive funds were primary contributors to this condition. Regardless, the result was the nearly complete devaluation of stock research.

What it opened up, however, was an opportunity to identify and exploit broader macro trends. Fortuitously, some securities rulings also enabled pioneering fund management companies to design certain exposures into exchange-traded funds (ETFs) that had previously been the exclusive purview of institutional investors.

One of the best, and most successful, representations of this movement is the ETF, PFIX by Simplify Asset Management. It was designed to provide a hedge against interest rate increases at a time, in early 2021, when the 10-year interest rate was historically quite low at about 1.5% and at a time when bond volatility was also low, so options were cheap.

So, one point is PFIX has worked out quite well so far. At a time when higher rates are deflating the values of long-term Treasuries, real estate, and other long duration investments, PFIX has performed exactly as advertised by offsetting those losses.

Perhaps the bigger point, however, is that PFIX, and other similar funds, have opened the door to a larger universe of return and diversification opportunities that had previously been inaccessible to non-institutional investors. This is a very welcome development!

Implications

With the massive volatility in bond yields recently, the continued high valuations for stocks, and the vivid reminder of geopolitical conflict, it seems to be a good time to review risk management.

One point is that risk assessments may be biased by the recent history of financial crises that have always driven bond yields down. This is a point John Hussman made earlier in the year:

A longer-term question - given 10-year trailing nominal GDP growth is among the best correlates of 10-year Treasury yields (yes, investors can be backward looking that way) is it possible that prevailing bond yields reflect "anchoring bias" that relies on crisis after crisis?

In other words, it is distinctly possible that investors’ range of expectations for bond yields is biased to the low side because of what has happened in the past. That would imply they may be poorly positioned for higher yields in the future.

Another perspective, which is consistent with this possibility, is that investors have become conditioned to react to messaging from policymakers rather than to proactively position themselves. The assumption is that policymakers won’t allow really bad things to happen.

As students of complex, adaptive systems know, however, there is just no knowing which snowflake is going to start off the avalanche. Rather, you have to recognize the potential and avoid the area.

Could it be that investors are traipsing through avalanche territory expecting policymakers to warn them before anything bad happens? It certainly seems that way. Perhaps it will take a few accidents to get the risk management engines fired up again.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.