Observations by David Robertson, 10/27/23

It was a busy week, let’s jump in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The yield on the 10-year Treasury hit 5% early on Monday and then quickly reversed. The reversal coincided with a comment from Bill Ackman that he was covering his short on Treasuries due to increased geopolitical risk and a comment from Bill Gross that recession is imminent.

While these are both accomplished investors whose opinions carry weight, they are also both people who have demonstrated in the past that they are not above using their prominence for personal benefit. Nor should any single investor be able to exert such influence on the Treasury market. No, the big moves in yields after the comments says something about how unhinged the bond market is right now.

To that point, discussions about volatility have been heating up too. While volatility (here I am talking about stock volatility) has been spiking, the less-discussed element is the degree to which volatility has been artificially suppressed. This has happened by way of large funds that sell/short volatility in order to generate income. This is akin to selling insurance to earn a premium.

Kris Sidial highlighted the phenomenon recently. Quoting a Bloomberg article, Sidial reports, “options-selling strategies this year … are sucking in billions of dollars like never before”. The story also says, “Derivatives specialists at firms including Morgan Stanley and Nomura Securities International have also argued that options-selling funds are acting as a market tranquilizer”.

As a result, for the spikes in volatility we have seen, those spikes most likely understate the underlying fundamental volatility. This creates a risk. Sidial summarizes, calling the short volatility trade “one of the biggest hazards to the broad market and it seems like its a topic that is just flying under the radar.”

The bottom line: Don’t be surprised to see a sudden, dramatic unwind of the short vol trade at some point that causes an eruption in volatility akin to the Volmaggedon event in February 2018.

Economy

Just as the bond market was getting comfortable with the economy slowing down, the CPI report came in hotter than expected. Then retail sales also came in hotter than expected and yields jumped up again.

At the same time, however, anecdotal evidence of worsening credit continues accumulating. For example, Randy Woodward posted that a credit union he works with was “seeing a serious spike in auto loan defaults”. While “Only 1% of their loans were originated with a subprime FICO”, they discovered the scores of those borrowers today “is now 10%”. It appears as if Covid stimulus checks temporarily improved the credit scores of many borrowers, a factor many lenders did not take into account at the time.

Once again, the evidence points to a lot of cross currents in the economy. Is credit getting weaker? Yes. Is part of this weakening trend due to the expiration of temporary Covid benefits? Yes. Is the economy, broadly, still doing fairly well? Yes again.

One point to take away is that as the economy continues to transition away from being driven by credit growth, there will be a difference in the trajectories of businesses and consumers that rely heavily on cheap credit and those who don’t. Having too much debt is likely to be quite painful. Another point, however, is that those who do not have too much debt should be able to carry on without too much trouble.

Technology

The Morals of Techno-Optimism

We believe the techno-capital machine is not anti-human – in fact, it may be the most pro-human thing there is. It serves us. The techno-capital machine works for us. All the machines work for us.

Marc Andreesen, the venture capitalist, recently published a manifesto on technology which John Authers commented on. The basic point is technology is wonderful. It saves lives and makes the world a better place. Oh, and if you do anything to thwart the advances of technology, you are making the world a worse place.

It’s not unusual for people in technology, or anywhere else, to talk their book. The technology world, however, is at least somewhat unique in its grandiose and uncritical fantasies. Sometimes these advance into what could be called “Toxic Techno-Optimism Syndrome” (TTOS). I do believe this is a thing in Silicon Valley whereby otherwise intelligent people become overwhelmed by a combined sense of optimism and self-importance and become delusional.

It could be that Andreessen has long been suffering from TTOS, but it has taken a turn for the worse recently. Or it could be that in the absence of free money, a lot of venture capital money invested into tech startups is getting burned up. Indeed, the possibility certainly exists that all that wealth creation over the last fifteen years was not so much due to Andreesen’s technical brilliance, but rather was mainly a function of cheap money.

Perhaps the immovable object of Andreesen’s ego is meeting the irresistible force of higher rates blowing up the business models of tech startups?

A final point to make on the subject is that while technology absolutely can serve many useful purposes, the degree to which it does so is contingent upon the environment. It is not an absolute good.

This is a point I made in regard to Neil Howe’s Fourth Turning thesis. Society has different priorities across the four different phases/generations of a typical human lifetime. During some stages, society is cohesive and effectively deploys technology to serve society as a whole. During other stages, technology is more likely to serve individual pursuits, often at the expense of greater society.

The unsatisfying, but more realistic evaluation of the usefulness of technology is, “it depends”. The dangerous evaluation of technology is to uncritically believe it is always good when it is actually causing harm.

Monetary policy I

Who’s in the Driver’s Seat, Powell or Bond Yields?

Perhaps critically, while Powell seemed to think that higher yields meant there was less need for another hike, he appeared intensely relaxed about the widespread belief that he will need soon to try to push longer-dated yields downward. He gave a number of explanations for the rise, including higher government budget deficits, which he stressed are on an “unsustainable” path. At the margin, higher long-term yields could mean less need for the Fed to hike, but he stressed he wasn’t “blessing” any particular level of longer-term rates. Instead, he said that policymakers would let the rise in yields “play out” and watch what happened.

“It’s appropriate to have a little bit of humility,” Powell said, because few people are confident they understand what is happening.

Last week Fed Chair Jerome Powell gave a speech that revealed some incremental insights in the Fed’s thinking on monetary policy. Namely, after a prolonged period of explicitly implementing policy to artificially suppress rates, the Fed now seems to have little concern with long-term rates rising rapidly. Further, in regard to higher long-term rates, Powell said, “There is no playbook,” indicating a large degree of indifference to the move.

One takeaway is that Powell is simply recognizing the many factors affecting long-term rates that are outside the Fed’s control. The Fed is not omnipotent. Fiscal policy and Treasury issuance are also important factors in long-term rates. Of course, this also means inflation is not totally within the Fed’s control either. Indeed, longer-term inflation expectations are beginning to go up again.

Another takeaway is this change in the Fed’s demeanor, from micro-management of rates to indifference, is unnerving to a lot of investors. As Authers put it: “Any signal that the Fed is worried that something in the financial system is about to ‘break’ would have been the green light for mass buying of bonds, and a fall in yields. He offered no such signal …” It looks like investors will need a new playbook too, one that is more sophisticated than just following what the Fed says.

Finally, it is hard to read Powell’s comments and not hear a persistent effort to avoid blame. While Powell was perfectly happy to promote the Fed’s ability to keep rates down after the GFC, now he is offering a litany of excuses as to why higher inflation and higher long-term rates are not his fault. While nothing less should be expected of a consummate political animal like Powell, that shouldn’t be encouraging for inflation expectations.

Monetary policy II

Projecting the Quarterly Refunding Announcement

https://johncomiskey.substack.com/p/projecting-the-quarterly-refunding

I think the TBAC charge that was included in the August QRA, specifically the future issuance scenarios, is analogous to one of those [software] bug error messages. I think its basically Treasury telling us what the future coupon issuance is going to be through next summer. Not precisely, but close enough to get a very good idea of the coupon supply coming in Q1, Q2, and Q3 of next year (and of course the remainder of Q4 this year).

There are times when it is important to step back and view the landscape from a high level perspective in order to appreciate the broad contours of change. There are also times when it is important to get deep into the weeds to understand the details.

John Comiskey seems to relish delving into the details of Treasury funding and thank goodness, because Treasury funding has fairly quietly been a driving force of the rising yields on Treasury bonds. To wit, the yield on the 10-year Treasury had remained within a band between the low-3s and 4% until the end of July. When the Treasury recommended financing report came out in early August, showing substantial increases in bond issuance, rates started a fairly steady climb to 5%.

So, one interesting point is “Treasury [is] telling us what the future coupon issuance is going to be”. I think this is right. It does not appear to be mysterious or conspiratorial. As Comiskey observes, “like error messages in code, sometimes you just gotta read the lines themselves, not between them”.

Another interesting point is “we have quite a bit more coupons to come”. Coupon issuance for the third quarter was $178B and is jumping to $347 in the fourth. But wait, there’s more. According to Comiskey, coupon issuance should be around $417B in the first quarter next year, $574B in Q2, and $675B in Q3. That’s a jump of almost 300% in a year’s time. Also note, these are Treasury decisions that affect long-term yields that affect financial conditions. The Fed can only watch.

While the increase in long-term rates in the third quarter almost certainly involved some front-running, the real test of where yields should be will come when investors are actually forced to sell other assets in order to absorb the massive increase in Treasury coupon supply. As I said back in early October, “This is where the rubber hits the road” in terms of price discovery. Finally, as a friendly reminder, the new quarterly refunding updates will be out next week. I don’t think the market has priced in all the extra supply that will be coming out.

Inflation

A lot of debate over whether inflation is rising or falling is based on various modification of the CPI number. What is really important, but often lost in the shuffle, is the measure of inflation expectations at some point in the future. For example, the 5-year, 5-year forward inflation rate has been inching higher since early summer (h/t Ole S Hansen).

The interpretation is fairly straightforward: Despite the zigs and zags of inflation in the short-term, investors are beginning to price in higher inflation in the future.

Another interesting point on inflation was made by Joseph Wang. He notes, “Median inflation expectations are moving towards 2%, but that hides significant dispersion. A sizable fraction of households and businesses now persistently report higher expectations.”

The quick and dirty interpretation is that even though the median expectation appears very much in line with the Fed’s inflation goal, that 2% level does not appear to be a very stable target. Of course, we’ll have to wait and see, but there is no reason to rest easy that inflation is acquiescing.

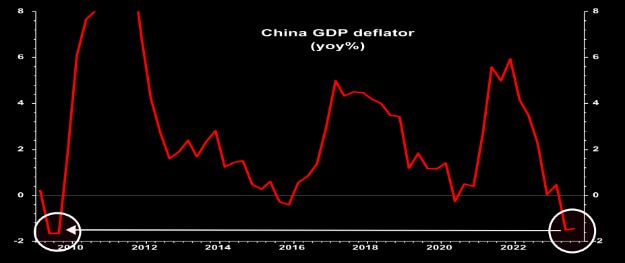

If that isn’t enough to digest on the inflation front, the following graph from themarketear.com ($) complicates things further. This is yet more evidence China is slipping into deflation.

This creates an interesting prospect. What if Western economies experience moderate, but above target inflation, while China experiences deflation? Certainly that would put a lot of pressure on Chinese debt holders and one would expect to eventually see the effects ripple into the currency market. Could get interesting!

Investment landscape I

One of the things that can be easy to lose track of in the investment landscape is how tradeoffs among different asset classes evolve for different types of investors. As Florian Kronawitter highlights, there is “‘significant interest’ among pension funds to cut equity exposure, lock in yields”.

Indeed, as yields go up, the liabilities of pension funds typically go down. When liabilities go down, there is less desire/need to take on risk. As a result, higher yields create a very rational inclination to reduce equity holdings and increase bonds.

This creates a very real risk for stocks that a lot of investors can miss because the decision-making calculus is different from their own.

On the topic of risk, Michael Pettis recently commented on the real estate crisis in China. In channeling the economist, Hyman Minsky, Pettis explains, “much of the Chinese economy – not just developers, but also other businesses, banks, and households – were...forced by surging prices and normally-distributed risk taking to bet implicitly or explicitly on a continued surge in property prices.”

In short, if you are caught in an environment of relentlessly rising prices, you need to keep paying up just to stay risk-neutral. This has the effect of both perpetuating the rise in prices, and also broadening the effects throughout the economy. The process is really fairly mechanical; no ill-intent or unseemly greed are required.

Ultimately, once prices stop rising, the consequence is people get “surprised by the extent and spread of financial distress”. One point, then, is there is a lot more financial distress coming in China. Another point is exactly the same situation exists with stocks and other risk assets in the US.

Investment landscape II

Friday Speedrun: October 20, 2023

https://fridayspeedrun.substack.com/p/friday-speedrun-october-20-2023

Everyone was calling for a recession and US growth is printing 6%ish for Q3. Rarely has the market been so wrong for so long on the trajectory of the US economy.

Brent Donnelly makes a few great points here in two short sentences. First, a lot of people have been wrong about an imminent recession and also wrong about interest rates. This can happen. While it may feel more comfortable to be amongst the majority, that doesn’t inherently mean the majority is right. Sometimes, in order to perform well, you need to do things differently than the crowd.

Second, part of the reason why so many people have believed in recession is because some prominent thought leaders - like Lacy Hunt, David Rosenberg, and Gary Shilling - have been arguing for it. I happen to have a great deal of respect for each of these people, and happen to agree with most of their logic. However, my outlook diverges from their’s in that I don’t believe the economy is basically being left to fend for itself.

Instead, I believe the government has taken a much more active role in dictating the path of the economy. With the US dollar as global reserve currency and with Covid proving the political utility of more activist policy, the US government has considerable resources to tilt the scales in its favor. In short, economic growth has become more a function of political preference than fundamental reality.

Finally, one of the key reasons for expectations of low growth is deteriorating credit conditions. Indeed, weakening credit has been a leading indicator of economic trouble, especially over the last forty years when credit growth exploded at a much faster rate than economic growth.

The growth in credit (as opposed to growth in investment and productive capacity) as the major driver of the economy was highlighted in the Economist over ten years ago. I even highlight the importance of credit in determining asset prices right on the Areté website. Insofar as the economic model is shifting from creditism back to capitalism, which I believe it is, deteriorating credit is likely to prove a less effective leading indicator for the economy than it has in the past.

Investment strategy

The Kobeissi Letter recently posted median returns by asset class:

High Yield Savings Accounts: 5.5%

6-Month Treasury Bill Yield: 5.0%

Investment Property Cap Rate: 4.5%

S&P 500 Earnings Yield: 4.2%

The assessment is that “Cash and Treasury Bills are now paying a HIGHER yield than real estate and the S&P 500. Similar messages were put out recently by Nick Gerli and Jim Bianco. In short, “risky assets are paying less than risk-free assets.”

This is absolutely true and a good reminder that yields and returns on various asset classes do change in different environments - and that can massively affect their relative attractiveness.

There are two important implications for investors. One is there are occasionally opportunities to realize substantially better risk/return propositions in the market. Now is one of those times. Cash, i.e., short-term Treasuries, are yielding more than much riskier assets like stocks and real estate. Major mispricings like this don’t happen very often.

Another implication is the striking risk/return differentials illustrate a major flaw with a lot of asset allocation models. A large proportion of those models rely on static, “long-term” returns of asset classes to determine allocations. However, the expected returns at any given time, based on current yields, can vary substantially. This is one of those times when static models produce recommended allocations that are significantly out of sync with current conditions.

Implications

The Grant Williams Podcast: The End Game: Episode 46, James Aitken ($)

https://www.grant-williams.com/podcast/teg-ep-46-james-aitken/

James Aitken did a great job summarizing some of the key implications in this market in his interview with Grant Williams and Bill Fleckenstein. As a result, I will highlight some of his insights and riff on those:

But I need to be open-minded here. I need to unlearn things. I need to think differently about the world if for no other reason than fiscal policy is all in.

And I think one of the key things people are struggling with is we thought we knew how monetary policy transmitted to the real economy.

Yup. I think most of us, certainly me included, would have guessed the economy would be crumbling right now and financial accidents would be happening all over the place with rates where they are. It’s not happening, at least not yet.

A key distinction is that “fiscal policy is all in”. In my own thinking, I am acknowledging the lower than expected impact of monetary tightening on financial conditions and therefore reducing my expectation of a recession in the near-term. I had been working from the normal political economy playbook, but, as Aitken suggests, I also “need to think differently about the world”.

Every day, we see this pitch battle over the next 10 basis points in core PCE. I mean, it’s great for eyeballs perhaps, but it’s like why are we obsessed with the next 10 basis points in core PCE, or three-month annualized ... People go on and on and on. You know why? They’re trying to pick the bottom. “Oh, this is it. This is the turn. The US consumer’s tapping out.”

It’s true, there is an awful lot of jabbering about a few basis points of inflation one way or the other. I think Aitken makes a great point - the only reason for nitpicking over such fine details is to try to time the market. This is an indication of an investor base habituated to speculating on directional bets. It does so because there has been such a dearth of fundamental anchors.

Insofar as the policy goal is to transition to a sustainable rate environment, however, there is a fundamental anchor. For 10-year Treasury yields that looks something like nominal GDP. On Thursday, that number came in at 8.5%. While that was definitely a bump up from the prior quarter, it gives an indication 10-year yields (currently about 5%) are not yet as high as they need to be.

Bank of Japan JGB purchases were the global suppressant of term premium, which is just a fancy way of saying, so huge were the Bank of Japan’s JGB purchases that they suppressed long-term bond yields everywhere, as intended.

So if anything ever changed there, we needed to be mindful because there might be some consequences for long-duration government bonds around the world.

This a good healthy reminder that what happens with US Treasury rates isn’t entirely determined within US borders. Excess Japanese savings have lowered yields around the world. As Japan appears to also be working toward a normalization of rates, capital flows and yields on financial assets will almost certainly be affected. Don’t say you weren’t warned.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.