Observations by David Robertson, 1/19/24

While the market had been projecting a calm, cool exterior, visible signs of anxiety emerged this week. Let’s take a look.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

After the holiday on Monday, Tuesday started off with a bang for the 10-year Treasury with the yield rising 13 bps to 4.08 before tailing off a bit at the end of the day. The US dollar also jumped almost 1%. A weak auction of 20-year bonds on Wednesday drove yields up again and longer-term yields pushed even higher on Thursday. At very least, the moves seemed to reflect a reversal of positions that had become quite extreme at the end of the year.

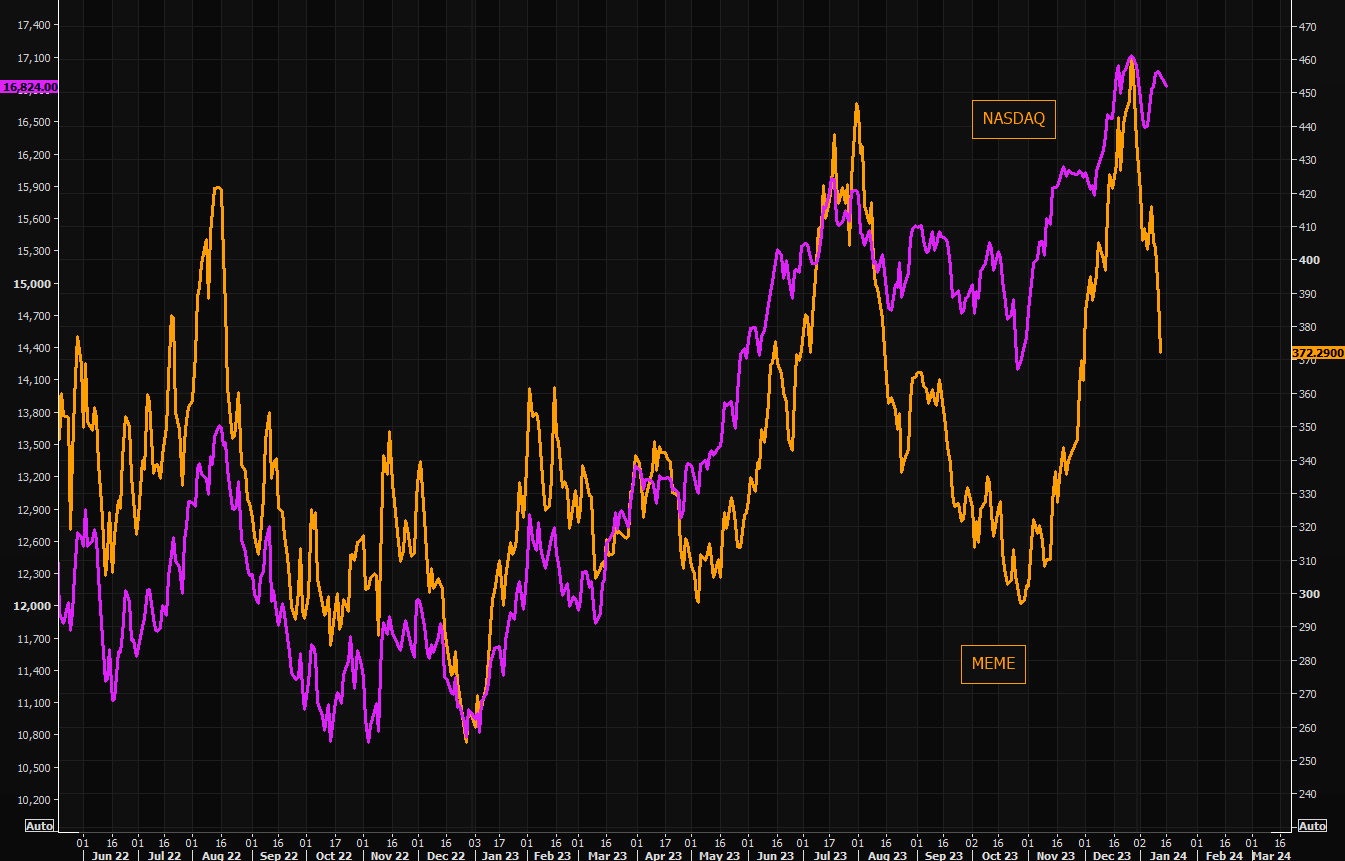

Another big change that is hitting the radar is the massive decline in meme stocks. As the themarketear.com shows, Nasdaq has tended to move in line with meme stocks but with lower volatility. Given that meme stocks were a canary in the coal mine in 2022, the recent decline warrants concern for broader market indexes.

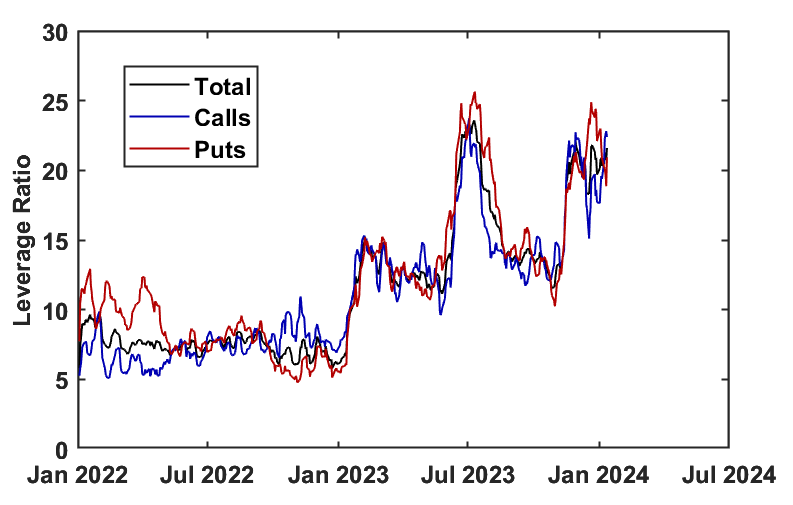

Another post by Dr_Gingerballs illustrates one of the more important, but probably less appreciated aspects of current markets: Derivatives are the tail wagging the market dog.

The upward trending lines represent leverage in derivatives contracts. This happens for a reason: “As more people get into the short vol trade, more leverage must be taken to achieve similar returns.” Just like with a drug, there are diminishing returns.

Also just like a drug, consumption tends to keep increasing until something gives. This phenomenon provides two interesting observations on markets. One is that an important part of the reason stocks keep marching up is because of the short vol (volatility) trade. Another is that these conditions are inherently unstable and prone to blow up. So we have that going for us.

Economy

Growth Slowdown & Inflation Comeback Will Be The Key Turning Points For 2024 | Lakshman Achuthan

https://adamtaggart.substack.com/p/growth-slowdown-and-inflation-comeback

We expected there to be a more obvious hard landing in 2023, and so far that didn’t present itself.

So the drivers of the economy, the cyclical drivers that underlie and anticipate kind of directional moves in the economy - those were all recessionary.

So, what’s the noncyclical stuff that’s at play and the number one item is very, very tight labor supply.

The typical pattern of government spending and stuff is that it ramps up and plugs a hole during a recession … and here that whole thing is happening before a recession.

Achuthan finds himself in good company for having expected a recession in 2023. Where he distinguishes himself is so clearly explaining why that didn’t pan out. The cyclical indicators were all pointing down - and they weren’t wrong.

The cyclical indicators were overwhelmed by two other factors though. One, the labor market was unusually tight and it was unusually tight because of the pandemic. Two, huge government spending propped things up. What was especially unusual this time around was the big spending occurred before a recession, rather than as a response after recession hit.

This unusual situation created something of a rug pull for analysts who had recession dead in their sights. They weren’t wrong on the economics, but economics wasn’t the only thing that mattered.

What was wrong, and what I have been arguing for well over a year now, is that politicians are not going to let recessions happen if it presents a real threat to them getting re-elected. As a result, recessions are now more political phenomena than economic ones.

As an interesting addendum to the discussion, the FT ($) recently posted a story on “Resurgent US electricity demand”:

US electricity demand is booming after years of stagnation, driven by emerging technologies such as artificial intelligence and electric vehicles and prompting warnings over the stability of the power grid.

Grid Strategies, a US consultancy, said that nationwide forecasts for electricity demand growth over the next five years had “shot up” from 2.6 per cent in 2022 to 4.7 per cent 2023, in a report based on an analysis of utility filings to the Federal Energy Regulatory Commission.

For one, electricity demand tends to be a fairly good indicator of economic growth. As such, if the numbers are close to being correct, electricity demand points to healthier growth ahead. This is an interesting counterfactual to declining cyclical economic indicators.

For another, “booming” electricity demand from high-tech industries is exactly the kind of narrative one would expect to hear from an administration that very much wants to get re-elected. I certainly wouldn’t take the statement at face value, but I wouldn’t completely discount it either.

Credit

What Lies Beneath, Almost Daily Grant’s, Tuesday, January 16, 2024

https://www.grantspub.com/resources/commentary.cfm

The water remains warm for speculative-grade corporate bonds, as the ICE BofA High Yield Index settled Friday at a 7.49% effective yield, down nearly 200 basis points from its late October levels.

Such euphoria was on full display in the deep end of the pool, as the Caa-rated portion of the Bloomberg U.S. High Yield Index rode that late flourish to a near 20% total return last year, marking its best annual showing since 2015.

It’s interesting to juxtapose the credit environment to the economic one. Caa bonds, which are those with some combination of high debt loads, poor cash flows, and volatile industries, i.e., the most vulnerable members of the credit world, had a blowout quarter. This happened just as the economic outlook was darkening.

The easiest explanation, and I think the best one, is the expectation is that slowing growth means more support from monetary policy - which means rising risk assets. I continue to believe monetary policy has been repurposed and the Fed is no longer in a position to continually boost risk assets.

Either way, the performance of low grade bonds are likely to be a good indicator of policy direction. If those bonds keep doing well despite weak economic performance, it would indicate the continuation of central banks providing a protective cover for risk assets. If low grade bonds start cracking as growth slows, however, it would indicate a new regime in which credit expansion is no longer the dominant mode of growth.

Eurozone

Germany was worst-performing major economy last year ($)

https://www.ft.com/content/792a1a09-701c-4c9d-aa77-0d9575d5bda9

German output contracted 0.3 per cent last year as high inflation, rising interest rates and elevated energy costs made Europe’s largest economy one of the weakest performers in the world, according to an initial estimate released on Monday.

“Overall economic development faltered in Germany in 2023 in an environment that continues to be marked by multiple crises,” said Ruth Brand, president of the federal statistical office.

Some time around the fall of 2022, after the initial shock of rising energy prices from the Russian invasion of Ukraine, the broader Eurozone area started taking victory laps for having mitigated the threat.

At the time I was extremely skeptical and posted in the September 9, 2022 Observations that “The economic pain of higher energy and power costs … has not yet been distributed to the ultimate bag holders. Much of the pain will fall on consumers and businesses, but much will also be laid off on to taxpayers.”

Here we are about a year and a half later, and economic development in Germany is being “marked by multiple crises.” This should not be a surprise. The pain was deferred and now it’s coming due. This will affect growth, but it will also affect inflation and relative currency strength.

Politics

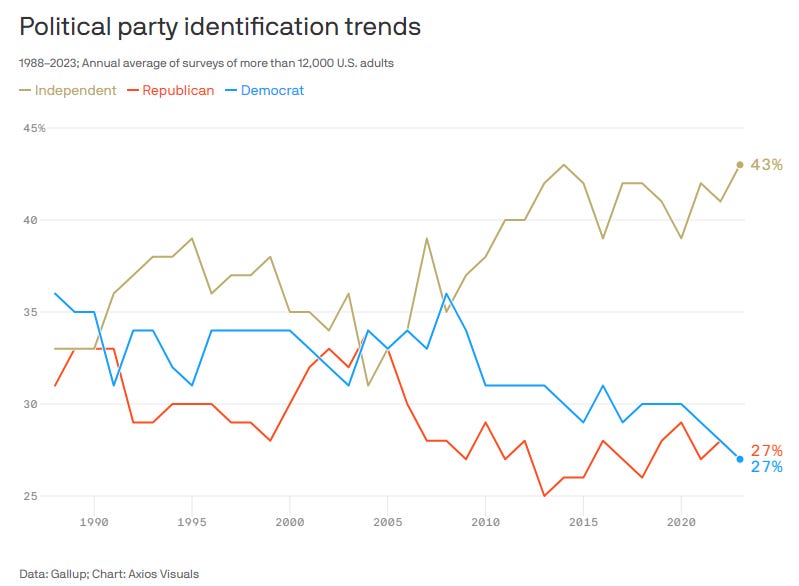

Ian Bremmer, the geopolitical strategist, recently posted a graph and a link to an Axios story illustrating trends in political affiliation.

The most obvious feature is the striking rise in the percentage of independent voters. The next most obvious feature is the long-term erosion of support for both of the major political parties. I suspect this speaks to a reality that can be very hard to extract from mainstream or social media accounts: Most people are not wingnut reactionaries or radical progressives but rather reside somewhere closer to the middle of the political spectrum.

Insofar as this is the case, it also corroborates a hypothesis I have had for a while. As much as the presidential election appears today as a battle between Biden and Trump, there is a lot of space for “surprising” things to happen. That could mean the emergence of a viable third party candidate or the exit of one or both of the major candidates from the contest.

The broader issue is neither of the two major candidates represents most of the country either demographically or politically. That seems to be a problem.

Monetary history

War and Gold: A Five-Hundred-Year History of Empires, Adventures, and Debt, by Kwasi Kwarteng ($)

It is a premise of this book that government finance, the need to accumulate treasure, whether by conquest, by borrowing or by taxation, provides a powerful impetus behind developments in society.

The indebtedness which Britain had incurred [from the Seven Years’ War] provoked genuine concern among the British political elite, and it was this concern that led in turn to the adoption of novel forms of taxation with which to pay for the burgeoning debt.

I have long believed one of the biggest blind spots of investment analysts is a lack of understanding and/or appreciation of history’s lessons. For anyone looking to brush up on monetary history, this book by Kwasi Kwarteng is very readable and provides terrific perspective.

The more one studies history, the more it becomes evident that government finance does indeed provide “a powerful impetus behind developments in society”. The British government spends beyond its means for a war and voila, you have an American Revolution.

Such insights are more than just interesting historically, however. Norms towards debt and fiscal prudence ebb and flow through time which provides useful perspective. For one, it is easier (and more useful) to see things happening today as not especially unique but rather as just different manifestations of trends that have occurred repeatedly in the past. As such, it is also easier see such trends as cyclical and not linear; and that is invaluable for long-term investors.

Investment landscape

The S&P 500 seemed to suddenly come down with a case of nerves this week as prices tumbled and volatility jumped. This probably shouldn’t be too surprising given the sudden burst at the end of last year and the extreme positioning that it entailed.

With this as a backdrop, it’s probably a decent time to highlight the risk of illiquidity. In this case, I’m talking about liquidity in the sense of market impact through trading, not about liquidity in the sense of funds infused to the financial system by the central bank. More tangibly, the risk involves large downward moves in stocks because the sellers have to sell - they need the cash.

The unusual ramp up in the VIX index may have something to do with it. Funds that have been selling volatility may need to either unwind trades or sell assets to contend with the higher volatility. It may also be that other investors are bumping up against risk limits and are forced to raise cash by selling what they can.

This is the broader point: When investors or funds or organizations must have cash, then they must sell what they can. This creates downward pressure on all assets, especially the ones that are easiest to sell. It also presents a big risk to any effort to diversify because when liquidity dries up, all correlations go to one.

Investment strategy

One of the more interesting aspects of the investment environment is its directional nature. In the third quarter, the trade was to get long rates going higher. In the fourth quarter the trade was just the opposite, for long rates to go lower. Never mind that underlying fundamentals had not changed all that much.

This perverse reality has implications for strategy. If you’re a macro trader, it may be look like a target-rich environment. But if you’re just trying to realize decent long-term investment gains, the dramatic ups and downs can be frustrating.

David Einhorn addressed this fundamental investment challenge in a podcast from last summer (h/t John Huber):

What do we have to do to make a good return if a tree falls in a forest and nobody is there to hear it? What happens if there aren’t other investors who are going to bid up the stocks and figure out what we have figured out after we figured it out?

In other words, what do you do if you can’t buy stocks and count on others to drive the multiple higher after you buy them? The answer is to buy stocks that generate decent growth and decent returns and be satisfied with that.

This is a rejection of the premise that stocks will keep going up. It is also a way out of the losing game of guessing where the flows will go. It is also a throwback to old school security analysis in which the generation of free cash flow is what really matters.

While I don’t expect the chasing of returns to stop suddenly, I do expect monetary priorities to shift from supporting stocks to supporting debt issuance. As that becomes increasingly evident, it will become much harder to generate returns by simply allocating to certain “exposures”.

Emerging markets

As the S&P 500 starts looking shaky early in the year it’s natural for investors to look for alternatives - and emerging markets are often at the top of that list. As has been the case for several years, emerging markets are much, much cheaper.

While I get the appeal as a valuation-based investor, I also recognize the market forces that have been preventing valuation from serving as a useful metric. I wrote the following two and a half years ago:

I have some serious reservations [about emerging markets], however, which parallel my reservations about the value style in general. The main point is things changed in 2010 when the Fed essentially made “emergency” monetary measures permanent by continuing them long after recovery from the financial crisis had taken hold. In short, the level of continuous monetary interventions substantially eliminates the types of free market incentives that enable “value” to work. I expect this pattern to continue until either central banks withdraw their unusual support or until inflation destroys the effectiveness of those policies.

This thinking still applies. While the Fed hasn’t eased per se, excess money from pandemic policies is still floating around. The proliferation of passive investing is still driving flows into stocks. Short volatility funds are gaining assets and continuing to put downward pressure on volatility. Foreign investors still find US companies as attractive assets. Big tech companies benefit visibly from developments in artificial intelligence. Less visibly, they uniquely benefit from tax havens that allow them to shield profits from intellectual property.

In short, the forces propelling the S&P 500 are wide-ranging and self-reinforcing. This makes the S&P 500 mainly a directional trade. Pretty much by definition, then, it also makes any alternative, such as emerging markets, also a directional trade.

I do think emerging markets are an interesting place to look and I do think they have potential to be rewarding investments. For that to happen in a material way, however, I still believe some combination of weaker central bank support and persistent inflation will be necessary to break the cycle of flows to the S&P 500. That said, we are clearly two and half years closer to the end of the line than when I first wrote the assessment.

Implications

In Adam Taggart’s interview, Lakshman Achuthan explicitly stated his assumption of a free market economy. While I think the assumption of free markets can still be useful in many ways, I also believe government policy is becoming increasingly interventionist. Interestingly, one of the reasons why Achuthan (by his own admission) missed the economic resilience last year was due to the continuation of high deficits.

This serves as an important marker for evaluating future possibilities. Regardless of what we might expect for growth based on economic signals, we can be fairly sure government is going to step in to tip the scales in its favor. This is why my base case is for decent economic growth this year. I think one should be very careful about assuming a free market economy.

That being the case, the only real question is how long can they get by with it? Given the political tolerance for short-term pain is vanishingly close to zero, I would say the answer is as long as they possibly can.

This means short-term pain will be deferred as long as humanly possible. It means progressively larger deficits will continue to drive debt levels up until politics finally puts an end to it (which seems unlikely right now) or bond markets end it by way of prohibitively high yields. If interventions prevent yields from going too high, then the release valve will have to be the currency.

As a result, I expect deficits to continue to push higher until either high long-term yields or a weakening US dollar stops them.

One implication is that trying to predict the timing of the recession is fools’ play because it’s largely a political choice. That doesn’t mean there won’t be bumps along the way, but allowing a harsh recession would be political suicide.

Another implication is higher inflation. Excess spending is a one-way train and will have to be monetized. Might as well prepare for it now.

Finally, the ultimate impact of inflation will depend a great deal on how other countries fare. The inflationary impact of deficit spending is a relative contest and the debt service capacity of the US actually fares pretty well relative to other major countries. That suggests higher inflation than what is in expectations now, but not dramatically higher either.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.