Observations by David Robertson, 2/28/25

Either the frenetic pace of news flow is slowing down or we are getting more acclimated to it. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The Conference Board survey this week confirmed what the University of Michigan report indicated last week: Consumer sentiment is dropping fast. While this would be something to watch on its own, it is also accompanied by other foreboding signals.

One of them is the redirection of corporate cash flow away from share repurchases and towards capital expenditures. Ultimately, this is good for the economy, but in the short-term it poses a risk to stock prices. This is a point Andy Constan highlighted in regard to Apple’s new commitment to higher cap ex.

One of the more interesting observations in the new year has been the outperformance of European stocks relative to US stocks. The following graph from the FT ($) shows the impressive run. It begs the question both of what the EU is doing right and what the US is doing wrong.

I have mentioned in the past that commodities tend to run in longer-term cycles. Most of the time, the relative balance of supply and demand drive prices on an incremental basis. Occasionally, however, especially at major turning points, supply can be at risk regardless of price. As Alyosha ($) notes, this may be happening with gold (and may be a harbinger for other commodities):

Gold is dominating the news in ways that undermine the creds of everything else because the people talking about it are serious people. The narratives are not about inflation now. They are about possession. When markets stop caring about the price of something and the focus shifts to the availability of it, or custody of it, it’s probably a good idea to hang on to what you have.

Economy

This week we got a little better outline of Scott Bessent’s economic plan. According to Axios, Bessent stated, "Our goal is to re-privatize the economy". He also said, “Government overspending brings distortions in the economy that inhibit dynamism,” and indicated the Biden administration left the economy “ultimately brittle underneath".

By “re-privatize” he means refocus economic growth on the private sector rather than on government. While much of the growth in government employment during the Biden administration was rebuilding from Covid, it is absolutely appropriate that the private sector should be the core driver of long-term growth. The comment that the economy is “brittle underneath” certainly sounds like the administration is planning for weakness and planning to blame Biden.

While Bessent’s objective sounds reasonable, the means leave one scratching one’s head. Widespread and largely indiscriminate cuts to government payrolls has the immediate effect of lowering incomes — and therefore demand for other products and services. The budget bill submitted to the House pays for extending tax cuts by making sweeping cuts to Medicare and Medicaid cutbacks which disproportionately effect lower income people (who also have a higher propensity to spend what they earn).

Not only that, the sum of the tax cuts substantially exceeds the spending cuts — which means the budget deficit will continue to grow. At the FT ($) reports, only the lone Republican holdout on the budget bill, Rep. Thomas Massie, was willing to concede this obvious reality: “If the Republican budget passes, the deficit gets worse, not better.”

In short, while Bessent’s objective is reasonable, Trump administration policies appear to make the situation worse, not better. As a result, Bessent’s plans sound more like economic demolition under the guise of privatization than it does of considered re-orientation. This interpretation is already showing up in consumer sentiment. We should start seeing signs economic reports shortly.

Housing

Even as mortgage rates ease up a bit, homebuilder stocks continue to get hit. A couple of snapshots of the housing industry are illustrative.

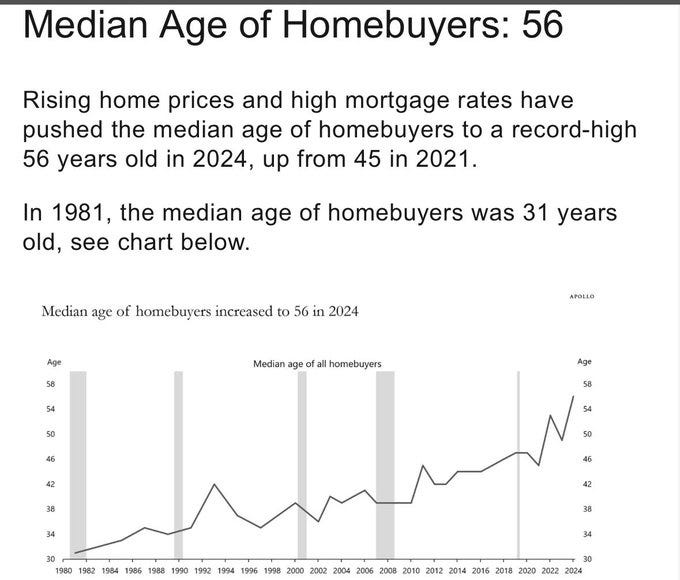

For one, as Rev Cap posts, the median age of home buyers has now risen up to 56 years old. This is a massive increase from 31 years old in 1981.

For another, as Nick Gerli explains, the “only thing propping up the Housing Market … [is] Luxury sales”. The only notable growth has been in the most expensive homes. Growth in sales of cheaper homes has been low or even negative.

These two posts paint a picture of housing as being mainly the playground of the older and wealthier. Younger and lower and middle-income buyers are mostly locked out of the market right now. Not a good formula for healthy economic growth and a motivated workforce.

Politics

Bruce Mehlman made a good point in his Substack last weekend that Washington is just not designed for frenetic, multifaceted policymaking:

Does Washington Have the Bandwidth? Working in a town of “northern charm & southern efficiency,” Washington generally has the bandwidth for one giant policy battle at a time. In 2009-10, it was the Affordable Care Act. 2011 was consumed by Simpson-Bowles, the “Supercommittee” and national debt. In 2013 it was the Senate Gang of 8 advancing bipartisan immigration reform; 2017 Trump’s tax cuts. 2018-19 were all about Trump’s trade wars and the end of the Washington Consensus, 2020 was COVID, of course, and 2021-22 was dominated by Biden’s ambitious industrial policy agenda (Infrastructure, IRA, CHIPs).

As he highlights, this legacy modus operandi is inconsistent with the current Trump administration’s desire to “advance on all of these fronts simultaneously – tackling debt/spending, re-shaping government, massive tax cuts, widespread new tariffs, mass deportations and broad health reforms (MAHA) concurrently”.

While advocates seem to appreciate the energy finally being directed to reforming government, others are responding differently. Some are tempering reactions and discounting various statements. For example, Robert Armstrong ($) observes:

Vladimir Putin told Donald Trump that he had no problem with the presence of peacekeeping troops in Ukraine after the end of the war in that country. Or so Trump said yesterday. This is, in the words of one analyst, “bombshell” news that changes the odds of peace significantly — if it is true. But no one is sure if Putin actually said it, and if he said it, whether he meant it. So Trump’s comments didn’t even make front pages. In 2025, in politics as in markets, nobody knows what to believe.

So, one response is to start tuning out. Another response is to push back against the inconsistencies of the Trump administration. As Matt Stoller writes, “Massive turnout at town halls and at Bernie Sanders' Tour Against Oligarchy suggest that something new is happening.”

Stoller explains that Bernie Sanders launched his “National Tour to Fight Oligarchy” this week — and it is immediately attracting attention. Sanders is talking to “overflow crowds in Nebraska and Iowa” and in addition “his videos are getting tens of millions of views, and his online campaign metrics are performing remarkably well”. In short, he seems to be hitting on ideas that animate people and in politics that is gold.

None of this should be taken too seriously as it is still early days in Trump 2.0. That said, it is rare that a new administration loses favor so quickly. The FT ($) shows just how poorly the second Trump administration is stacking up against prior administrations:

Not only are Trump’s approval ratings lower than any other president since the 1950s, his disapproval ratings are far higher as well. While some of this can be chalked up to increasing political partisanship in recent years, it cannot be considered a “mandate”.

By almost any scorecard then, Trump administration policies are failing. Consumer sentiment is down, approval ratings are down, disapproval ratings are up, and political opposition is coalescing around anti-oligopoly sentiment. Nor is the narrative traveling well as the belief system in Trump is getting crushed by the economic reality of Trump. It is exceptionally hard to view Trump policies at this point as any kind of serious effort to make things better for Americans.

The only place where Trump policies are “working” are among the Trump faithful who have not been adversely affected yet. Increasingly, this looks like where the political battle lines will be formed. Either continued erosion of economic strength will bring more voters into the Trump fold — or there will be a massive backlash at some point. Either way, things will get messy.

Politics II

Is Elon Musk’s war on fraud just cover for a power grab? ($)

Yet the Nixon precedent helps to explain why many people—including senior civil servants—mistrust the Trump administration’s campaign. And experts say that although fraud is a big problem in the federal government, and that Mr Musk is right to raise it, what he is doing is unlikely to improve the situation. In fact, some fear that the sloganeering about “waste, fraud and abuse” is designed to create political cover for unilateral cuts of congressionally mandated spending Mr Musk and Mr Trump do not like and for gaining access to sensitive data systems.

Yet Mr Musk’s claims about fraud so far have had only a limited relationship with the reality of the problem. He has regularly described as “fraud” authorised programmes he doesn’t like, such as everything paid for by USAID. “You might not want the government to invest in DEI training in Ireland, but that isn’t fraud,” says Ms Miller. “Somebody made the decision to invest that money.”

A key here is that while to date, “there has been only limited effort to fix this [fraudulent spending],” Mr Musk’s claims “have had only a limited relationship with the reality of the problem”. One problem is that “many of the programmes targeted by fraudsters—unemployment insurance and Medicaid, for example—are largely administered by the states.” Another is that nobody can explain “why fighting fraud requires inexperienced political appointees to have direct access to IRS or Social Security data.”

If the approach to a political problem is not even a plausibly constructive one, then voters are left to wonder two things. How much harm will it cause and what is the ulterior motive?

Investment landscape I

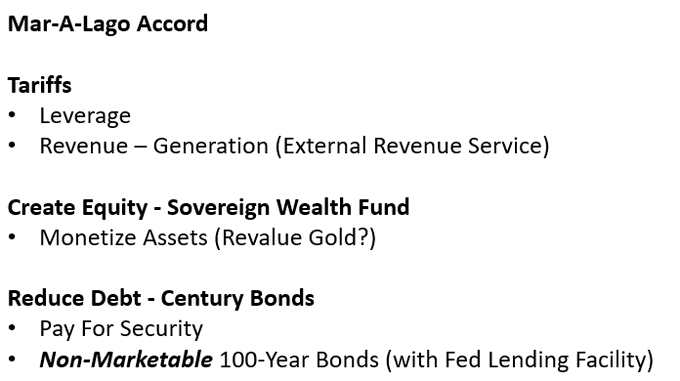

The notion of some kind of formal agreement to manage the value of the US dollar down is making the rounds and often referred to as the “Mar-A-Lago Accord” (MALA). Jim Bianco provides a good thread on the ideas, many of which derive from the Stephen Miran paper I referenced last week (Observations 2/21/25). The summary, in a single slide, looks like:

I noted some of my reservations about the plan last week, to which I would add two more points. First, the urgency of getting the federal budget on a sustainable path does argue AGAINST not doing anything, but it does not argue FOR MALA. Second, there are no silver bullets here. It is ridiculous to rule out options such as raising taxes or cutting spending which can help incrementally. Because guess what, tariffs aren’t going to raise all the necessary revenue either.

A good, thorough “rebuttal” was also posted by Andy Constan. A key objection is “A lot of those (US) assets are held by the private sector of ROW”. As a result, “they are not likely to be cajoled into action”. In other words, the “stick” from MALA doesn’t even work with a large portion of asset owners. Further, there are no “carrots”. Constan concludes for now, MALA is “a pipe dream”.

What does all this mean? For one, the Trump administration still seems to be using MALA as a policy playbook. As a result, it’s often easy to trace ideas back to that. In addition, while there is a lot of scuttlebutt about MALA, there is exceptionally little economic or political wisdom to commend it. As a result, it does not seem to be gaining any substantive traction.

Finally, and probably most importantly, as investors and commentators ruminate on the potential second- and third-order effects of such a policy, it is easy to see how the negative consequences (in the forms of distrust, pushback, and even open opposition) could overwhelm any possible benefits. Bianco is right that something needs to be done, but it shouldn’t be shooting yourself in the foot. Whether this increasing realization is contributing to weaker consumer sentiment or not is imponderable to a large degree, but they are both happening at the same time.

Investment landscape II

One of the most important concepts in finance is the notion of a risk-free asset. One of the most interesting phenomena in the investment landscape right now is all the ways in which previous assumptions about safety are getting upended.

At a high level, while the geopolitical environment has suffered from increasing tensions from Russia and China, the US has long been viewed as a stabilizing influence.

That has changed. As Ian Bremmer posted, “the united states has become the largest source of geopolitical uncertainty in the world.” He adds, “it’s an extraordinary development.”

Uncertainty has also increased within the US. Brent Donnelly notes, “as the Leviathan is torn down by billionaires, the collateral damage is that many $100k / year jobs in Washington, DC will be lost.” Of course, job losses also extend well beyond Washington, DC and well beyond government. As USAID is dismantled and funds are withheld from research organizations, job losses are also mounting in academia.

Regardless of whether one considers such job losses in a positive or negative light, what is hard to refute is that broad sectors of employment such as government and academia, which had been considered “safe”, no longer are “safe”. Further, that reality dramatically changes not only the spending habits and risk-taking ability of everyone who lost a job, but also everyone who still has a job but now knows they could lose it at any moment.

Similar changes in sentiment are also beginning to infect the US Treasury market. Foreign owners, in particular, have to be increasingly concerned about the receipt of both principal and interest, especially if their government is in conflict with the Trump administration. Even US holders of Treasuries must now ponder, according to the FT ($) “whether a president might force out a central bank chair or launch a global trade war.”

This unusual combination of developments does two things simultaneously: It both increases the demand for safe investments and decreases the universe of investments that can still be considered safe. One effect is that while US Treasuries are unlikely to be dethroned as safe assets in the near future, there is a good chance yields will be a lot more resistant to falling than they have in the past. Another is that cash is likely to become more attractive.

Implications

In considering the whole of Trump administration policies thus far, one cannot escape a multitude of inconsistencies — to the point of wondering what the ultimate goal even is.

For example, one can laud the desire to reduce trade imbalances, but find the prescriptions of MALA to be not only untenable, but undesirable. On this point, Paulo Macro wrote:

The U.S. is more dependent on foreign capital but they also have much more access to foreign capital. This could change but for now if anything the U.S. has too much foreign capital in the country not too little. Just like … an EM [emerging market] before it blows up

While most people would agree EMs are far more vulnerable to “hot” money flows than the US, that is predicated on the US being perceived as safer. Clearly, that perception is changing.

By the same token, one can laud Treasury Secretary Bessent’s goal of lowering long-term Treasury rates, but wonder how tanking the economy is going to be very helpful in that process. Won’t a weaker economy drive up budget deficits even higher? Assuming so, an economic slowdown may initially drive bond yields down, but could eventually push them up as it creates exit liquidity for foreign owners of US Treasuries.

Finally, one can commend the effort to root out fraudulent and wasteful spending in the government, but wonder why the “chainsaw” DOGE is using is the correct implement. Doesn’t indiscriminate cutting cause a lot of unnecessary damage?

The common thread in all these examples is that of sloganeering around a desired proximate goal at the cost of a longer-term, ultimate goal. This begs the question of whether there is an ulterior motive. Dirty Texas Hedge offers one:

The point of DOGE isn't really about cutting costs. The point of DOGE is to deliberately reduce the state capacity of the federal government in a way that will be extremely difficult to undo

If there is an ulterior motive in Trump administration policies, how long will it take investors to start acting on that knowledge? I suspect a key signpost will be long-term rates that don’t go down as much as it seems they should based solely on economic conditions.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.