Observations by David Robertson, 5/19/23

“The inconceivable is absolutely conceivable when the survivability of the state is threatened.”

There are a lot of things to discuss this week, but I thought the quote above by Russell Napier was an appropriate way to start off. Another way to express the same sentiment is: “Be alert to some of the unbelievably crazy stuff you are about to witness.”

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

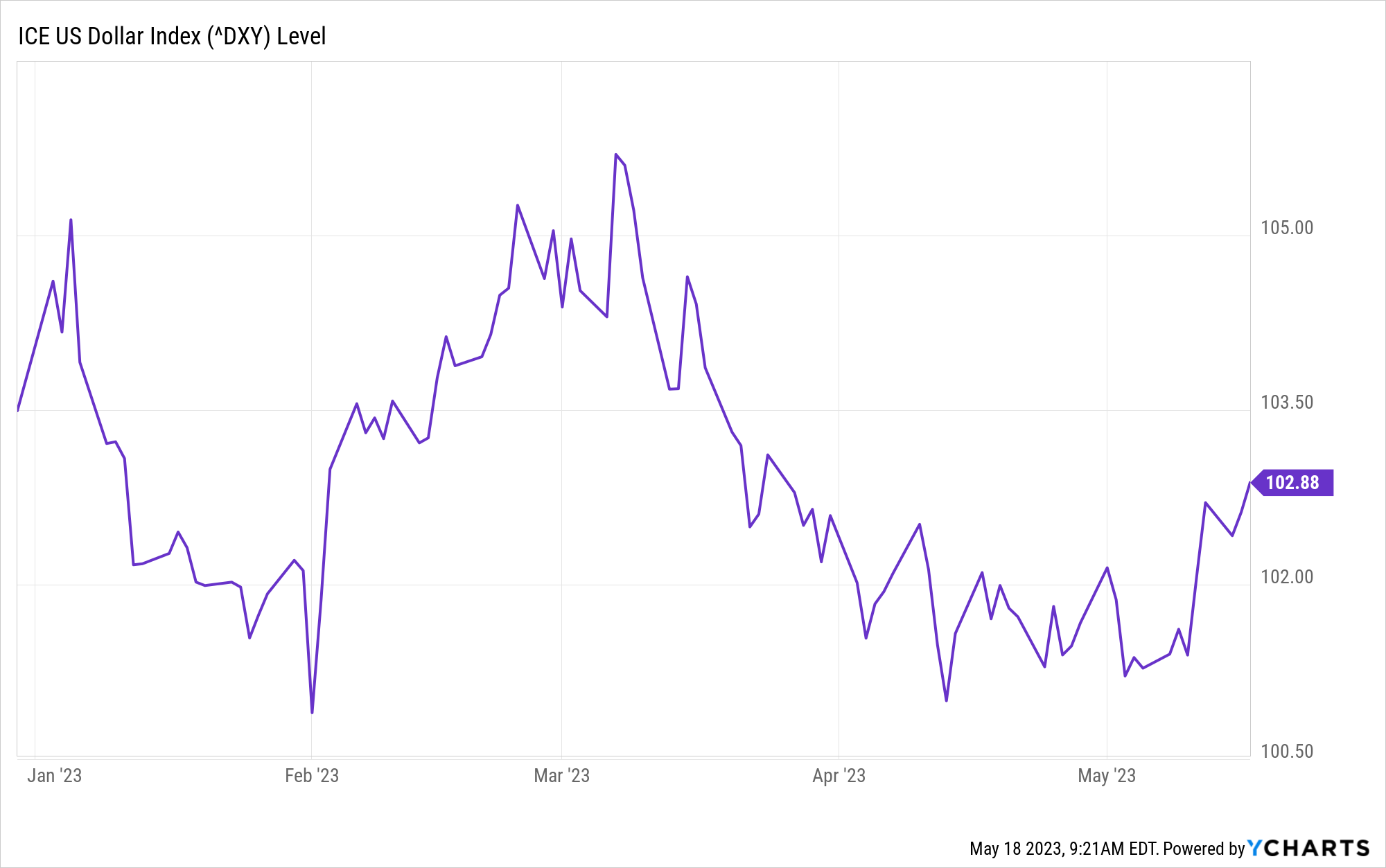

Look who’s making some noise recently - the US dollar! After getting beaten down earlier in the year due to easing liquidity conditions, and again in March and April due to the belief that emergency bank relief measures amounted to capitulation on Quantitative Tightening, USD sprung up off the mat yet again. Clearly the “de-dollarization” media campaign came up short.

This hasn’t seemed to have affected markets yet with the S&P 500 hanging out near the top of its recent range. There are some hints USD may continue its upward march, however. The yuan has been weak lately and 10-year Treasury yields are also rebounding. Maybe, just maybe, the easier liquidity conditions that began last fall were just a brief intermission and not a change in direction. If that is the case, there will be a lot of pain coming around this summer.

Credit

What Seems to be the Problem, Officer?, Almost Daily Grant’s, Monday, May 15, 2023

https://www.grantspub.com/resources/commentary.cfm

Though the early-spring credit curtailment is readily explainable, high-yield investors should nonetheless take careful heed of that dynamic. Going back to 1997, the proportion of loan officers tightening credit compared to those easing it has never been as high as its current level outside of recession, Lehmann, Livian, Fridson Advisors chief investment officer Marty Fridson relayed Sunday.

Considering that the metric accounts for nearly half of long-term variance in high-yield spreads over time, by Fridson’s assessment, spreads are accordingly “way out of line,” the dean of high-yield argues. Prior to this year, the narrowest monthly spread seen during periods of a net 40 to 49.9 percentage point tightening in the survey going back to 1997 was 644 basis points, with the median gap registering at 771 basis points. By contrast, the option-adjusted spread on the ICE BofAML High Yield Index finished Friday at just 476 basis points.

This is another good news/bad news story. The bad news is credit, which normally provides an early warning signal, has been somnolent. This is especially worrying as many investors have incorporated high yield into their allocation mix for either diversification benefits, yield enhancement, or both.

The good news is there is another signal that seems to be working better - and that is the proportion of loan officers tightening credit. Given its historical relevance in explaining spread variance, and the dearth of other useful credit signals, it is something investors should pay attention to. Not only that, but investors should also be wary of becoming complacent. Just because many traditional signals are not flashing red does not ensure everything is OK.

China

The meaty mystery at the heart of China’s economic growth ($)

Yet other data reveal a more modest recovery—only to levels last seen in 2019, before covid-19, and not beyond them. Although more people travelled this year, spending per head was down by more than 10% against 2019, according to hsbc, a bank. As a consequence, domestic tourism revenues were up by a mere 0.7% on four years ago. “Chinese consumers are not back to normal,” warns the boss of an asset-management firm. They are focused on food and fun, not big-ticket items like cars, he says. Auto sales were down 1.4% year on year in the first four months of 2023.

This Economist article provides some nice color on the economic recovery in China after its Covid lockdowns. There are several parallels with the US recovery. For example, a lot of people are actively seeking experiences as an antidote to being trapped at home for too long.

In addition, some patterns appear to have changed. In China, spending on big-ticket items has not recovered. I suspect this is at least partly a response to the capriciousness of public policy. If you acquire a new appreciation for how sudden and how harsh policy can be, then maybe you want to hold on to some more cash and be more reluctant to take bigger financial risks.

It will be very interesting to watch if this new level of cautiousness on consumer spending endures. If it does, China’s economy will have problems.

In other China news, Diana Choyleva reports, “#China is pressing farmers to increase #SoybeanProduction, using a combination of subsidies, government stockpiling and public pressure” in a drive to bolster food security. This highlights both China’s heavy hand in regard to public policy and its sensitivity to food security. Either or both of these factors could easily become flashpoints in the not-too-distant future.

Geopolitics

The president can do two things at once ($)

https://www.ft.com/content/f6a5fa05-19b9-41d0-917c-2316953804a2

I [Gideon Rachman] was witness to a fascinating exchange between US officials, think-tankers and their European counterparts in Berlin recently. When the American side was pressed on the impact of the enormous subsidies being offered in the US - for chips and EVs - it seemed to me that their response boiled down to: “If we don’t do this, Trump will win the next election and then we’re all screwed.” To which one French participant responded (and I’m paraphrasing): “Yes, but if you do do it, then we’ll lose lots of industrial jobs and we may get Marine Le Pen at the next election. And that won’t be great for anyone either.”

One observation to note from Rachman’s analysis is that Jake Sullivan’s presentation to the Brookings Institute (which I highlighted in the 5/5/23 edition) has been reverberating through global policy circles. In other words, it’s a big deal.

Another observation is it also illuminates some of the potential complications the Biden administration will have in working with its European allies. They have political challenges too - which limit the degrees of freedom in pursuing certain policies. Mainly, this is a good example of the kinds of nitty gritty details and frictions that emerge when trying to implement a policy of such grandiose scope.

Politics

So this is actually setting up worst for Repubs because McCarthy’s speakership is held hostage by a handful of MAGAs whose personal optimal strategy is to say no and let it burn. The optimal strategy for Dems who know history is to let them. And Repubs take the blame.

Some comments here on the debt ceiling by PauloMacro on Twitter. I post this because I think it is an interesting analysis and definitely not a consensus view. If this plays out, a lot of investors will be very unpleasantly surprised.

That said, when it comes to politics I always think of the answer Bob Woodward gave to a question at a Speaker Series presentation. When asked how much of what goes on in Washington is the public actually aware of, Woodward answered, “About 2%”. As a result, I am extremely disinclined to try to predict what will happen with something of which I know almost nothing. By the same token, I am also disinclined to categorically reject possible scenarios.

Monetary policy

Probing LCLoR

https://fedguy.com/probing-lclor/

An unwelcome move towards LCLoR would leave the Fed without many options other than a repeat of the 2019 Reserve Management Purchases. Pushing cash out of the RRP and into banks by toggling the RRP offering rate or adjusting counterparty limits is very unlikely because it interferes with the Fed’s ability to control rates. But purchasing bills to add reserves would be effective and tailored. The Fed would not perceive this to be a change in the stance of policy because it is duration neutral, but other market participants may view it differently.

Fedguy Joseph Wang raises an issue that will be important to monitor. As money continues to move out of the banking system into money market funds, the Lowest Comfortable Level of Reserves (“LCLoR”) is likely to be breached “within a few months”. What will the Fed do?

I have been assuming eventually the RRP is mainly just a different type of excess reserve and when the time comes, the RRP will deplete. This can happen through coercion, if the Fed modifies the terms of the RRP so as to make it less attractive, or it can happen naturally, if the money market funds that constitute the majority of the RRP start finding Treasuries more attractive at some point. All this would take is evidence that short-term rates are unlikely to continue going higher.

Wang argues otherwise, however. He seems to assume RRP will remain relatively unchanged. As a result, he thinks bank reserves will need to be maintained/replenished through “persistently high bill issuance”, of which the Fed will be a significant buyer. While the Fed may not “perceive this to be a change in the stance of policy”, I am fairly confident most people watching the Fed’s balance sheet get bigger will feel differently.

Ultimately, this comes down to a long-term/short-term strategic decision for the Fed. It can either lose some control of rates now in order to regain control of monetary policy for the future, or maintain some semblance of control now but at the cost of forever ceding control of rates in the future. If it chooses the former, monetary policy will be tighter than the market currently expects. If it chooses the latter, the ground will be well fertilized for the future growth of inflation. I still lean towards the former.

Fed Asymmetry Threatens Credit Crisis

https://www.theinstitutionalriskanalyst.com/post/fed-asymmetry-threatens-credit-crisis

If all of this is not enough worry on your risk dashboard, the folks at the Fed have managed to screw up the Treasury bond market so that the cash and the futures are no longer tracking. TBAs and MSR hedges are not performing as expected. Or in plain English, the off-the-run Treasury bonds are now the cheapest to deliver against your short position.

Much of this note amounts to Chris Whalen bellyaching about the harm caused by higher interest rates. As annoying as this may be (and it is), Whalen knows a lot about banks and the financial system and exposes an important dynamic here.

In our highly financialized and highly leveraged economic system, one of the things that facilitates the high leverage is the availability of hedges. If you reduce the risk by using hedges, you can apply more leverage.

That works right up until the hedges stop working. As Whalen points out, Fed actions have “screwed up” the Treasury market in ways that disrupt commonly used hedges. As a reminder, a similar dynamic occurred in March 2020 when the Fed intervened strongly in the Treasury market during the onset of the pandemic. The result was significantly underperforming hedges among the mortgage REIT companies. Annaly Capital, the largest of the group, lost 40% of its value almost instantaneously - for the crime of prudently managing risk.

So, Whalen’s point is a good one. In our complex financial system, it is hard to tell what kinds of unintended consequences may arise from significant policy interventions. As a result, it is harder and more costly to protect against risk. The implication is to avoid complexity. When there is a lot of financial engineering and/or a very complicated business model, a lot of things can go wrong.

Public policy

Projecting the X-Date and the TGA

https://johncomiskey.substack.com/p/projecting-the-x-date-and-the-tga

Is the X-Date in June?

Will the TGA make it to the end of June before exhausting (and thus to some point in late July or August)?

Yes! I think so, the output of my model tells me it will anyways, but it will be waaaay too close for comfort, and there is significant disagreement between what my model projects for remaining deficit between May 11 and June 30th (229b) and what Treasury suggests is remaining (288b) based on the early May updated refunding statement.

I won’t say a lot here other than that John Comiskey has done outstanding work on tracking Quantitative Tightening (QT) and now on the TGA. Check out his Substack if you are interested in diving into the details - it’s the best work I have found.

Inflation

All the focus has been on 1-year inflation expectations which continue to decline. Interestingly, however, the long-term expectations continue going up. This is very bad for the Fed and suggests expectations are becoming “unanchored” (in the monetary vernacular).

The long-term expectations are looking anything but transient and are hotly at odds with expectations of Fed rate moves.

This is essentially the same conclusion Matt Klein ($) reaches in a Substack post that disentangles pandemic era inflationary pressures from more persistent ones. He finds, “Inflation is not continuing to accelerate, but instead seems to be settling into the 4-5% range.”

He too recognizes that “we are still far removed from what Fed officials say they want—and most asset prices today also seem inconsistent with the idea that inflation has permanently reset from ~2% a year to 4-5% a year.”

Landscape I

MacroVoices #375 Mike Green: Banking Crisis, Debt Ceiling, De-dollarization and more

Passive bond funds allocate investments on the basis of the market capitalization of the various bond issuers.

But if you simply think about what bonds do best as the Fed cuts interest rates. Low coupon, very long dated bonds, right? So 100-year bond, zero coupon, if it's issued at 2% interest rates and interest rates go to zero, that bond is going to explode in value. It becomes a giant portion of the index.

That meant that it received twice the weight within the bond indices. Who's buying it and that proportion? Turns out it wasn't European pension plans trying to asset liability match, etc. The largest buyer was Vanguard. Right, what we saw was the impact of passive investing on bond markets, in the presence of interest rate cuts caused the duration sensitivity of the bond market to explode.

For all the ruckus in regional banks, and all the blame that can appropriately be leveled, it is a fact that rapidly rising interest rates severely impaired the value of all Treasuries and hurt long-term Treasuries the most. Not surprisingly, this value destruction occurred to anyone holding Treasuries … including Vanguard and Blackrock and, therefore, quite possibly - you.

The additional problem for Silicon Valley Bank was that it started losing deposits at an incredibly fast rate and therefore did not have sufficient time to make up for the losses. Vanguard, on the other hand, has continued to have money flowing into its bond funds despite the poor performance. If and when those flows reverse, Vanguard will have the same challenge as Silicon Valley Bank.

If and when that time comes, it will be very interesting to see what happens. Either money will flood out of Treasury markets driving prices down and yields up, or the large purveyors of bond ETFs will need to impose gates and throttle the amount of money that exits. While we may start out with option #1, I’ll bet we end up with option #2. If that’s the case, a lot of people will become much more long-term holders of fixed income than they intended.

Landscape II

Exclusive Interview with Russell Napier: Save Like a Pessimist, Invest like an Optimist

As always, Russell Napier provides a tour de force in analyzing the global economic and political landscape. Because his comments are so extensive and wide-ranging, I will save a few points for next week. This week I’ll focus on areas where I think the consensus opinion is off the mark.

Let’s start with the politics. Napier makes a great point in highlighting that a chief concern of governments is to “get the debt/GDP ratio to a sustainable level”. Without that, debt continues to strangle the economy and problems get progressively worse. When that happens, governments get overthrown. No can do.

So, if we acknowledge reducing debt/GDP is the primary political problem in many developed countries, then all we have to do is game out the various ways to accomplish that. Very high on the list must be slowing down growth in debt. There are two straightforward ways to do that.

One way to slow debt growth is to raise interest rates. Higher rates means less borrowing. The other way is to vastly scale back non-bank, asset-backed securitizations. Essentially, these activities amount to unregulated and uncontrolled money creation.

In my opinion, a big mistake a lot of investors are making is to miss the primacy of the government’s interest in reducing debt - and its ability to do so. Rather, too much attention is place on central banks.

To that point, Napier describes:

“the central banks do not have the power to deliver these things [e.g., 2% inflation]; these powers are being stripped from them; and that’s the path for central banking. Not that they fail conventionally by having the wrong policy settings, it’s that the tools they need In order to deliver are being stripped from them … It’s just the politicization of credit.”

Again, I think the notion that the Fed, or any other central bank, are driving the train here is misguided. Central banks serve a purpose in the form of appearing to fight inflation, but they do not have the tools to pull it off. Nor is that even the desired outcome. Over-indebted governments want inflation (to reduce debt), but they can’t appear to be insensitive to the harm it causes.

One of the quiet, but effective, ways the government harnesses the power to lower debt/GDP is by capturing the banking system. It does this through a series of emergency measures, such as those implemented during the regional bank crisis in March. The hitch to such measures, however, is “There’s a price to pay”. As Napier describes, “This is the capture of the financial system to do the public good”.

Once again, there are a lot of bad takes on what is really going on with the banks. A lot of commentators extrapolate from the GFC baseline and concluded we are on the threshold of a banking disaster. This isn’t right.

The better take is that the banking “emergencies” provide the pretense for government to become ever-more involved in the banking sector. While done on the pretense of keeping it “safe”, it paves the way to direct credit and eventually to sustain financial repression. If you focus to much on the past, you miss groundwork being laid for future policy.

Put more plainly, the government is positioning to have much more influence over the banking sector - which is the most important source of money supply in the economy. Inflation anyone?

Implications

While short-term market moves continue to confound, the longer-term contours of the investment landscape are becoming clearer. Debt/GDP has to come down because the political consequences will be too dire if it doesn’t. As a result, financial repression will be deployed.

Eventually, this will mean there will be excellent opportunities in industrial and commodity companies that can rebuild productive capacity. It will also mean a fairly long span of poor returns to fixed income.

The interim period can go a lot of different directions, however. A severe crash is certainly possible based on excessive valuations, but the regular stream of inflows is likely to prevent that. More likely is a downward ratcheting that takes place over years. Some periods will get ugly and prices will reset down, but regular inflows will prevent a spontaneous unraveling.

It is also worth considering the possibility that major indexes don’t move down much at all. In such a scenario, there could be a massive reordering of leadership, from tech and other long duration plays to industrials, commodities, and other cyclicals. If regular inflows continue at about the same pace, however, there would be little catalyst for big declines in overall index values. Something to think about.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.