Observations by David Robertson, 5/2/25

After a slow start to the week, markets started rocking and rolling again. Let’s take a look.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Stocks continued their win streak through Thursday. While the rebound started off as a normalization of oversold conditions and short covering, it soon morphed into something more. As The Daily Shot illustrates, the gamblers were also busy chasing meme stocks:

It wasn’t just meme stocks. The Mag 7 and other usual suspects were also a big part of the rebound.

That optimism did not extend to oil though. Brent crude continues to say global economic growth is slowing down.

Economy

The week started off with ominous signs on the economy from the latest Dallas Fed survey:

Perceptions of broader business conditions continued to worsen notably in April. The general business activity index fell 20 points to -35.8, its lowest reading since May 2020. The company outlook index also retreated to a postpandemic low of -28.3. The outlook uncertainty index pushed up 11 points to 47.1.

Not only had the outlook for growth turned decidedly negative, the report also indicated “Price pressures accelerated in April”.

That somber tone was continued with the data bonanza on Wednesday morning. ADP showed weak (but still positive) job growth over the last month. Core GDP wasn’t bad, but the headline number was negative and huge imports almost certainly front loaded demand for products subject to tariffs.

Finally, the Treasury Borrowing Advisory Committee also reported on Wednesday. While there was little of note regarding the quarterly refunding, the committee did report, “The global economic outlook is now among the most uncertain in recent memory.”

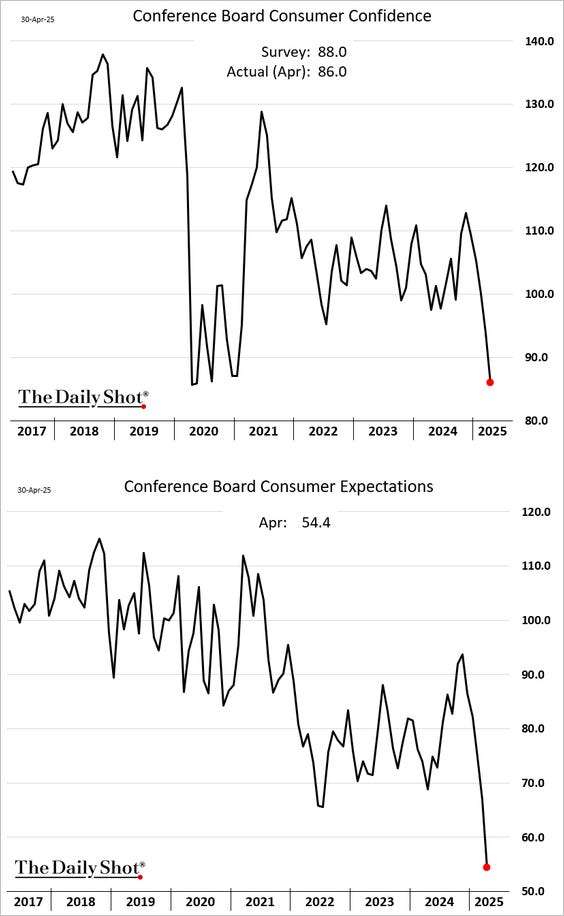

Not surprisingly, consumer confidence and expectations are turning down hard and fast as The Daily Shot illustrates:

Gold and cryptocurrencies

Mike Green ($) outdoes himself again in deploying AI to better understand monetary dynamics. For starters, he recognizes the “Satoshi white paper establishes a testable programmed system” which means it can be gamed out through AI. The analysis concludes:

All models converge toward a consistent conclusion after rigorous recursive analysis: Bitcoin's fair value is approximately $4,000-$6,000, representing 91-94% decline from current market prices. The models demonstrate that Bitcoin's structural constraints—limited supply, energy consumption, and technical limitations—create mathematical impossibilities for meaningful adoption. The most probable outcome (65-79% likelihood across all models) is either technical obsolescence or continuation as a niche technology that primarily benefits early adopters while imposing costs on non-participants.

In short, unless you are a crypto zealot, there isn’t much place for owning crypto other than as a novelty item.

Green goes even further though and hypothesizes that cryptocurrencies have been “stealing the thunder of gold” thereby causing it to be undervalued. If money that has flowed into crypto had flowed into gold instead, Green estimates “bullion likely sits in a $6 k-10 k band today”. In other words, the huge move we have seen in gold thus far would have been even more impressive.

Because gold is such an important store of value, if it did substantially reprice in dollar terms, it would affect other assets as well. Green reports a move to $6k-10k would “unleash a rapid re-pricing cycle across commodities, real estate, and equities”. Good to know.

Interestingly, as The Daily Shot reveals, the uptick in retail gold buying has been focused almost exclusively in Asia. Retail purchases of gold just haven’t changed much in the US or Europe. Perhaps that is about to change?

Politics and public policy

With the Trump administration now having crossed the 100 day mark, grades are rolling in and they are not good. The following analysis comes from The Bulwark ($):

CNN, in the field April 17–24, has Trump with a 41 percent job approval rating—down 7 percentage points over the last two months—and a 59 percent disapproval rating. Only 22 percent of respondents “strongly” approve of his performance while 45 percent “strongly” disapprove.

The numbers are pretty striking. And what’s also striking is that support for Trump’s performance on a wide range of issues has declined across the board. Obviously, he’s stronger on some issues than others—but on all of them, he’s trending down. This kind of broad disapproval is harder to reverse than if there were simply one issue harming his presidency, on which he could presumably change course. There’s no obvious silver bullet for Trump to reach for in order to restore his public standing.

Point one is the CNN poll result is not a one-off; very similar results were reported in surveys by ABC News/Washington Post Ipsos and New York Times/Siena. Point two is that Trump is trending down on every issue — which represents “broad disapproval”.

To this point, Bruce Mehlman highlights an interesting phenomenon. According to what he labels the “perplexed plurality” (which excludes either political extreme), “the Trump Administration often seems to have the right goals but consistently disappointing means for achieving them. The Administration is doing what a majority thinks is right, but in a way that a majority thinks is wrong… “

He presents DOGE as an example:

A similar differential score between goal and implementation can be found on an issue like immigration. For example, The Bulwark ($) also reports a Reuters/Ipsos poll found “that 50 percent of respondents believed Kilmar Abrego Garcia, who was wrongly deported to El Salvador, should be returned to the United States while only 28 percent said he shouldn’t be.” In short, “People want immigration to be quote-unquote ‘handled’ but they want it to be done in a way that fits with their idea of the American justice system.”

While these responses in themselves don’t necessarily mean a whole lot, they can be indicative of things to come. For one, political dissatisfaction may be closely related to negative market sentiment and an indication that most voters do not believe the country is on the right path. Keep that up for very long and the politics will get brutal.

For another, a growing tide of negative sentiment gives license to others to express their own misgivings. As the Bulwark points out, “What the [negative] poll numbers can do is help strengthen the nerve of individuals and the will of institutions to resist Trump and Trumpism.”

China

News about China in the US is dominated by talk of Trump’s tariffs and daily spin on the status of negotiations. Take a look from outside the US and the perspective is very different. As Shannon Brandao reports for China Boss ($):

As Trump's tariffs, disruption, and trash-talk ricochet through global markets, countries aren't rallying behind Washington—they're bracing, hedging, and cutting their own deals. Even Ursula von der Leyen, once hailed in D.C. as a China hawk, is pitching Beijing for stability.

The White House claims over 70 countries are rushing to negotiate. In reality? Just 18 proposals, per the press secretary—and many initiated by Washington itself.

Not only are global trading partners extremely reluctant to cave in to Trump’s demands, China is also trying to make it as hard as possible on them to give in. Specifically, “Beijing has delivered a stark ultimatum to US partners: Do not align with Washington’s economic pressure campaign against China, or you will face repercussions.”

Pushback on Trump’s tariffs is being manifested in other ways too. For example, some major retailers like Walmart have agreed to absorb additional tariff costs on some items, thereby acknowledging the reality that they need the goods more than the price. A recent post by Bob Elliott highlighted this phenomenon: “companies like Walmart appear to be just accepting the tariffs will be paid for by the US.”

Another post by Bob Elliott showed that the Chinese perspective on tariff negotiations varies considerably from that of the Trump administration:

Chinese policymakers continue to take a tough stance on extreme US tariffs.

Refusing to negotiate, official accounts openly mocking the US, and today publishing a revisit of Mao's "On Protracted War" all point to little desire to give in anytime soon.

In addition, the FT ($) reported, “Beijing’s top economic officials have said China could do without American farm and energy imports”. China’s public statements certainly aren’t suggesting any kind of imminent deal.

Further, if words aren’t strong enough, there are always actions. Zerohedge reports China “quietly seized a disputed reef just miles away from the Philippines’ most important military outpost in the South China Sea, in a sharp escalation of a regional dispute with the Philippines, raising the risk of a new military stand-off between the two rival claimants.”

In sum, what is going on between the US and China is way bigger than a little tariff negotiation. It is about a broader superpower struggle that is morphing into a cold war — and perhaps something even bigger. As China Boss summarizes, “Suffice it to say, once again: the US-China clash has moved far beyond tariffs—it’s now a litmus test for global alignment.”

Investment landscape I

One of my favorite strategiests is Russell Napier because he always has a way of providing a perspective that makes things look so much easier. It’s easy to get caught up weighing incredibly negative sentiment data against decent (but weakening) hard data and trying to guess whether Trump’s tariffs will last and if so, at what level and for how long. In contrast, as Napier points out in his latest Solid Ground letter, “The Anguish of Central Banking 2: Just When You Thought It Was Safe To Go Back In The Water,” there is really just one issue to focus on: Excessively high debt burdens among all the largest economies.

To be sure, excessive debt is a complicated issue that is affected by many different factors, but it’s pretty easy to trace most of the serious imbalances back to weak consumer demand in China. That weak consumer demand gets compensated for by exporting excess manufacturing supply and then creates problems all over the world.

Napier contends this problem will get solved one way or another and surely that is right. If debt continues to rise, it will strangle economic growth. In democracies anyway, that would almost certainly cause severe political pushback. The least bad prescription is financial repression, whereby bond yields are kept below inflation. So yes, the problem will get resolved one way or another.

The path between here and there is uncertain, however, and probably even more uncertain with the Trump administration. How long with the Fed hold out before easing policy? How effective will monetary policy be in this environment? Will the Trump administration loosen fiscal spending even as deficits reach extreme levels? How long will bond yields hold?

Clearly there are lots of moving parts and lots of possible scenarios for the interim. My baseline scenario involves an economic downturn in the near term. That will provide cover for the Fed to ease policy and for the Trump administration to select its preferred ways to stimulate the economy. Whether those policy responses lead constructively to financial repression, or to something else, remains a major uncertainty.

Investment landscape II

Massive volatility in the last few weeks is causing a great deal of consternation and a fair amount of anxiety as to what it portends for markets. Endgame Macro provided some excellent perspective on the phenomenon.

In one post, the volatility was described not as market panic, but rather “a trust rotation not just out of risk assets, but out of the very institutions that once anchored global stability.” It went on to summarize, “ This Isn’t Just De-Risking. It’s De-Trusting.”

Another post described the unusual ensemble of activity as a “credibility fracture” and went on to conclude, “This is what it looks like when trust begins to unwind at the sovereign core.”

In so many words, what these commentaries are saying is the Trump administration’s approach to trade and international relations in general is causing global investors to question the fundamental safety of US investments — including Treasury bonds.

Pressure has backed off a little bit, but that is deceptive. Once you question the reliability of counterparty, there is no going back. The damage to credibility and trust is done.

That damage was further highlighted when, according to the FT ($), “Donald Trump’s top economic adviser Stephen Miran struggled to reassure leading bond investors in a meeting last week that followed a bout of intense tumult on Wall Street triggered by the president’s tariffs.” According to the report:

“[Miran] got questions and that’s when it fell apart,” said one person familiar with the meeting. “When you’re with an audience that knows a lot, the talking points are taken apart pretty quickly.”

One point is this arguably shouldn’t have been too much of a surprise. In February I wrote, “In my reading of the [Miran’s] paper, I felt it fell far short of persuasive economic policy advice.” I don’t think this was a contentious statement; the weak arguments were there for all to see and pick apart.

Another point though, is the scrutiny is becoming increasingly public. Not only are more people gaining first hand knowledge of the Trump administration’s policy arguments, they are also gaining first hand knowledge of the people promoting them, and finding those people to be “out of their depth”. The more this happens, the more the “credibility fracture” worsens.

Investment landscape III

Even with Wednesday’s early data-driven selloff, equity investors still seemed content to mainly ignore the din of weakening fundamentals, excessive valuations, and increasing uncertainty. John Hussman captured the sentiment in a post:

investors so frantic about not missing the "tariff normalization" trade that they've driven the S&P 500 back to where it was before tariffs were announced

not a forecast, but given an active recession warning composite and an open valuations/internals trap door, the unwind may be spectacular

Alyosha ($) shared a similar sentiment from a trader’s perspective:

My two cents is a fitting contribution to the curious. There isn’t enough money to pay for the rips and rallies of yore when the government sent everyone a check and mainlined $6 trillion into stocks. This is so not “run hot.” This is the detox. It takes a lot of money to get to 6000 on the S&P, and that money left the building weeks ago.

At this point, the most likely scenario is an economic slowdown for some period of time eventually followed by public policy responses to stabilize and revitalize the economy. The longer it takes market prices to adjust to that likelihood, however, the greater risk of rapid and severe market selloff.

Worse, without a significant adjustment (downward) in market prices, there is a risk that a whole slew of disruptive influences could start hitting all at once in a “mass realization event”. Imagine if tariffs and other public policy measures, along with a relatively tight Fed really do slow down growth significantly. Also imagine that supply chain disruptions cause prices to continue to rise. Imagine fiscal deficits exploding even higher while tax cuts threaten to make them even worse. Imagine a Treasury that needs to significantly increase bond issuance at a time of heightened “credibility fracture”. Imagine looser monetary policy is completely ineffectual and the Trump administration is not equipped to course correct with stimulative fiscal policy. Imagine at the worst possible time, geopolitical conflict escalates significantly.

Is this scenario a slam dunk? Absolutely not. Is it a vanishly small likelihood? Absolutely not. When things have gone so right for so long, it can be easy to forget how many things can go wrong.

Implications

One major implication of the current environment is there are no easy answers. As a result, it is silly to hold out hope for DOGE to really gain traction or for a slew of tariff deals to come through or whatever. Even if those things happened, the bigger problem problem would not yet have been solved.

Another implication is the Trump administration is not on a constructive path. Negative sentiment readings and declining poll results indicate there is a significant gap between Trump administration goals and the will of the people. This is not sustainable.

As a result, there are two general ways forward. One is that politics continues to exert its force and the Trump administration eventually concedes. This would lead to an environment of persistent inflation through monetary debasement. It will probably require an initial foray into recession, however, to justify significant monetary expansion without undermining the value of the US dollar.

A second path would involve a disorderly dislocation rather than a more orderly adjustement. This option would become more likely in the event the Trump administration fails to react to political feedback and adapt and instead unilaterally pursues its own agenda at the expense of the country and its own political approval.

It’s frighteningly easy to imagine ways in which it might manifest as well. If Scott Bessent suddenly quit or was fired markets would erupt. The possibilities are endless though. As Ian Bremmer points out, “President Trump individually concentrates so much more decision-making authority than any other president in modern US history”. This means the potential for capricious, and world-changing, action is always a risk. Invest accordingly.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.