Observations by David Robertson, 6/6/25

While the news flow has continued, stocks have barely reacted. It’s like they turned the sound off. Let’s dig in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

The most notable observation of the stock market over the last few weeks has been how little it has moved. Despite a continuing onslaught of political uncertainty, the VIX volatility index is bouncing around its lowest levels since the inauguration and stocks seem like they are on autopilot. As Tier1 Alpha posts, “The consolidation continues. $SPX hasn't closed more than 1.7% away from the 5900 strike in over three weeks.”

Even the soft ADP employment and weak ISM services numbers on Wednesday, which caused Treasury yields to decline, left stocks essentially unchanged. The one thing that has been working, as illustrated by The Daily Shot, is artificial intelligence-related stocks.

Politics and public policy I

Why doesn’t government work in the US? ($)

https://www.ft.com/content/44a69ce3-7398-40f4-9fff-5c89e04b6d38

The general sense that things don’t work the way they once did contributes directly to Americans’ enormous cynicism about government, and is one factor explaining Donald Trump’s popular support.

Beginning in the 1960s, however, activists on both the right and left increasingly saw the government as a negative force that was corrupt, captured or simply incompetent, one that had to be constrained by multiple layers of rules and procedures.

Conservatives have been arguing for decades that we are living under a tyranny of “unelected bureaucrats” who make up rules on their own outside the control of democratically elected officials. The truth is rather the opposite: because America has a long history of distrusting government, we have added layer after layer of procedures that limit what officials can do.

In his usual manner, Francis Fukuyama provides a great deal of perspective to the discussion about government ineffectiveness. For one, he very much acknowledges this was a key issue in helping Trump get elected: “The general sense that things don’t work the way they once did contributes directly to Americans’ enormous cynicism about government, and is one factor explaining Donald Trump’s popular support.”

The main problem that explains government ineffectiveness, according to Fukuyama, is an ever-increasing compliance burden on government employees. Indeed, if businesses think they have an unseemly amount of red tape to work around, most government officials have even more! In both cases, there are good reasons to have some constraints; but there also needs to be enough flexibility to function.

In this respect, government is like a computer cache that is full of crap and needs to be cleared in order to function properly. Or like a hoarder who can’t even move around the house any more because things are piled up everywhere. It mainly needs to be cleaned out.

While Fukuyama’s argument is extremely plausible, it is probably not surprising to note the Trump administration offers a very different diagnosis. It claims the main problem is a bunch of loose cannons arbitrarily exceeding their authority. While this does happen, by all appearances it is the exception and not the rule. Besides, it is an oddly incoherent claim that government is inefficient and ineffective because government employees have too much authority to get things done rather than too little.

Much of the argument about increasing government effectiveness boils down to one’s beliefs as to what the proper role of government is. If you believe the less government the better, then government effectiveness can be improved by shrinking it. If necessary, tear it down and rebuild later. This seems to be the view of the Trump administration and is captured in its admonishment of the “Deep State”.

If you believe government provides many valuable services but is handcuffed by too many rules that limit its flexibility to accomplish things, then a refresh of governance is required. In order for that to happen, however, people need to appreciate the value of government services. As Gary Gerstle ($) noted in the FT: “No progressive movement can succeed without restoring popular faith in the positive uses of government.

With an increasing number of accounts of Trump voters who become disappointed by the negative consequences of Trump policies on them personally, it is hard to avoid the speculation that perhaps those supporters just didn’t really appreciate the value of government services until they no longer received them. If absence makes the heart grow fonder, perhaps a dramatic reduction in government services will be required to raise awareness and increase appreciation of them?

Politics and public policy II

Pretext Upon Pretext ($)

https://thedispatch.com/newsletter/gfile/trump-administration-tariffs-congress-constitution/

Anyway, the point is that virtually the entire agenda of the second Trump administration is grounded in pretextual arguments. On almost every front, his stated arguments for why he’s doing what he’s doing, and from where he derives the authority to do it, are just BS.

But the stated arguments need some connective tissue with the facts, with truth, with good faith representations about motives and intent. When the arguments are all pretextual, you don’t get that. So arguments stop mattering because arguing with liars and fabulists is a waste of time. That’s why I am more interested in the legal fights, because at least in a courtroom, there’s a penalty for lying. In politics right now there are precious few penalties for lies, at least in part because a lot of voters have lost faith that politicians and the press really believe anything that they’re saying. If the politicians and pundits won’t bother caring about the truth, why should we? Better to just pick the lies you want to believe and call everyone else a liar for choosing different lies.

Jonah Goldberg articulates a point I have been struggling with since the beginning of the Trump administration: If most of the rationale for policies are “just BS,” how does one think about and incorporate that reality into meaningful and actionable investment insights? Goldberg provides a great example, “He [Trump] invokes the Alien Enemies Act, which grants certain powers to the president during a war or invasion, when we’re not at war and not being invaded.”

With even a layperson’s reading, the justification is “just BS”. As a result, the easiest conclusion is that it is not representative of an authentic effort to govern. Further, in combination with what I wrote last week, the Project 2025 agenda, which is clearly a driving force in the Trump administration, is transparently NOT an effort to unify the country or to govern it as a whole. As Goldberg puts it, “The whole point of a pretextual argument is to craft a plausible, often hypothetical, case for doing something that you want to do anyway.” Sounds about right.

Unfortunately, as such, there is very little room for discussion. As Goldberg notes, “But you know who Trump’s obviously pretextual arguments work on? The people who simply want Trump to have as much power to do whatever he wants.” As a result, you either accept the BS as the means to an end you believe in, or you just accept that it’s all BS.

In the short-term, it’s hard to tell how Trump administration policies will work out due to all kinds of unpredictable and unknowable factors. In the longer-term though, the ongoing acquisition of knowledge and the development of social systems to enhance cooperation are the things that have led to the enormous success of the human species. Attacking those will most likely set it back.

Politics and public policy III

When a significant chunk of the Trump tariff scheme was invalidated last week, the administration’s narrative machine kicked into gear explaining the whole episode was just a bump in the road. Matt Stoller ($) posted a different view, however. He argues the ruling was based solidly on “both broad constitutional principles and a reading of the underlying statute”.

We’ll start with two separate theories of Constitution law. The first is called the “non-delegation doctrine.” That theory says that there must a meaningful separation of powers between the executive and legislative branches in the Constitution. As such, the legislative branch can’t just delegate its authority to the executive without some limiting principle. Delegating broad tariff-making authority to the President, which is a Congressional prerogative, falls under this theory.

Additionally, there’s something called the “major questions doctrine,” which the Supreme Court recently adopted. According to that doctrine, when the President wants to do something major, the law he’s using has to be extra clear on his authority.

The IEEPA law requires a declaration of emergency … The second set of tariffs were about dealing with the “emergency” of imbalanced trade. The court looked at the statutory language and said Congress did not allow broad trade imbalance of the kind cited by Trump to be considered an IEEPA emergency, but had to be addressed under a different trade law.

One conclusion from the recent tariff ruling is that Trump’s “credibility has diminished, and his legal tools are blunted”. The ruling is very clear that Trump exceeded his authority to impose tariffs on multiple fronts.

In addition, now everyone can see this, including countries on the receiving end of tariffs. As a result, any kind of leverage the Trump administration may have had is also greatly diminished. Any country being forced to accept high tariffs or any company being strong-armed into reshoring will be well advised to wait and see.

Of course, another big challenge will be determining the future direction of the Trump administration: Will it back off, keep on, or double down?

Paul Krugman ($) shared his views on Substack — and he doesn’t see an off-ramp to the tariff regime. He writes:

In a conversation I had with Joseph Politano, who has been following the tariff issue very closely, he predicted that tariffs would be going up, not down, from here. His reasoning was that Trump would begin adding tariffs on specific goods to across-the-board tariffs on everything we import from a country. So far it looks as if he’s right: The tariff rate on steel has just jumped from an already very high level of 25 percent to 50 percent.

While Politano’s outlook provides some useful insight, it also reveals the growing complexity of the challenge. First it was about how serious Trump was about tariffs, then it included the reaction function of the judiciary, then it included the reaction function of the Trump administration. At some point, it will include the reaction function of various trade partners. The number of variables keeps increasing.

Krugman provides the one assessment that can be made with some degree of certainty: “And the legal wrangles over what Trump can and can’t do will only add the the uncertainty and sense of chaos that is strangling business investment.”

Investment landscape I

Dollar’s correlation with Treasury yields breaks down ($)

https://www.ft.com/content/9ca05517-b3fb-46f1-9cde-866061e816a7

“The strength of the US dollar comes partly from its institutional integrity: the rule of law, independence of central banking and policy that’s predictable. These are the components that create the dollar as the reserve currency,” said Michael de Pass, global head of rates trading at Citadel Securities.

“The last three months have called that into question,” he said, adding that “a major concern for markets right now is whether we are chipping away at the institutional credibility of the dollar”.

One of the most notable, and important, phenomena of the last several months has been the break down of the historically tight relationship between the US dollar (USD) and longer-term Treasury yields.

Of note, there has been a whole litany of reasons for investors to harbor concerns over both USD and Treasury yields. The latest is Section 899 in the budget bill which creates the authority to impose incremental taxes on foreign holders of US assets.

John Authers ($) from Bloomberg calls it “The three numbers alarming the bond market.” The Economist ($) says, “America has found a new lever to squeeze foreigners for cash.” Gillian Tett ($) at the FT says, “There’s a ticking time bomb in Trump’s ‘big, beautiful bill’.”

Tett describes the provision as “a novel ‘revenge tax’ (as some lawyers call it) that Trump could use to bully friends and foes alike in trade negotiations.” She reports:

“Section 899 is toxic [and] a potential game-changer for foreign investment,” Larson Gross, a tax advisory group, told clients this week. Or as Neil Bass, a Canadian lawyer wrote in his own missive: “The US just declared a tax war and it’s targeting allies.”

The Economist highlighted the considerable change in tone of the provision towards foreigners: “Foreigners’ labour, investment and business operations in America are treated not as opportunities to be embraced, but choke-points to be squeezed.” It concluded, “If enacted, this would render America all-but-uninvestable for many foreigners.”

John Authers at Bloomberg provided a more general assessment in saying, “the way the bill is structured would permanently add a new risk, as the unfair taxers list would be revised every three months.” He also opined that the bill is “really likely to happen.”

In short, there are very good reasons why investors, especially foreign ones, are getting increasingly squeamish about the US dollar. According to Tett, “No wonder investment groups ranging from Canadian pension funds to mighty Asian institutions tell me that they are stealthily diversifying away from US assets.”

Investment landscape II

Treasury secretary Scott Bessent insists US will ‘never default’ on its debt ($)

https://www.ft.com/content/9c652f09-cfca-4078-9e2b-5fdacd772a75

“The United States of America is never going to default, that is never going to happen,” Bessent told CBS’s Face the Nation on Sunday. “We are on the warning track and we will never hit the wall.”

The first thing to recognize about Scott Bessent’s statement on Sunday morning is that it triggers rule number one in politics: If you have to make a public denial, that itself is a confirmation there is a problem. Or, as Ronald Reagan said, “If you’re explaining, you’re losing”.

It is also interesting that the issue of concern about the debt is being addressed seriously and publicly. Virtually every other pushback on Trump administration authority, including multiple violations of due process, gets unceremoniously relegated to soundbites and social media posts. The debt, however, gets a high profile meeting with the American public.

James Carville was probably right, the bond market can intimidate anybody. The important takeaway here is the bond market is beginning to intimidate the Trump administration.

Another thing to recognize in Bessent’s presentation is his pattern of awkward communication. Here’s my unsolicited tip for Mr. Bessent: If you are trying to provide calming words to the public, don’t use a metaphor with the word “warning” in it. That sort of undermines the whole exercise.

That wasn’t all, though. He later went on to say:

“The deficit this year is going to be lower than the deficit last year and, in two years, it will be lower again,” said Bessent.

This statement violates rule number two in politics: Don’t commit to things that are outside your control and that can be held against you in the future. With the bill still being debated and no formal reply from the Senate yet, let alone any kind of compromise between the House and Senate, it is too early to make any claims on what it will and will not provide.

Making such claims only undermines one’s credibility. One might dare to conjecture Mr. Bessent just isn’t cut out for this kind of work. But then, that isn’t exactly reassuring either, is it?

Investment landscape III

To date, most of the public policy debate in regard to foreign countries has been about tariffs. As Bob Elliott posted, however, we shouldn’t forget to think in broader terms:

Need to think about US-China engagement holistically rather than narrowly from a macro perspective. Found this useful, with the Hegseth comments as a kicker this weekend.

For one, these comments suggest a much broader application of tariffs than just combating persistent trade deficits. In addition, it appears tariffs are also playing a role in strategic positioning in regard to China, in particular.

This corroborates what I have written several times before that the conflict with China runs deep and will not be “solved” easily, and the trajectory of the relationship increasingly appears to be a Cold War. As a result, the imposition of tariffs on China may not even be mainly about tariffs, but a different angle of a broader conflict.

Russell Napier highlighted the possibility of more intense conflict with China in his latest Sold Ground newsletter by quoting liberally from a speech by Secretary of Defense, Pete Hegseth, on May 31st:

We are also increasing security in the western hemisphere, taking back The Panama Canal from Chinese influence…..Deterrence starts in our own backyard. Beyond our borders and beyond our neighbourhood, we are reorienting towards deterring aggression by communist China.

So first, the Department of Defense is prioritizing forward-postured, combat credible forces in the Western Pacific to deter by denial along the first and second island chains.

Hegseth goes on to express the intention of executing “peace through strength”. To my ears, thems sound like fightin’ words. Investors who are fixated on whether tariffs will be 10%, 20% or some other figure, might be missing the more important message here.

Investment landscape IV

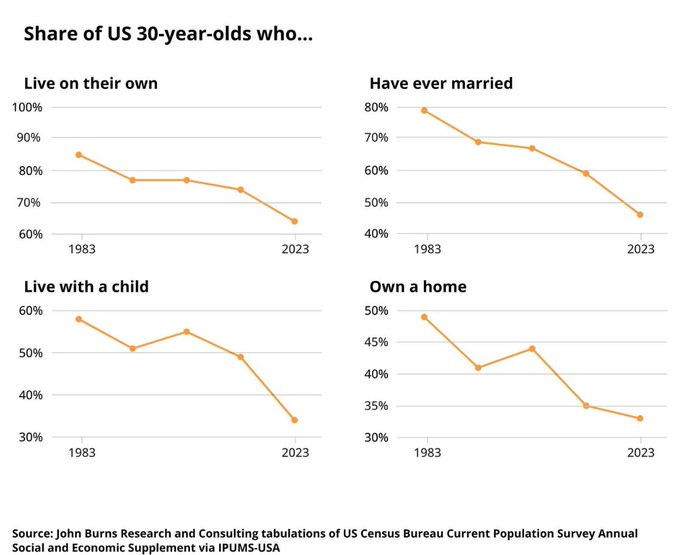

While there has been widespread dissatisfaction with government, younger generations arguably have more valid claims than anyone else. After all, they are they ones being saddled with rising debts and poorer economic opportunities.

Morgan Housel put out a post on social media that at once identifies investment wisdom and provides a stinging commentary on public policy:

The 3 keys to wealth are:

- Patience

- Diversification

- Being born in an era that aligns your first home purchase with the occasional window of cheap home prices or low interest rates.

What goes unsaid is that if you are of an age to consider your first home purchase, and house prices are at record highs, even though interest rates have also come up a great deal, then you are going to be significantly constrained in accumulating wealth. As unpleasant and unfair as it is, those are just the facts.

Geiger Capital illustrates the increasing challenges for younger adults even more explicitly in a post:

The collapse of healthy society and the middle class. A direct result of catastrophic policy and deficit spending. Our leaders borrowed prosperity from future generations.

As the charts show all-too-clearly, the probability of young adults today to form households is considerably lower than it was forty years ago. Whatever benefits public policy may have delivered over those years, these are the costs.

That would be bad enough, but the House’s budget bill that is currently in the Senate for review mainly makes things worse, not better for young adults. This pattern is likely to continue until there is meaningful political pushback. The most surprising thing to me is there just doesn’t seem to be much resistance, at least not yet.

Implications

The eerie sense of calm in stocks may reflect the start of summer and a much-needed slower pace for investors and traders. Given the events on the horizon, however, it may also be the calm before the storm.

For one, once the budget bill passes this summer, the focus will shift to ever-growing signs of a slowing economy. Slower growth and higher prices will be exacerbated by the effects of tariffs and other policies making their way through the economy.

For another, once the debt ceiling is lifted, the Treasury will need to issue outsized amounts of debt to restore its general account. That will suck liquidity out of the system and provide a strong headwind for asset prices.

Finally, as global investors are already on edge, the passing of time significantly increases the chances that foreign ownership of US assets starts falling on the margin at least.

In short, the forecast is for a high probability of turbulence later this summer and into the fall.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.