Observations by David Robertson, 7/26/24

There was a surprising amount of news for a week in the middle of the summer. Let’s jump right in.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

There is a lot that can be written about politics and its implications right now but Matt Stoller captures the main takeaway as well as anyone:

This election is so weird in that Kamala Harris who couldn't seem more corporate is attacking Donald Trump on populist grounds and Donald Trump who couldn't seem more populist is going full corporate, and neither of them have told the country what they plan to do if elected.

Politics may or may not have been the reason for Wednesday’s selloff, but selloff it was. In action that investors haven’t seen for a long time, prices started down about one percent at the open and with the exception of a short break for lunch, kept leaking lower all day.

The slow and steady move down suggests poor liquidity was at least part of the issue. The fact that gold stocks started the day off moderately positive but were mostly down by the end of the day also pointed to poor liquidity. When you have to sell, you sell what you can.

With a combination of some weak earnings, talk about weakening the US dollar (USD), hefty auctions for Treasury bonds this week (to be issued next week), and exposures to stock being generally very high across the investment universe, there were plenty of reasons why stocks might have sold off. The bigger question is to what extent this move is an omen for the month of August, which historically has some of the lowest liquidity of the year.

In other news, Robert Armstrong ($) reported on Lamb Weston’s big selloff (down 28%) on Wednesday. He summarized the CEO’s comments: “competition is forcing us to cut prices, and future revenue and profit growth will be — for the first time in years — driven by selling more potatoes” Of course the way the company had been driving revenues was by raising prices.

When I mentioned last week, “It will be interesting to see if pressure on margins on is becoming apparent in quarterly reports the next few weeks,” this is exhibit A. The answer is, “Yes”.

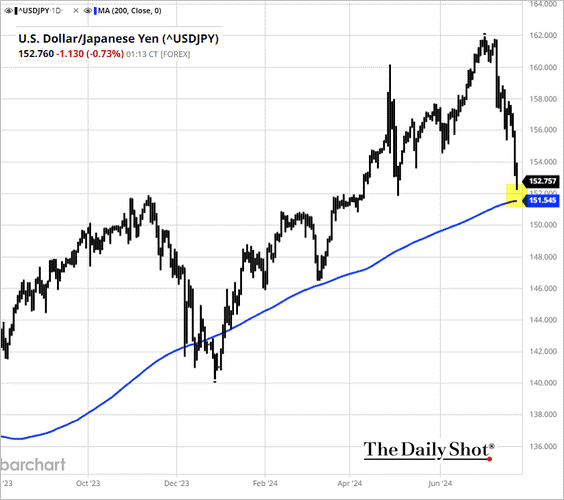

Finally, as Almost Daily Grant’s (Wednesday, July 24, 2024) notes, “Monetary crosswinds are swirling in the Far East.” Indeed, the graph from @SoberLook vividly illustrates the dramatic reversal in the Japanese yen.

While the move has been amplified by interventions from the Ministry of Finance and expectations of a rate increase, it was also surely affected by the unwinding of a popular carry trade. As such, this may be the source of some of the selling pressure this week as well.

China

China’s Third plenum concluded and we are starting to get a sense of what its public policy priorities will be over the next several years. This comment from George Magnus sums it up pretty well:

The read out indicates party is as focused on security as on economy. No change there. But there’s an unusual big focus on international relations material. Suggests econ, security, geopol are indistinguishable. Message for foreign firms: you’ve been warned, know it or not

He concludes with:

Finally, high quality development - the elixir -> innovation and higher TFP [Total Factor Productivity]. Drumroll for new productive forces and science, tech, education. Aka industrial policy on steroids, exports, hacking off many countries. This is a big deal, but not nec w/ good outcomes . Stay tuned

As Magnus puts it, the development efforts amount to “industrial policy on steroids”. As a result, it will be fair to expect continued tensions in global trade and mixed results on China’s economic recovery. While this doesn’t amount to a significant incremental change for China policy, it does highlight a model that is very different than the one many of China’s business partners are currently working with. As Magnus notes, “you’ve been warned”.

Oil

China Sputtering ($)

https://www.commoditycontext.com/p/china-sputtering

Apparent Chinese petroleum consumption is contracting, becoming a drag on global demand growth after last year’s unprecedented Chinese advance drove three-quarters of global gains.

Demand growth is slowing across all major petroleum products, but weakness is especially stark in industrial-linked fuels like diesel, which are suffering both from slower industrial activity as well as direct displacement by other fuels like LNG in the core heavy transportation sector.

Rory Johnston recently highlighted the visible weakness in China’s consumption of oil. While this certainly serves as a warning flag for slowing growth in China, the analysis is complicated by a separate, countervailing factor: China’s transport industry is rapidly switching from diesel to liquified natural gas (LNG) as its primary fuel:

Domestic Chinese analysts are increasingly pointing to displacement in the heavy duty transport sector by liquified natural gas (LNG), to the tune of somewhere between 300-600 kbpd

The far lower landed price of LNG as well as new trucking emissions standards have driven the accelerated rate of LNG truck adoption, with LNG truck sales up 127% y/y to 92.6k units so far this year, roughly one-fifth of total truck sales.

This is interesting for a couple of reasons. First, it highlights a very real, large scale energy arbitrage by a major economy. Natural gas is a lot cheaper on a per/BTU basis than oil. If the natural gas conversion continues in China, and/or is also adopted by other large economies, the dent in global petroleum demand will be significant.

Second, the decision to convert heavy duty transport to natural gas from oil depends on long-term forecasts for both oil and natural gas. By moving toward natural gas, China is implying it anticipates the energy arbitrage continuing. That may be due to either the expectation of cheap natural gas from Russia, increasingly expensive oil on the open market, or both.

Commodities

Copper miners expect shift to direct deals with users ($)

https://www.ft.com/content/220ef9d2-df1e-4b93-b044-fb1957591428

The world’s largest copper miners predict closer collaboration with end users from carmakers to utilities, upending a hitherto fragmented supply chain as shortages of the metal crucial to green technologies are set to flare up in the years ahead.

“Ultimately those that will be utilising the copper — whether that is for charging stations, grid buildout or vehicles — will start to get more interested in how they access this copper,” said Jonathan Price, chief executive of Teck Resources, a Canadian copper and zinc producer.

In the idyllic world of neoliberal globalism, commodities are in endless supply at cheap prices and can be cheaply and effortlessly hedged. In the world of increasing geopolitical tensions and trade barriers, it’s not just the price of supply that matters but also the reliability of that supply. Big producers must be able to ensure long-term sources or they will suffer expensive shutdowns. As the FT relates, the process of alleviating these challenges is already happening in copper. The fact that it is happening while spot copper prices continue to fall highlights the magnitude of divergence between short- and long-term views.

As longer-term supply arrangements proliferate, a couple of things happen. One is the short-term prices on exchanges become progressively less important because they become progressively less relevant to the economics of the industry; they aren’t the prices at which most business gets done. By the same token, longer-term supply contract prices become even more reflective of longer-term supply economics.

For old hands in commodities markets, this is nothing new. It is the price at which long-term supply is set that dictates the economics of reinvestment and therefore supply growth. For speculators, however, the game fundamentally changes as the bulk of supply switches to longer-term contracts. Short-term prices still whip up and whip down, but rather than adhering to past trend channels, they start gravitating to (higher) price ranges that can justify reinvestment. While it may not look like it right now, this is coming for copper - and a lot of other commodities.

Monetary policy

Stephen Miran put out a great post discussing how the Treasury’s recent practice of issuing a disproportionate amount of Treasury bills (relative to longer-term coupons) has amounted to large scale monetary easing:

Summary: changes to Treasury's issuance policies have provided similar economic stimulus as a 1% cut in the Fed Funds rate, usurping core functions of monetary policy and blocking the Fed's efforts to restrain inflation and growth.

While there isn’t a whole lot of new information here, per se, and I have been reporting on the story in Observations, this is an especially good summary of the phenomenon that Miran calls Activist Treasury Issuance or ATI. The main result has been:

In other words, the Fed is not as restrictive as they think they are. ATI has blocked the Fed's attempts to restrain growth and inflation, offsetting all hikes in 2023 and helping to explain persistently strong nominal growth over the last two years.

This is exactly what I was talking about in the market review for the second quarter entitled, “The Fed’s kaput”. In short, to the extent investors are looking to the Fed and when it cuts rates for guidance into the market, they are looking in the wrong place. Lately, the key driver has been Treasury through ATI.

The question of how long Treasury may continue in its efforts to stimulate the economy through excess liquidity provision is an open question, and an important one. If it continues, “we are likely to transition into a world of more emphatic political business cycles”. If it is unwound, it “will have a temporary contractionary effect on the economy equivalent to 2% of hikes in the Funds rate”.

The bigger picture issue is the same. Whether it is the Fed helping things along with liquidity provisions, or the Treasury, the bottom line is the same: Organic economic growth is not strong enough to support existing debt levels without being very disruptive. One way or another, this reality will become actualized - either through weaker growth or higher inflation.

Currencies I

More on dollar devaluation ($)

https://www.ft.com/content/9d19b4c6-105c-4324-a188-59df963393a1

We also suggested that a tax on foreign holding of US assets, one of the ways to force devaluation, would be a “doomsday” scenario for the market. Pettis argues that a tax on holding the US dollar is the most practical way to close the US trade deficit. He reasons that the US trade deficit is fuelled by its much larger capital account imbalance, and resolving the gap between investment and savings in the US by restraining capital flows would in turn resolve the trade deficit. Tariffs would not be nearly as effective.

With one of the dominant policy priorities of Trump being to weaken the US dollar, quite a bit of commentary this week focused on the issue. As the FT’s Unhedged letter reveals, “a tax on holding the US dollar is the most practical way to close the US trade deficit”.

That policy comes with a nasty side-effect, however: It “removes one of the biggest tailwinds supporting the very high valuations of US financial assets”. Indeed, this is increasingly the dilemma facing most public policy proposals. It’s just getting harder and harder to provide goodies to constituents without having negative consequences become almost immediately apparent.

Charles Gave viewed the issue from a different perspective. Reported by John Authers ($), he notes, “instead of buying US Treasuries as they did in the past, the foreign holders of US dollars have bought the shares of these information oligopolies —otherwise known as the Magnificent Seven”.

As a result, his recommendation to weaken the US dollar is to “emulate Theodore Roosevelt” and “go after the Magnificent Seven and their like and break them up.” By making the Magnificent Seven less attractive to foreign buyers, there would be less upward pressure on USD. Fair enough, that could work too.

The interesting element of both proposals, however, is that their implementation would be largely antithetical to continued market strength. So, the open question is would Trump be willing to sacrifice levitating financial assets for his favored policy? Even if the policy accomplished its goal of weakening the dollar, would he be willing to accept the consequences of substantially lower prices for financial assets?

The challenge is even further complicated by the likelihood of a strategic response from other major trade partners. If the US dollar was intentionally devalued in order to gain advantage in trade, it would be fair to expect other major trade partners to devalue in kind. The logical end of that game is much higher commodity prices.

Currencies II

While we’re on the subject of currencies, it’s also appropriate to talk about the Chinese yuan. As Russell Napier highlighted in his early July Solid Ground letter ($), he thinks China’s authorities “will have to back away from their exchange rate management regime” fairly soon in order to prevent a disorderly debt deflation.

This raises an important possibility. While US investors are focused on domestic politics, the potential for getting blindsided by a deflationary blast from China is increasing. While I don’t think it is likely China will drag the rest of the world down with it, the outcome will depend on the timing and efficacy of policy responses.

The main takeaway is there is a lot of room for investors to get wrong-footed. I wouldn’t be surprised to see a deflationary wave scare the bejesus out of investors only to be quickly followed by aggressive stimulus that leads to significantly higher inflation. Things are getting interesting.

Investment landscape I

You’re Soaking in It

https://www.hussmanfunds.com/comment/mc240721/

Yet despite the rise and dominance of the internet, smartphones, advanced semiconductors, social media, and process efficiencies driven by technology, real U.S. GDP growth and real U.S. corporate revenues have grown slower, not faster, over the past 20 years than during the past 30, 45, 60, and 75 years.

Structural growth has slowed progressively in recent decades both because U.S. demographic labor force growth has slowed, and because cycle after cycle of speculative malinvestment – encouraged by cheap money – has left us with an economy that generates progressively less net domestic investment in each cycle, as a share of corporate revenues and GDP. Despite all the fanciful noise about technological innovation unleashing untold growth, an economy that prioritizes financial speculation over productive investment ultimately cannot produce the long-term cash flows that justify that speculation.

Here is another periodic reminder that stocks have not been rising because of enormous economic growth. Not even remotely. As Hussman describes, “real ‘structural’ GDP growth” is “only about 2% annually”. So, while technology and AI and whatever make nice stories, they are wholly overwhelmed by the realities of low labor force growth and persistent speculative malinvestment. Structural growth is slowing down, not speeding up.

Some investors will come back with something like, “bu … bu … but … inflation hedge”. Yes, while it is true stocks can provide a good hedge against inflation, the quality of that provision is conditional on starting conditions. As Hussman describes, “Whatever reputation stocks have as an ‘inflation hedge’ has been earned during periods of below-average valuations, modest inflation, or both.” In other words, when stocks are at record high valuations as they are now, they do not provide good inflation protection.

Portfolio strategy

The dramatic political events of the last few weeks combined with the massive rotation into small caps have definitely given a sense that this is more than just a regular hiccup in the market. At very least, these events give the appearance that the market is no longer on autopilot.

Exactly what may be in store is open to debate, but Michael Kao makes a good point in a recent post: “I'm starting to see Idiosyncratic value being cast off amidst this Beta meltdown, so that makes me wary that we might be approaching a Correlation 1 event.” In other words, we may be approaching a liquidity event in which all risk assets get sold at the same time because nobody has enough liquidity.

While I don’t believe we are right at the cusp of a major selloff, I do believe Kao is right that some funky things are going on and it makes sense to peel back some risk on the margin.

There are two reasons for this. First, because the markets are increasingly fragile, it wouldn’t necessarily take a lot to initiate selling. In addition, because players are fairly leveraged, it wouldn’t take a lot of selling to metastasize into something much bigger.

Second, with Biden out as head of the Democratic ticket, the playbook of political economics becomes a lot more uncertain. Will Harris receive the same kind of fiscal and monetary support that Biden would have? How many of those people in the Biden administration will be looking for jobs elsewhere instead? At very least, it’s fair to say most scenarios are less positive for the market, through the end of the year at least, now that Biden has dropped out.

Implications

Taking the subject of politics a bit further, one thing the race had with Biden in it was some degree of policy cohesiveness. Whether one liked his policies or not, Biden did have fairly consistent beliefs in areas like foreign relations, national security, and industrial policy. With Trump and Harris now the top contenders, these two are much more purely political creatures with few principles to guide policy direction.

While this view may be too cynical, let’s play it out in a thought experiment. Let’s assume that over the next few months, voters hear all kinds of promises about delivering goodies, but with no viable means of doing so. Neither major party demonstrates the capacity for thoughtful leadership on public policy or a sincere effort to unite the country.

True partisans are alright with it, but no one else is. Anybody but the true zealots simply opt out from a combination of disgust and fatigue with the whole thing. Suppose turnout is really poor. Regardless of who wins, the race will lack a strong sense of legitimacy and may even be contended for an extended period of time.

To be sure, this scenario may be wrong. Nonetheless, it illustrates that a lot of different and unexpected things can happen between now and November 5. The main point is this is no longer just any election: It has a far wider universe of possible outcomes than most. As a result, I think it makes sense to consider the “chaos” trade every bit as much as the “Trump” trade.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.