Observations by David Robertson, 8/11/23

After stocks were down week last week, they bounced around this week. Weak summer volumes certainly can explain part of the erratic behavior, but it feels like something bigger is going on.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

This is a timely update from themarketear.com ($) on CTA positioning. CTAs are funds that follow trends across several different asset classes. Many of them use stocks as one of the asset classes.

One of the characteristics of CTAs is they are formulaic: Either something is trending, or it isn’t. There is no debate, no subjective assessment. Rules are rules. This graph shows CTAs as a group are about as leveraged to stocks as they ever are. That also means when the trend changes, CTAs as a group will have to sell stocks and that is likely to put further pressure on stocks.

One a different front, natural gas prices in Europe popped this week. The graph from @SoberLook reveals the move to be the most consequential since Russia invaded Ukraine.

The proximate cause of the spike was concern about a strike at LNG facilities on the other side of the world in Australia. While other factors were surely at work, the extreme sensitivity reveals an important vulnerability in Europe that does not seem to be fully discounted.

China

If you subscribe to the “mosaic” theory of financial analysis, results out of China lately paint an ugly picture. Imports and exports were both down significantly on a year-over-year basis and were also weak sequentially. The large and heretofore well-regarded property development company, Country Garden, missed payments on two international bonds sending it on a fast-track to default and dealing yet another blow to the real estate industry. Finally, as @SoberLook reports, Chinese prices are actually falling now.

The point of this is not to revel in doomsaying. Chinese authorities seem well aware of the challenges and are making attempts to resolve them. Rather, the point is to debunk the overly optimistic notion that things always work out for China. The challenges run deep and there is no easy way out. Expect a lot more unsatisfying economic news from the Middle Kingdom.

Politics

Why Joe Biden is the heir to Trump ($)

https://www.ft.com/content/f43f0e63-0fa4-4771-8eb4-b5d61f87ada4

Trump, however, repudiated the pro-globalisation consensus of the previous 40 years. On the campaign trail, he accused China of laughing at America and raping it. In his inaugural address, he lamented the “American carnage” that he blamed on globalisation.

And what has Biden done with all this “weird shit”? Rather than shovel it to one side, his administration has retained most of these Trump-era policies — and even built on them.

This piece by Gideon Rachman touches on a theme I have been following for a while - areas of overlap between between Republican and Democrat worldviews. As Rachman contends, it is fair to call Trump’s repudiation of “the pro-globalisation consensus” a “radical break from the past” from “free-market philosophy”.

Indeed, one of the lesser told stories is the degree to which the Biden administration has maintained positions similar to the Trump administration. As Rachman puts it, “Much as they would be loath to admit it, the Biden team has come to share many of Trump’s basic assumptions — about trade, globalisation and rivalry with China.”

The main takeaway for me is while a lot of people are preoccupied with getting triggered by cultural battles, they are missing a much more important phenomenon: There has been a “radical break from the past” that happens to transcend political affiliation. It will be interesting to watch if this increases the migration of one or both parties to the “center”.

Inflation

Inflation, still scary ($)

https://www.ft.com/content/254a46d6-8a58-44d0-83f4-267830119897

Because the sharpest inflation increases happened in the first half of 2022, annual comparisons for the rest of this year’s CPI reports will be boosted by more slowly rising denominators. The dominant soft-landing market narrative is anchored in part by the pretty little 3-handle on current headline annual inflation. If this starts rising, even if it reflects a tame monthly rate, investors could begin doubting their assumptions about how immaculate disinflation will be.

Ethan Wu highlights the importance of “base effects” in framing the appearance of inflation. While I pointed out the same issue in the 7/7 Observations, the issue is more immediate now, especially so with longer-term inflation expectations also on the rise (per @SoberLook):

The bottom line is that recent market outperformance was based on a narrative of “immaculate disinflation”. Any little dent in that story (and there are plenty of things that can go wrong with the story) and investors will start discounting higher inflation (and lower stocks) again.

Monetary policy

One story that has been lingering in the background but I think is telling is that of Treasury buybacks. The following is a brief explanation posted by @FedGuy12, Joseph Wang:

Some details on Treasury's new buyback program starting next year (ht @BlacklionCTA):

It's going to be small - maximum of $240b a year ($120 in liquidity purchases and $120 in cash management)

I think this is telling on a couple of fronts. First, when the idea of buybacks was initially circulated, a number of commentators immediately characterized it as a backdoor effort at Quantitative Easing (QE). While I certainly reserve a fair amount of skepticism about the intentions of public policy, this characterization describes the pre-pandemic policy environment much better than the current one.

I read the policy differently. I believe a major government policy goal is to keep the Treasury market functioning properly. The potential for downside became clear in March 2020 and was highlighted again with the gilts crisis in the UK in September last year. Ultimately, the market needs to be restructured for better resilience but that will take time. Short of that, the buyback option is an appropriate intervening step in the right direction. For what it’s worth, Andy Constan is unambiguous that buybacks are not QE.

As such, the buyback option as currently outlined is completely consistent with the expectation for future policy responses I outlined in January:

baseline policy will remain slow and gradual. It also means if interventions are required, they will likely be much more surgical and limited than in the past.

For many reasons then, the evidence points to “surgical and limited” interventions as being the better explanation for the new buyback policy.

Public policy

One observation is that a number of investors are finding longer-term Treasuries attractive again. As the graph above from @SoberLook illustrates, retail purchases of the TLT ETF have been rising along with 10-year Treasury yields. Apparently, these investors are satisfied that inflation has been defeated.

This is interesting partly because disconfirming evidence is also widely available. Treasury’s recently publicized large increase in long-term debt issuance gives every indication that prices will need to come down and yields go up. At the same time, long-term inflation expectations are also increasing along with bond volatility. One might think investors would be more wary of long-term bonds right now.

The fact that they aren’t, however, is pretty darn consistent with the playbook I laid out in the second quarter Market Review. Insofar as government’s ultimate goal is to reduce debt through financial repression, it needs to be able to issue a lot of long-term debt at yields that will ultimately be lower than inflation. The best way to do that is to at least start the issuance process while inflation is at a low ebb (that is happening) and to also allow yields to bump up to relatively more attractive levels (that is also happening). To me, this looks like a plan coming together, not an attractive investment option.

Of course, there are limits to this and in extremis, there might not be enough demand for long-term Treasury debt. Stimpyz mitigates this concern in a recent Twitter post by highlighting an alternative view. US Treasuries have had to compete with enormous quantities of asset-backed securitizations (ABS) that have produced a useful substitute: “Synthetic safety”. As the ABS business model breaks down under higher short-term rates, US Treasuries will have less competition, and therefore greater demand. Yet another moving part.

Investment advisory

The Fees Are Too Damn High For Most Liquid Alts ($)

https://blog.unlimitedfunds.com/the-fees-are-too-damn-high-most-liquid-alts

Liquid alternatives products often offer the allure of returns that could benefit most portfolios - equity-like returns with lower market beta. Many managers in the sector are able to deliver that kind of outcome, but once these managers take their cut, most of these products go from making sense to being a bad deal.

Let’s start with the fees, which are as you might expect, are too damn high.1 The figure below shows the distribution of AUM by the all-in fees charged for small-scale investors (including a 3-year amortized load if applicable). Almost 50% of investor funds are in products with a 3% annual fee or higher.

It’s good to see someone else discuss a topic I have harped on repeatedly for over fifteen years. It’s not that professional money managers don’t have talent. The problem is they charge waaay too much for it. As Bob Elliott puts it in regard to liquid alternatives, “on average, the industry takes 100% of the alpha that it generates.” This means there are no excess returns left over for the investors to benefit from. You might as well invest in an index.

In regard to the fees, the industry has a terrible record as a whole, but there are exceptions. As Elliott explains, “there are diamonds in the rough that offer opportunities to benefit investors’ portfolios.” He goes on, “The products that are most compelling are those that not only deliver alpha, but also sport lower fees relative to that alpha than others in the sector.”

A final point to make is in regard to liquid alts. The label, “liquid alternatives”, is a marketing one; it doesn’t have any intuitive meaning for most investors so don’t feel bad if you don’t quite understand what it means. One manifestation is “equity-like returns with lower market beta”. Another is a fairly well diversified portfolio that produces better returns and lower risk than the traditional 60/40, stocks/bonds portfolio that is the bread and butter of the advisory community.

There is absolutely a solid investment rationale for breaking from the 60/40 schema. For one, both stocks and bond are currently overvalued. As a result, low, and perhaps even negative returns should be expected. For another, inflation wreaks havoc on such portfolios. This creates an imminent need for better expected returns and access to a broader array of return streams, as well as better protection against inflation and increasing volatility. None of this is easy or cheap to do well. The value of any individual proposition depends importantly on the fees.

As a postscript, I rarely talk about what Areté does in these pages, but these issues are so germane I’ll make an exception here. First, the idea of taking risk through the markets but sharing the benefits with investors has been a governing principle of Areté since its inception fifteen years ago. For another, Areté’s transition to its “All-Terrain” allocation strategy falls right in middle of the “liquid alts” trend. It is refreshing to see the proposition beginning to gain some traction.

Investment landscape

How bonds ate the entire financial system ($)

https://www.ft.com/content/5631cc22-a04d-405c-9154-e307f938f8f3

It is hard to overstate the importance of US government debt, or Treasury bonds. Besides its size — at $25tn, this is by far the biggest bond market in the world — the Treasuries market is essential to the functioning of the international financial system. Because of the US dollar’s status as the world’s dominant currency, Treasury yields are what almost everything else is priced off, and they act as collateral for all sorts of other transactions.

Mark Cabana, an analyst at Bank of America, warned that “large-scale illiquidity” was becoming a “national security issue”, with the US government facing the possibility that it might be unable to finance itself.

If you want a fairly concise, yet broad overview of financial history and summary of the key developments, you would be hard placed to find a better account than Robin Wigglesworth’s piece in the FT. Especially notable is the story of how the financial system has evolved away from banks and towards nonbank financial institutions (NBFIs), i.e., shadow banks.

This migration of finance away from banks is important for a number of reasons. For one, regulators have jurisdiction over banks, but not NBFIs. The more finance moves away from banks, the less control (and market insight) the regulators have to keep things safe. For another, the nonbank world of finance is still not well or broadly understood. For many of us, our college Econ books never even touched on the subject.

Given this, and given the “Treasuries market is essential to the functioning of the international financial system”, it is not hard to see how the world of nonbank finance can be perceived as a “national security issue”. If bad actors really wanted to, it’s not outlandish to picture a scheme to cause the nonbank finance sector to freeze up (a la Lehman in 2008) and wreak havoc on global financial markets.

This is the point I believe a number of investors are missing right now. They still see the Fed as driving policy and being naturally inclined toward easing. I think the Biden administration is correctly perceiving the national security risk of such undisciplined policy alongside a creaky Treasury market over which it has too little control. Such risks are especially evident in light of geopolitical threats from China and Russia, among others.

In sum, the risks of the growing nonbank financial system, ridiculously loose monetary policy, and poorly structured Treasury markets have been around for a long time. What is different now is the level of external threat. Insofar as this assessment is correct, expect continued progress on the war-readiness of the financial system.

Investment strategy

The more I think about it, the more I believe the model of four “Turnings” that Neil Howe discusses in his new book (and that I discussed in the note last week) is a very useful one for thinking about asset allocation and long-term investment strategy.

For starters, the notion that the length of a Four Turnings cycle is about that of a human lifetime suggests an investor should be prepared to encounter extremely different investment environments over the course of his or her lifetime. In addition, the cyclical nature of the Four Turnings suggests a recognizable pattern that can be used to identify landmarks in the cycle.

Perhaps most importantly, the characteristics of the different Turnings provide a basis by which to better understand the associated investment environments and all of the forces that impinge upon them. Politics always play a role, for example, but broadly reflect the priorities of society at any point in the cycle of Turnings.

For example, it was only after an extensive period of centralization that Reagan’s platform of deregulation in the 1980s struck such a political chord. Conversely, it was only after a long period of decentralization that voters today are beginning to prefer a greater degree of central control again. This is what good politicians do - they pick up on what society wants and manifest those desires in policies.

As a result, the forcefulness of public policy as well as its orientation (e.g. labor vs. capital) are largely functions of the societal landscape. Geopolitical priorities are also a function of the landscape. Elements of market structure are a function of the landscape. Even the function of capital markets themselves depend importantly on what society wants to get from them in any particular environment.

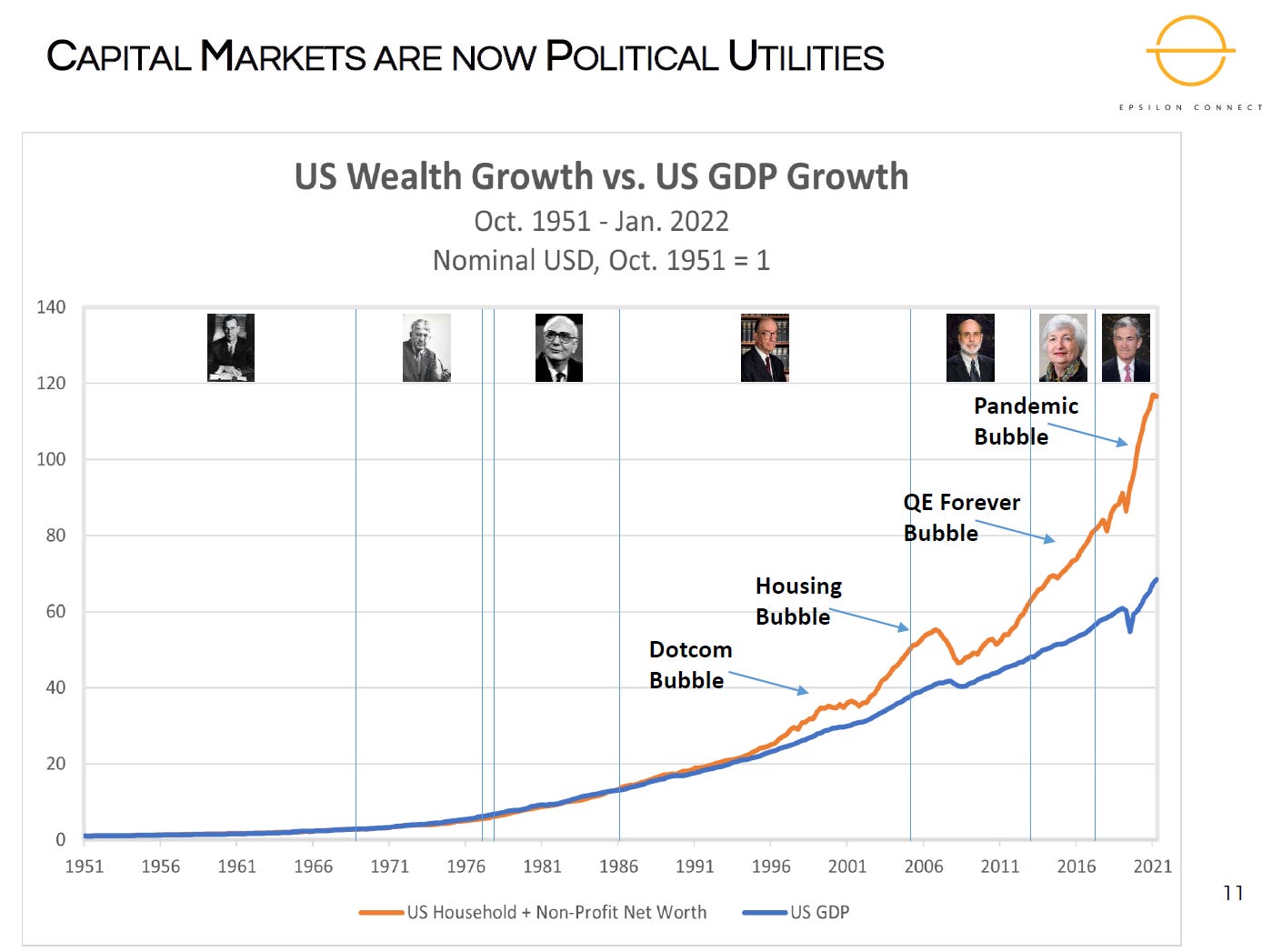

This is an extremely important point. As I also mentioned last week, Ben Hunt’s notion of capital markets as public utilities is a very useful one. Investors might assume, as I did at the time, that slow growth and rapidly increasing debt would eventually be extremely bad for stocks. That’s true, but only eventually.

During the interim, politicians need to get re-elected - and that can only happen when voters are reasonably pleased with the economic environment. That can only happen when either the economic environment either actually is strong, or alternatively, appears strong. Indeed, as the graph below from Ben Hunt illustrates, the latter has been more accurately the case since the mid-1990s.

The bottom line is Neil Howe’s model of Four Turnings provides valuable context from which to better understand the investment environment. All of the forces that can affect markets - public policy, market structure, and geopolitics, among others - get manifested differently in different environments. As a result, the Four Turnings model provides useful structure from which to interpret such factors.

Implications

One of the hardest things for investors to do is to change course. Part of this is due to a natural proclivity to think of history in linear terms. Part is due to the belief if something is working, there is no reason to change it. The cyclical model of Four Turnings addresses each of these issues. Over a longer period of time, history has recognizable cyclical patterns. As a result, if something has been working, it is only a matter of time before the “season” changes and that something stops working - and something else takes its place.

For better and worse, today’s investors have enjoyed over forty years of which the environment has been kind to both stocks and bonds. Now, the season is turning and about to become much more difficult for both. Just glance at the graph (above) of US wealth growth vs. GDP growth and you can get a rough idea of how much asset impairment is in store for wealth to reconnect with GDP. This is a major risk to avoid that traditional 60/40 portfolios are massively exposed to.

It is also important to understand the idea asset values are far too high is not merely an academic point or an ideological one. Asset values appreciated primarily due to artificially suppressed interest rates and excessively loose monetary policy. In a time of relative peace, these policies served a purpose. In a time of greater geopolitical conflict and a higher priority assigned to national security, these policies come across as dangerous security threats.

For example, suppressed interest rates facilitate misallocation of resources. This is a completely unacceptable condition for establishing war-readiness. Scarce resources must be used efficiently and effectively. That means more “normal” interest rates - which means short-term rates aren’t going down meaningfully any time soon unless a major catastrophe happens.

In addition, excessive asset values create significant potential for financial instability. With the massive expansion of asset-backed lending, a huge part of the financial world depends on relatively stable collateral values. This was one of the underlying vulnerabilities of the GFC. US home prices declined and that blew up a lot of financing vehicles. Inflated asset values would be an easy target for hostile parties in the event of a serious conflict.

Interestingly, and increasingly, the steady walk back of globalization and heightened prioritization of national security are not very partisan issues. While the preferred implementation is likely to vary by party, the underlying philosophy does not. This means important parts of public policy direction are changing regardless of who wins any given election - and that points to a very different investment environment.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.