Observations by David Robertson, 8/27/21

Welcome back!

As you may have noticed, I am modestly changing the title of the publication this week. I am keeping the “Observations” name because that still best describes what I report here. Rather than referring to Areté, however, I will simply attach my own name.

This change is intended to make the writing more accessible and to make it come across as more personal – because it is. I put in the time and the effort every week to write “Observations” for the purpose of helping people do better with their investments, not because I get paid a lot (or any) money or because I have nothing better to do.

I still really like the word areté because it represents so much of what I believe in – goodness, excellence, fulfillment of purpose, living up to one’s potential. For purposes of this letter, however, I will let those ideas reside in the background.

Let me know if you find the commentary helpful or not, or if you have comments. You can reach me at drobertson@areteam.com.

Market observations

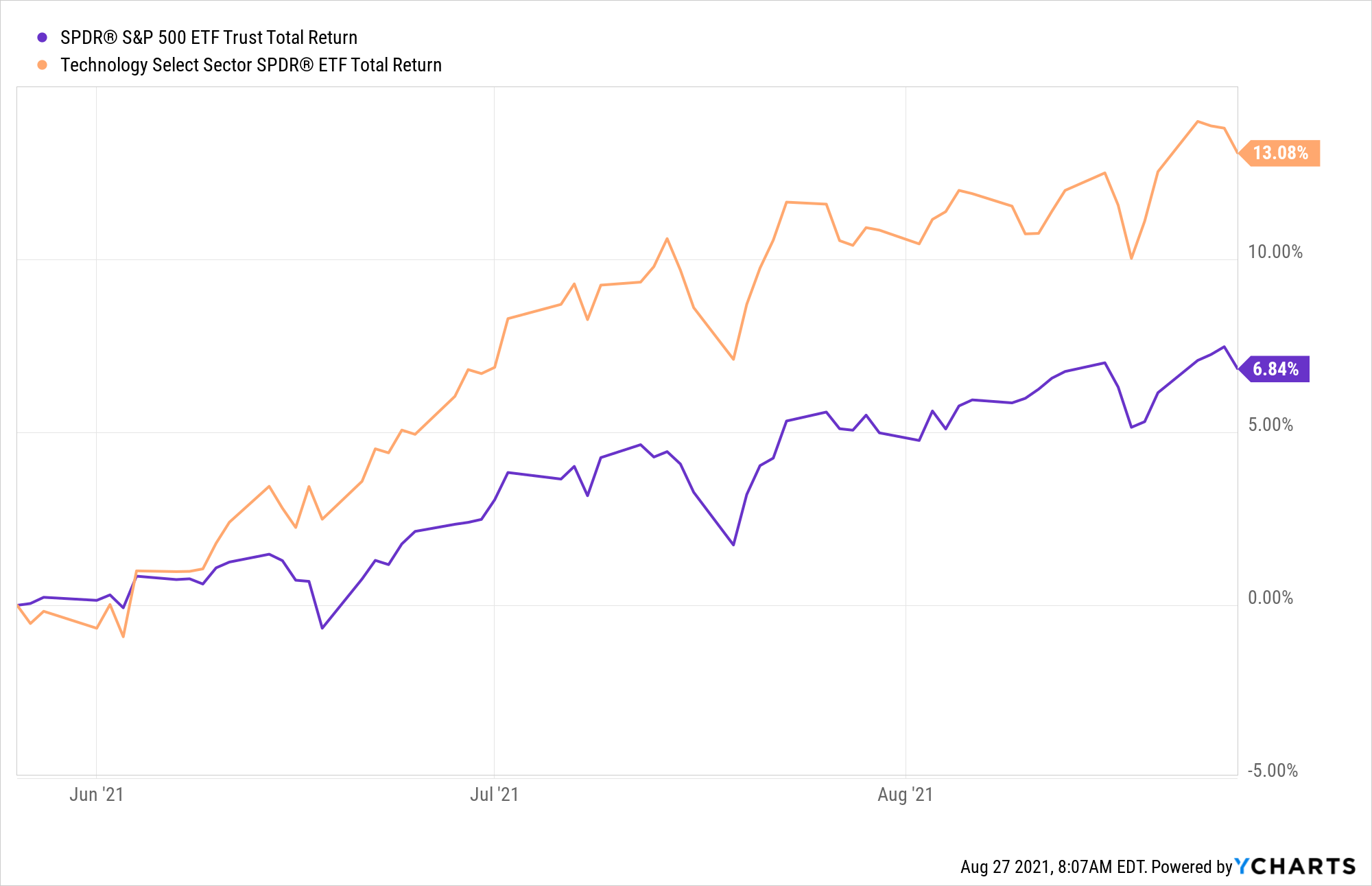

Stocks jumped out of the gates on Monday with the expectation no big news would come out of the Jackson Hole central banker summit this week given the recent decision to hold the event virtually instead. The trends have included a resurgence in tech and an easing of the reflation trade.

One-third of Investors Trade While Drunk

https://401kspecialistmag.com/one-third-of-investors-trade-while-drunk/

“One can imagine how trading apps make this easier than in the old days when an investor might have had to call their broker from the bar,” writes MagnifyMoney’s Kamaron McNair. “Younger investors admit to falling into this trap much more frequently than older traders, with 59% of Gen Zers admitting to drinking and trading, versus just 9% of baby boomers.”

A couple of points can be taken from this. One is services that make trading accessible through mobile phone apps and “free” of charge are certainly going to enable incrementally higher impulsive trading. Another point is the lack of sustained selloffs for over a decade modulates the perception of risk to a generation of investors.

Lower friction enables more activity and that is exactly what we have seen. Sometimes this is good, especially when frictional costs prevent important transactions. Beyond a certain point, however, too little friction causes problems – just as it is hard to steer a car on a sheet of ice. Thus far, most of the excessive activity has been bidding certain stocks up. It will be interesting to see what happens when that activity diminishes - or even reverses.

Goldman Puzzled As Options Price In Market Shock Similar To 1987 Crash, GFC And Covid Crisis

"high implied volatility, high skew, and high vol-of-vol are all signs of defensive option positioning"

“This means that, all else equal, while stocks may be levitating ever higher on ever lower volumes and ever shrinking breadth, the options market is preparing for a crash.”

Point one is there is some funky stuff going on in the options market and real information often finds its way into options prices before it is discounted in stock prices. Point two is there are a lot of crosscurrents in options markets as well, so it is hard to isolate a definitive cause and effect relationship. As a result, the characterization of the options market as “preparing for a crash” is likely an exaggeration. It is probably more accurate to say the options market is preparing for the increased probability of a selloff.

That may not sound like much of a warning, but it shouldn’t be taken lightly either. As extraordinary monetary policy has persisted for such a long time now, the number of financial metrics that aren’t tainted by those policies is vanishingly small. As such, we must make the most of whatever imperfect and garbled signals we do receive.

Labor

Employers grapple with fallout from the Great Resignation

“The Great Resignation is underway, and employers are grappling with the fallout. A whopping 65% of employees said they are looking for a new job, according to PwC's survey, conducted Aug. 2-6, of 1,007 employees and 752 executives in the U.S.”

“In PwC's latest U.S. Pulse Survey, nearly half of executives said they want to reduce their dependence on employees’ institutional knowledge.”

A couple of things strike me about this report. For one, 65% of employees looking for a new job is a huge percentage. This is backed up by the datapoint that “88% of executives said their company is experiencing higher turnover than normal”. This has all the makings of a fundamental shift in the workplace dynamics.

Another striking point is the employer response. With the potential to lose a significant part of the workforce, employers want to reduce their dependence on those employees. The irony is it is quite likely many employees are considering leaving in the first place because of underinvestment in their training and education. Reduce that even more, and there won’t be any reason at all for workers to take most jobs.

Are teen summer jobs back for good?

https://www.ft.com/content/b3ec25ee-bd06-4320-9b7b-d051c360b9c5

“A number of young people believed that they had their entire life to devote to work, so that engaging in relatively poorly paid employment, and diluting their focus on studying would be pointless, both in the short term (because of the nature of the work available) and also in the longer term (in terms of getting to university and getting a ‘graduate’ job).”

Many of us have lasting memories (good and bad) of summer jobs from high school. For a time it was a common thing to do to earn some spending money and maybe to save money for college. Today the calculation is different and summer jobs are increasingly viewed as counterproductive to the goal of attaining higher education.

This raises an interesting debate. Advocates for summer jobs argue they increase one’s appreciation for the value of money. They are also character building and develop real-life problem-solving skills. Finally, work in summer jobs creates exposure to people from a much broader set of racial and economic backgrounds which helps instill empathy for others. Opponents argue summer jobs dilute the focus of their study in return for virtually no benefit.

It seems to me the overarching desire to attain higher levels of education is undermining the perspective and empathy required to put those tools to good use. Look around at many of today’s tech leaders and it is clear they are not out to make the world a better place.

Geopolitics

The Promises of Politicians by Radigan Carter

https://www.radigancarter.com/dispatches/the-promises-of-politicians

“The ugly truth that most of us who spent a lot of time there on the ground understood is there was never a hard and fast line where the Taliban stopped and Afghan politicians started because it was all about money. Whenever the US started talking about drawing down more troops, another spectacular attack was allowed to happen to show the situation was still too perilous for the US to drawdown further. The amount of money that flowed into Afghanistan during the War on Terror cannot be understated.”

“Every time an American President said drawdown, everyone getting paid from the War on Terror saw that as a direct threat to their income and a return of Taliban rule. Spectacular attacks then happened to prevent this inevitability as long as possible. There was never a doubt in any of our minds the Taliban would take the country back when we left and the flow of dollars stopped. The strong always rule over the weak.”

Twenty years since 9/11 — a personal story ($)

https://www.ft.com/content/b520a7e1-b228-4820-876e-1fd8e9e03ff3

“Later that same day, September 12 [2001], my Pakistani colleague, Farhan Bokhari, and I found ourselves in the Rawalpindi home of Hamid Gul, former head of the ISI, Pakistan’s intelligence agency, who confidently informed us that Osama bin Laden was being framed for the attack on the Twin Towers. It had in fact been a Mossad operation, he said. Among Gul’s bogus bits of evidence was that none of the hundreds of Jewish people who worked at the Twin Towers had turned up for work that morning. Even now, it is hard to believe that he said that on the record to a western publication. It was my first of many bleak tutorials in the world view of the ISI.”

With so much news about Afghanistan spilling out the last couple of weeks, these two reports struck me as providing the best perspectives and lessons. The first is by Radigan Carter who describes his experience succinctly: “I spent 27 months in Afghanistan. There was never a grand strategy beyond staying alive and making money.” The second report is by Ed Luce who found himself in Pakistan the day after 9/11. Because both reporters had firsthand experiences, their accounts have a much different character than many of the popular headlines.

One of the things that strikes me is the perspective. Both accounts focus on the big picture; neither gets wrapped up in trivial details. Carter doesn’t talk about the “War on terror”, or national security, or nation building. The strategy was about making money. Luce doesn’t bemoan a brazen lie told straight to his face, but rather reflects on the “world view of the ISI” that comprehensively fails to appreciate the degree to which its credibility is undermined when it promotes demonstrably false theses.

Both accounts embody a somewhat melancholy tone that comes with the wisdom there are just some problems that cannot be solved.

Monetary policy

Go with the flows: Yet one more thought on ageing and inflation ($)

https://www.ft.com/content/07d895e0-80f2-4c00-bb53-49c2da87d7c9

“The effect of the inclusion of China and eastern Europe in the global work force thirty or forty years ago was to increase the supply of labour and lower its price per unit. With those changes came lower inflation expectations and a lower non-accelerating inflation rate of unemployment (Nairu), which is the lowest level of employment possible before inflation goes up. The ageing of the world population will have the opposite effect.”

“[Andrew] Smithers argues that the biggest risk from the demographic shift that G & P [Goodhart and Pradhan, authors of The Great Demographic Reversal] describe — which is, basically, a labour supply shock as the world ages — is that it increases the probability of a very bad central bank policy mistake.”

With all eyes on the Jackson Hole central bank conference this week, the big question is: What should monetary policy evolve to? Powell’s tendency seems to be to make small, incremental changes on a gradual path back to “normal”. But what is normal? The fact is world demographics are changing significantly and fairly quickly. If normal is healthy prepandemic supplies of labor, gradual reversion may be ok. If normal is a supply shock with significantly less labor, the Fed is already way behind the curve. As a result, there is a good chance the Fed is moving too slowly and to the wrong goal. Why do I keep hearing the words “subprime is contained” in the back of my head?

Lessons for investment analysis

The Dividend Futures Disaster Revisited: Anatomy of a Very Bad Trade ($)

https://diff.substack.com/p/the-dividend-futures-disaster-revisited

“Looking back, the biggest mistake I made was the sunk cost fallacy. Normally, this refers to a more purely financial decision: you bought at $10, and now it's at $9, so you're going to hold on until you break even. (And then it goes to $2.) But I wasn't trying to break even in monetary terms, I was trying to avoid having wasted my time. Putting a lot of effort into a model for a trade that will work about 98% of the time is risky in part because the other 2% of the time, you'll feel bad for throwing away all your hard work.”

This is such a great point it should be carved in stone for any investment analyst. The sunk cost fallacy entails costs in both money and time. Analysts at investment firms get paid to generate ideas that get implemented. If those ideas don’t get implemented, their careers don’t go anywhere. Similarly, do-it-yourself investors often have only limited time to devote to investment projects. When a lot of time is spent on a project, there is a compulsion to do something regardless of its merits.

The real problem boils down to the disproportionate emphasis placed on adding investments that will outperform as opposed to avoiding investments that will underperform. This is where it can really pay to have multiple competing hypotheses, to play devil’s advocate, and to do a premortem analysis. All of these activities require even more effort, however, and at the same time increase the chances the original investment idea will be rejected. As a result, these straightforward analytical exercises are performed far less frequently than they should be.

Landscape for investing

Daily Briefing: Chinese Tech Continues to Get Battered and Eviction Moratorium Remains

“So, I would broadly just put it into the category of when you see this extraordinary 45-degree line, particularly post-March marching up where the market just behaves with this incredibly high Sharpe ratio type dynamic. The explanation for that is the decay of option positions and dealers basically being given the luxury of every single day slowly hedging out a decaying option position.”

“There's really no fundamental information that flows through in that setting. And I think that's again one of the big challenges that people have because we're all looking at the markets and say, hey, wait a second, the S&P is up 18% for the year and yet the economic surprise index is hitting decade lows. Consumer sentiment is falling apart. How can we marry these two up? The answer is very simple. As myself and others have highlighted, you now have a market that is largely dominated by technical factors and market structure. It's just not that much information.”

In the space of 41 minutes, Mike Green manages to provide a lucid and understandable synopsis of all the critical trends in the market. Arguably, the most important one is the dissociation of market movements from economic and financial information. “S&P is up 18% for the year and yet the economic surprise index is hitting decade lows” and the same time “consumer sentiment is falling apart”. How does this happen?

The answer is simple: technical factors and market structure. In other words, money keeps flowing into target date funds, and index funds, and into stock buybacks. This happens with virtually complete disregard for fundamentals and continues to push prices up.

Similar dynamics were addressed in a piece in the Economist to which I referred last week. The basic idea is when money flows into stocks, it has a disproportionate impact on stock prices. The authors refer to the idea as the “inelastic markets hypothesis”.

Interestingly, Robert Armstrong from the Financial Times highlighted the same Economist article and found the subject compelling enough to write a two-part analysis here ($) and here ($). In the second, he talked to one of the authors of the study to vet out the mechanics of the thesis. Essentially, the bottom line is when excess money flows to funds with rigid mandates, something has to give. If supply doesn’t increase substantially, then prices have to go up.

The result is counterintuitive, contradicts conventional finance theory, and is hugely important for investors to understand: With this market structure, stock prices do not reflect discounted cash flows, i.e., underlying economic value. Instead, prices simply represent the supply and demand for stocks. For example, when funds flow to stock funds, one of the main sources of supply is balanced funds. The only way for a balanced fund to remain in balance if it sells stock, however, is if it only sells stock at a high enough price to offset the sales. Voila, higher prices.

Implications for investment strategy

Probably the most important implication of inelastic markets is stock prices convey exceptionally little information content. Prices in this environment march up in a very mechanical way. Investors who chase those prices are like the blind leading the blind; they make lemmings look cerebral.

This isn’t to say there aren’t still a lot of voices promulgating outdated theories. Plenty of academics still adhere to the efficient markets hypothesis. Plenty of tech advocates claim cheap and accessible information is massively increasing the efficiency of markets. These ideas are nice sounding, but wrong.

Another important implication is the way the narratives describing how the market works are changing. A couple of years ago, Mike Green and one or two other people were making their theories about market structure known in venues such as Real Vision and other distinctly non-traditional outlets for financial information. Now the ideas are coming through the Economist and Financial Times which are decidedly more mainstream.

As the narrative becomes more broadly recognized and accepted, it is reasonable to expect more investors to act according to that knowledge. Specifically, this is likely to include lower discretionary allocations to stocks as downside risk becomes increasingly elevated.

Principles for Areté’s Observations

All the research I reference is curated in the sense that it comes from what I consider to be reliable sources and to provide meaningful contributions to understanding what is going on. The goal here is to figure things out, not to advocate.

One objective is to simply share some of the interesting tidbits of information that I come across every day from reading and doing research. Many of these do not make big headlines individually, but often shed light on something important.

One of the big problems with investing is that most investment theses are one-sided. This creates a number of problems for investors trying to make good decisions. Whenever there are multiple sides to an issue, I try to present each side with its pros and cons.

Because most investment theses tend to be one-sided, it can be very difficult to determine which is the better argument. Each may be plausible, and even entirely correct, but still have a fatal flaw or miss a higher point. For important debates, I express my opinion as to which side I believe has the stronger case, and why.

With the high volume of investment-related information available, the bigger issue is not acquiring information, but being able to make sense of all of it and keep it in perspective. As a result, I describe news stories in the context of bodies of financial knowledge, my studies of financial history, and over thirty years of investment experience.

Note on references

The links provided above refer to several sources that are free but also refer to sources that are behind paywalls. All of these are designed to help you corroborate and investigate on your own. For the paywall sites, it is fair to assume that I subscribe because I derive a great deal of value from the subscription.

Comments

One goal of this letter is to provide fairly dense information content – so you don’t waste your time filtering through a lot of fluffy verbiage. A consequence of that decision, however, is sometimes things may not be as understandable as they could be. If you have follow-up questions or comments, please use the comment utility, or send me an email at drobertson@areteam.com.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.