Observations by David Robertson 9/10/21

Welcome back!

I hope everyone had a nice long Labor Day weekend. Now it’s back to work and things are shaping up for an eventful fall.

Let me know if you have comments. You can reach me at drobertson@areteam.com.

Market observations

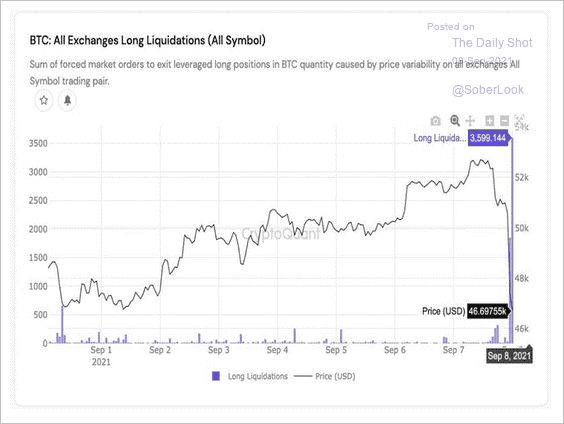

Stocks had a feeble start to the holiday-shortened week which cast an eerie pall over the market. The real fireworks came from cryptocurrencies. Bitcoin dropped Tuesday morning and took a bigger hit in the afternoon. The graph shows the liquidation of long positions due to margin calls was the nudge that caused the slide to advance in the afternoon.

The US dollar was also strong on Tuesday and Wednesday, but then weakened on Thursday. Was this just the other side of crypto weakness? Was it a function of deteriorating credit conditions in China over the weekend? Or was it just random noise? Regardless, the dollar is worth watching because it is one of the few signals that still contains a fair amount of information content.

Entitlements

The Coming Insolvency of Social Security ($)

https://morning.thedispatch.com/p/the-morning-dispatch-the-looming

“An annual government report published earlier this week estimated that, due to the COVID-19 pandemic, Social Security’s funding will run out in 2033—one year earlier than previously projected. Medicare’s life expectancy remained unchanged from last year, when it was forecast to be depleted by 2026.”

“People fixate on the idea of a date,” Michael Tanner, senior fellow at the Cato Institute, told The Dispatch. “What really counts is cash flow. Cash flow to [the programs] is negative and growing worse—not some magic date at which the trust fund has a dollar or doesn’t have a dollar. The trust fund is just an accounting measure of how much the federal government owes Social Security.”

The clock is ticking and has started ticking even faster. The point on cash flow is right. The way the depletion of the funds will be experienced is negative cash flows will require incrementally higher debt issuance to fund the programs on a regular basis. In other words, debt is going to crank up like a hockey stick. You ain’t seen nothing yet.

It would be nice to think reasonable minds could sit down, recognize the mathematical implications, and figure out a way to prevent a disaster. Alas, one of the few things both parties agree on is that “entitlement reform is the third rail in American politics”. As a result, the most likely scenario is these programs will remain in place until they become financially ruinous and it is too late to extricate from them without significant harm.

I have written about this issue several times in the past. Older generations feel strongly they have the “right” to their Social Security and Medicare and younger generations seem somewhat resigned to the notion they are going to get cheated out of their fair share. All this means is things will have to get really bad before there is enough political impetus to change anything. I wish it were otherwise, but it is hard to see how.

Economy

Depressed economic surprises need more "juice"?, Sep 06 2021 at 06:00 ($)

https://themarketear.com/premium

This graph highlights a couple of really important points about the economy. For one, the Fed’s balance sheet certainly has the capacity to dramatically change the trajectory of economic growth. However, that resource comes with two important caveats. One is the effect is only temporary; it rapidly wears off.

The other is the effectiveness of balance sheet expansion in boosting the economy is contingent upon the fiscal spending it underwrites. Even more specifically, effectiveness is contingent upon the type of fiscal spending. Spending that quickly gets into the hands of consumers who are likely to spend does have a positive, but short-term effect. With stimulus checks a thing of the past and pandemic benefits running out, so too is the economic boost from the expansion of the Fed’s balance sheet rapidly diminishing.

Credit

Paper Tiger, Almost Daily Grant’s, Wednesday, September 8, 2021

https://www.grantspub.com/resources/commentary.cfm

“Then, too, keeping up with the currently-bounding rate of inflation is proving virtually impossible even within the speculative corner of the debt market. As Deutsche Bank strategist Jim Reid points out today, some 85% of the high-yield realm currently fetches a negative real yield. Prior to this year, no more than 10% of the index had ever dipped below the measured rate of inflation going back to at least 1996.”

As the Fed has successfully pushed investors further and further out on the risk curve, what lays in store now that even “high yield” doesn’t produce returns higher than inflation? The prognosis isn’t good. Reid concludes the difference between current yields and historical norms “pretty much ensures that historical returns are absolutely no template for the future.” Copy that. In fact, copy that for virtually all financial assets.

China

"What China's Dual Circulation Policy & Resurgent Party Leadership Means For Investors" ($)

https://www.eri-c.com/news/782

Stewart Patterson of Capital Dialectics is an experienced and insightful analyst on China, and he provides a stark wakeup call for investors in this presentation. He frames recent policy changes in the historical context of “profound turning points in strategy”.

From a top-down perspective, one of the big changes he observes is that of “Ideology replacing pragmatism”. For many years China was tolerant of capitalism and entrepreneurialism insofar as they also served state goals. No longer. Relatedly, “Economic growth is no longer key objective”. As a result, China’s growth trajectory is likely to take on a very different look in terms of both scale and nature. For one, growth will be much lower. For another, investment-led growth will be replaced by growth in strategic areas such as technology.

While his lessons for investors are far-reaching, the most direct one is a warning. As he puts it, “China is not capital constrained - they don’t need your money”. As a result, it is hard to justify being there if you don’t have to be.

The Chinese control revolution: the Maoist echoes of Xi’s power play ($)

https://www.ft.com/content/bacf9b6a-326b-4aa9-a8f6-2456921e61ec

“A monumental change is taking place in China. The economic, financial, cultural and political spheres are undergoing a profound revolution,” Li Guangman, the pen name of a prominent leftist commentator, wrote in a commentary that captured the zeitgeist. “It marks a return [of power] from Capitalist cliques to the people . . .”

The FT is also recognizing the magnitude of the political pivot in China in this first of a two-part series on the “control revolution”. This creates a very interesting real-time opportunity to compare and contrast different political systems since the US and China are contending with many of the same problems – such as aging demographics, excessive debt, and high levels of inequality. How successful will each be in dealing with adversity?

The US has a better starting point with greater wealth and resources and more robust infrastructure, but China has a clearer strategy on what it wants to accomplish and how to move forward. It is easy to pit the differences in ideological and moralistic terms and some of that is fair. I suspect when all is said and done, beliefs in American “transparency” and “rule of law” and “land of opportunity” will come out at least somewhat bruised. On the other hand, I think investors will do well to heed the words “monumental change” and “profound revolution” in China.

Japan

Japan Bulls Pray for a Helicopter Lift After Suga’s Demise ($)

“Since New Year’s Eve 1989, when Tokyo peaked at a point when the total market cap of corporate Japan comfortably exceeded that of corporate America, the economy has been in a disinflationary slump and its stock market has massively underperformed the U.S. If we take the Topix’s performance relative to the S&P 500, in common currency terms, and start on the last day of 1989, this is the picture of persistently painful performance that emerges:”

John Authers provides some good background on Japan and its struggles over the years. After so many people have been burned so many times, it’s hard to seriously entertain the idea of investing in Japan. Perhaps that is exactly the type of washed-out situation that presents a value opportunity, however. Further, Japan’s epic underperformance started from the top of an epic bubble. What if the tables are turning? In a world of precious few cheap stocks or sectors, Japan is interesting.

Cybersecurity

Inside the response to the massive Russian SolarWinds hack

“In the book's [‘Tools and Weapons’] new sections, Smith writes that SolarWinds represented more than cyber-espionage as usual, but wasn't a full-on act of cyber-war, either. Rather, Smith writes, it was a ‘moment of reckoning’ that showed just how much unfinished work remains to be done to set global rules and norms for how technology can be used by nation-states to attack one another.”

“The U.S. government itself fails to sufficiently share data on cybersecurity threats, according to Smith: ‘Repeatedly in late 2020 we found people in federal agencies asking us about information in other parts of the government, because it was easier to get it from us than directly from other federal employees’.”

One takeaway is cybersecurity is an ongoing threat for which the severity level seems to keep getting dialed higher. Another takeaway is the observation of how little has actually changed since 9/11. Despite having a great deal of exciting technology, there is still a big gap between technological capabilities and important problems that need to be solved.

Smith shares his assessment: "It's impossible to avoid the grave conclusion that the sharing of cybersecurity threat intelligence today is even more challenged than it was for terrorist threats before 9/11”.

Commodities

Tightening into slowing momentum?, Sep 05 2021 at 19:30 ($)

https://themarketear.com/premium

The graph above shows the strong relationship between credit and commodity performance. This is especially timely as the strong performance over the last year makes it incrementally harder to add to commodities for their longer-term inflation protection. As I mentioned last week:

“I am watching and waiting for a selloff in these stocks to provide a more attractive entry point. I still like the longer-term supply dynamics, but the potential for near-term demand weakness needs to get discounted first.”

So far, it looks like the opportunity is unfolding. We’ll see.

Cryptocurrencies

In other cryptocurrency news, Zerohedge reported, “In response to the SEC's legal threat, Coinbase CEO Brian Armstrong lashed out at the agency on Twitter, complaining that his company had attempted to do the right thing, but that the SEC has failed to be transparent about its crypto policies, and is instead ‘engaging in intimidation tactics behind closed doors’.”

This strikes me as both naïve and immature and does nothing to enhance my respect for cryptocurrencies when coming from the CEO of one of the industry’s most prominent companies. It is incredibly naïve to expect “transparency about its crypto policies”. Regulators do not get paid to pioneer new technologies nor to explore the implications for regulation.

Regulators are notoriously backward-looking because regulations only get written after something has broken. Registered investment advisors operated for years without any guidance in regard to social media and there are still plenty of gray areas. We may not like it, but that’s the way things are and it defines the parameters under which we must operate. To complain about it is just being a crybaby.

The response also comes across as immature. For one, it makes him look stupid to anyone who has ever run a company in a regulated industry. For another, it is generally not a good idea to get into fights with people who can put you out of business. Armstrong did a poor job of picking his battles.

Or, as Axios reports: "’The SEC doesn't have the obligation (or the resources) to issue guidance about things that should be obvious to a baby securities lawyer,’ tweets Georgetown Law professor Adam Levitin. ‘It's really astounding that Coinbase thinks it's entitled to anything more’.”

Implications for investment strategy

One of the most important challenges for investors is inflation and as a result, it is a topic I have featured repeatedly in “Observations” as well as in blog posts. Because the topic is a big one, I thought it would make sense to tie a number of ideas together from past writings.

A good place to start is with the special report on inflation I published on Substack in December 2020. A lot of useful background is provided in that report, not least of which is the important role of expectations. Because expectations are a function of social beliefs about inflation potential, expectations take time to shift, but when shifts occur, they can be very sudden and nonlinear.

In the “Observations” from 4/30/21, I discussed a report by Epsilon Theory that highlighted importance of volatility of prices:

“Great points by Rusty Guinn at Epsilon Theory. The main one is that the volatility of prices is also an important factor, not just the direction. Any business or consumer making decisions must evaluate not just direction of prices, but also timing. Being too early or too late to a big pricing move can be more destructive than being wrong on the direction of the move.“

Finally, I wrote a blog post in April 2021 that highlighted the false dichotomy of choosing between inflation and deflation:

“While the tendency to make directional bets is understandable, the increasing ambiguity around the inflation issue suggests a portfolio approach is more appropriate. In a sense, constructing a portfolio designed to weather very different possible future environments isn’t an especially innovative proposition.

What it is, however, is a break from the past. It is a break from the 60/40 mindset, and it is a break from almost everything that has defined the investment landscape over the last forty years. It is also a break from the conditions that have guided the fortunes of a couple of generations of business leaders, money managers, and financial advisors.”

While none of these observations captures the totality of dealing with inflation, each provides incremental insight. One point is inflation is a process and it is messy. As a result, there is no “plug and play” answer to it. Relatedly, managing through changing inflation requires a somewhat active approach. The last thing you want is to be handcuffed by a “moderate scope for variation in response to changing market conditions” which I discussed in a recent blog post.

Probably as much as anything, dealing with inflation will require a different mindset. After several years of being able to sit peacefully on the sidelines just watching stocks go up, the prospect for inflation is going to require more active participation by investors. As with any endeavor, getting into the game and being effective is going to require preparation and a willingness to take on a very different role.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.