Observations by David Robertson, 5/3/24

After hitting a peak at the end of the first quarter, the ride for stocks has been a lot bumpier. Let’s take a look.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Michael Taylor identified one of the biggest problems for the market on X: “Too many big mo-names have/are breaking”. Among those names are NFLX, TSLA, AAPL, GE, CAT, MCD, SBUX and SMCI. Nor are these just a random set of names. As Taylor describes, “This is where retail lives.”

Another area where momentum has been breaking down is Bitcoin. As themarketear.com ($) reported on Wednesday, “Yesterday BTC broke below the lower part of the range (62k) that has been in place since March. The sell off continues today and we have BTC crushing the 100 day moving average, trading at 57.4k as of writing. We haven't seen the crypto below the 100 day since October last year.”

After its big run up in the first two and half months of the year, it’s been nothing but a slow burn for BTC since.

Finally, the Japanese yen made headlines a couple of times this week. Early Monday morning the yen suddenly swung weaker and then suddenly swung stronger against the US dollar. It drifted weaker through Wednesday when in the evening it suddenly swung stronger again.

While Japanese authorities are not commenting on the moves, they have all the earmarks of intervention. As much as anything, alleged interventions illustrate the bad set of choices Japan faces: It can either spend money on a mainly futile effort to keep the yen from depreciating too far too fast, or it can keep raising rates and suffocate its economy.

Japan does have levers to pull so this isn’t a crisis, per se, but it is a good marker that time is running out. The headline, “Japan's ruling party considers tax breaks to spur yen repatriation, officials say”, that PauloMacro ($) reported indicates monetary authorities are taking the next steps. Those next steps will most likely involve the repatriation of capital from markets outside of Japan back to the home country. When that happens, capital will get more expensive in those other countries. It’s happening.

Politics

The Spiritual Unspooling of America: A Case for a Political Realignment

https://newrepublic.com/article/177435/chris-murphy-case-political-realignment-economics

It strikes me that in both urban and rural landscapes, and across class, gender, and racial identities, we are all feeling a set of common anxieties. These include: a loss of control over economic and family life; an acute loneliness and disconnection from community; a frustration with the pace and nature of technological change; and an exhaustion with suffocating consumerism.

For much of our country’s history, we did a decent job at balancing profitmaking and citizenship. Many sectors of the American economy, like health care and education, were deemed so vital to our sense of collective moral mission that they were kept out of for-profit control. But today, the idea of forsaking profit for the common good is a laughable anachronism.

But our decision to base our political groupings on these issues masks a potentially massive, hidden alignment between Americans on both the right and left—an alignment that could potentially address the set of spiritual problems I have outlined here.

This effort by Senator Chris Murphy (CT) is interesting for several reasons. For one, I think he is right in diagnosing “common anxieties”. They certainly resonate with me and I’m sure they do with a lot of other people as well.

This leads to another interesting aspect of the article: The effort to reach out to both sides of the political spectrum sounds an awful lot like the Neil Howe’s idea of regeneracy (mentioned here, here, and here, among others) which happens at the end of a Fourth Turning. As I described before:

The major parties are getting forced apart from both sides: The schisms provide the “stick” for followers to change affiliation and policies that garner bipartisan support (such as pro-labor) provide the “carrot” for them to form new ones.

Finally, while the reconfiguration of political affiliation happens naturally at the end of a Fourth Turning, it sounds a lot like Murphy is identifying an opportunity and running with it. In the context of what he describes as the “coming realignment” of “our long stable, and probably stale, two-party system”, his efforts smack of political entrepreneurialism.

There is no doubt there is a large unmet need for less partisan and more center of the road policymaking as well as more of a focus on things that matter most to people. There is also no doubt that standard messages from both Democrats and Republicans are old and tired and out of sync with growing chunks of the population. As a result, Murphy’s effort marks an important milestone in the process of regeneracy.

Geopolitics

Beijing gives Blinken cold shoulder, extends warm welcome to Musk

Gzero Daily, April 29, 2024

Last week, US Secretary of State Antony Blinken made a high-profile visit to China, marked by terse talk and some tough symbols. Two days ahead of Blinken’s arrival, China launched a submarine-based ballistic missile test, and as he departed, the Chinese air force flew jets over the Taiwan Strait. Beijing was not amused by the US Congress passing a supplemental spending bill last week, including billions in military assistance to Taipei.

This is another good characterization of the relationship between the US and China. Mainly, it looks like two young siblings in the back seat of the family car who can’t stop poking at and provoking one another. Nonetheless, there they are, right next to each other.

It begs the question of what the nature of the tensions between the US and China even is. While I have written about the seriousness of this geopolitical challenge in recent issues, I started reading Paul Tucker’s book, Global Discord, for more insight. Fortunately, he brings it.

Part of the problem in analyzing this new challenge, for those of us who are not scholars in history or geopolitics, is context. Most post-war international institutions and norms were developed by the West and for the West. Despite “differences and aggravations,” the guidelines for international relations still “drew on shared histories and cultures”.

So, that has changed. Obviously, the US and China have very little shared history or culture. As a result, the question that needs to get answered is: “How can the West and other constitutional democracies maintain their liberal traditions in the face of interdependencies with rising (or revived) authoritarian states?”

Simply by asking the right question, Tucker frames the challenge in a much more useful way. For one, this is no easy yes/no type of question. Rather, finding the answer is likely to be a process that plays out over a long period of time ((i.e., several decades). As a result, it’s likely to be a grinding “work in progress” and it’s not likely to reach any definitive conclusion for the foreseeable future.

As a result, the pattern of high points and low points and of mixed messages is likely to persist. What is also likely to persist is the potential for tensions to escalate if domestic challenges become so severe that a distraction is needed.

Monetary policy

After a great deal of anticipation, conspiracy theories, and wild speculation, the Treasury’s Quarterly Refunding Announcement (QRA) forecast came in … wait for it … unchanged. Yup, the forecast for issuance of coupons (longer-dated Treasuries) was exactly what it was last quarter.

As anticlimactic as that was, there were still things to be learned from the event. One of the more prominent variables was the degree to which Secretary Yellen might tweak coupon issuance in an effort to ease longer-term yields. This was based on her decision last fall to reduce coupon issuance just after 10-year yields had bumped 5%. Doing so clearly created the perception that she politicized policy and that was probably at least part of the motivation. Nonetheless, the lesson learned this time around is the issuance pattern has not become as politicized as some had feared.

Another nugget was the indication Treasury is in something of a holding pattern right now with coupon issuance. Both this quarter and last the QRA came with this statement: “Based on current projected borrowing needs, Treasury does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters.”

The statement is meaningful because it conflicts with the longer-term goal of limiting bills to about 20% of outstanding debt. Since bills are over that limit today, it begs the question of what the longer-term plan is. Is this short-term overage simply part of an effort to deplete the Reverse Repo Program (RRP)? Perhaps. Is it early days in the unfortunate devolution to emerging market finance? Less likely in my opinion, but certainly possible. Is it the least crappy option available that will be reversed instantaneously when the s*&t hits the fan? Also possible.

What we know for now is coupon supply is going to continue to pressure long-term yields higher, all else equal. However, we also know Treasury can ease liquidity pressures by issuing more T-bills - which it plans to do. In addition, per the FOMC press release, the Fed plans to cut back on its QT (Quantitative Tightening) program beginning in June. That will also ease pressure on the long end. Net/net, it looks like the Fed/Treasury team will try their darnedest to stave off significant increases in longer-term rates for the foreseeable future, which probably means until the election in November.

As to the Fed, the FOMC meeting really just confirmed what everyone already knew: The Fed is in no position to lower rates, but it doesn’t want to raise them either. More interesting was the market reaction. In the early minutes of the meeting the S&P 500 shot up about 1% - even though there was no content in the press release or comments afterward that merited such a move. By the time the press conference was over and it was clear there would be no dovish remarks to goose the market, it quickly sold off to where it had started.

Maybe I’m old fashioned, but if the largest and most liquid stock market in the world can move 1% purely on a bet that the Fed might say something dovish, that doesn’t speak well to the health of the investment landscape - or the information content of market prices.

Investment landscape

Stagflation Loses Showdown With Magnificent Seven ($)

But it’s the Magnificent Seven that matter. Bloomberg’s earnings expectation service shows that blended forecast and actual first quarter earnings are 58.1% higher than at their nadir in November 2022. Meanwhile, the 493 companies in Bloomberg’s Large-Cap 500 Excluding Magnificent Seven index are on course to come in 8.4% below the estimate from that same date. So if you’re wondering why market watchers seem obsessed by just those seven stocks, that would be one reason:

While it’s not a surprise that the Magnificent 7 stocks have been driving the S&P 500 by outperforming the others, this chart of earnings trajectories illustrates just how dramatic the performance differential has been.

Looking forward, it is certainly possible the Magnificent 7 continue on their roll, but the contrarian in me has a hard time believing it is likely. For one, an important part of the declines for industrial and consumer businesses has been declines in inventory. Given that personal consumption has maintained a healthy pace, and that inventories have been depleting, it is reasonable to expect inventories need to get rebuilt. If so, that would provide a healthy bump to companies that make things.

On the other side of the equation, most of the Magnificent 7 companies are facing serious charges from the FTC and/or other regulatory organizations. Because these tend to be slow-moving and haven’t been very consequential in recent years, it has been easy to dismiss them as background noise.

To do so, however, misses a more aggressive/less passive approach to policing uncompetitive behavior by the FTC. It also misses an increasingly popular and bipartisan support for efforts to push back on corporate policies that hurt consumers and hurt workers. My sense is we are still in the early innings of increasing headwinds for the largest global companies.

In addition, since the Magnificent 7 are global companies, they are also subject to global risks. Nowhere can that be seen more clearly than in China. As geopolitical tensions have heated up, so too have trade restrictions and home-country biases. While China used to be the great hope for growth among otherwise stagnating global businesses, it is now at least as much a risk for stranded capital.

A recent blog post by Calcbench highlights the trend: “Large U.S. businesses saw their revenue from China fall 4.7 percent in 2023, according to an analysis of their geographic segment disclosures.” Among the ten companies reporting the most China revenue last year, “Seven of them saw revenue declines from 2022 to 2023,” and the aggregate decline was 3.6%.

If you are looking for reasons why leadership in the S&P 500 might change, you found them.

Investment advisory landscape

Like so many other things, the merits and de-merits of the investment industry are often reduced to over-simplified narratives that strike a chord, but miss important points. These two posts [here] and [here] by Ptuomov do a wonderful job of excising the important points from the narrative.

An opinion: Institutional asset managers, in contrast to retail mutual fund managers, deliver alpha to the clients net of fees and trading costs. The alpha is small but positive in aggregate. I speculate that retail mutual funds and direct retail investors are the primary source of this alpha. Can't post empirical proof but I believe this to be true.

I believe that asset managers prefer clients that understand the process, have outside information about the profitability of the process, and that put relatively little weight on the past track record. In my experience (from both sides of these relationship), the manager is happy to share his/her alpha with a client that isn't redeeming with the hot money after a period of negative alpha when the opportunities are often the greatest. My conclusion is that there is a second scarce skill in active management that can also plausibly get paid in the long run.

The first highlights the fact that there is a business difference between retail mutual funds and institutional asset managers. Retail funds have many more clients, relatively high marketing and distribution costs, and tend to have lots of customers who do the worst things at the worst times - like selling out at the bottom of a market downturn. This creates a significant overhead of costs, all of which are NOT investment-related. The dark little secret of the retail mutual funds business is that it is more of a marketing business than an investment one.

Institutional management, on the other hand, tends to be more of an investment business, but with caveats. As suggested by the second quote, in order for investors to realize alpha from a skillful manager, there needs to be some kind of mutual recognition of the symbiotic nature of the relationship: A skillful manager has the best chance to deliver alpha if he/she can rely on capital staying there through the market’s ups and downs. In other words, the fickle, performance-chasing behavior of many investors has negative externalities for both the manager and other co-investors.

One point is these are nice insights into the investment business. Another point is they are also major reasons why I founded Areté. The fact of the matter is investors do not have a very fair chance to do well in most retail-oriented investment products. I am trying to change that, and there are others too. Part of the deal for having a better chance at doing well, however, is being patient with one’s invested capital. The more investors understand these market dynamics, the better chance they have of reaping the market’s rewards.

Implications

At a very high level, the challenge most developed countries face is they have spent far more than they have earned. As a result, public policy has centered on forestalling the consequences of those past (and present) transgressions. This means there will be a serious reckoning, but we don’t know when.

Further, because policymakers are basically out of good options, they are getting progressively more desperate. That makes their behavior, and the market’s reaction to it, less predictable.

In sum, the investment environment is comprised of a pretty toxic mix of unsustainable growth, unrealistic expectations, and unpredictable policy intrusions, all packaged with a limited shelf life. Needless to say, it’s getting a lot trickier for investors to navigate.

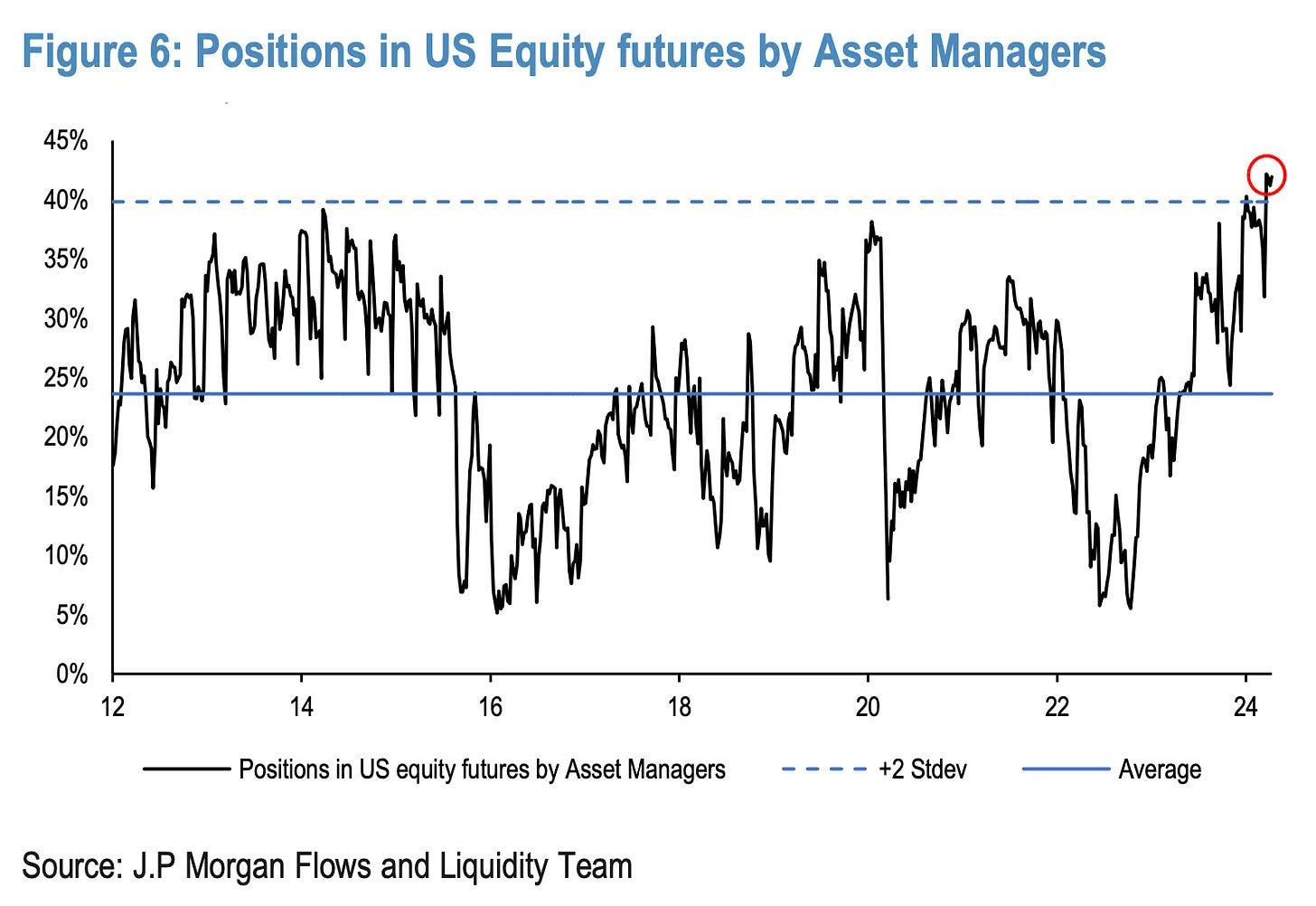

At the same time, however, asset managers are incredibly bullish on stocks. Here is a friendly reminder from Jesse Felder that positioning in US equity futures is higher than it’s ever been in the last twelve years:

And here is a friendly reminder from John Hussman as to the outcomes of such extreme positioning based on recent experiences:

S&P 500 retreats from peaks in futures positioning

-13% from Dec 2014 - Feb 2016

-18% from Jan 2018 - Dec 2018

-34% from Feb 2020 - Mar 2020

-25% from Jan 2022 - Oct 2022

Not a forecast, not an investment strategy, just FYI

As much as anything, this probably demonstrates the difference between short-term and long-term goals. Long-term investors can see the risks and slow down or step aside. Short-term investors are speeding down the highway and can’t see all the brake lights right in front of them.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.