Observations by David Robertson, 8/18/23

It was a fairly quiet week in terms of news and a quietly down week for the market.

As always, if you want to follow up on anything in more detail, just let me know at drobertson@areteam.com.

Market observations

Perhaps the most important chart in all of finance right now is that of yields on 10-year US Treasury bonds. For one, they are the foundation for the valuation of virtually all risk assets. For another, they have been breaching important thresholds which spells trouble for those valuations.

Back in March I identified the possibility “that long rates can go much higher yet”. I also noted that 10-year rates can break over 5% based on the normalization of term premia alone. Those warnings were absolutely warranted. If there is more room to run in long-term rates, and I strongly suspect there is, it will only be a matter of time before the impact gets felt.

Also notable among the list of important charts are the currencies of China and Japan. Both have been extremely weak, both countries have serious issues to deal with, and either one can cast a chill wind over global asset markets. Is this the time for China to finally devalue the yuan? Will Japan finally break from Yield Curve Control (YCC) and allow rates to increase? These will be extremely important variables to monitor.

Finally, another observation worth noting is a change in the trading of the S&P 500. A pattern of opening at or near the high of the day and then fading through most of the day to finish at or near the day’s low has emerged. This has not been so much a consistent pattern as an increasingly regular one. It could be due to a migration from Buy The Dip (BTD) behavior to Sell The Rip (STR) behavior. And/or, it could be some chunks of money are slinking vewwy vewwy qwietly towards the exit.

China

Chartbook: Whither China? Part I - Regime impasse?

https://adamtooze.substack.com/p/whither-china-part-i-regime-impasse

Adam Posen and Li Yuan talk in general terms about “confidence” and credibility, but their narratives and evidence actually pertain to three different groups. Households are the center of the Posen story … Secondly, there are the corporate chieftains who not only toe the line, but whose businesses also have really big investment budgets that are easy for the regime to inspect. And then, the third group, the nameless group of “business owners” who are Li Yuan’s interlocutors.

Adam Tooze does a nice job in this piece of exposing some useful insights about China, and also revealing some pitfalls in the journalistic coverage of China. For example, the Li Yuan story he highlights reveals a great deal of disenchantment with Xi Jinping’s policies amongst business leaders. The Posen story highlights a new, heightened sense of insecurity amongst consumers resulting from the capricious and impactful Zero-Covid lockdown policies.

One point to make is China is a big country and care should be taken to avoid making overly simple or overly general assessments. Another point is there are a lot of different groups of economic participants that have different perspectives. While insights into those groups can be informative, they should not be widely generalized.

Tooze reserves his strongest criticism for the broader generalization both authors make from reported misgivings to a thesis that “the regime’s authoritarianism” is the main cause of such problems. For example, Posen states explicitly, “The autocrat’s Achilles’ heel is an inherent lack of credible self-restraint.”

While such a statement by itself is not necessarily wrong, it is inappropriate in the context of the main story for two reasons. First, it is not necessarily related to the main story of heightened uncertainty among Chinese consumers. Second, in making the statement about autocracy, Posen goes beyond reporting on news to telling us how to think about that news. It’s hard enough to get reliable insight into what’s happening in China; we don’t need the waters further muddied by reporters imposing their opinions on us.

Social dynamics

Hey, America, Grow Up! ($)

https://www.nytimes.com/2023/08/10/opinion/trauma-mental-health-culture-war.html

In earlier cultural epochs, many people derived their self-worth from their relationship with God, or from their ability to be a winner in the commercial marketplace. But in a therapeutic culture people’s sense of self-worth depends on their subjective feelings about themselves. Do I feel good about myself? Do I like me?

The instability of the self has created an immature public culture — impulsive, dramatic, erratic and cruel. In institution after institution, from churches to schools to nonprofits, the least mature voices dominate and hurl accusations, while the most mature lie low, trying to get through the day.

Amidst an environment frequently spotted with bizarre and unseemly behavior, I often find myself wondering, “Why on earth would anybody do something like that?” David Brooks provides an interesting and helpful answer: Because our “therapeutic culture has create an “immature public culture” which is “impulsive, dramatic, erratic and cruel”. You don’t have to spend a lot of time on social media to see some truth in this. In other words, much of the public screaming and yelling we all encounter is the product of an epidemic of immaturity.

This is helpful in the sense that a lot of bizarre behavior has nothing to do with us and rarely says anything useful about the circumstances. Beyond that, though, Brooks offers only generalities:

If we’re going to build a culture in which it is easier to be mature, we’re going to have to throw off some of the tenets of the therapeutic culture. Maturity, now as ever, is understanding that you’re not the center of the universe. The world isn’t a giant story about me.

The downside of this assessment is there is little end in immediate sight of the proliferation of immature public expression. It permeates our politics and virtually all of our public interactions.

There is hope, however. For one, widespread self-absorption is a luxury; it is a function of circumstances so benign as to obviate the need to combine forces and work together. Perhaps a touch of real adversity might be enough to crack the shell of the “giant story about me” for many people.

For another, inasmuch as the world is riddled by the cries of the immature, the “most mature lie low”. That doesn’t mean they don’t exist; it just means they are quiet right now. In the event of greater adversity, however, maturity will again become a necessary and valuable contribution to society. When it does, we’ll start hearing a lot more from a more mature group of people.

Politics

This Twitter post by Mark Kahn resonated with me:

It's absolutely amazing how little social media chatter or even MSM coverage Sam Bankman-Fried having his bail revoked and being sent to jail is garnering. For some reason, all the air seems to have gone out of that story.

I agree. It seems pretty clear to me that Bankman-Fried is a first-class scumbag. He didn’t so much break rules as never really acknowledged rules applied to him at all. Not only did he run a Ponzi scheme, he broke laws and breached fiduciary duty not just repeatedly, but as a modus operandi. Once caught and confined to his parents home, he started tampering with witnesses. The guy just doesn’t stop.

So, what happened to the story? Why aren’t we hearing about one of the biggest financial scandals of all-time? Ben Hunt answers the question, and it all has to do with narratives:

It [the SBF story] doesn’t fit the worldview of the dominant narrative entrepreneurs on the red tribe (Biden DOJ is giving SBF a sweetheart deal) so it didn’t happen.

It doesn’t fit the worldview of the dominant narrative entrepreneurs on the blue tribe (SBF was our ally) so it didn’t happen.

This is important for a couple of reasons. One is that narratives are dominating our media and politics. Increasingly we are not just getting news, we are getting told how to think about a certain subject. Obviously, this is a huge part of the political landscape, but also certainly the economic one.

The proliferation of narratives is also important, however, for what is not said/reported. The SBF story is a perfect case in point. The fact we aren’t hearing about it does not speak to its relative newsworthiness. We aren’t hearing about it because it doesn’t fit neatly into either a Republican or Democrat narrative.

As a result, analysts must not only disentangle news stories from their narratives, but also must identify the newsworthy stories that aren’t being told because they don’t fit into convenient narratives.

Monetary policy

On the surface, little has been happening. It’s normally quiet late in the summer anyway and there is no FOMC meeting until September. FOMC minutes came out on Wednesday which revealed “most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy”, but that was hardly a big surprise. The only big thing on the calendar is the central bank shindig at Jackson Hole next week. As I mentioned in Observations from 7/28, a good case can be made that the Fed chair will avoid rocking the boat and just let things play out.

Beneath the surface, however, there is a lot more turmoil. The Chinese yuan is plunging again as deflationary pressures are building and real estate problems are metastasizing. The Japanese yen has also been especially weak, even in the face of strong growth and rising inflation. Stateside, longer-term US bond yields are hitting an inflection point beyond which would almost certainly roil asset markets. All said, there are plenty of potential catalysts for important monetary events.

As a result, it will be worth being on the lookout for any clues that may come out of the Jackson Hole gathering.

Public policy

I enjoy a good conspiracy theory as much as anyone, not least of which is because they often turn out to be true. Often, but not always. While conspiracy theorizing seems to be turning into a national pastime, especially in regard to public policy, sometimes there is no conspiracy at all. Sometimes people are just doing a job as best they can.

This appears to be the case with Treasury issuance. While Twitter is ablaze in theories about the degree to which Treasury is managing liquidity with ulterior motives, a quick perusal of a Treasury Borrowing Advisory Committee (TBAC) presentation reveals another theory. Namely, TBAC is primarily focused on ensuring smooth functioning of the Treasury market.

For example, the second quarter 2021 TBAC Charge focuses on “Treasury Market Functioning”. Fair enough, especially given the obvious failures in March of 2020. It states as its charge:

Treasury market liquidity has, at times, been strained during recent episodes of broader market stress. What lessons have been learned in recent years regarding Treasury market structure and vulnerabilities in the non-bank financial sector, and what efforts should be considered to improve market functioning and reduce the need for public sector interventions during future episodes of heightened uncertainty?

Hmmm. This sounds a lot more like a concerted effort to shore up demonstrated weaknesses than a devious plot to artificially boost liquidity and exacerbate inequality.

The report goes on to address considerations such as “Liquidity within the UST complex can vary; on the runs tend to retain liquidity better”, “Opportunistic players provide a valuable source of demand through cash/futures or broader relative value arbitrage, but quick exits can be disruptive”, and “Intermediation has not kept pace with the scale of increase in the outstanding UST debt supply”. All very reasonable.

The various policy responses to be considered include “A standing repo facility”, “A standing buyback or purchase facility”, “Targeted bank regulatory changes (mainly SLR)”, “Mandated central clearing”, “All-to-all trading”, and improved “data collection and disclosure”. Again, all very reasonable.

By actually reading through the TBAC presentations, then, a very different view emerges as to the nature of the committee’s recommendations: It seems to be engaging in a fairly systematic and organized effort to resolve recognized problems in the Treasury market. This is good!

That said, the TBAC process certainly isn’t perfect. Many of the problems that arose in March 2020 were known beforehand; it didn’t have to wait for problems to occur. Further, beginning the analysis more than a year after the fact isn’t exactly a lightning response. Nonetheless, as imperfect as it may be, the TBAC process itself serves a useful purpose.

So, while there certainly are Treasury decisions that are made with political motivations, not all of them are. It is counterproductive to overgeneralize. Also, the TBAC presentations not only provide insights into the funding process, but they also provide insights into policy development. If you wonder where various policies come from, you can often find their origins in TBAC reports.

Investment landscape

One of my favorite follows on Twitter is @PauloMacro, partly because he regularly posts thoughtful investment theses (along with his rationale), and partly because he often has an interesting perspective. A recent thread of his makes the case the US is sliding down the monetary drain and becoming a “banana republic”.

So it really all boils down to: do you think the US is a banana republic, or have legislators addressed the outrageous deficits (both current and projected) to your satisfaction? You all know where I stand…until a credible approach is taken to rein this insanity in - tchau!

The basic idea is there is no fiscal discipline in the US (just like banana republics) and as a result, the US is rapidly descending into a highly inflationary environment. Whereas yield curves in developed markets uninvert “thru 2s rallying”, in emerging markets curves uninvert “via long end selloffs”. Since he expects the US to become an emerging market, he expects long-term bonds to sell off (and yields to go up).

I find this especially interesting because I agree with the conclusion but not the rationale. I do think US Treasury bond yields will continue to go up. But I don’t view it as a sign of the unraveling of US financial stature. Rather, as I mentioned in the second quarter market review, I view the move higher in bond yields as one plank in a broader strategy to (eventually) pull debt down through financial repression. Eventually, that repression is likely to cause the dollar to decline, but not any time soon.

To be sure, my views on the US fiscal situation and by association, the US dollar (USD), have evolved. It is hard to look at the fiscal deficits and the politics and not see it as a disaster. However, and it’s a big however, as bad as the USD may look, it is still not worse than any other fiat currency - by a long shot. The vast natural resource and geographic assets of the US, its vastly superior military strength, and its unrivaled bond market, among others, confer advantages to the US that no other country, or currency, has.

What I find so interesting about this juxtaposition of hypotheses and worldviews is they differ mainly due to differences in interpretation. Part of this is politics probably, and part may be cultural. The main point, though, is there is no discernable difference in accepted facts.

So, one takeaway is I could be wrong - and the USD could unravel shortly. This would be extremely painful and the possibility should not be dismissed out of hand.

USD doesn’t need to unravel for longer-term rates to go up, though. Another possibility is we are both right - for a while. A critical mass of traders start betting USD will decline and do so partly by selling/shorting longer-term Treasuries. In this case, long-term yields will still rise. As a result, two different points of view end up with the same conclusion: longer-term rates are going up.

Investment strategy

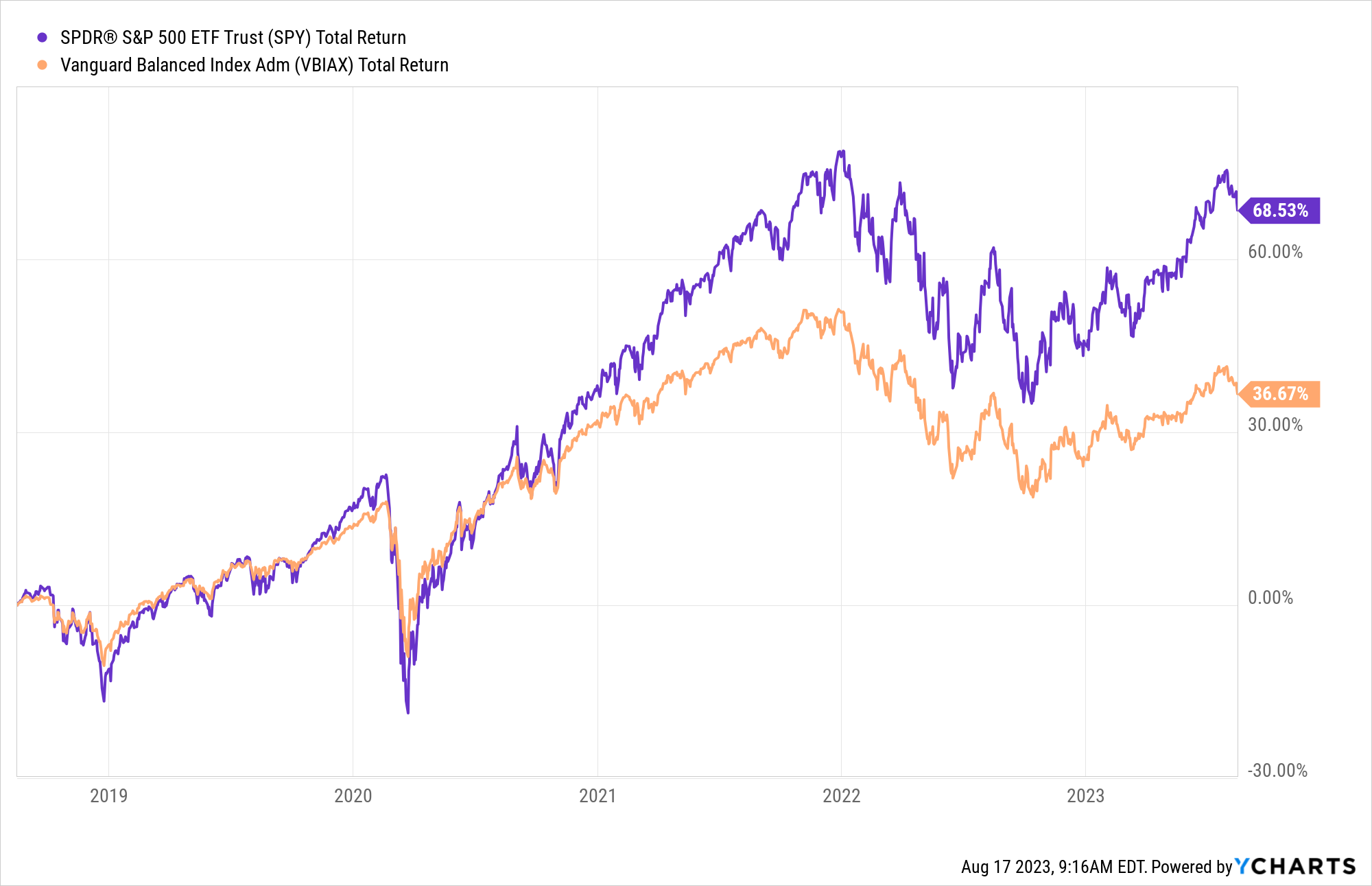

The default investment strategy for a large proportion of retirement funds is some take on the 60/40 stock/bond portfolio, which includes “balanced” funds and target date funds. The basic idea is bonds cushion the higher volatility of stocks to provide smoother returns and less dramatic drawdowns.

The basic formulation worked in spades for over forty years, but not so much because of diversification benefits, but because both stocks and bonds benefited from the extended decline in interest rates. While this period stands out as an aberration from the rest of financial history, it is the formative experience of most investors today. As a result, it is an appropriate time to highlight some of the increasingly visible problems with the 60/40 strategy as an appropriate one for the next forty years.

The first thing to notice on the graph above is that through the pandemic, stocks and bonds moved together. Since late 2020/early 2021, however, bonds have been dragging down the performance of the balanced fund relative to stocks only. Another thing to notice is over that period, the balanced fund has done basically nothing. By the way, this unexceptional performance has also been boosted by stocks which nearly returned to all-time highs.

A major point is things have changed with the emergence of inflation. Not only does a balanced fund get hurt by inflation, both of the major assets - stocks and bonds - get hit by inflation. Unless you believe inflation has gone away for good, which I happen to think is a terrible bet, the balanced portfolio is uniquely exposed to a great deal of downside risk. Bonds have taken the biggest hit thus far, but there is plenty of risk in both assets.

Implications

When confronted with the expectation that balanced funds could face significant headwinds, investors and advisors often respond by asking what can be done to diversify. While this makes some sense, it is also extremely misleading.

It is misleading partly because it assumes stocks and bonds should remain the anchor assets of the portfolio. In many cases this is not true. With current stock valuations implying long-term returns below zero and with the prospect of inflation slicing expected bond returns, neither stocks nor bonds look attractive for long-term investors right now.

It is also misleading to presume there are a couple of asset classes like real estate or high yield, or more exotic assets like private equity or venture capital, which can diversify away any turbulence. Mostly these other assets classes are just as affected by interest rates, growth, and inflation as stocks and bonds are. Over longer periods of time, these assets move very much in line with stocks and bonds.

As a result, the current challenge to long-term investment portfolio requires more than just a little diversifying tweak; it requires a major philosophical re-think of what drives asset returns. Part of that answer involves searching further afield than many investors are comfortable with to things like gold and commodity trading advisors (CTAs). Part of the answer also involves simply avoiding the onslaught coming to the core assets of stocks and bonds by holding short-term Treasuries.

Note

Sources marked with ($) are restricted by a paywall or in some other way. Sources not marked are not restricted and therefore widely accessible.

Disclosures

This commentary is designed to provide information which may be useful to investors in general and should not be taken as investment advice. It has been prepared without regard to any individual’s or organization's particular financial circumstances. As a result, any action you may take as a result of information contained on this commentary is ultimately your own responsibility. Areté will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Some statements may be forward-looking. Forward-looking statements and other views expressed herein are as of the date such information was originally posted. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Areté disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities. Past performance is not a guarantee of future results. Areté is not responsible for any third-party content that may be accessed through this commentary.

This material may not be reproduced in whole or in part without the express written permission of Areté Asset Management.